For years, SQM Research’s managing director, Louis Christopher, was a big supporter of negative gearing reform (see here). Then in 2016, Christopher flip-flopped, releasing an incredibly superficial report that was comprehensively debunked by Dr Gavin R Putland.

Today, Louis Christopher has updated its 2016 report, which reaches many of the same flawed conclusions. Here’s the report’s “key findings”:

Yields to Rise

International comparisons, historical precedents and the effective grossed up yield benefit all indicate that acquisition rental yields are likely to rise between 0.85% and 1.2% (85 to 120 basis points) over a two to three year period post the implementation of the new tax policy. Average acquisition yields therefore may rise from approximately 4.0% up to 5.2%. If interest rates are cut by 50 basis points, the rise in yields will be smaller, with a rise to between 65 and 95 basis points. Much would depend how much of the interest rate cut is passed on by the banks.

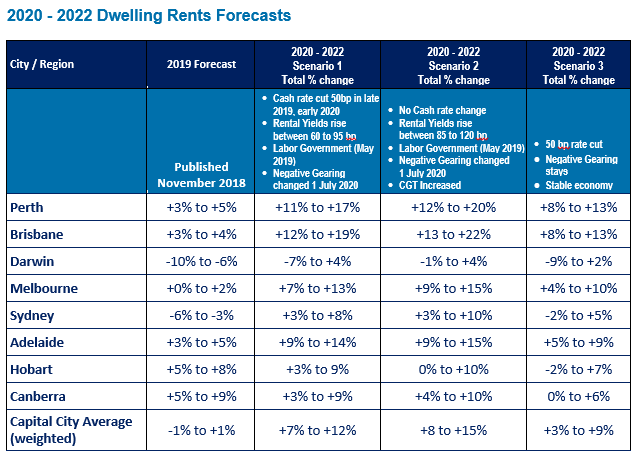

Rents to Remain Stable – Initially

Rental changes are initially likely to remain stable at -1% to +1%. However there is likely to be upward pressure from 2021 due to the current slump in building approvals which will be aggravated by the loss of negative gearing. The slump in approvals has now fallen below underlying demand requirements which may create a shortage of dwellings from late 2020.

SQM Research believes market rents could accelerate rise between 7% to 12% over the period 2020 to 2022, assuming there is an interest rate cut. Brisbane and Perth are likely to record the largest rises in rents.

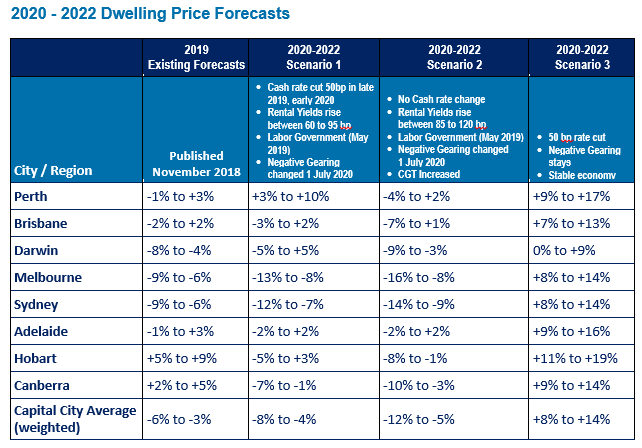

Dwelling Prices to Fall

Given the forecast of initial negligible rental growth and a rise in gross rental yields, SQM Research forecasts further price falls in the housing market over the period 2020 to 2022. There may be a brief rally in the lead up to the proposed change of negative gearing, especially if there is an interest rate cut prior to legislation passing. This would also be as a result of grandfathering opportunities and, potentially a mild loosening of the current lending restrictions by the banks.

Thereafter, dwelling prices would likely fall again due to a rapid decline in investor demand.

Sales Turnover and Stamp Duty Revenue to Fall

Advertisement

Property sales turnover is predicted to fall another 8% to 15% from 2019 levels with most of the declines in sales to occur in calendar 2020. This would result in a fall in aggregate state stamp duty revenue of $2.3 billion dollars.

