Australia

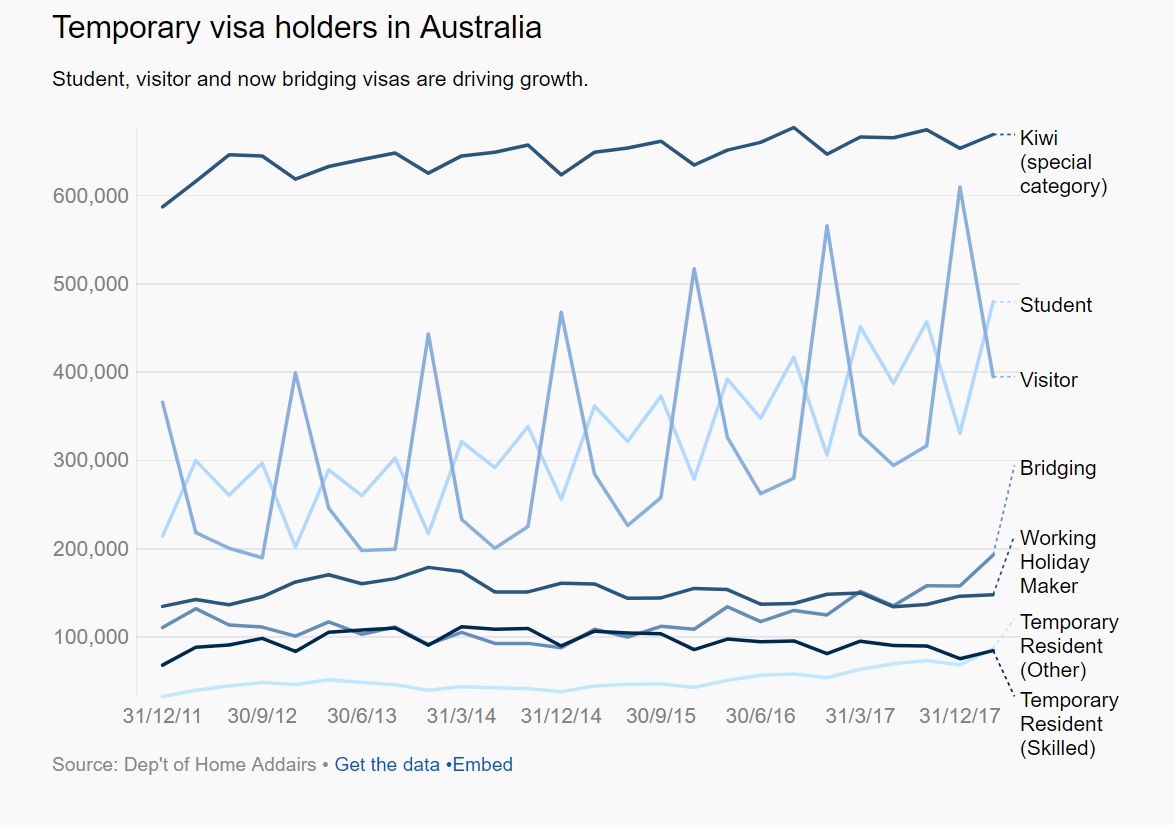

Australia – temporary visas

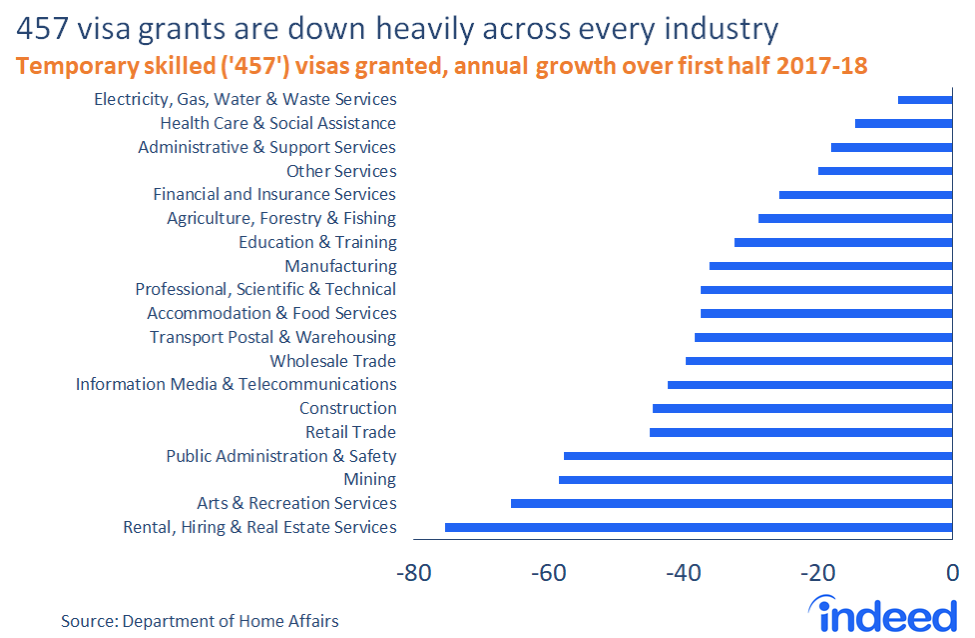

Declines in 457 visa numbers

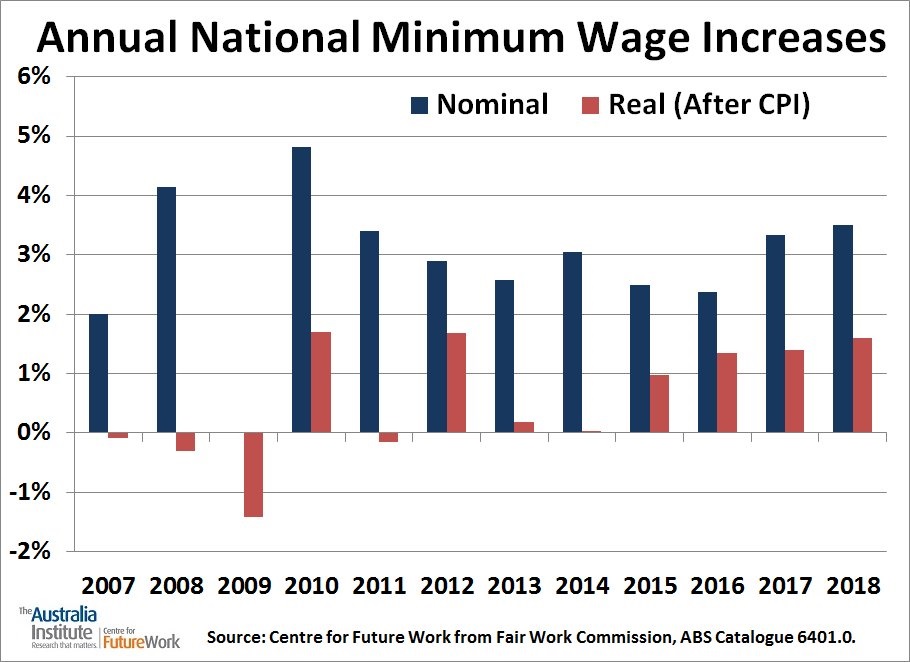

Australian National Minimum Wage Increases

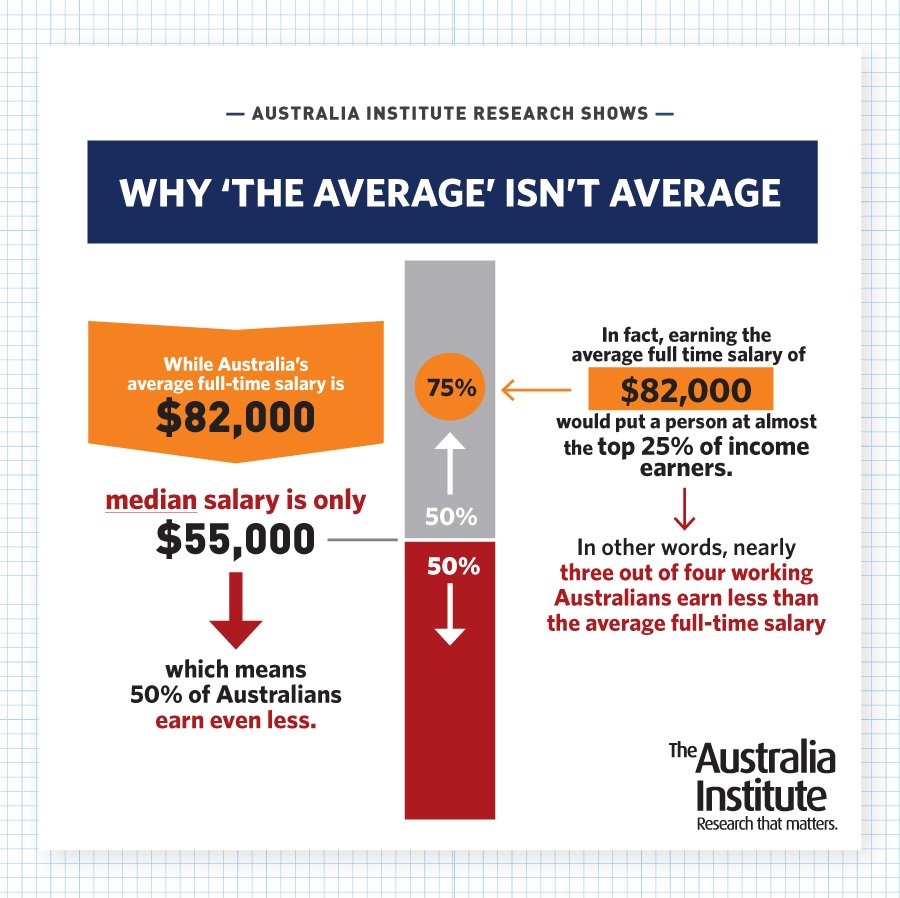

Australia – Average and Median Incomes

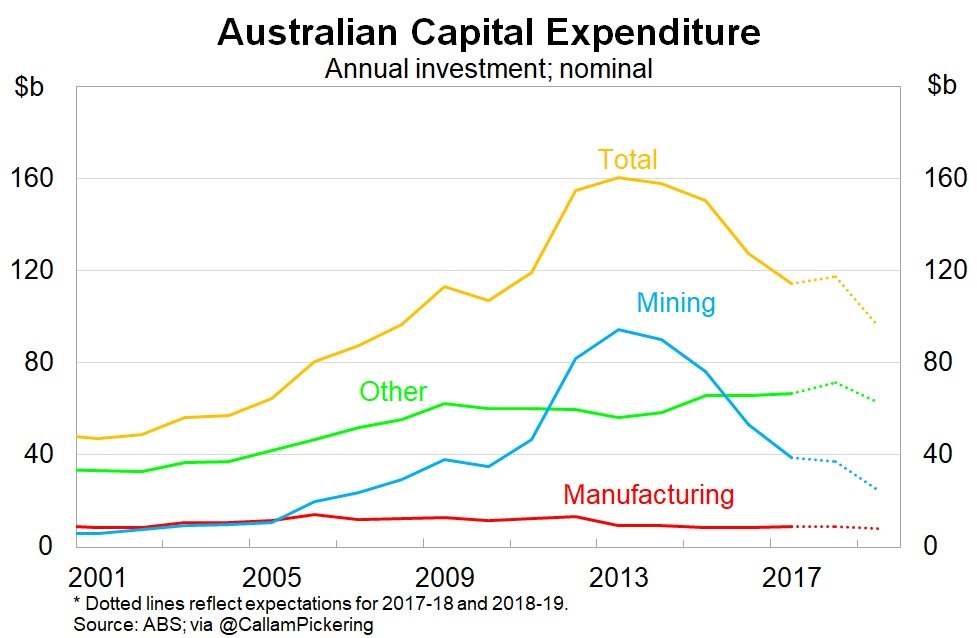

Australia – Capex

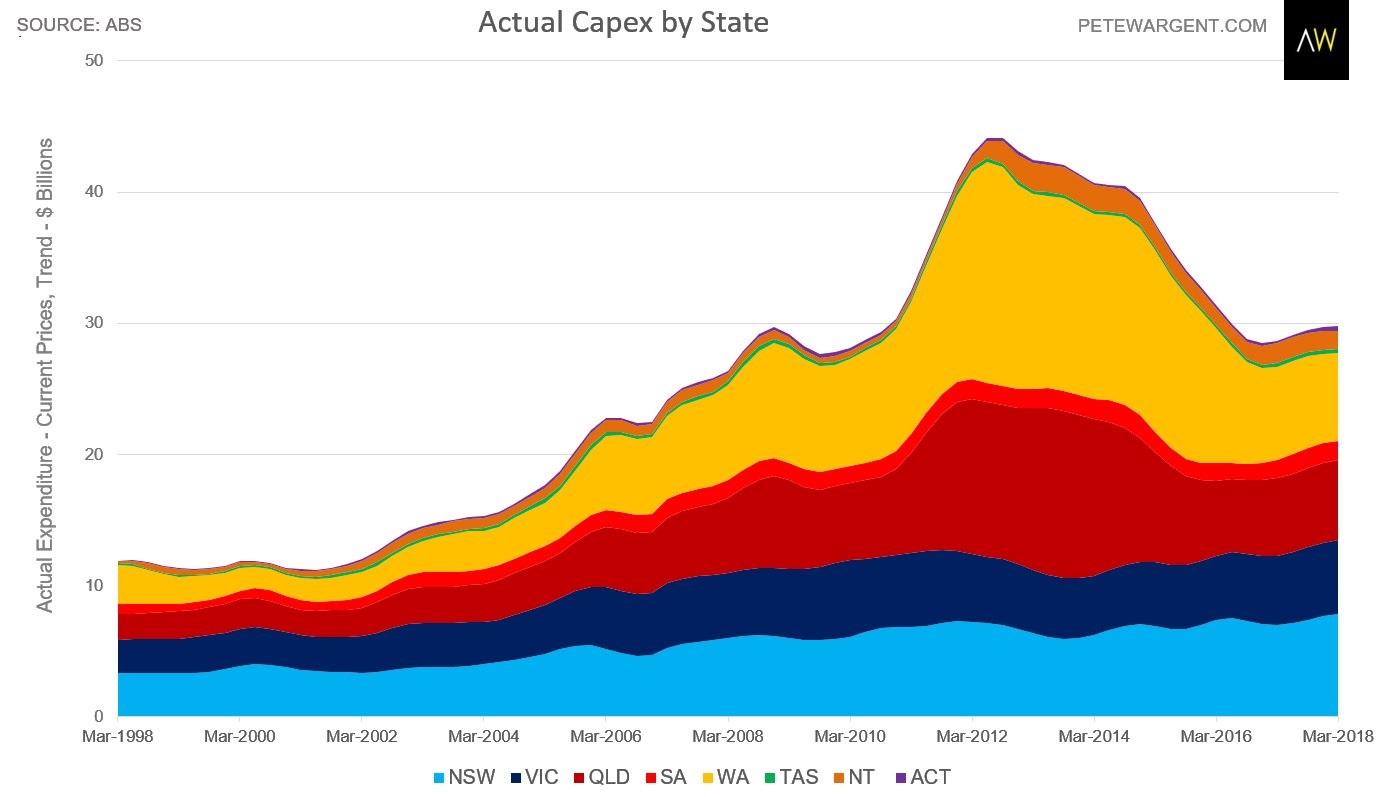

Australia – Capex by State

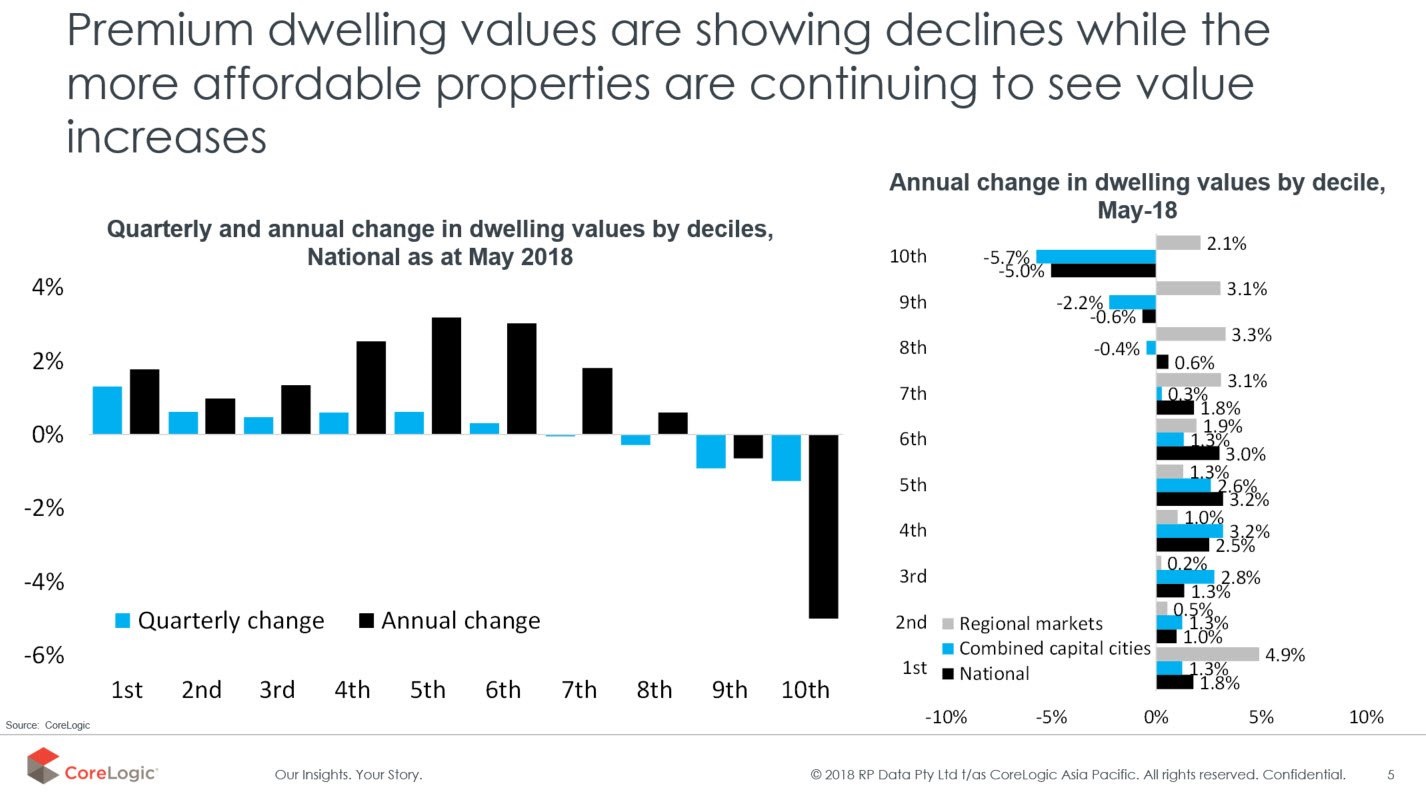

Australia – changes in dwelling values

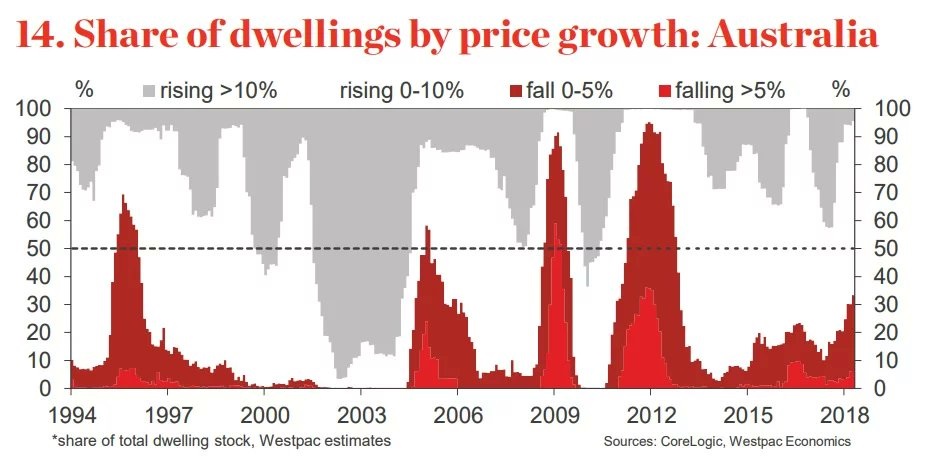

Australia – share of dwellings by price growth

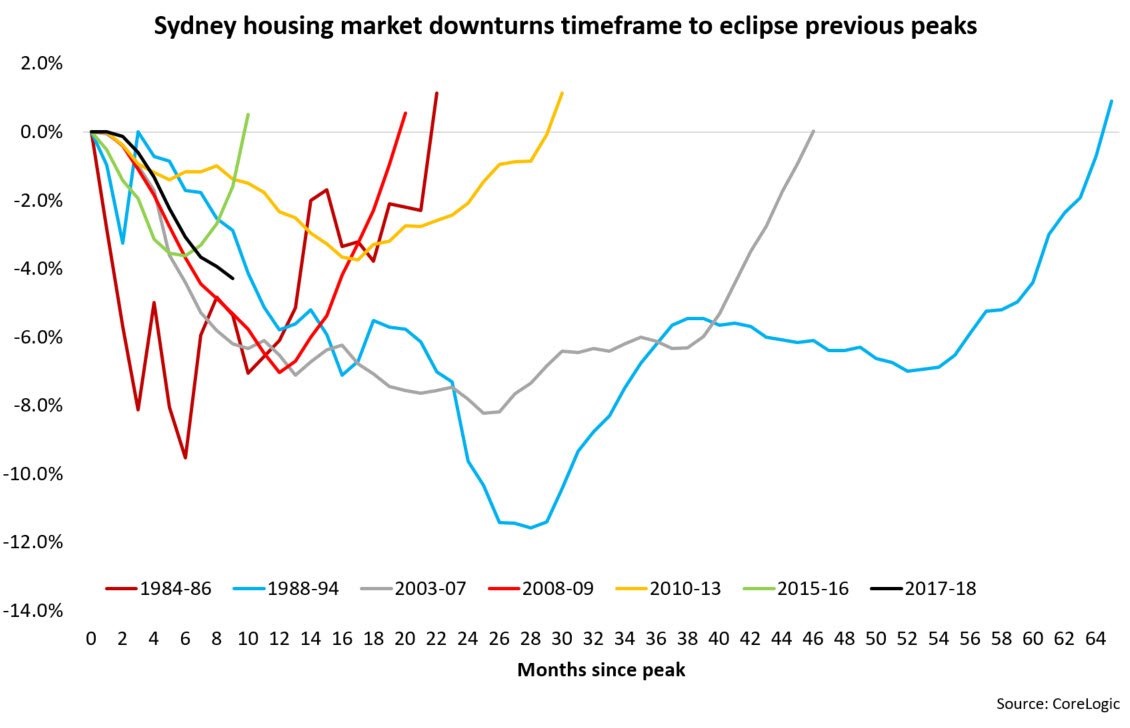

Australia – Sydney Real estate downturns and return to peak

