Advertisement

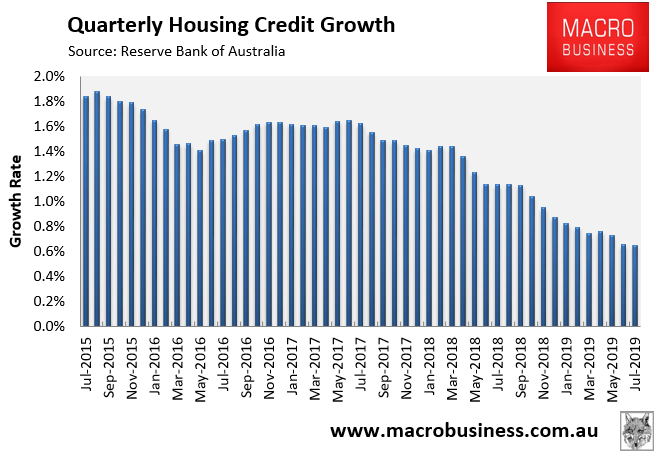

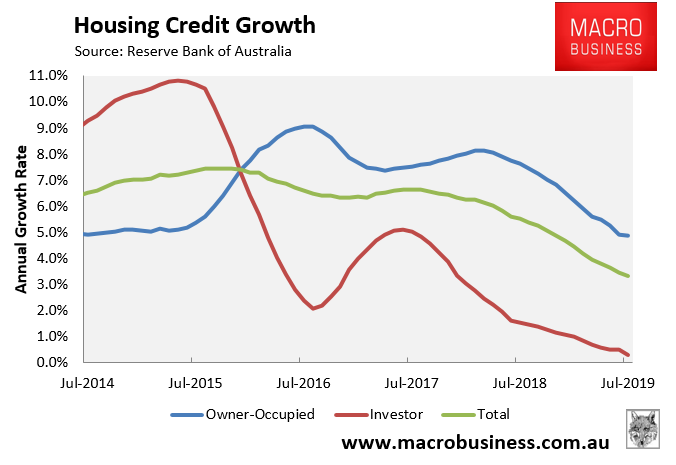

Friday’s mortgage credit data from the Reserve Bank of Australia (RBA) revealed record low mortgage growth on both a quarterly and annual basis (see below charts).

Following this post, several readers questioned how house prices can reportedly be rising when mortgage growth is crashing. Below is a sample of these comments:

Advertisement

AngryMan

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement