SQM Research’s managing director, Louis Christopher, has been a big supporter of negative gearing reform over the years.

Back in April 2014, Christopher penned a piece arguing that the best time to repeal negative gearing was when the housing market was experiencing a boom – i.e. like right now:

“In my opinion, if you were to time such a repeal, you would do it while the market was in recovery and not while it was having a downturn. Implementing such a change may also hold off interest rate rises”…

He also argued that restricting negative gearing to newly constructed dwellings only would likely keep construction going even if prices fell:

“… if the story above is correct in regards to keeping negative gearing on new dwellings, then we may well keep the dwelling construction side of the economy going”.

In 2015, Christopher kept the arguments to reform negative gearing flowing. On 11 March 2015 he noted the following with regards to the Abbott Government’s refusal to reform the tax lurk:

“We are of the belief that the less government intervention there is in the property market, the better. Governments all round should be doing more to promote housing affordability, not unaffordability.

Reducing negative gearing, a highly distortionary policy, would have a far more beneficial effect on promoting housing affordability. If negative gearing was repealed or altered, investors who are now gobbling up property would back off buying houses, which is what those who are demanding lower dwelling prices want to see…

So, if anything needs to be done, it is to eliminate existing distortions, and not introduce more”.

Christopher then followed-up on 30 March 2015 with a strongly worded piece arguing that negative gearing should be restricted to new dwellings in order to boost dwelling supply:

“I firmly believe negative gearing should be restricted to new residential real estate. By allowing negative gearing on new residential properties and off-the-plan developments, we are providing a proper tax benefit to where it is justified and needed most: the construction and development of new dwellings.

That was the original purpose of negative gearing. The tax benefit was actually first introduced in 1936 with the direct aim to increase the supply of housing and move the economy forward from the Great Depression.

The problem is when it is applied on existing properties there is no real tangible economic benefit. Instead, it is unnecessarily stimulating demand on existing housing and, therefore, pushing house prices artificially upwards and so, damaging affordability.

Now in all this, if negative gearing is restricted, it will unlikely mean dwelling price falls everywhere. The market is driven by many factors including population growth, interest rates, the exchange rate and, of course, the health of the economy. However, I would expect a moderate correction, where investor demand has been very strong in recent times, such as the Sydney housing market…

If governments wish to improve affordability in the market, restricting negative gearing to new homes would be ideal. It would stimulate new housing and reduce investor activity on existing housing”.

Louis Christopher this morning told SmartCompany he was disappointed in the Prime Minister’s “hypocritical” decision to leave negative gearing unchanged.

“Now would have been a perfect time to implement changes, given the market is on a little high, it would have been able to withstand any changes now, rather than in a period of downturn,” says Christopher.

Christopher says given the backdrop of the budget black hole and a housing affordability crisis, a reform would have been a “vote winner” for the Abbott government.

“Tony Abbott now has hardly any leg to stand on when talking about tax reform and tightening our belts and so forth,” he says.

“The changes will fall on the working class, when he’s willing to give breaks on big companies and breaks on investors, it’s hypocritical. This will be a vote loser”…

Christopher also says the decision seems to go against the direction of Abbott’s own Treasurer, Joe Hockey, and believes the PM is listening to “self-serving” voices and not looking at the bigger picture.

“It’s stupid from a property market perspective. He’s failed.”

This year, Christopher has continued the push for negative gearing reform. In February, he appeared on Sunrise to argue the case:

Here’s the money quote:

“The notion of having negative gearing on new property is not a bad idea because I think that will encourage supply and puts the concession where we need it most, and that is increasing the supply of new real estate, which will keep the rents at a stable level and make sure that we don’t have a long-term housing bubble”.

A few days later, Christopher appeared on The ABC arguing that Labor’s policy would most likely lower rents:

DAVID TAYLOR: [Christopher] says there’s no clear evidence that the Labor government’s policy to scrap negative gearing in the 1980s led to higher rental prices.

LOUIS CHRISTOPHER: The truth is that the rental period at that time, across Australia, was mixed.