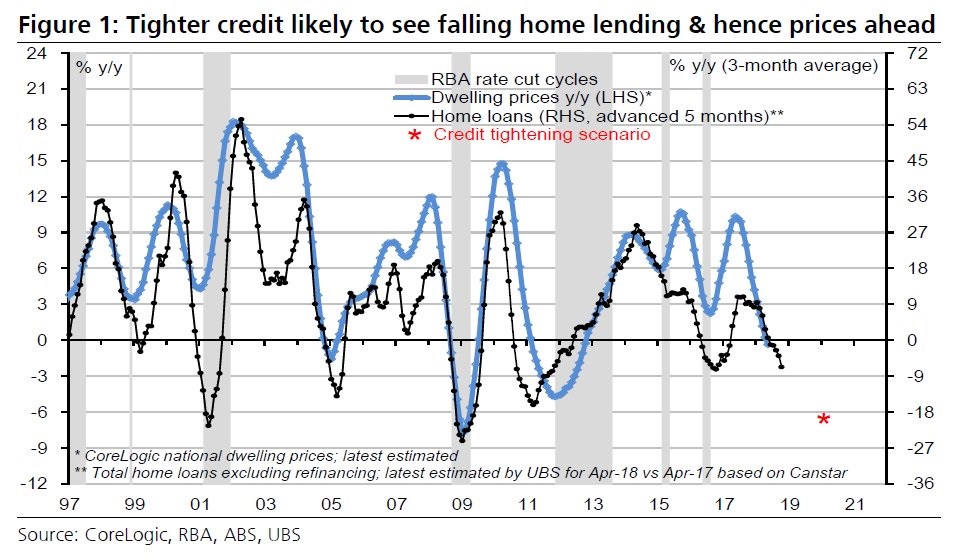

Australia – Home lending and prices 1

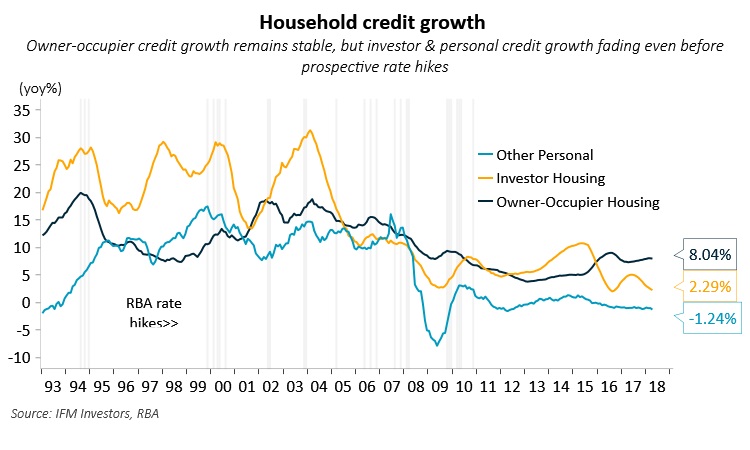

Australia – Household Credit

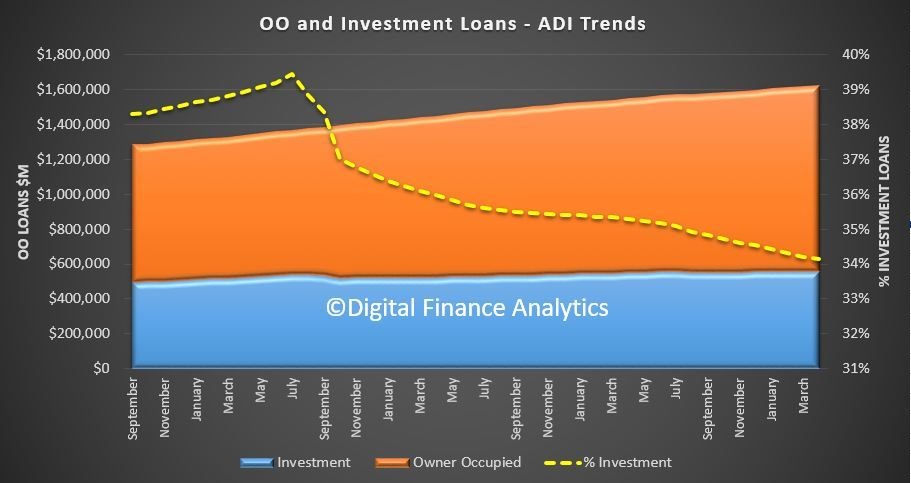

Australia – Owner Occupied and Investor Lending

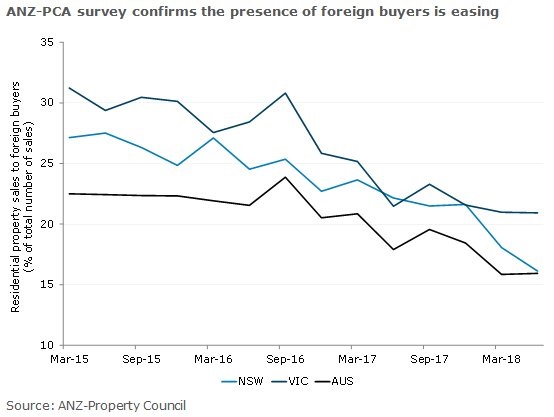

Australia – declining foreign residential real estate buys

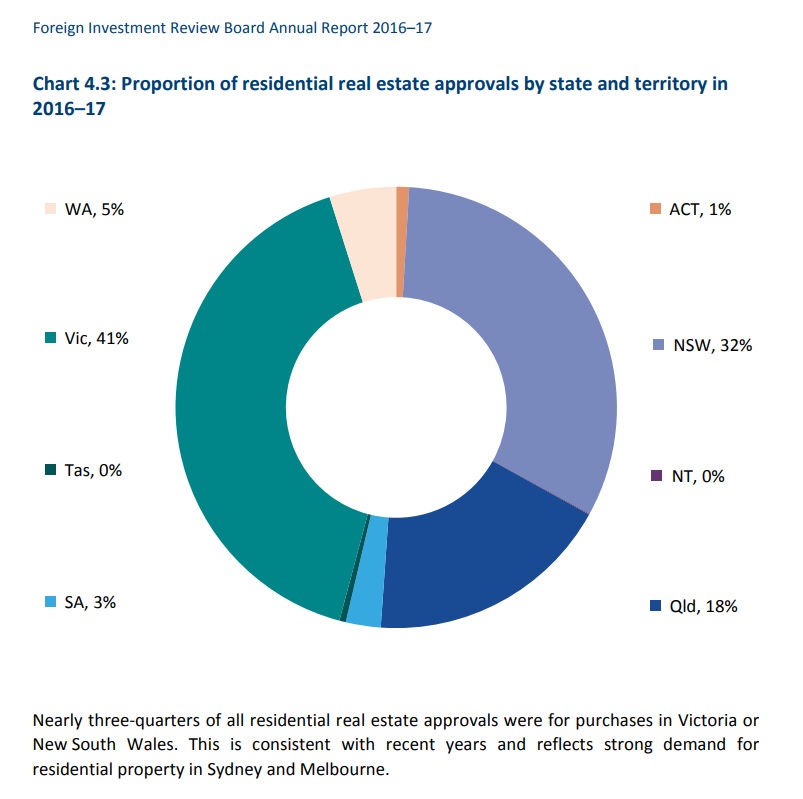

Australia – FIRB approvals by state

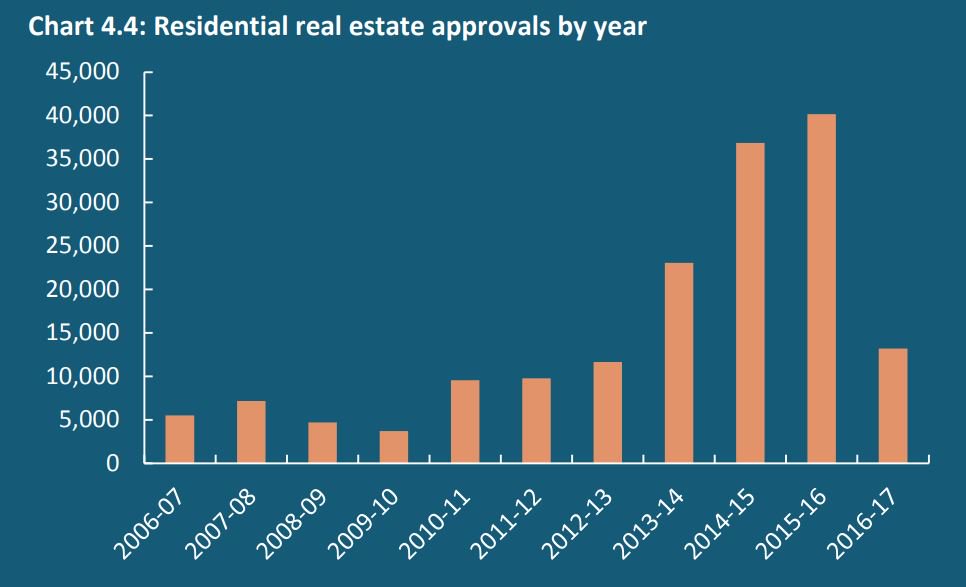

Australia – FIRB Real estate Approvals by year

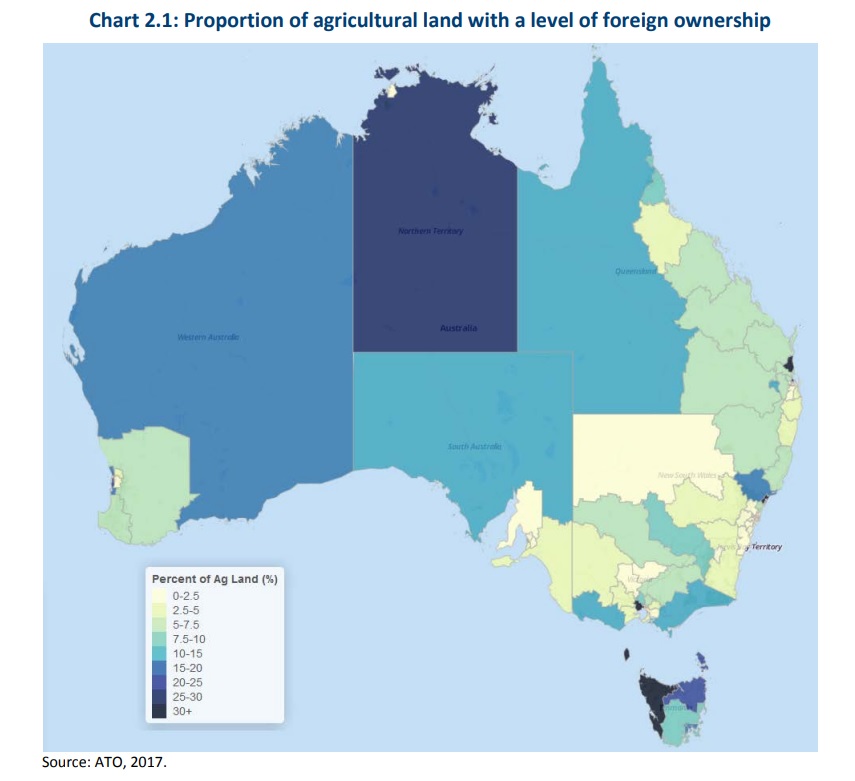

Australia – Proportion of Foreign Owned Agricultural Land (note Northern territory, NW Tasmania, and Werribee [to west of Melbourne])

