CBA’s senior economist, Gareth Aird, has published a new report on the explosive growth of international education exports, which are “booming” and “continue to grow at a remarkable rate”:

Overview

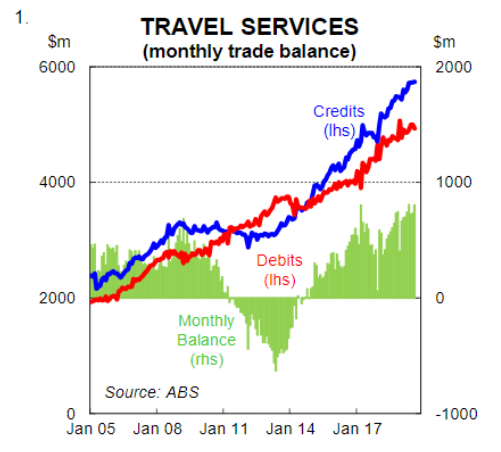

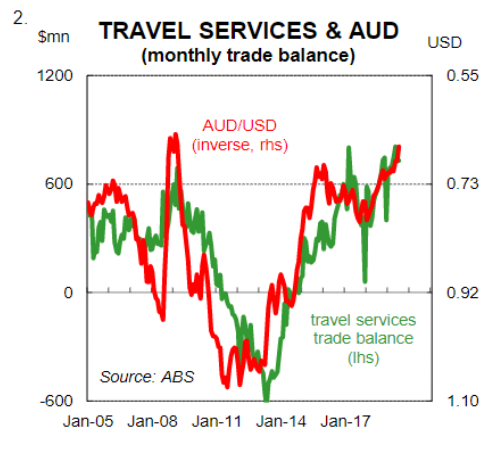

The improvement in Australia’s external position has been quite profound. Australia is now posting very large monthly trade surpluses and in Q2 19 a current account surplus was recorded for the first time since 1975. Rising commodity export volumes coupled with a lift in the terms-of-trade have been the primary driver of the big trade surpluses. But services exports have also played a supporting role. More specifically, the travel services trade balance, (which is essentially money spent by foreigners in Australia in some capacity less money Australian’s have spent offshore)has steadily increased at the same time as the Australian dollar has depreciated (charts 1& 2).The monthly travel services trade surplus is currently running at approx. $750 million.

In this note we look at recent trends in Australia’s services exports. Our focus is on travel services and the recent trends in tourism and education exports.

Services sector exports and the importance of travel services

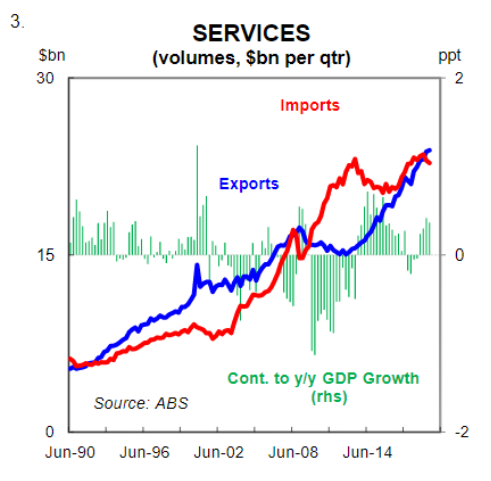

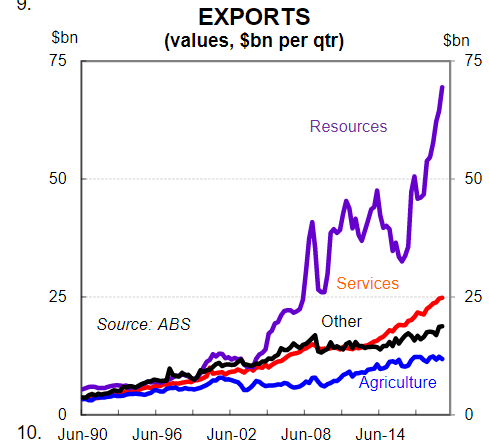

The Australian tradables services sector broadly comprises three groups: travel services (which are mainly tourism and education-related), transport and business services. The latest national accounts indicate that services exports were worth around 20%of total exports in Q2 19. In the year to Q219, services exports totalled $96.9bn (equivalent to 5% of GDP).

