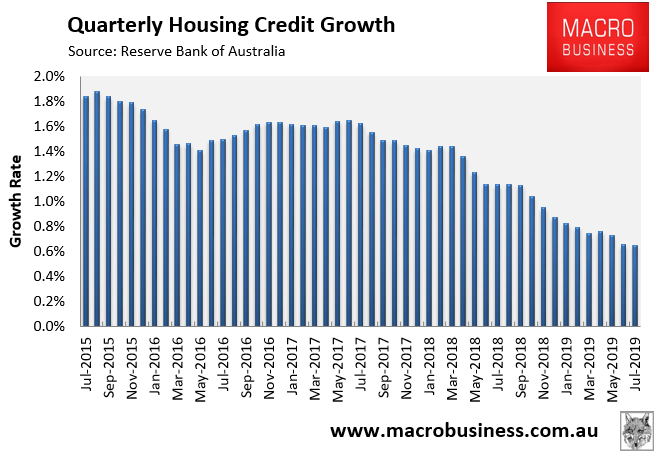

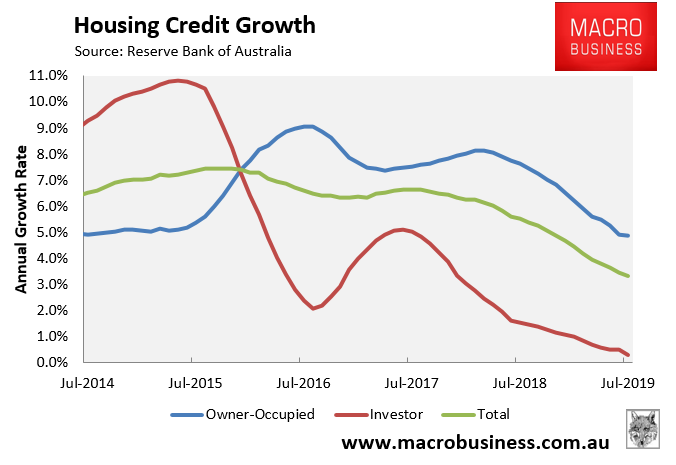

Last week’s mortgage credit data from the Reserve Bank of Australia (RBA) revealed record low mortgage growth on both a quarterly and annual basis (see below charts).

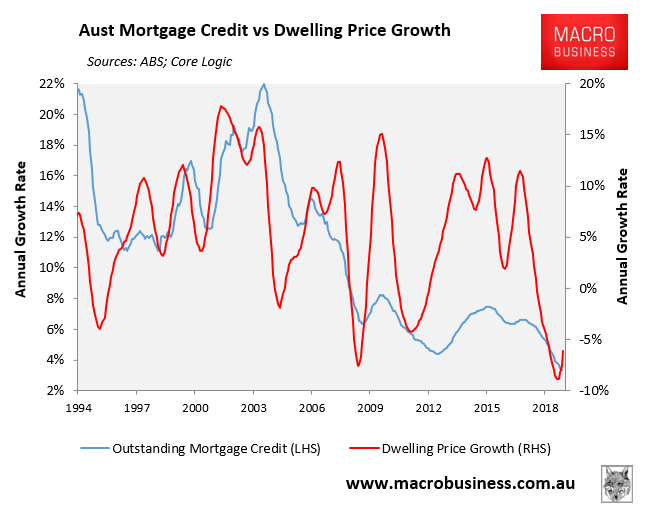

As I showed earlier this week, there is huge disconnect between mortgage growth and dwelling price growth, making mortgage growth a rather useless indicator for house prices:

I explained this disconnect as follows:

The reason why the correlation with mortgage credit is weak is because it measures two primary things: 1) the addition to the mortgage stock from new mortgages taken out by borrowers (increases the stock of debt outstanding); and 2) the repayment of mortgage debt by existing borrowers (reduces mortgage debt).

Only the first point – new mortgages created – actually impacts house prices. The second – mortgage repayments by existing borrowers – does not reflect new housing demand and does not impact prices.

Indeed, when interest rates are at record lows – as they are currently – we are likely to see mortgage repayments rise, which lowers mortgage credit growth, but doesn’t actually impact house prices. Similarly, many investors have been forced to switch from interest-only mortgages to principal and interest, meaning they are now lowering the stock of mortgage debt outstanding (other things equal) without adding to housing demand.

Yesterday, my contention was confirmed by the Herald-Sun, which noted that Australians are repaying their mortgages at record rates:

Mortgage customers are making massive inroads into their loans and optimising record-low interest rates…

Latest statistics from the nation’s largest bank, the Commonwealth Bank, found 77 per cent of customers are ahead on their loans.

And those who are in front are, on average, 35 monthly payments ahead of their scheduled repayments.

Fellow big bank National Australia Bank’s data shows 66 per cent of customers are at least one month ahead of their repayments.

On average, NAB customers are 38 months ahead of their repayments, including cash held in offset accounts linked to their loans…

NAB’s chief customer officer of consumer banking, Mike Baird, said borrowers should be optimising cheap mortgage deals by paying extra or tipping more cash into their offset account if they had one.

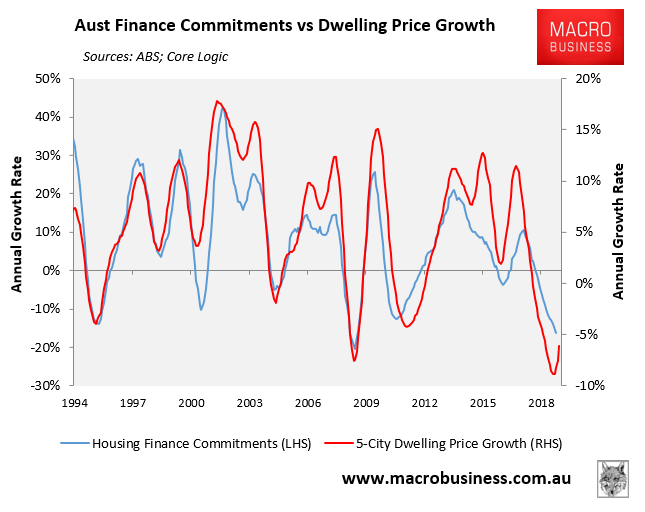

For this reason, MB prefers to look at the value of housing finance commitments (excluding refinancings) when assessing the housing market, since it only measures new mortgages and leaves out the noise generated by repayments:

As you can see, the correlation between housing finance and house prices has historically very much stronger.