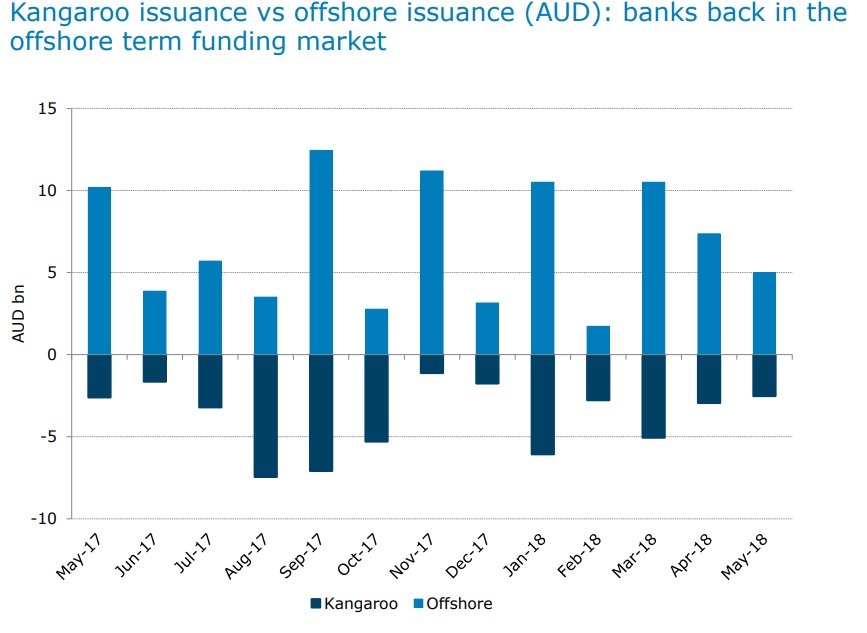

Australian Banks – Offshore and Onshore funding

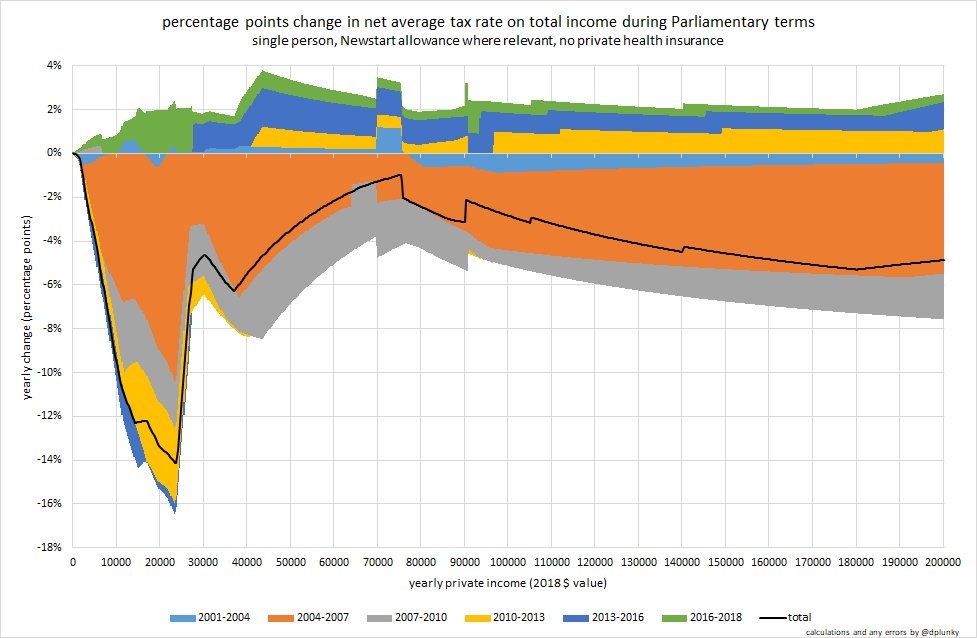

Australia – The ghost of the Howard tax cuts

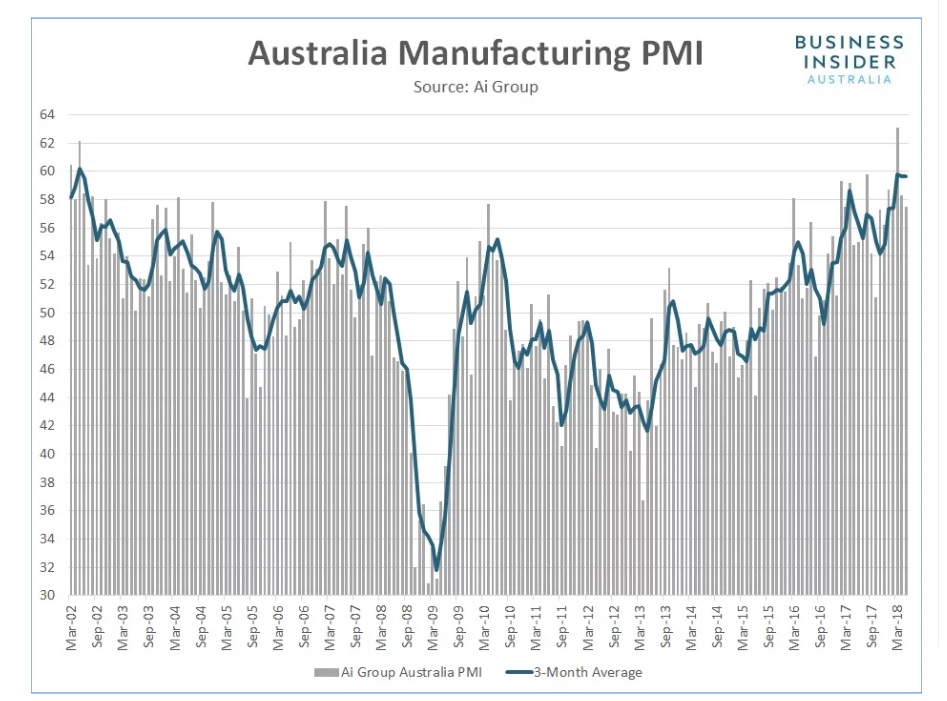

Australia – Manufacturing PMI

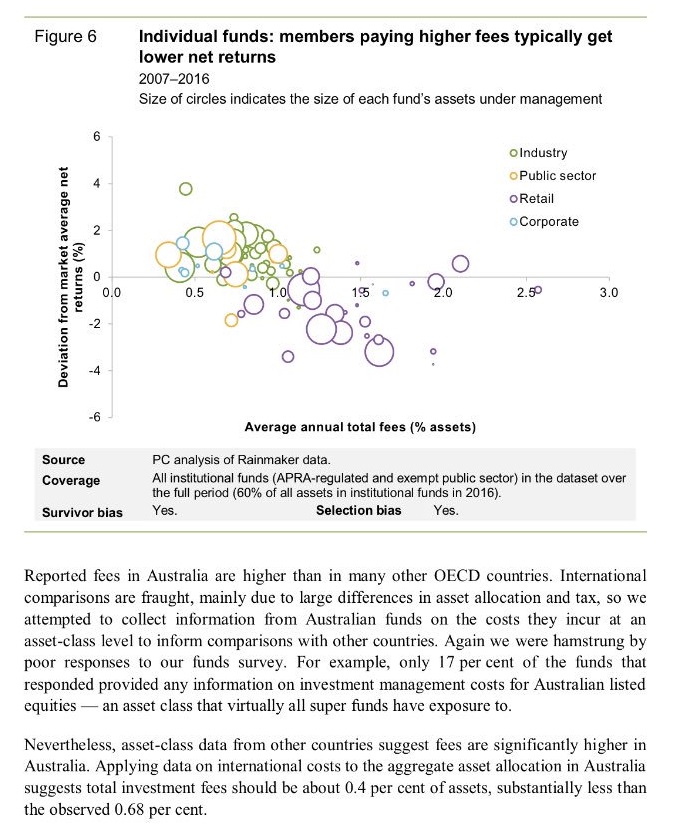

Australia – Superannuation returns and fees

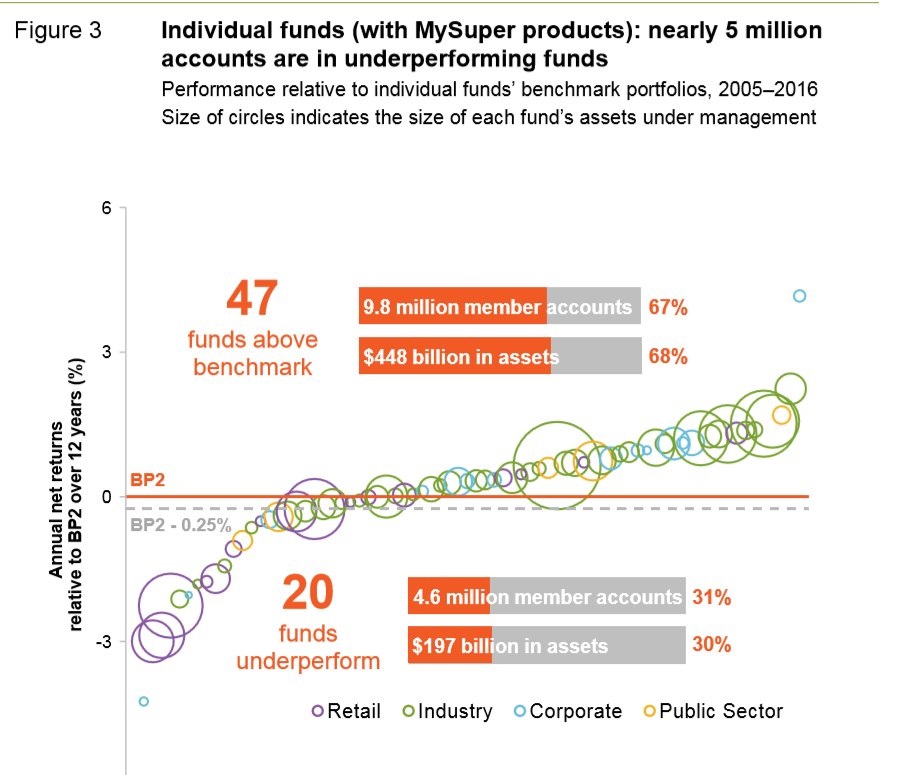

Australia – Superannuation performance

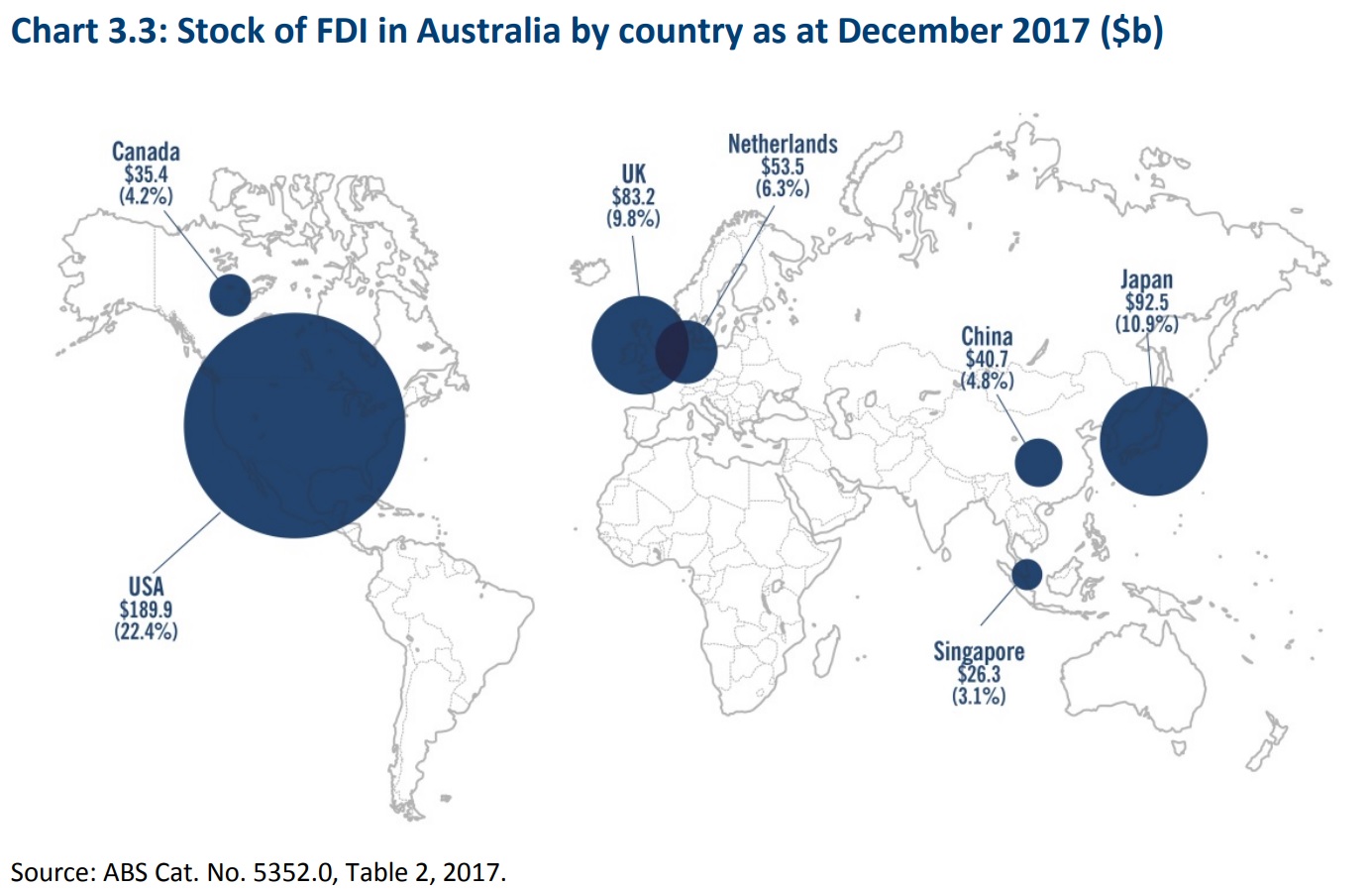

Australia – FDI Stock