There were some cities during this time which recorded falls in rents; there were other cities, namely Perth and Sydney, which were recording rises in rents above and beyond inflation.

DAVID TAYLOR: Louis Christopher, based on your numbers though, do you suspect that rents would rise if negative gearing was taken away, as property investors try to make up for some of the other expenses?

LOUIS CHRISTOPHER: What Labor has actually put forward is about stimulating new supply of property, so we think that that would put a little bit of a dent in that whole argument that “look, rents would dramatically rise”, because what they’re trying to do here is actually stimulate the supply side, and we think they would have some success in doing that.

And later in February Christopher argued that there would be no rent spikes or market decimation under Labor’s policy:

“Would there be a surge in rents?

In our opinion, we think no. And that is based on what happened in history as well as the fact that if Labor’s policy passed, it would keep negative gearing on new property…

Labors’ proposal to keep negative gearing on new properties would most likely ensure a strong supply side response to the market. We have seen such directed stimulus work on the markets before, namely in the form of various first home owner grants, so we are confident, the market is responsive to such stimulus.

We believe that should Labor’s proposal succeed there would be an adjustment period where, yes, many investors may stay away from existing property for a period of time, but only until such time that a rise in yields gives them incentive to start buying existing properties again. This would happen as investors would demand a higher yield to offset the lack of tax concessions.

But such a period would not go on forever. Once yields are higher, investors would then re-enter the market. Potentially yields could rise to the point where existing residential properties are cash-flow positive from day one, or at least, cash flow neutral. Which I believe would be a positive for the asset class over the long run…

But this adjustment does not necessarily mean there would be an outright “decimation of the market”. We may well likely see for example a period of stagnation in property prices for existing property. Or prices rising more slowly than rents”.

Then in March 2016, Christopher slammed the dodgy BIS modelling’s claim that rents would rise by 10% under Labor’s policy:

SQM Research managing director Louis Christopher also called the report’s findings, in particular a rent increase of 10 per cent, “hard to believe”.

“We think the opposite would play out – there would be a moderate increase in supply,” Mr Christopher said.

“Negative gearing is an existing distortion and the market will eventually adjust to the new reality,” he said.

So, why am I taking you on this long walk down memory lane? Because SQM Research has now released analysis arguing that the property market would likely experience a prolonged contraction and rents would rise in the medium-term under Labor’s policy, which obviously contradicts Christopher’s previous statements.

Below is the media release:

SQM Research, Australia’s most respected property investment research house, today released a report into the likely housing market effects of The Labor Party’s proposal to change negative gearing.

Key findings

Yields to Rise

International comparisons, historical precedents and the effective grossed up yield benefit all indicate that acquisition rental yields are likely to rise between 90 basis points and 1.1% over a two to three year period post the implementation of the new policy. Average acquisition yields therefore may rise from approximately 4.4% up to 5.5%.

Rents to Remain Stable – Initially

Rental changes are initially likely to be negligible with rental growth remaining at current levels of between 1-2%, nationally. However there may be some upwards pressure from year three (2020) due to an expected decline in completions, which in itself may occur due to the forecasted downturn in the market. SQM Research believes market rents could accelerate to 6% in a worse-case scenario.

Dwelling Prices to Fall

Given the forecast of initial negligible rental growth, SQM Research forecasts a correction in the housing market of:

• -3% to +1% in FY2018

• -8% to -3% in FY2019

• -4% to -2% in FY2020.The positive end of the range takes into account a response rate cut of 50 basis points by the RBA. The negative end of the range assumes no rate cuts in response.

Downturn Period to Last between Two to Four Years

The total adjustment in the market housing market is forecasted to last between two to four years with most of the adjustment phase occurring within three years. Thereafter the market would likely potentially return back to equilibrium, having ‘priced-in’ the loss of the tax concession.