Build-to-Rent Schemes will increase

With the housing market potentially trading at a higher gross rental yield, we anticipate an increase in interest in the housing market by financial institutions, particularly industry super funds who will invest via build-to-rent schemes. This is a concept that has had some success in improving rental affordability overseas and could be useful for improving long term affordability in Australia.

Off-the-plan Investors at Risk

Investors seeking to benefit from negative gearing remaining on new properties/off-the-plan developments are exposed to a substantial risk of their property being valued below purchase price, especially if the investor is seeking to sell their investment within the first three years.

Comments

Managing Director of SQM Research, Louis Christopher, said “In short, if Labor’s Negative Gearing policy is legislated in its current form, we expect a rise in rental yields which will occur through a combination of additional falling dwelling prices and, eventually, a rise in rents.

Our analysis suggests the market impact would last by around three years. There is, right now increased consensus that the RBA may have to cut rates this year. If we were to see a cut of say 50 basis points, this would provide some cushion to the effects of Negative gearing changes. Even so, the market would still record dwelling price falls. Housing construction; already in a slump, would likely fall further due to the lack of investor demand. This would set up a shortage of housing come later 2020, based on current strong population growth rates.

Such a tax change during a housing downturn is in our opinion a risky move for the economy and so we encourage discussion of perhaps a phase in period for such legislation that would reduce the economic shock that this tax change could create.

Once again, strongly encourage Labor to consider some of the investor issues, particularly surrounding the distortion their policy may create on pricing of off-the-plan developments and the likely losses investors in those properties would face come resale time to those who won’t have the tax concession.

While we take the view that negative gearing reform is a good thing over the long term, such reform should be executed as part of a wider property tax reform that should be phased in over time.”

So basically, property prices and dwelling construction will be higher and rents will be lower under a Coalition Government (Scenario 3).

While SQM’s assertion about dwelling values falling and rental yields rising is fair (although its price forecasts are a bit extreme), its claim that Labor’s policy would drive rents-up and push dwelling construction down is flat-out ridiculous.

Advertisement

As we all know, Labor’s policy will redirect negative gearing tax benefits into newly constructed dwellings, which would make new dwellings relatively more attractive to would-be investors, thereby helping to increase construction and lower rents (other things equal).

Curiously, SQM has ignored this fact and instead argued that “housing construction… would likely fall further due to the lack of investor demand” because of “the likely losses investors in those properties would face come resale time to those who won’t have the tax concession”.

SQM directly contradicts itself here. While it argues on the one hand that investors would avoid new dwellings for fear of having to sell at a loss, it simultaneouly argues that “there may be a brief rally in the lead up to the proposed change of negative gearing… as a result of grandfathering opportunities”.

Advertisement

If investors will supposedly be scared away from new properties because they won’t be able to re-sell them to negative-gearers, why would they rush to buy established properties before the policy change given they won’t be able to re-sell the right to claim negative gearing afterwards?

In any event, several commentators and builders have recently admitted that Labor’s negative gearing for new-builds policy will boost dwelling construction (other things equal), thereby lowering rents.

“Our sense is that the relative attractiveness of new dwelling investment compared to investment in established dwellings should be a positive, at least at the margin, for new dwelling construction”.

“Our business will rip… We’re all about new product… If the investors are going to participate in the market like they have in the past, that means they’re all pointing at our product and other developers’ products”…

Of course, this is precisely the stated objective of Labor’s policy: to put taxpayer subsidies to work to boost supply and lower both prices and rents.

Advertisement

What Really Happened Between 1985 and 1987?

The most questionable section of SQM Research’s report relates to its re-writing of history regarding the temporary abolition of negative gearing between 1985 and 1987. This, of course, was completely different to Labor’s policy, since it didn’t maintain negative gearing for new homes.