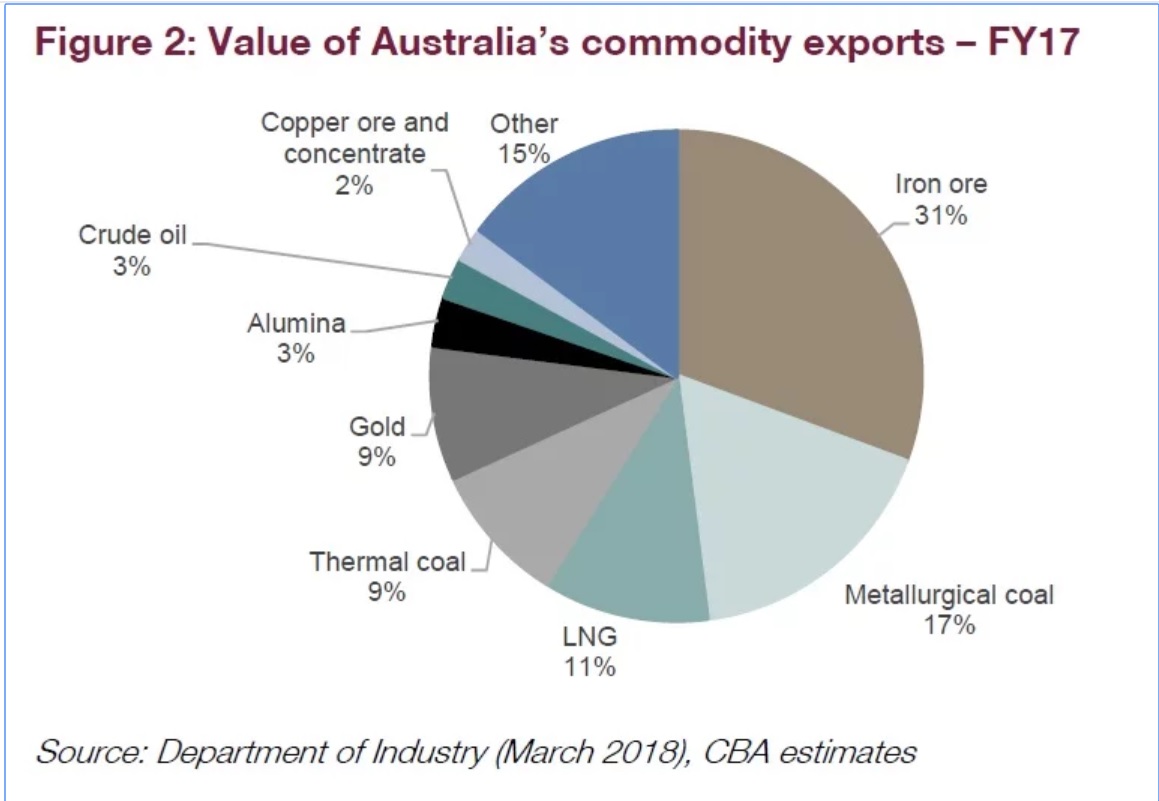

Australia – Commodity Export Values

United States

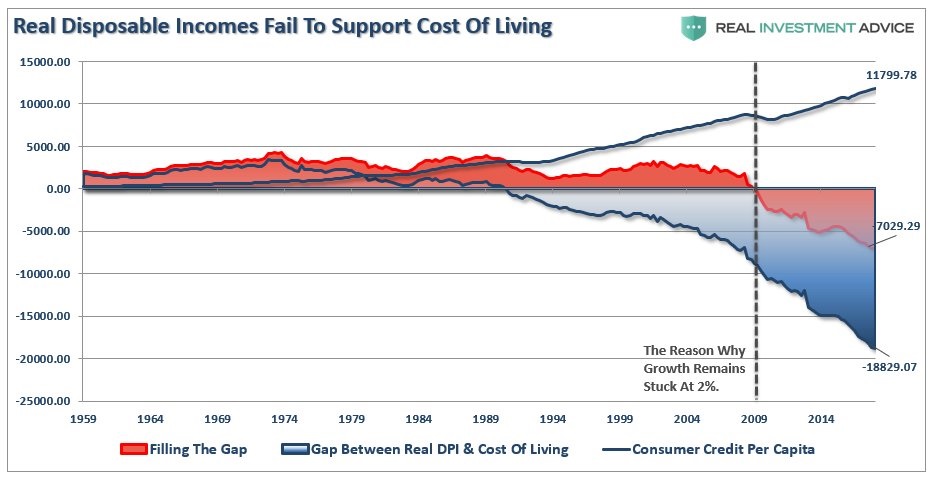

United States – disposable income, credit & cost of living

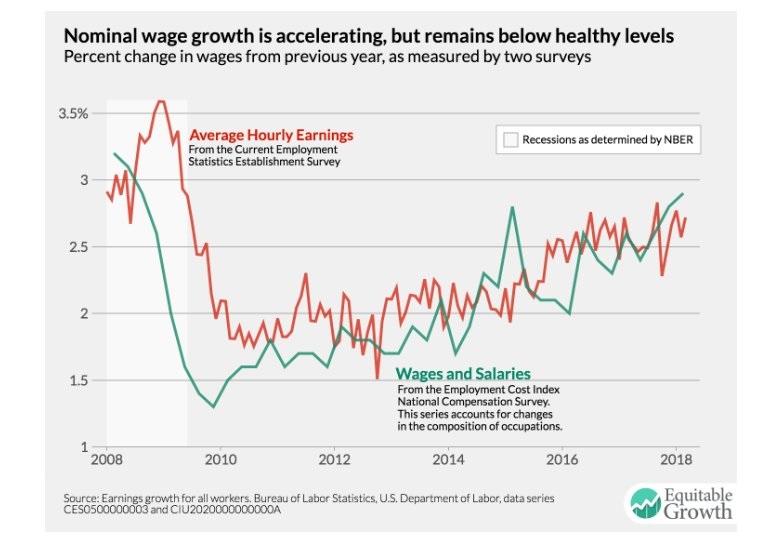

United States – Nominal Wages

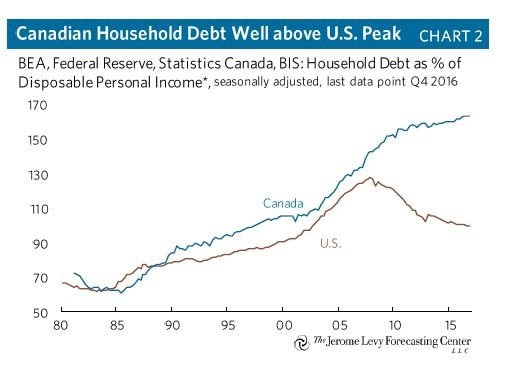

United States & Canada – debt to disposable income

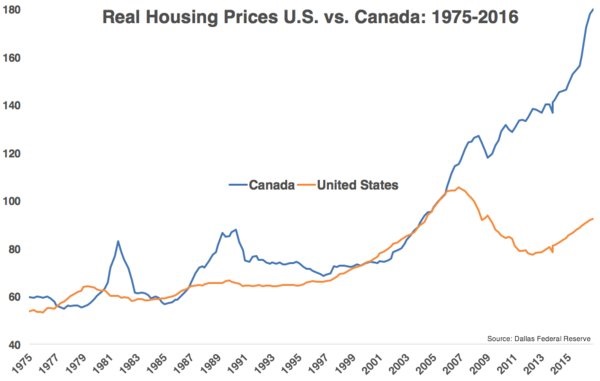

United States & Canada – real house prices

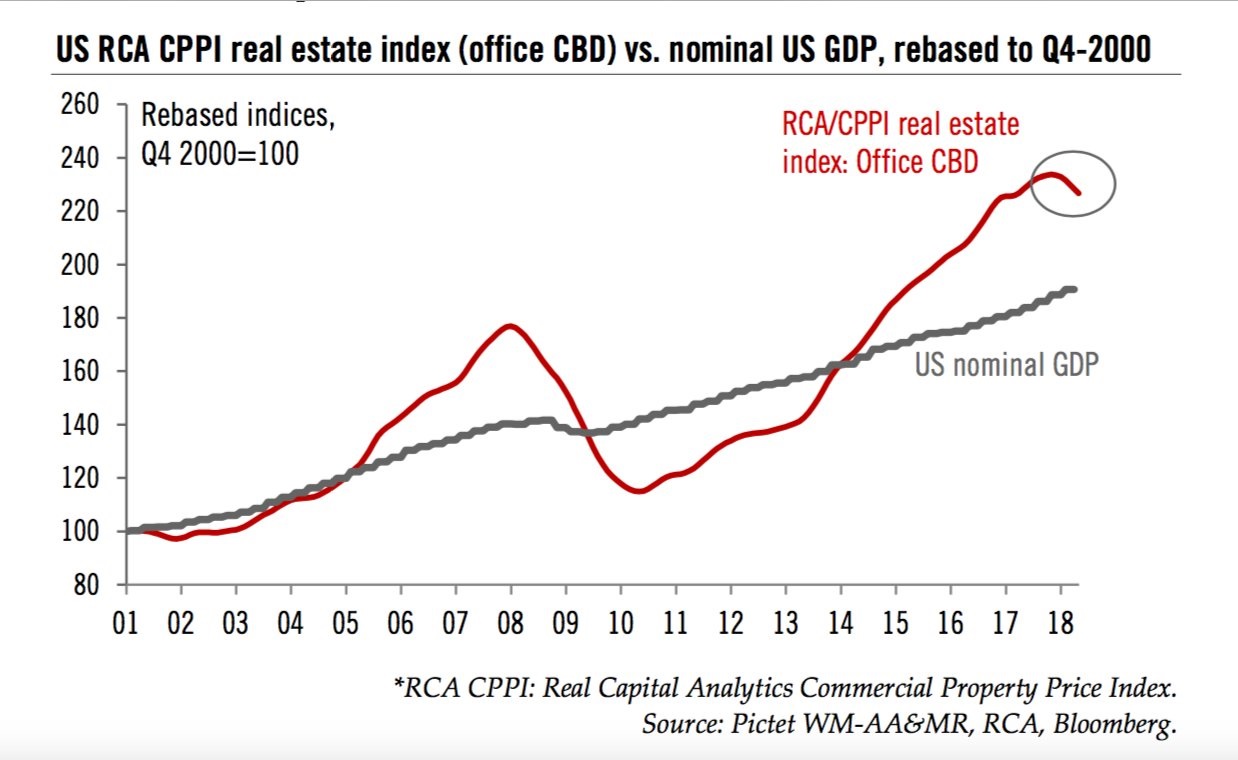