Sales Turnover and Stamp Duty Revenue to Slump

Property sales turnover is predicted to fall 17% to 20% with most of the declines in sales to occur in the first year (FY2018). This would result in a fall in aggregate state stamp duty revenue of between $3.1 billion to $3.8 billion.

Off-the-plan Investors at Risk

Investors seeking to benefit from the new concession by buying new properties/off-the-plan developments are exposed to a substantial risk of their property being valued below purchase price, especially if the investor is seeking to sell their investment within the first three years.

Managing Director of SQM Research, Louis Christopher, said “In short, there will be a market impact if Labor’s Negative Gearing Policy is legislated.

Our analysis suggests the market impact would last by around three years with sales falling significantly in year one and a correction to take affect with dwelling prices falling the most in the second year. We think there would be a possible response to this event with the RBA cutting rates, thereby mitigating some of the potential price falls. We don’t think the market will crash per say, but it will be felt by the economy. We then expect the market to return to equilibrium from year three.

We strongly encourage Labor to consider some of the investor issues, particularly surrounding the distortion their policy may create on pricing of off-the-plan developments and the likely losses investors in those properties would face come resale time to those who won’t have the tax concession.

While we take the view that negative gearing reform is a good thing, such reform should be done as part of a wider property tax reform that should include a broad based land tax and the elimination of stamp duties. Such reform should have a phase in period of up to three years. Doing so would reduce the risks of a significant downturn which would likely have wider ramifications on the economy.”

So, after banging the drum loudly on negative gearing reform for several years, SQM now believes that reform should only take place as part of a “wider property tax reform” program, which is a pipe dream.

SQM is also overly concerned that Labor’s policy would create “distortions” in the “pricing of off-the-plan developments”, despite arguing previously that the existing negative gearing system is “a highly distortionary policy” and calling for it to be shifted towards new builds.

SQM also seems to assert that Labor’s policy would push-up rents by up to 6% in the medium-term, despite arguing previously that it would likely have the opposite effect, thanks to its stimulatory impact on new construction.

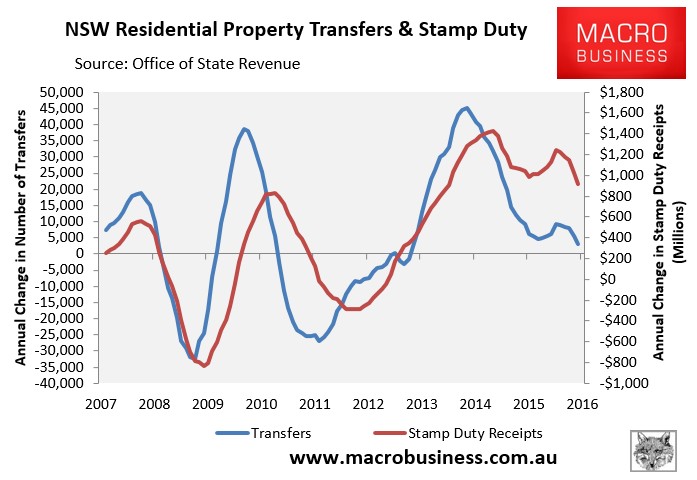

Even on stamp duty, SQM has failed to mention that it is a highly volatile tax under current tax arrangements and due for correction anyway, as illustrated by the below chart on NSW:

So rather than blaming any downturn on Labor’s negative gearing reforms, the states should instead seek to shift their tax bases to more stable and less distortionary land taxes.

There is also the argument that current tax arrangements are pro-cyclical, thus exposing the housing market, economy and state budgets to more volatility than would otherwise be the case (an argument made by the Murray Financial System Inquiry). Thus, Labor’s policy to unwind negative gearing and the CGT discount would help to stabilise the market over the longer-term.

In short, SQM seems to have flip-flopped on negative gearing, undoing its previous good work and giving oxygen to the Coalition and real estate parasites that want the lurk maintained.

Now wait for Scott Morrison and Malcolm Turnbull to use SQM’s report to slam Labor and scare voters.

Instead of being a force for reform, SQM’s report will unfortunately become the resistance.