The Australian’s Adam Creighton has penned an excellent article attacking the Morrison Government’s decision to exclude the ‘family home’ from being considered in the upcoming retirement incomes review:

Treasurer Josh Frydenberg ruled out “ever” including the principal residence in the eligibility test for the pension.

If the age pension is going to be means tested, then the “family home’’ must be included.

How can people respect the social security system when a pensioner in a Toorak mansion, clearly with vastly greater resources, is treated the same as one in a fibro in Sydney’s Bankstown.

No one should ever be forced to move but if a pensioners’ total assets (housing and financial) exceed some high bar, say $2m, then surely any age pension payments should be deducted from the ultimate inheritance.

A $2m tax free inheritance might become, say, $1.9m.

Oh the horror!…

Today the pension is as much about subsidising inheritances as alleviating poverty.

Creighton is spot on. And there is a wide range of commentators that have recommended including one’s principal place of residence in the assets test for the Aged Pension, including the Productivity Commission, The Grattan Institute, The ACCI, The CIS, and Professor Kevin Davis.

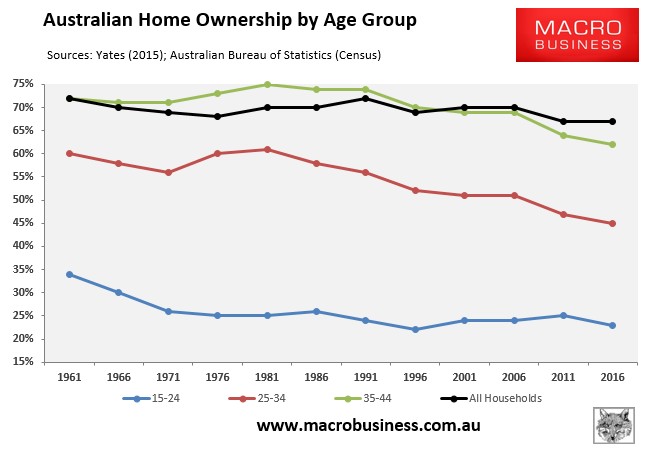

Indeed, Australia’s current retirement system is based on the presumption that most people will own their homes. But that assumption is running face first into the falling rates of home ownership rates among younger Australians, who will become future retirees:

Therefore, in addition to lowering the system-wide cost of housing through a combination of reforms, the Aged Pension system needs to be transformed to make it more neutral between owning a home and renting.

The solution I have espoused many times is to:

- Include one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2022), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Raise the overall pension asset test threshold as well as the base rate.

- Extend the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HECS-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under such a plan, asset rich pensioners choosing to remain in place could continue to receive an income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers. But they would similarly be incentivised to move as the family home would no longer be viewed as a tax free shelter. Renting pensioners would also be made significantly better-off via the combination of a higher asset test threshold and a higher pension base rate.

The May 2018 Budget addressed the third point by extending the Pension Loans Scheme, but it did not touch the other two areas, which is vital if the system is to be made more neutral towards home owner retirees and renting retirees.

One wonders how long this issue can continue to be ignored given the collapse in home ownership and the rise in renters.