United States – Office Real Estate to GDP

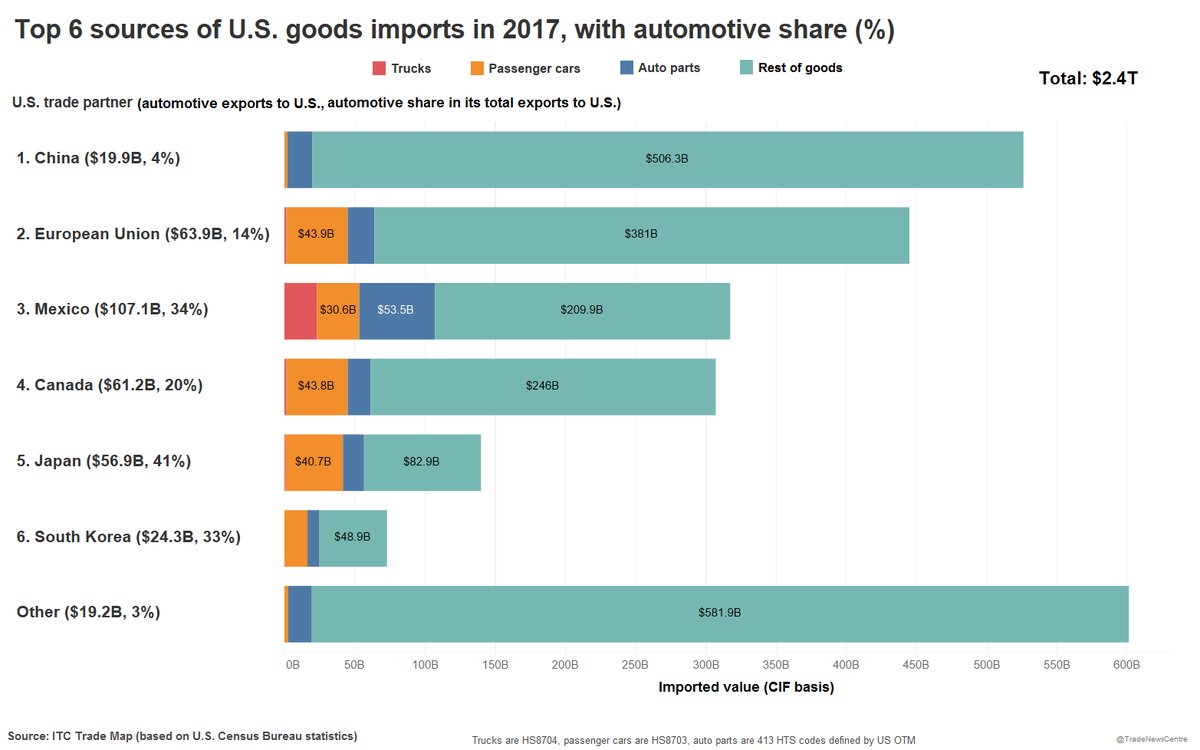

United States – Auto related imports

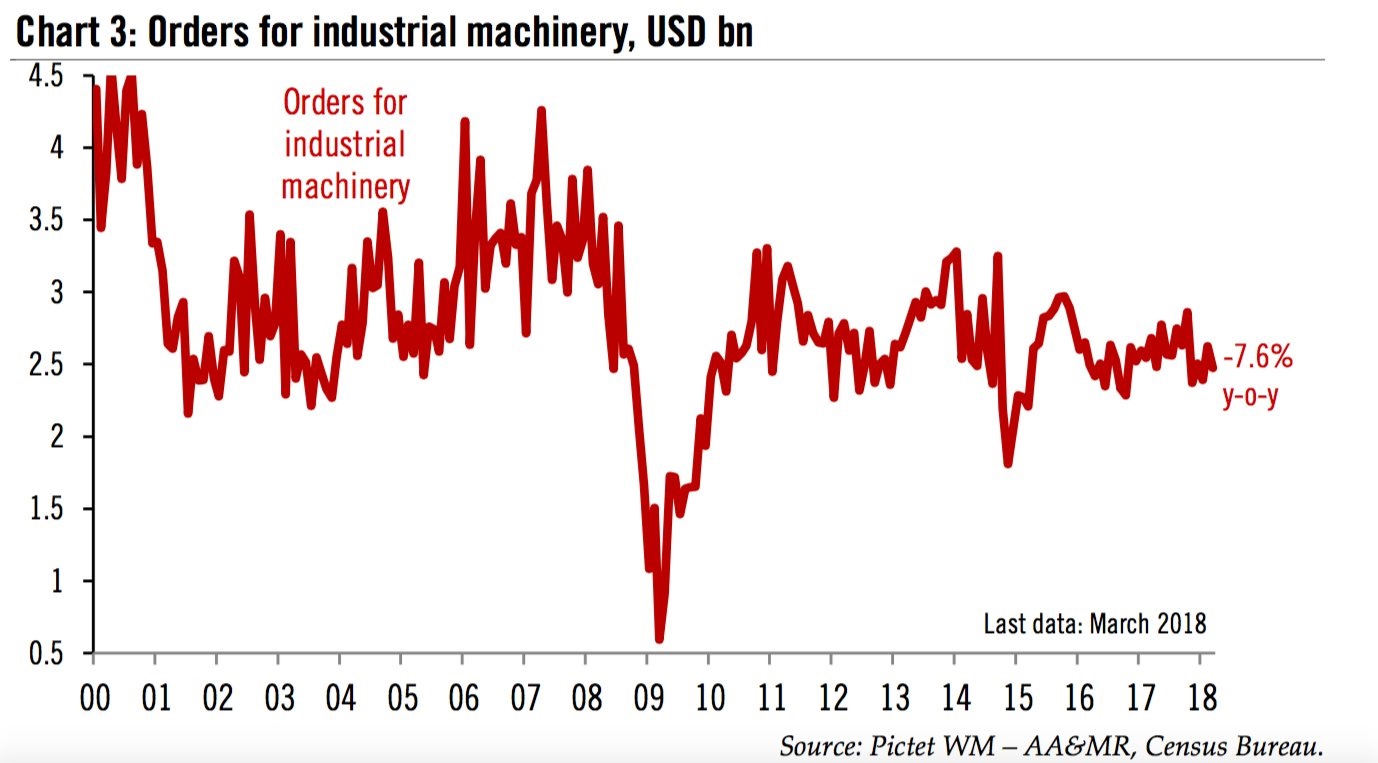

United States – Industrial Machinery

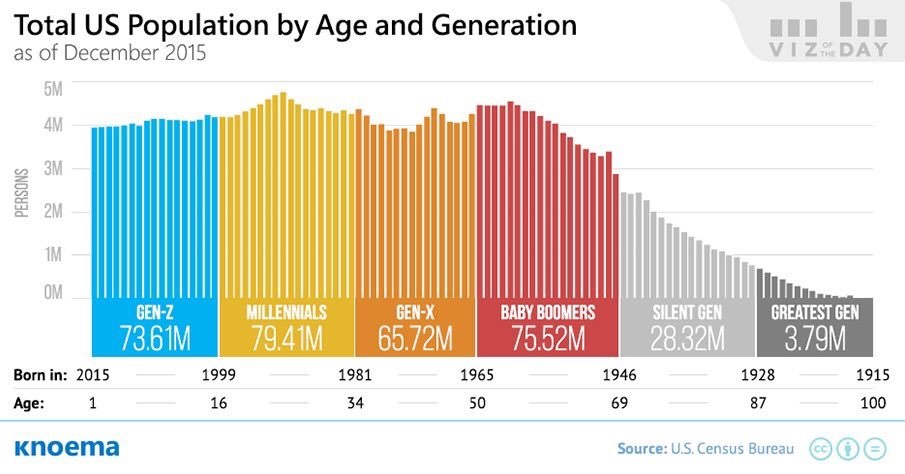

United States – Population by Age and Generation

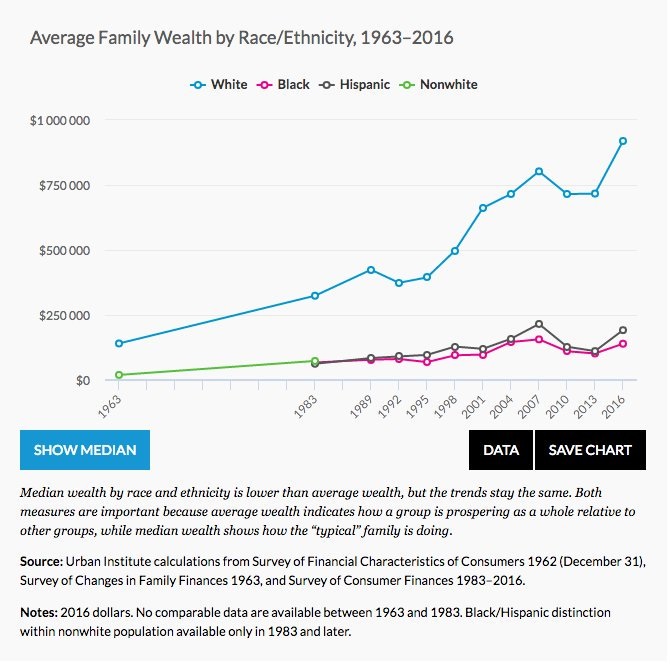

United States – Wealth Race & Ethnicity

China & Asia

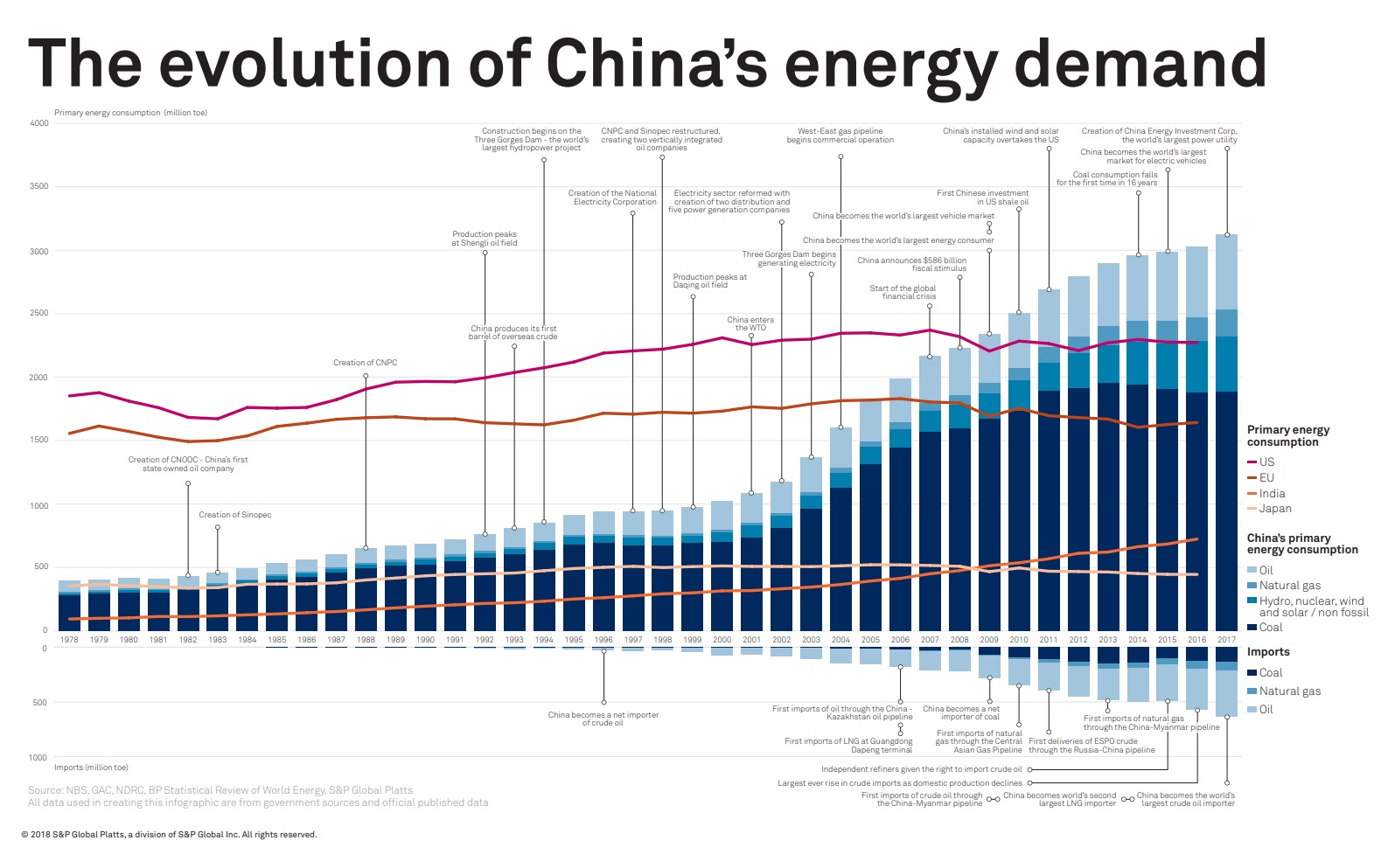

China – energy demand (epic chart)

