The superannuation industry continues to white-ant the announced retirement incomes review, claiming that abandoning the legislated increase in the superannuation guarantee (compulsory superannuation) would raise our taxes:

“There’s two significant debates going on. The first is whether super should be compulsory or optional, and the second is whether the [amount of super] that employers pay on top of your wages should be frozen,” [Industry Super Australia (ISA) chief executive Bernie Dean] said.

“Both of those are bad ideas. Winding back compulsory super would leave the whole country worse off, as we’d all end up paying more tax to support a flood of people fully relying on the pension.”

Employers are currently required to contribute 9.5 per cent of an employee’s salary into their superannuation fund – but current legislation will see that figure (known as the superannuation guarantee) increase 0.5 per cent a year from 2021 until 2025.

This claim is unambiguously false. In addition to lowering workers’ take-home pay, since the superannuation guarantee is paid for by workers via lower wages, compulsory superannuation tax concessions also cost the federal budget more than they save in Aged Pension costs.

This was made clear by the Henry Tax Review, which explicitly stated:

Advertisement

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

Accordingly, the Henry Tax Review explicitly recommended against raising the superannuation guarantee, also because it would lower workers’ take home pay and have a particularly adverse impact on lower-income earners:

“Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners”.

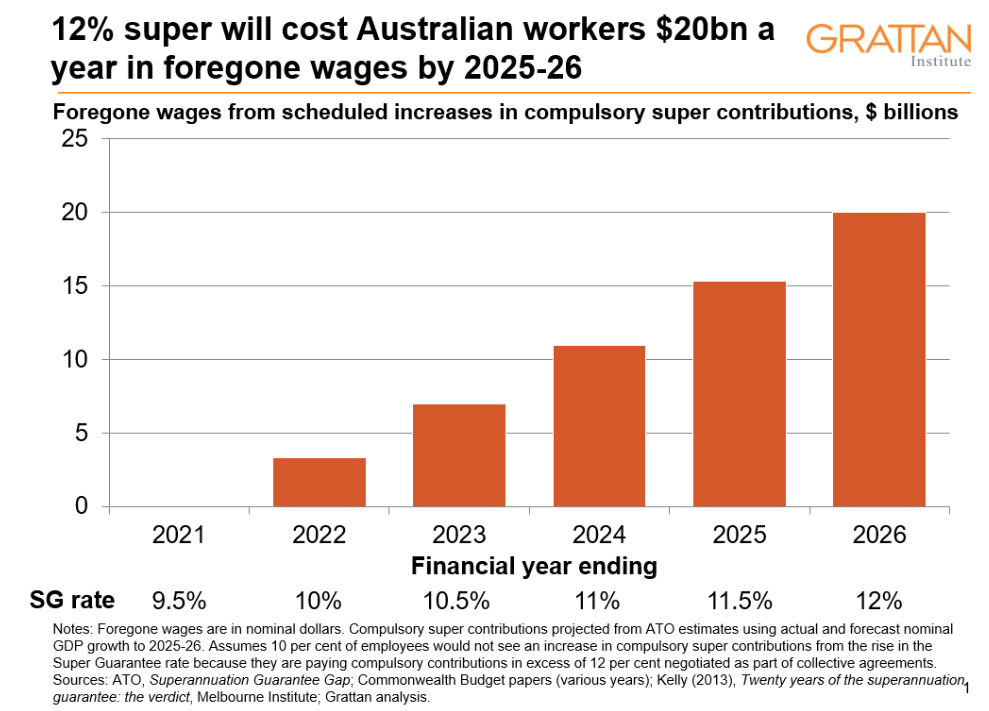

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

If compulsory super contributions go up, wages will be lower than they otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP…

[Moreover] both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments:

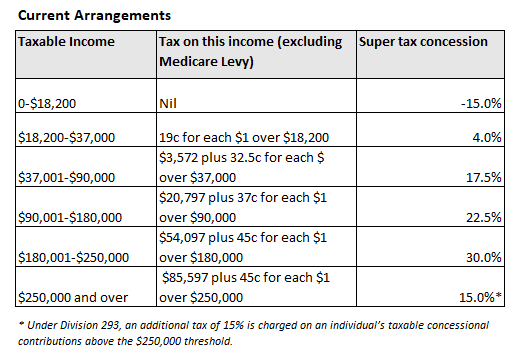

The reason why raising the superannuation guarantee would be so ineffective can be explained by Australia’s flat 15% tax on contributions and earnings. This ensures that those workers on lower incomes receive minimal concessions (or are penalised), whereas those on higher incomes receive the biggest tax concessions on contributions:

Advertisement

Raising the superannuation guarantee would merely heighten inequities already present in the system. It would rob younger (and lower paid) workers of much-needed disposable income and worsen the long-term sustainability of the Budget.

About the only winners from such a policy would be the superannuation industry, which would get to ‘clip the ticket’ on more funds under management and earn fatter profits. This explains their furious opposition to freezing the superannuation guarantee and their constant lies.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.