Services sector exports come largely from Australia’s two biggest states, NSW and Victoria. This is in contrast to hard commodity exports which primarily come from the resource-rich states of WA and QLD.

Data on services exports is published by the ABS both monthly and quarterly (in the International Trade in Goods and Services and Balance of Payments releases respectively). But the level of detail differs between the two publications. In the monthly trade data there is no split between education and tourism exports. As a result, we focus from here on the quarterly data. But we note that the higher frequency monthly trade data suggests that tourism and education net exports will make a positive contribution of around $2.3bn to the Q3 19 current account.

Travel services explained

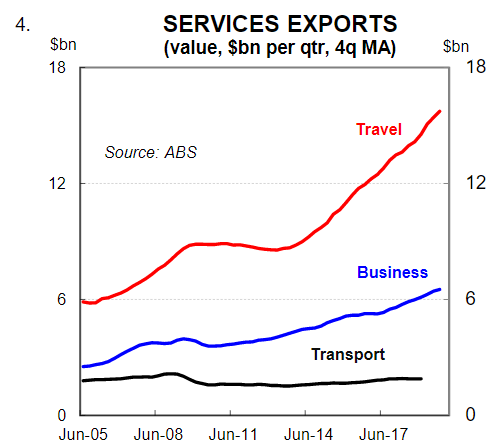

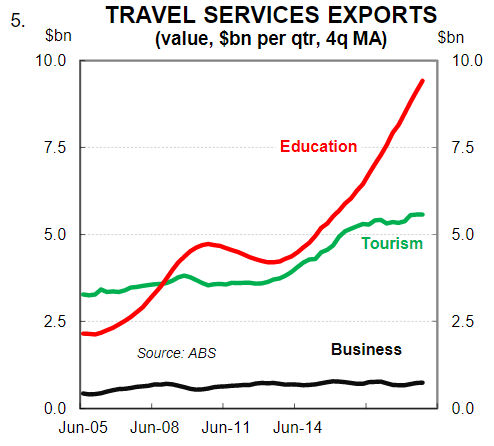

Travel services exports (as measured by the ABS) are an estimate of all of the spending by foreigners on goods and services while they are in Australia(e.g. retail, accommodation, recreation, transport). The three main components of travel services are education and tourism (i.e. personal travel) and business travel. Travel services make up the bulk of services sector exports. Andthey have been the primary driver of the improvement in services sector net exports (charts 4& 5). We cover the education and tourism export components below.

Education:

Education exports measure the total expenditure of overseas students who are studying in Australia (i.e. not simply tuition fees which is important distinction). They are, put simply, booming. There has been incredibly strong growth in the number of overseas students studying in Australia and this has generated a large lift in the recorded value of education-related services exports. In the year to Q2 19, education exports were worth approximately 40% of total services exports. On the league table, this makes education Australia’s fourth largest export after iron ore, coal and LNG.

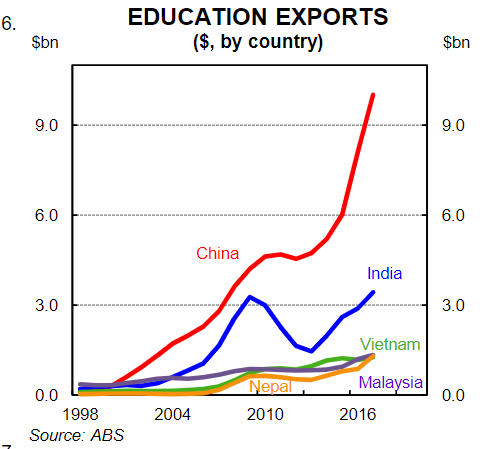

Education exports to China are larger than to any other country (charts 6 & 7). In 2018, Chinese students accounted for a third of the expenditure of students studying in Australia –a record high share. This was substantially more than the next largest group (students from India, representing 13% of total expenditure by students).