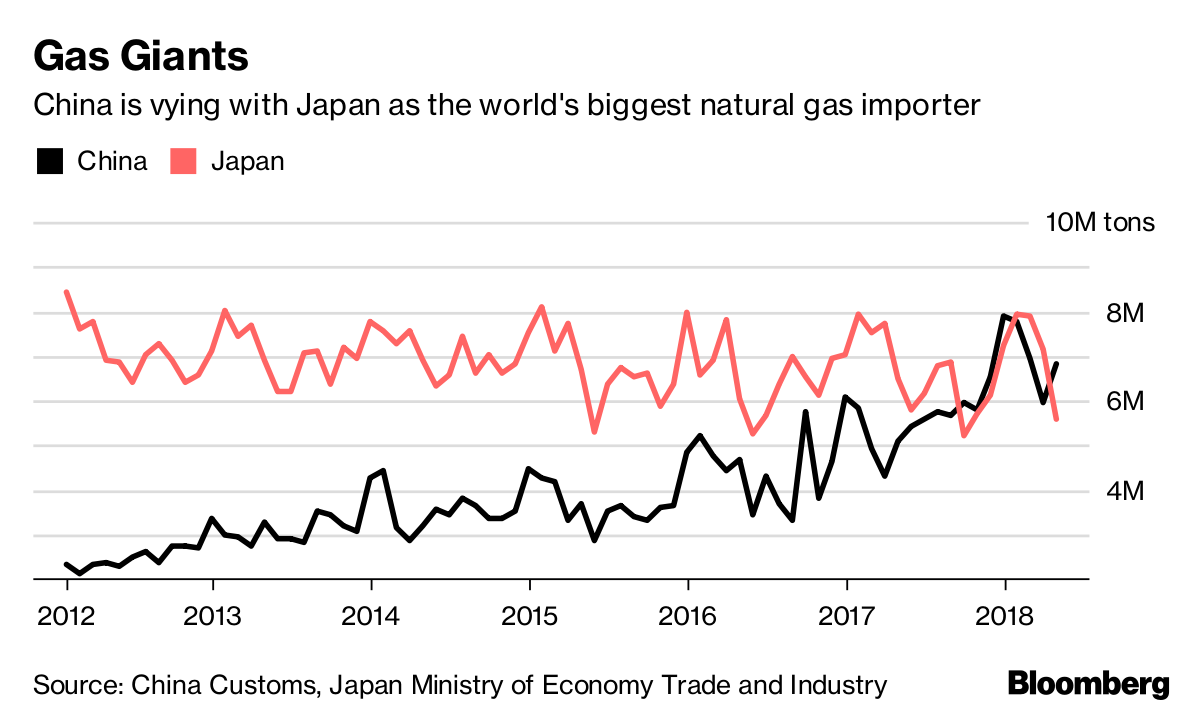

China & Japan – Gas Imports

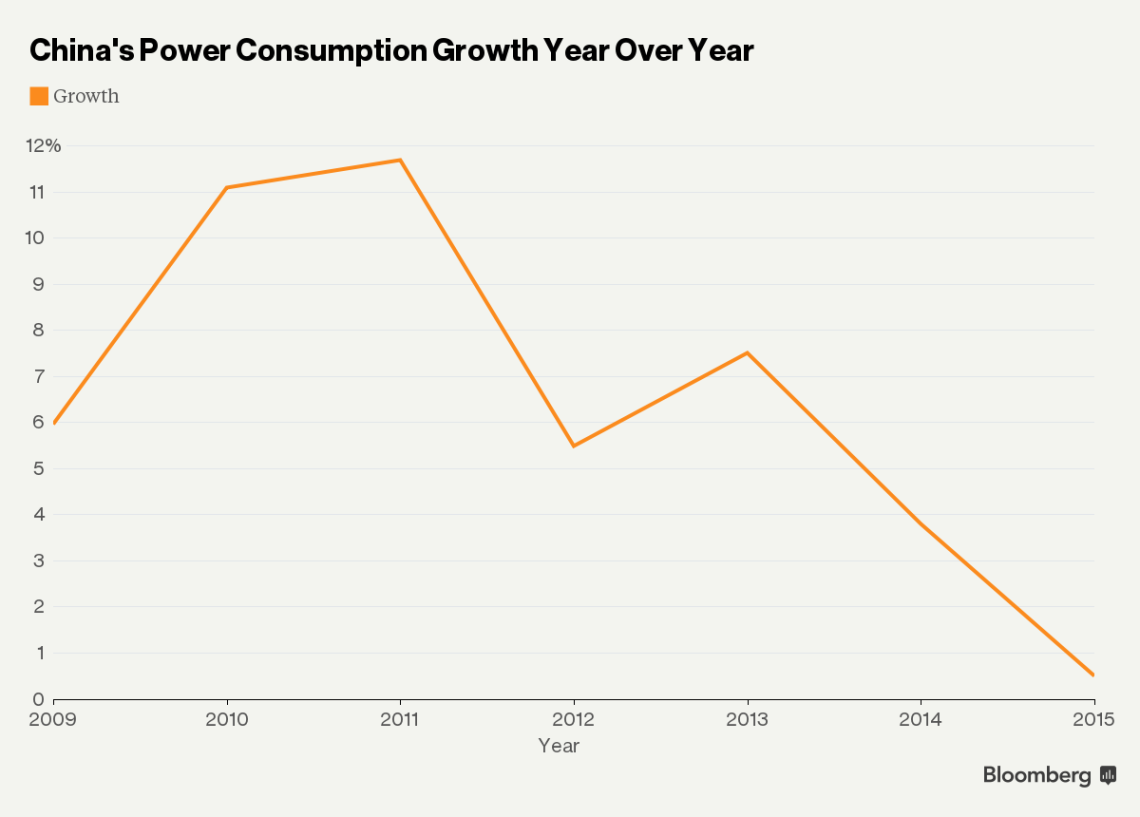

China power consumption growth

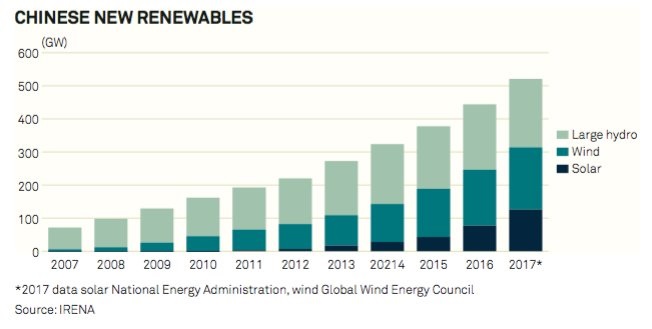

China Renewables

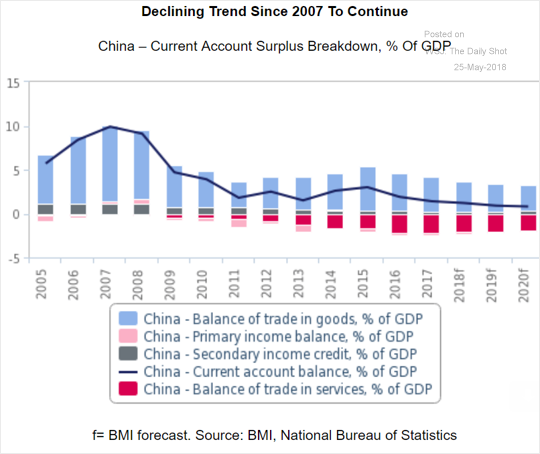

China – Current Account

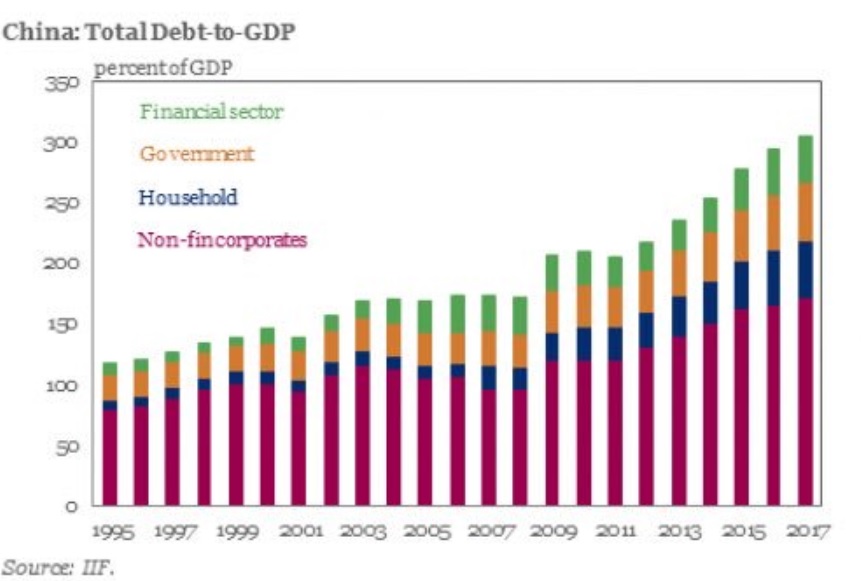

China – Total Debt to GDP 1

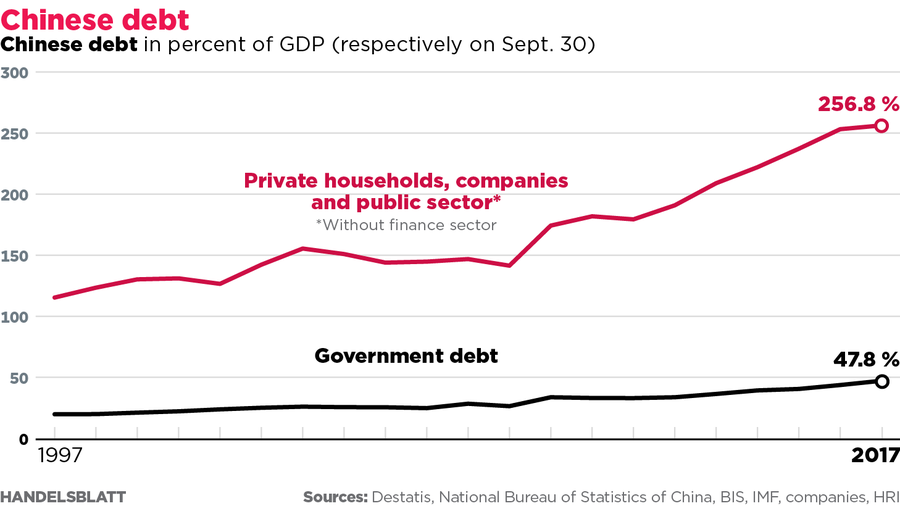

China Debt 2

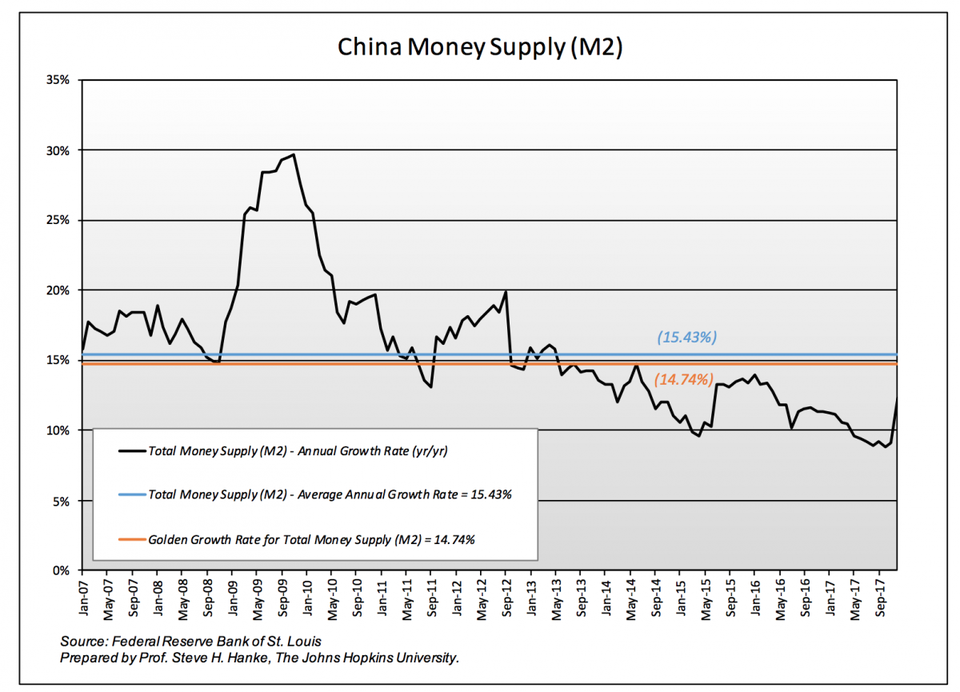

China Money Supply

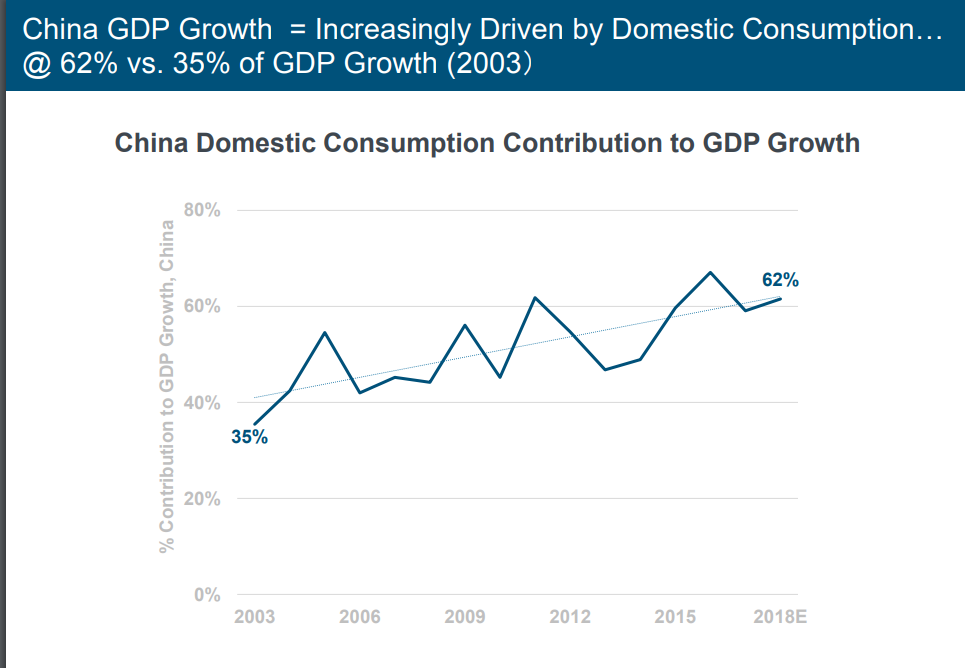

China GDP and domestic consumption

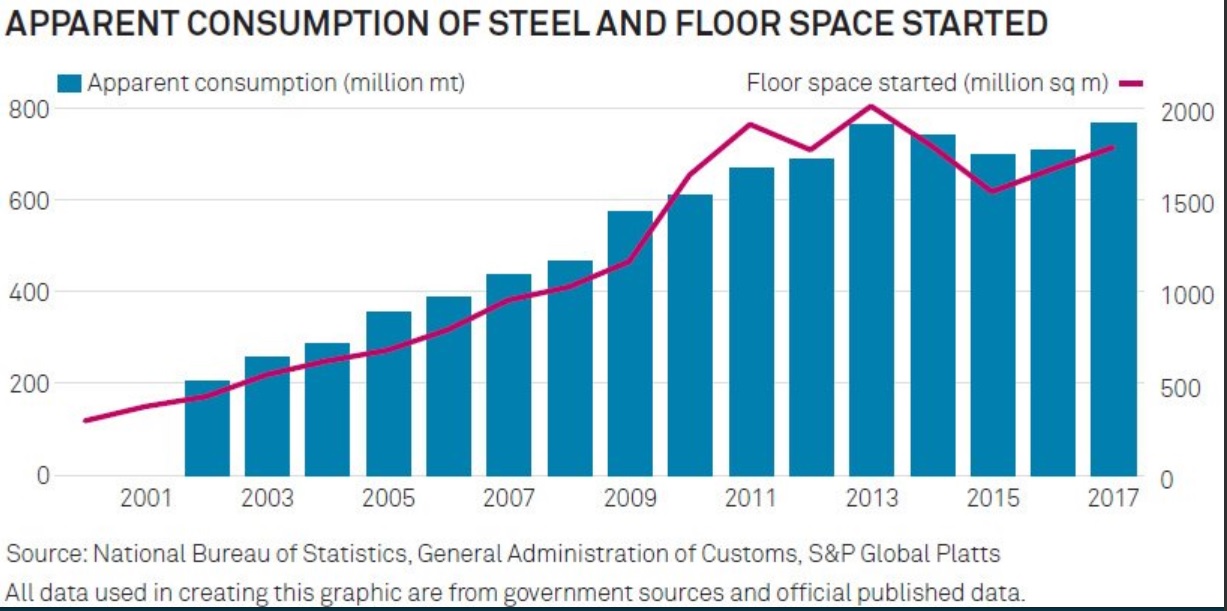

China – steel consumption and floor space

