It’s fair to say that Industry Super Australia (ISA) has a vested interest in raising the superannuation guarantee (SG) from the current 9.5% to 12%, since this would result in more funds under management to ‘clip-the-ticket’ on, and more fee revenue.

This vested interest helps to explain why ISA’s chief economist, Stephen Anthony, has put forward more flimsy arguments in favour of raising the SG:

…the SG is said by some to retard growth and living standards by leaving lower-paid Australians worse off. The irony in that argument is that working Australians in the aggregate have not been receiving “productivity” wages for a decade.

In an era when labour productivity is not feeding through to real wages (which once was automatic), employers have the capability to pay SG while not impacting wage increases…

Those who are against an increase in the SG claim that growth in employees’ take-home wages today will be offset by close to the full amount of the SG rise. Given the complexity of the labour market (and the myriad interactions and wage-setting mechanisms it involves), such an argument is broad and simplistic.

There is also no guarantee that there will be a wage rise if the SG does not go up. Recent history shows us employers have not been returning labour productivity gains to employees, with wages only rising with the CPI. The critics of the SG haven’t explained the transmission mechanism for how a full pass-through of productivity will occur (either to catch up for a lost decade or in the future).

Thinking about the macroeconomics, there must be a theoretical upper limit to SG contributions, but that number is higher than 9.5 per cent, based on how many Australians are still relying on the aged pension to some extent.

Provided that the superannuation system is efficiently converting deferred wages into an adequate stream of retirement income, that number could be well north of 12 per cent, even as high as 15 per cent as was originally envisaged by the system’s architects…

So, the clear-cut lesson is that the SG needs to be higher than it is now.

Stephen Anthony’s arguments around wages do not make sense.

Employers only care about their overall wage cost and don’t care what proportion of their wage bill is paid directly to workers or into a superannuation account. The cost to them is the same regardless.

Moreover, while real wages have stagnated, nominal wages have in fact risen by 14% over the past six years. Raising the superannuation guarantee from 9.5% to 12% (or even 15% as championed by ISA) would simply ensure that nominal wages grow by less than they otherwise would, with the difference going into workers’ superannuation accounts.

This wage trade-off is non-controversial and has been documented by the Henry Tax Review, the Grattan Institute, the Parliamentary Budget Office, among other places (see yesterday’s post).

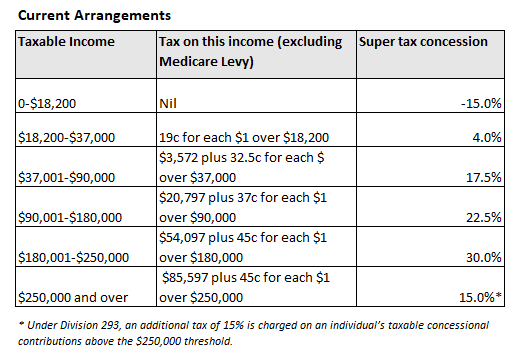

Second, Anthony conveniently fails to mention that the way superannuation concessions are structured is highly inequitable and is set up to harm lower income earners.

This is because the flat 15% tax on contributions and earnings ensures that those on lower incomes receive minimal concessions (or are penalised), whereas those on higher incomes receive the biggest tax breaks on contributions/earnings:

Accordingly, the Australian Treasury last month revealed that high income earners are receiving the lion’s share of benefits from Australia’s compulsory superannuation system:

Therefore, lifting the SG without first fixing the concessions system would amplify these inequalities and inefficiencies, thereby robbing lower-paid workers of take-home pay while also depriving the federal budget of much-needed tax revenue from higher-income earners.

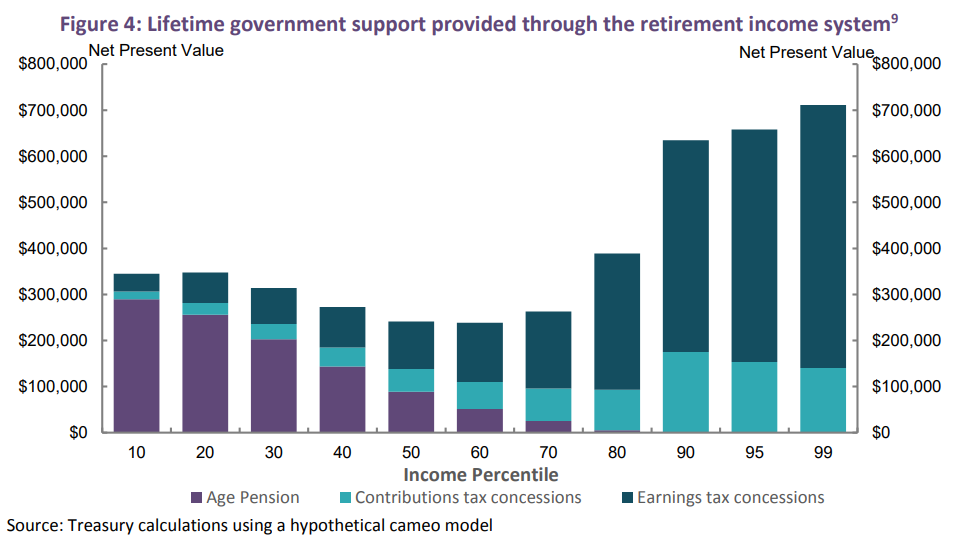

Indeed, unless the concession structure is fixed, the cost to the federal budget from further increases in the SG will exceed any cost savings from the Aged Pension:

Lifting the SG is unambiguously poor policy. Instead, focus should be placed on fixing the concession structure, as well as ensuring the existing system works equitably and efficiently.