Around half of international students are enrolled in higher education (largely universities). A little over a quarter are enrolled in vocational study. And ~20% are enrolled in English Language Intensive Courses for Overseas Students (ELICOS) and non-award studies. The bulk of international students are concentrated in NSW and Victoria, particularly Sydney and Melbourne.

This big increase in overseas students studying in Australia has increased demand for accommodation. And it has added to the supply of labour since most overseas students are eligible to work. Indeed education exports are one channel in which the permanent population of Australia increases. That is, a significant proportion of overseas students who arrive on temporary student visas go on to become permanent residents (see here).

According to the Australian Government, of 1.6 million overseas students (from all education sectors) granted a visa between 2000/01 and 2013/14, 16% transitioned to a permanent residency visa at some stage after arriving in Australia. This figure, however, understates the true proportion of international students who become permanent residents because it excludes international students who transition to another temporary visa before gaining a permanent residency.

According to the Parliament of Australia, “given the increasing number of Temporary Graduate visas it is likely more people are transitioning from a student visa to a different category of temporary visa and then gaining a permanent residency visa. There is no publicly available data on this group of people.”

Tourism

Tourism services exports essentially capture the income that the Australian economy generates directly from overseas holidaymakers visiting and consuming in Australia. It is the income that the economy receives from both the sale of goods and services to overseas holidaymakers in Australia.

Over the past year tourism exports have continued to rise, but the rate of growth has eased. The total money spent in Australia from overseas residents having a holiday in Australia rose by 4.6% (or $1bn) in 2018/19.

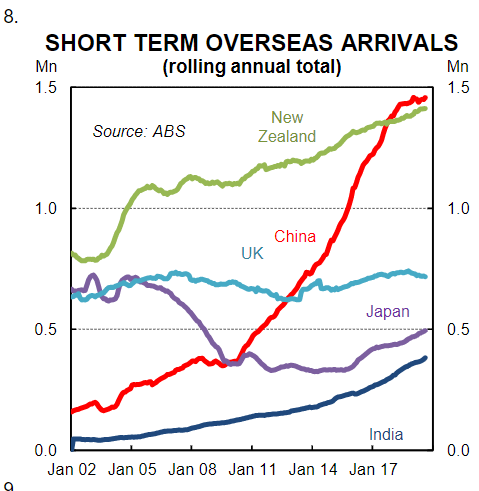

Whilst tourists from China continue to lift in absolute terms, the growth rate has slowed. In the year to July, the number of short-term arrivals from China to Australia had risen to 1.45m (compared with 1.439m over the corresponding period a year earlier –a lift of 1.4%). It’s difficult to ascertain why growth in Chinese arrivals has slowed so materially.

In contrast, growth in the number of short-term arrivals from India continues to rise strongly (chart 8). This is a structural story. India is projected to overtake China as the world’s most populous nation within a decade. And as incomes rise, overseas travel will increasingly become part of the consumer spend.

The direct impact from a lift in tourism exports is measured in the ABS Balance of Payments. But there are also second round impacts. Employment multipliers for sectors exposed to tourism like retail (10.17)and accommodation (7.86) tend to be higher than most industries (CBA puts the average FTE employment multiplier at 6.35).

Outlook

The short term outlook for tourism exports in Australia will essentially be driven by the level of the Australian dollar and the global business cycle. The slowdown in global growth is probably already having a dampening impact on the local tourism sector. But to date that has been partially offset by a weaker AUD. Our working assumption is that tourism exports continue to growth, but the rate of growth over the next year will be less than the average of the past few years without a further depreciation of the exchange rate which is not our expectation.

If growth in arrivals slows then growth in tourism-related investment will also ease. According to Austrade’s Tourism Investment Pipeline 2017/18 (latest available), the investment pipeline held 213 projects valued at $44.0bn–a $6.2bn increase compared to the 2016–17 pipeline. The Tourism Investment Pipeline is an annual publication and is generally released in October which means the 2018/19 report should be forthcoming.