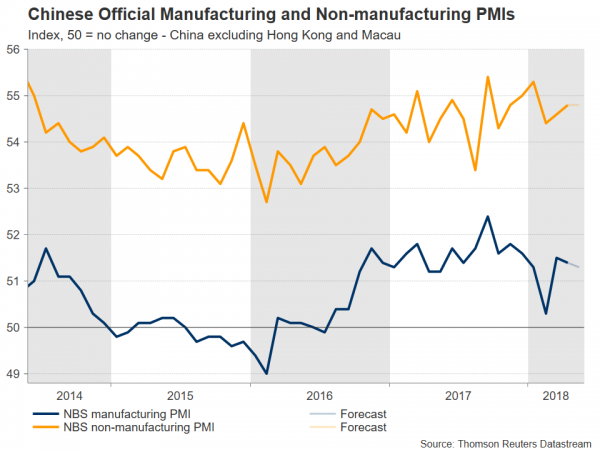

China – PMIs

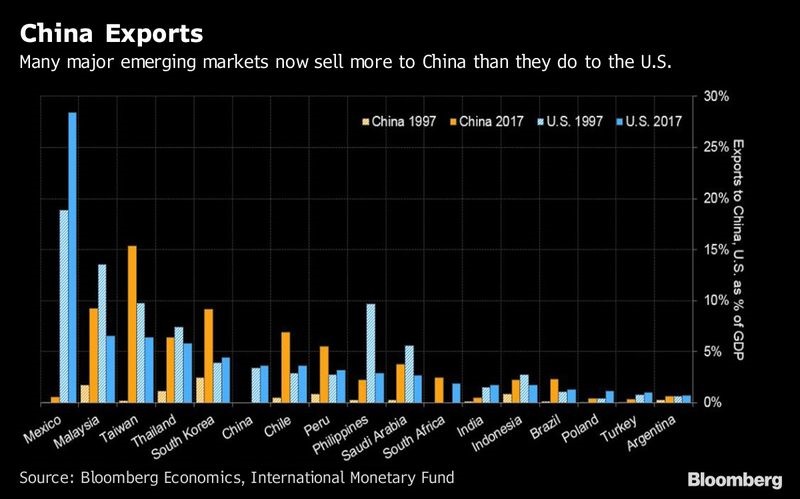

China – Emerging Nations exports to

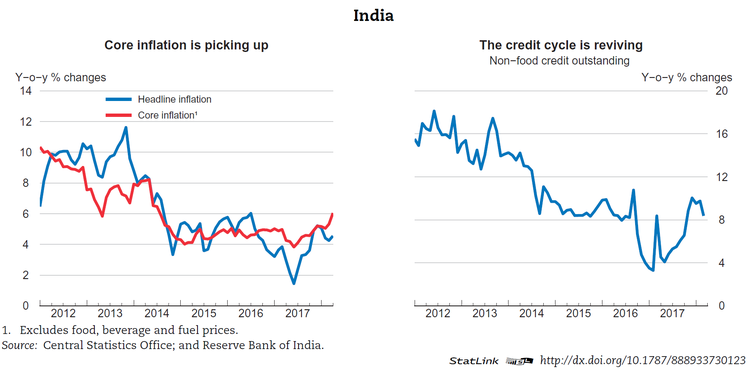

India – core inflation and credit

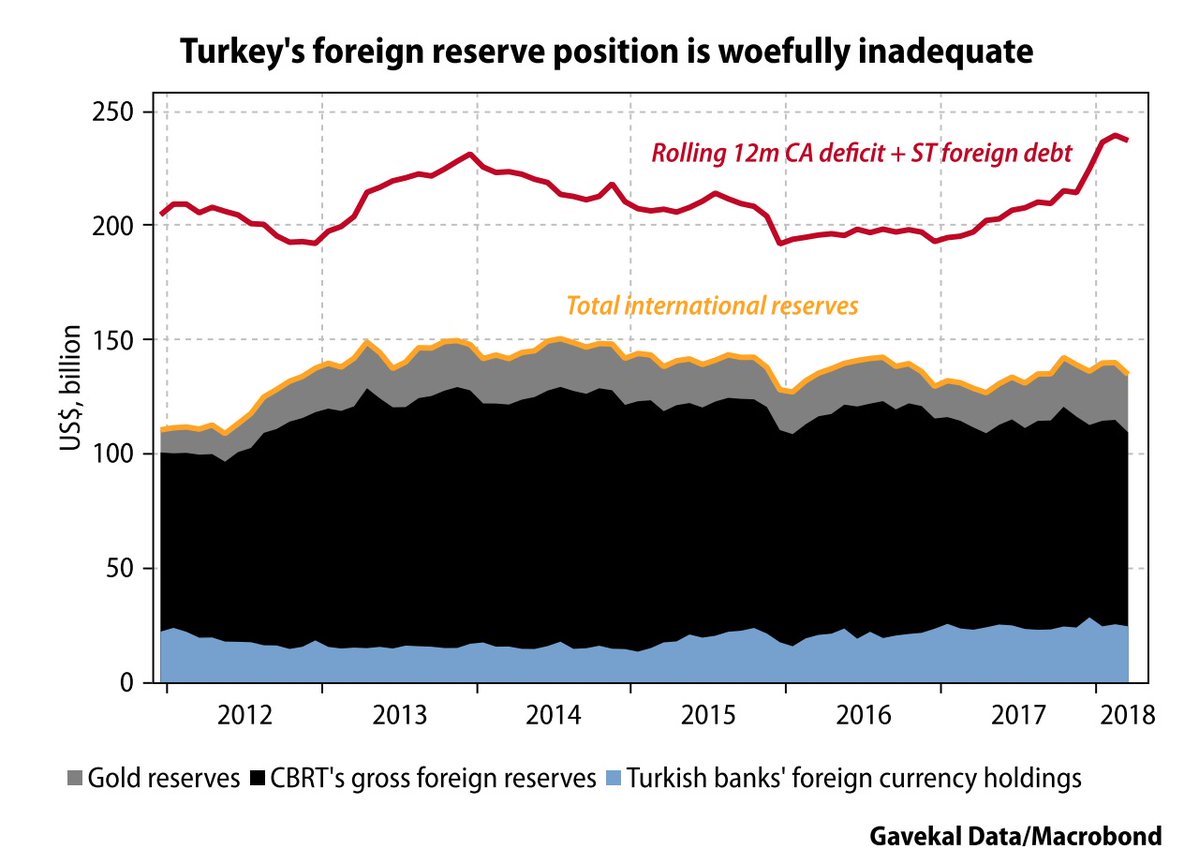

Turkey – reserves, current account & short term foreign debt

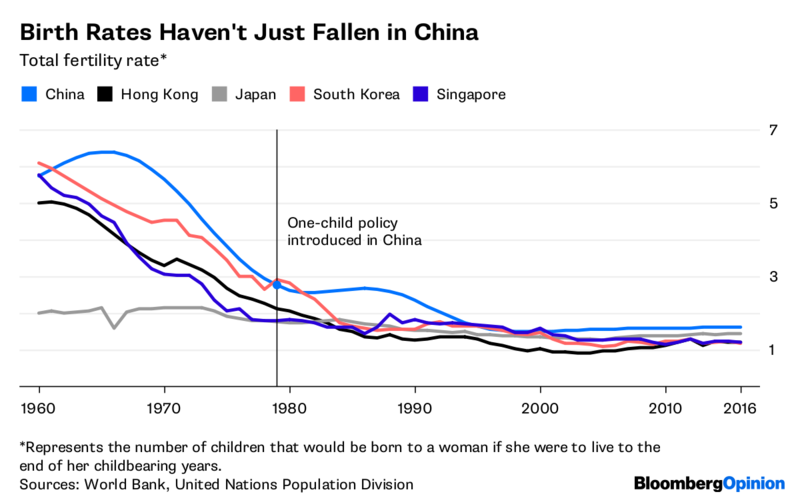

Asia – Selected Birth Rates

Europe

Europe – Brexit and its impacts

Europe – Collective Action Clauses & Debt

Europe – Electricity Generation

Europe – Steel Exports the the United States

Europe – National Debt to GDP

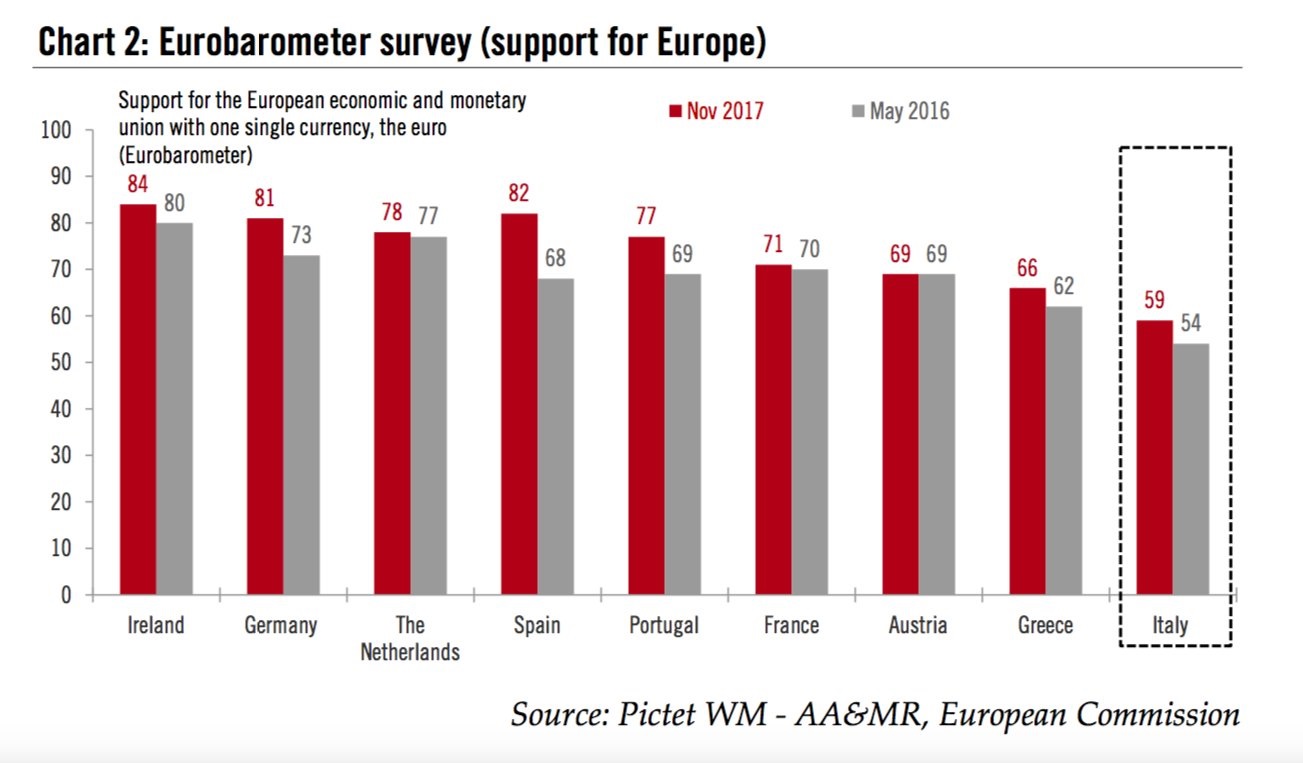