Nevertheless, SQM claims the complete abolition of negative gearing between 1985 and 1987 caused rents to rise:

Advertisement

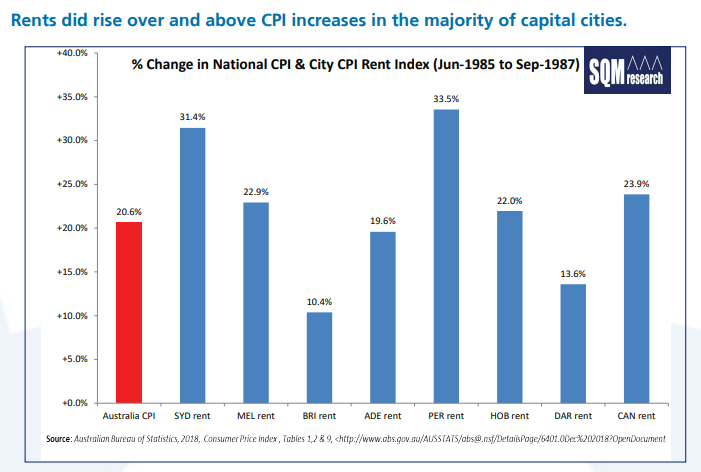

According the Australian Bureau of Statistics Consumer Price Index Table Sydney rents rose by 31.9%, Melbourne rose by 22.9%. Perth rose the most by 33.5%. In all, five of the eight capital cities rose by more than the CPI increases over the period Negative Gearing was repealed.

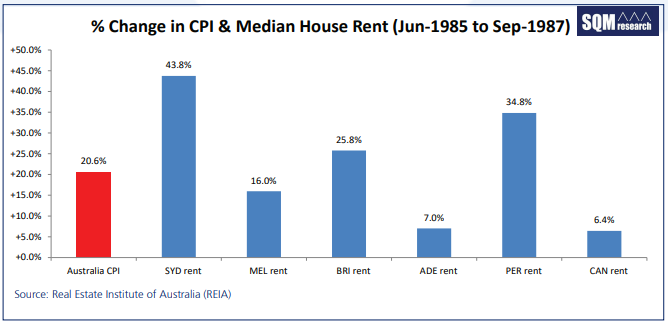

Additional evidence from the Real Estate Institute of Australia (REIA) suggests that rents for houses recorded rampant increases over the period. The REIA records that rents for 3-bedroom houses in Sydney, rose by 43% over the period June 1985 to September 1987.

And it caused dwelling construction to fall:

Housing Commencements Fell in all States

The average decline was 23.7%. The Northern Territory recorded the largest decline, falling by 47%. NSW fell by 30.2%. Victoria fell by 29.9%. Queensland fell by 12.9%.

The large declines in commencements reduced new supply relative to underlying demand. This would have directly attributed to the large rises in rents over the same period.

Leading to the below conclusion:

Advertisement

There was an impact on the housing market as a result of the repeal of Negative Gearing between 1985 and 1987. This was reflected in a sharp decline in commencements, a rise in rents for the majority of capital cities over and above CPI, a fall in sales turnover, a rise in rental yields and a fall in housing finance approvals.

Again, this is incredibly superficial analysis that is easily debunked.