The outlook for education exports is a little more complicated. The extent to which Australia has grown its education exports is nothing short of phenomenal. But there are capacity constraints. International students per head of population are already incredibly high in Australia and it is unlikely that enrolments can continue to grow at their recent rates without Universities encountering supply side issues. Policymakers also need to ensure that domestic students are not ‘crowded out’ and that standards of education are not comprised. Our Universities are generally ranked well on global league tables and it’s paramount that good reputations are preserved. So the right balance needs to be struck. On a more general note, big swings in commodity prices will remain the dominant driver of the trade balance and the terms-of-trade given resource exports are worth more than half of our total exports (chart 9). And as we covered last week, we see Australia’s key commodity prices moving lower from here which means that growth in export receipts will slow (see here).

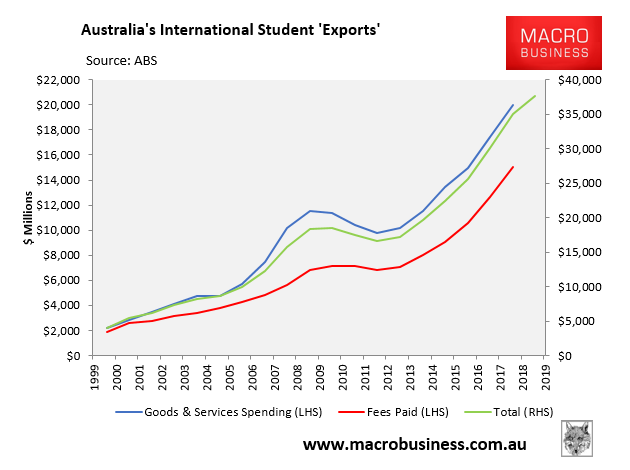

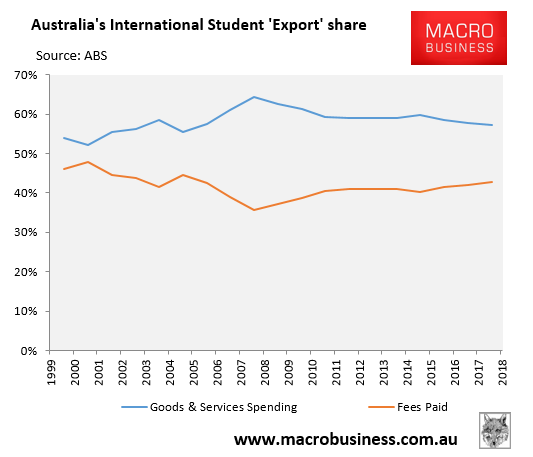

One thing that needs to be emphasised is that Australia’s education exports are overstated, since they include both tuition fees and expenditure while studying in Australia.

The below charts derived from ABS data hammers the above point home. As you can see, spending on “goods & services” by international students ($20 billion in 2018) outweighs spending on enrolment fees ($15 billion in 2018):

Advertisement

Much of this $20 billion of spending would have been earned via paid work within Australia, which is not actually an export. Indeed, such spending is no more an ‘export’ than expenditure by domestic students living away from home that is paid for via income earned through paid employment.

Advertisement

A significant share of this spending would also have been on imported goods, which actually worsens Australia’s trade balance.

Professor Salvatore Babones’ noted similar recently in his excellent research paper for the CIS:

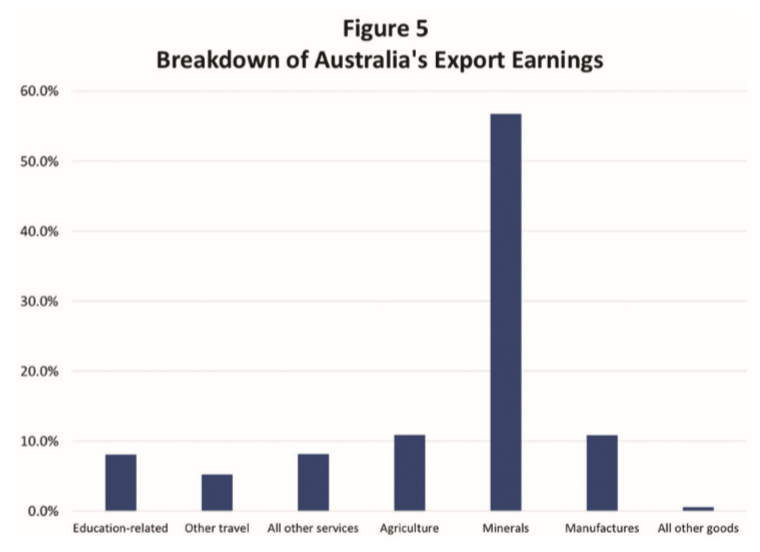

International students are clearly important for Australia’s universities, but their importance to the economy as a whole is frequently overstated. One oft-quoted statistic is that educational exports have risen to become Australia’s third-largest export after iron and coal. That doesn’t really capture the full story, since exports in different sectors are reported at different levels of granularity.

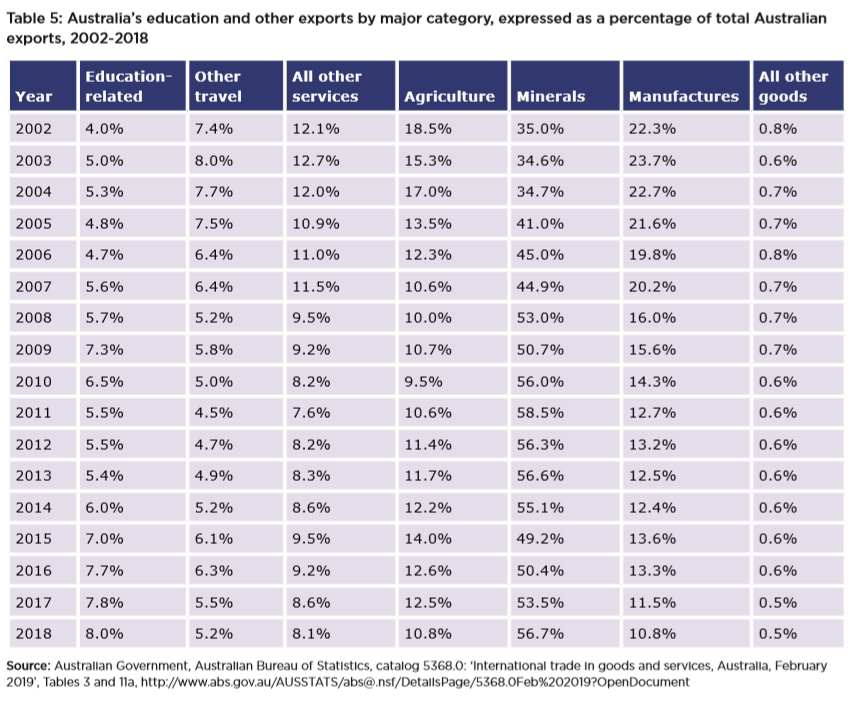

Figure 5 compares the size of Australia’s educational exports to that of other major sectors from across the economy, using data from the Australian Bureau of Statistics (ABS). Additional historical data going back to 2002 are reported in Table 5 in the Appendix. Educational exports overtook receipts from all other travel (tourism, family, and business combined) in 2008, but are still smaller than Australia’s exports of agricultural or manufactured goods. Moreover, more than half of Australia’s reported educational exports (53.7% in higher education and 57.2% for the education sector as a whole) consists not of student fees, but of goods and services bought by students while in Australia. Since this spending is at least partly generated by income that students earn from working in Australia while studying, the true net value of education exports to the Australian economy is likely lower than the headline figures reported by the ABS and DET…

Advertisement

Education exports are also likely to peak shortly, given the stiff headwinds facing Chinese, Indian and Nepalese students – Australia’s three biggest sources (see here and here).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.