Last month, research director at the Australian Centre for Financial Studies, Professor Kevin Davis, called for one’s principal place of residence to be included in the assets test for the Aged Pension.

In doing so, Davis joined a bunch of diverse groups that have called for reform, including the Productivity Commission, The Grattan Institute, The ACCI, and the The CIS. MB has, of course, also lobbied hard for reform of the pension assets test over the past three years.

In its pre-Budget submission, the ACCI has once again urged the Turnbull Government to include the family home in the pension assets test, arguing that it is essential for improving Budget sustainability. From The Australian:

Its budget submission says people older than 65 have almost $1 trillion in equity in their homes, which should be used to defray the costs of retirement.

It says the value of a home in excess of a threshold of about $450,000 could either be used in the Age Pension means test or to secure an interest-free loan to cover living costs for the first five years after becoming eligible for the pension. The loan would be recouped when the property was sold, either on death of the owners or their shift into aged care.

“Paying taxes throughout life does not entitle citizens to a government-funded pension regardless of financial circumstances,” the business group says. “Taxes pay for government services in the year they are collected.”

The group says the pension age should be reviewed every three to five years and shifted higher, in line with increasing life expectancy.

The ACCI’s prescription is similar to the approach long championed by MB, although we also believe that some of the Budget savings should be used to increase the overall assets test and base rate as well. Our specific plan is to:

- Include one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Once implemented, raise the overall assets test for the Aged Pension, as well as the base rate.

- Extend the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HELP-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under MB’s plan, house-rich pensioners could continue to receive a regular income stream as they do now under the Aged Pension, but with less drain on the Budget.

Younger taxpayers will benefit from not having to spend as much to fund wealthy retirees via their taxes.

Meanwhile, poorer renting pensioners, and those without significant assets, would receive greater financial assistance than they do currently.

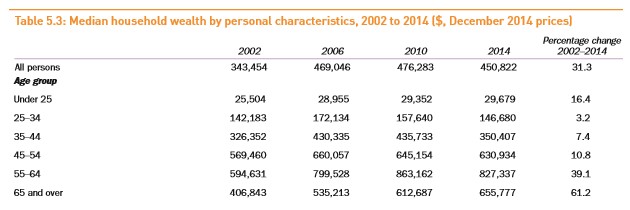

The last point about poorer renting pensioners being made better-off is important. It is true that around three-quarters of retirees own their homes (most outright) and many have enjoyed massive windfall gains in wealth, thanks to the mammoth surge in Australian home values over the past 20 years:

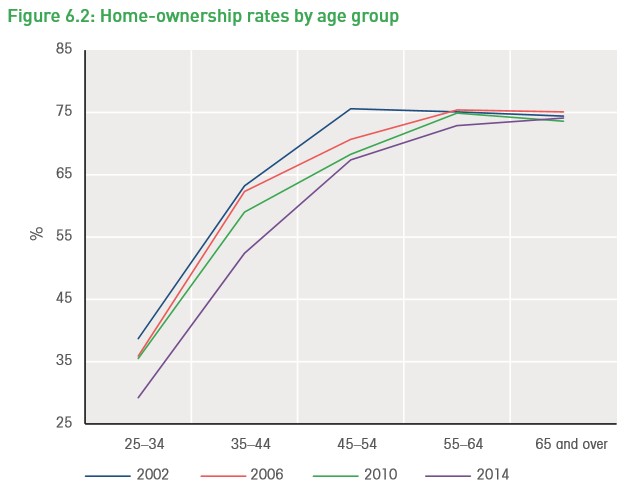

It is also true that this surge in retiree housing wealth has come at the direct expense of younger Australians, whose wealth has barely increased, and who are now either locked-out of housing altogether or are required to undergo a lifetime of debt servitude in order to pay off a home:

However, a quarter of pensioners have missed-out on this wealth boom and are doing it tough. The below article published over the weekend in Starts at 60 explains:

Professor Peter Phibbs, a housing specialist at the University of Sydney, says the stratospheric cost of buying housing has helped push up rental costs, leaving many renters on the Age Pension “doing it tough” because they have no way of increasing their income to cover rising costs.

“They’re paying the rent and utilities and whatever they have left over, they live on, and if they get an unexpected bill, they just eat less,” he says. “There’s no leeway”…

Fiona York, co-manager of the Melbourne-based Housing for the Aged Action Group (HAAG), says research shows Age Pensioners in the private rental market spend about 70 percent of their pension payments on rent.

“There’s a myth going round that all older people are homeowners,” she says, noting that between the 2006 and 2011 censuses, there was in fact a 44 percent jump in the number of renters aged over 55…

Phibbs warns that the issue of older renters doing it tough isn’t going to go away.

“There’s going to be increasing numbers of older renters,” he says, as sky-high house prices lock more and more of today’s workers out of the property market.

Research released by Victoria’s Swinburne University of Technology in October shows there are 425,000 over-50s renters in Australia, with the number expected to rise to 600,000 by 2030 and to 830,000 by 2050, and that those people tend to have little personal wealth.

Clearly, including one’s principle place of residence in the assets test, along with increasing the overall assets test threshold and base rate for the pension, are essential reforms to make the Aged Pension fairer to both younger and poorer older Australians doing it tough, while also improving the long-term sustainability of the Budget.

Let’s hope all sides of politics embrace reform.