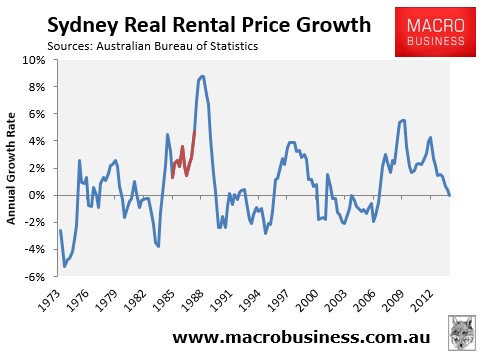

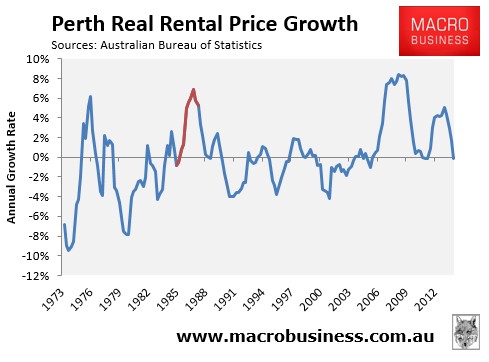

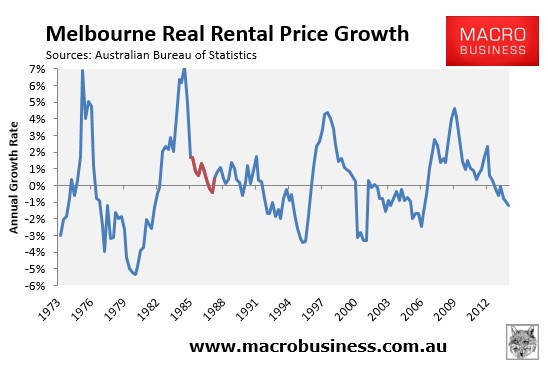

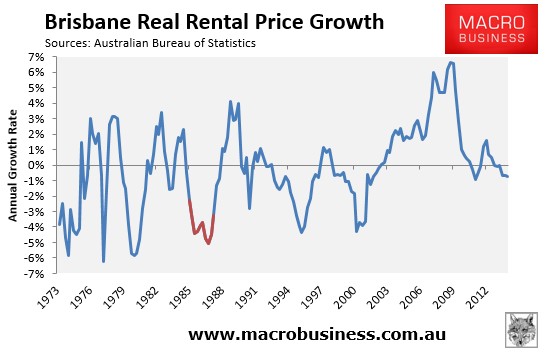

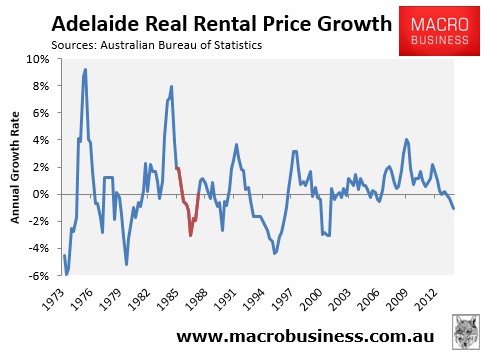

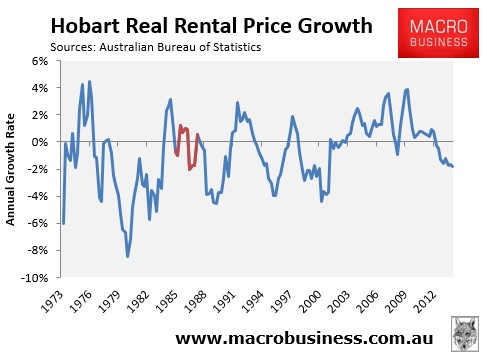

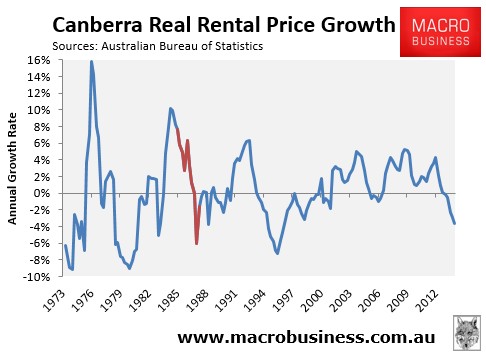

First, SQM gives no longer-term context. The below charts show clearly that real rental growth only increased in Sydney and Perth when negative gearing was abolished in the 1980s (shown in red):

Advertisement

Whereas real rental growth was flat or fell elsewhere:

Advertisement

Advertisement

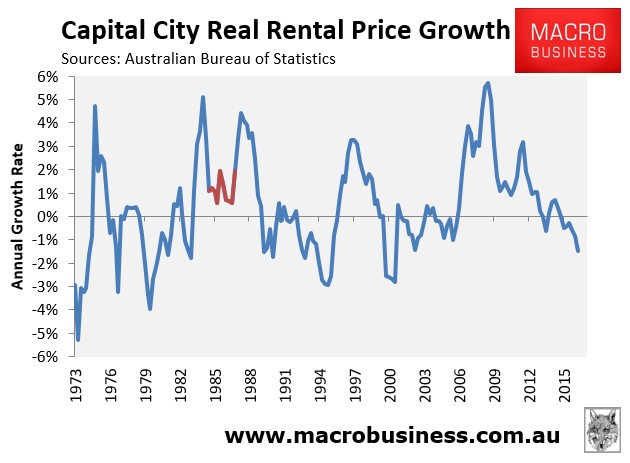

There was also no discernible impact nationally:

But don’t just take my word for it. Here’s what the 1987 Cabinet Submission on negative gearing said about rental growth (my emphasis):

“Data for individual capital cities suggest that, as might be expected, rents have risen more rapidly in those cities where vacancy rates have been tightest. In the twelve months to March quarter 1987, rent increases in six of the eight capitals lagged the CPI“.

Advertisement

Now, if there was any truth whatsoever in the claim that abolishing negative gearing pushed up rents, then wouldn’t rental growth have risen Australia-wide, rather than in only Sydney and Perth?

As for the REIA data, real rents fell across Melbourne, Adelaide and Canberra, according to SQM’s own chart. Whoops!

As an aside, the 1987 Cabinet Submission on negative gearing explicitly stated that “the ABS measure of rental cost movements [is] superior” because “the ABS index is based on a properly constructed sample of dwellings representative of the overall rental stock. The MBFA and REIA measure the asking rent of dwellings available through advertisements (MBFA) and real estate agents (REIA) without full regard to their representative nature”.

Advertisement

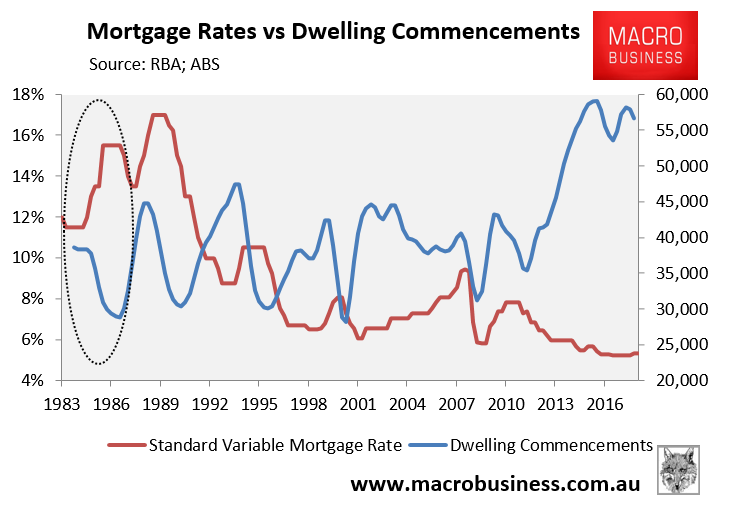

Finally, SQM’s claim that dwelling construction fell after negative gearing was repealed is asinine. The fall in construction can be explained by the sharp rise in mortgage rates, from 11.5% in March 1985 to 15.5% in September 1986 to June 1987 (circled below):

Indeed, the decline in construction, which bottomed out in March 1987, was one of six corrections over the last three decades that all closely followed, or were simultaneous with, rises in mortgage rates.

Advertisement

SQM references the rise in mortgage rates in passing, only to then dismiss it:

There were other contributing factors over the time. Average home lending rates rose from 11.5% (June 1985) up to 15.5% (May 1986). Then were later cut from September 1987.

This would have also been a contributing factor in the decline of housing finance approvals and commencements plus the rise in yields. However, this alone can not explain the immediate acceleration rents that happened in some cities such as Sydney.

We also note that gross rental yields fell post the re-introduction of Negative Gearing even while interest rates rose again over the course of 1988 to 1990; also a time when rental growth was slowing.

Amazingly, regarding the last paragraph, SQM doesn’t acknowledge that the stock-market bubble would have attracted funds away from property, or that the ensuing “crash of ’87”, would have caused a flight back to property.

Advertisement

Overall, this is very superficial analysis that has attempted to re-write history, alongside misreading the likely impact on construction and rents.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.