Europe – Eurobarometer

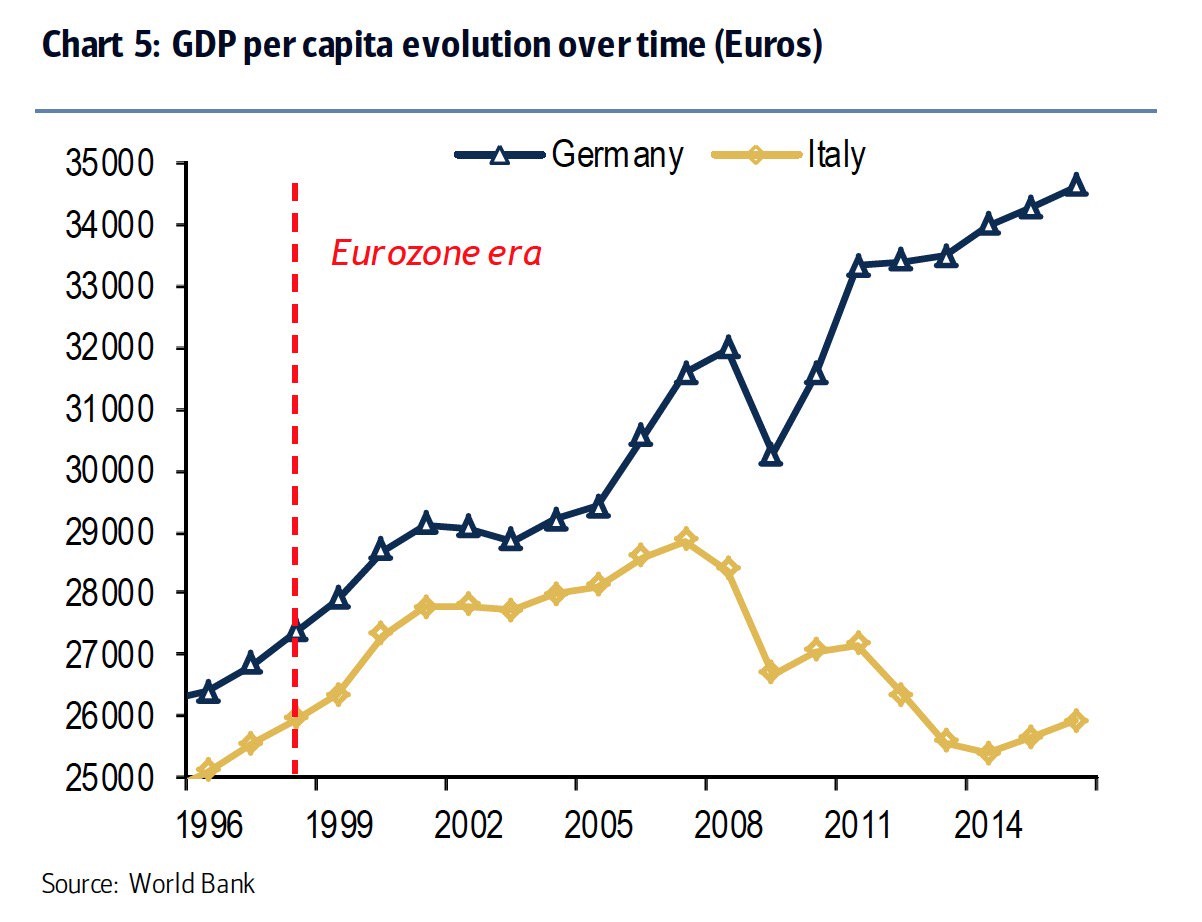

Germany & Italy – GDP per capita 1

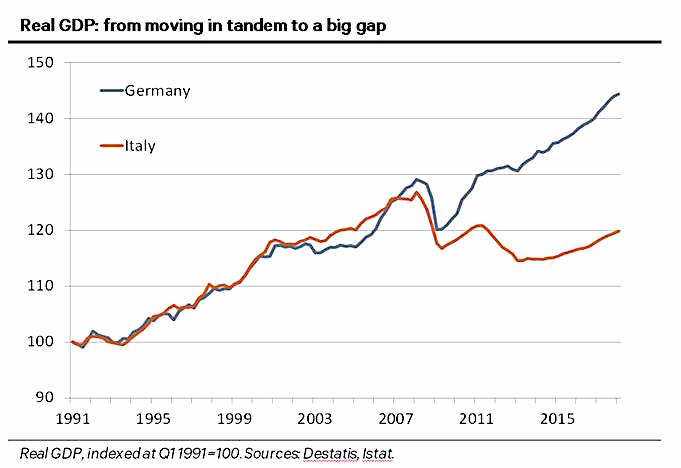

Germany & Italy – Real GDP 2

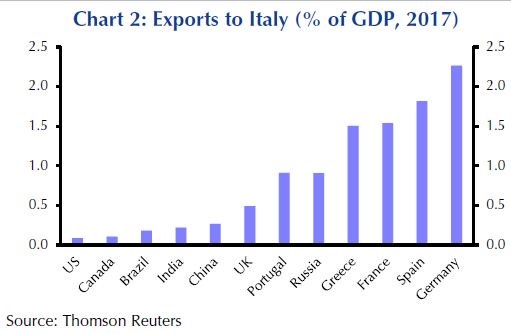

Italy as export destination – selected countries

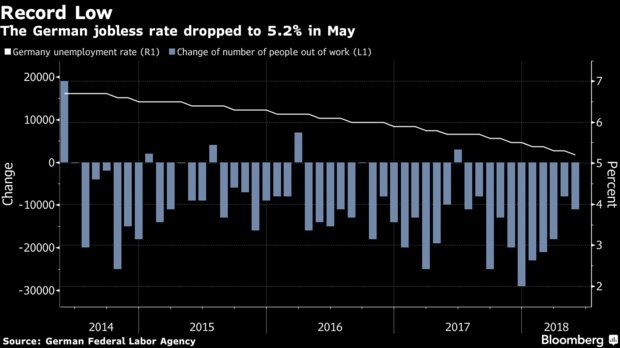

Germany – Unemployment

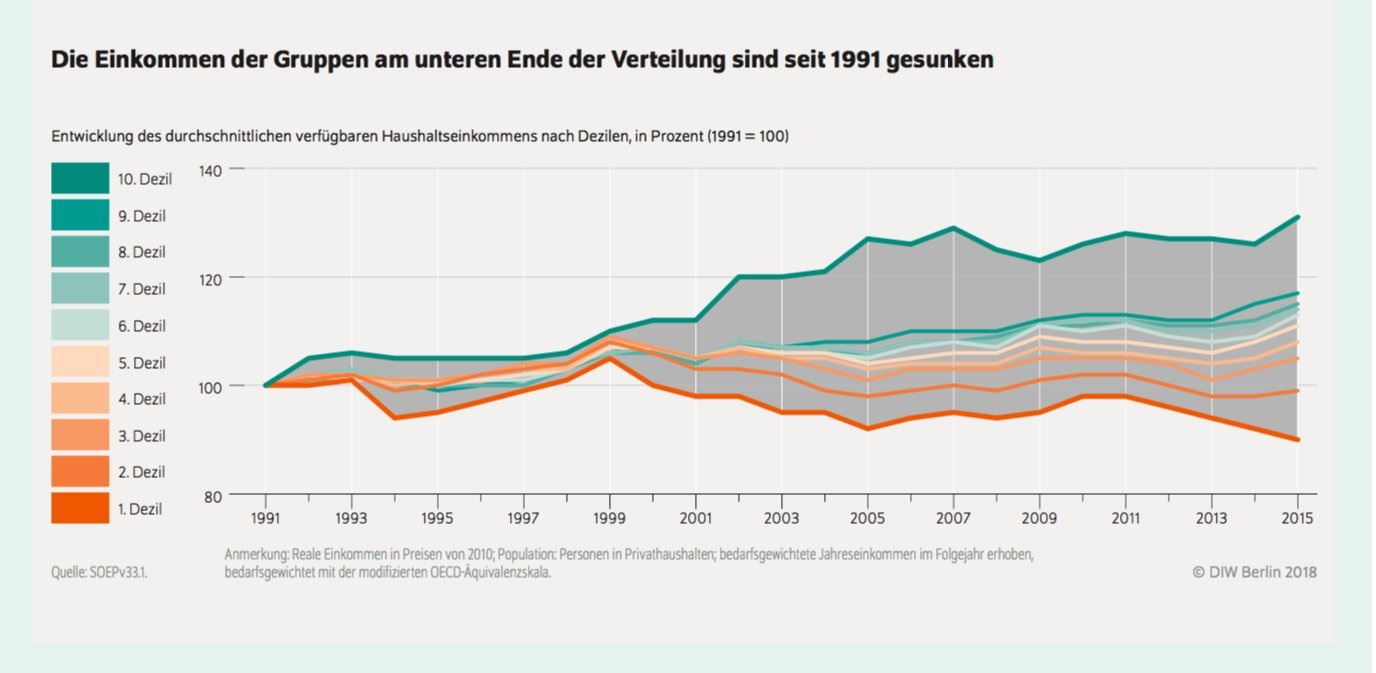

Germany – Income outcomes by decile since 1991 (in Deutsch)

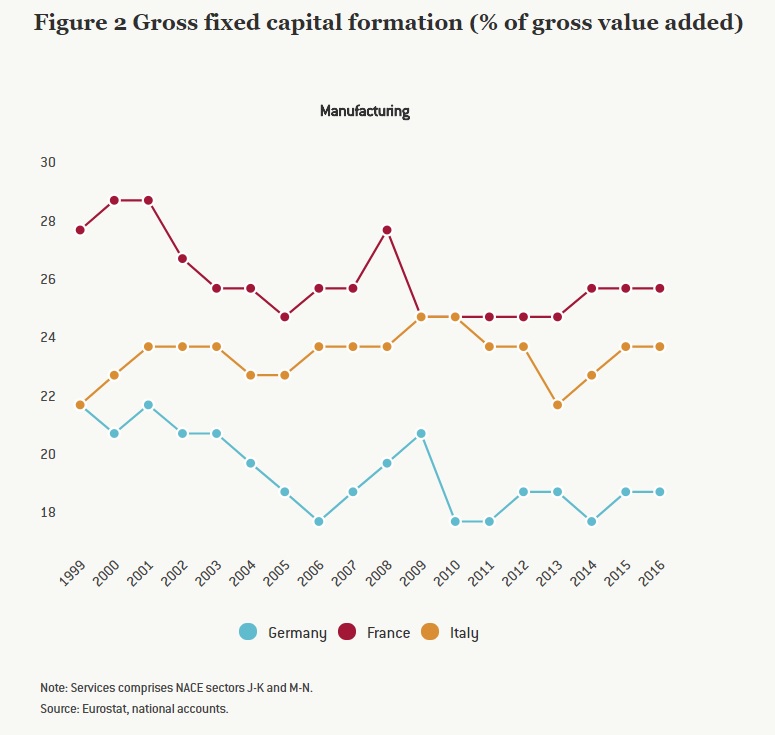

Germany France & Italy – Manufacturing Gross fixed Capital Formation

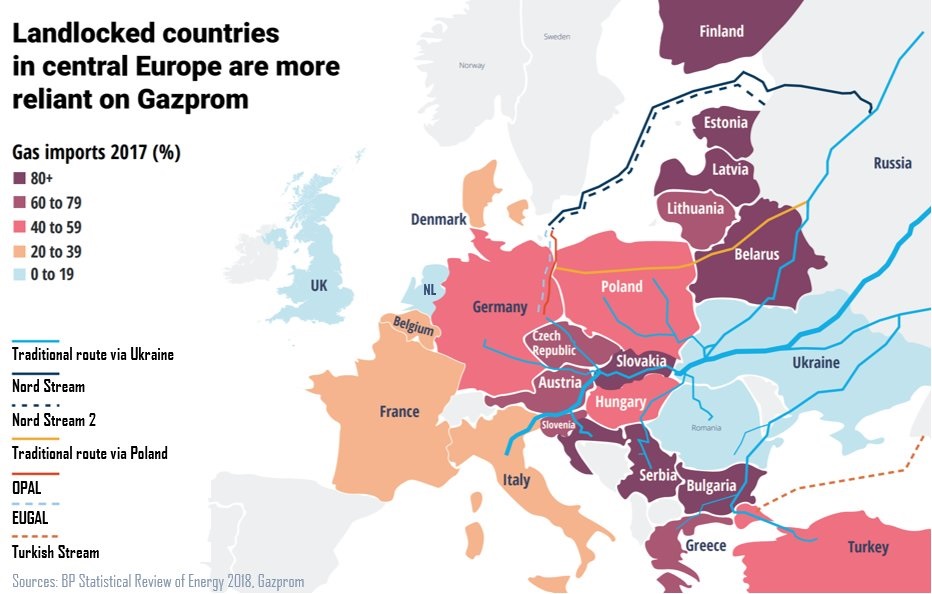

Europe – reliance on Gazprom (Russian gas)

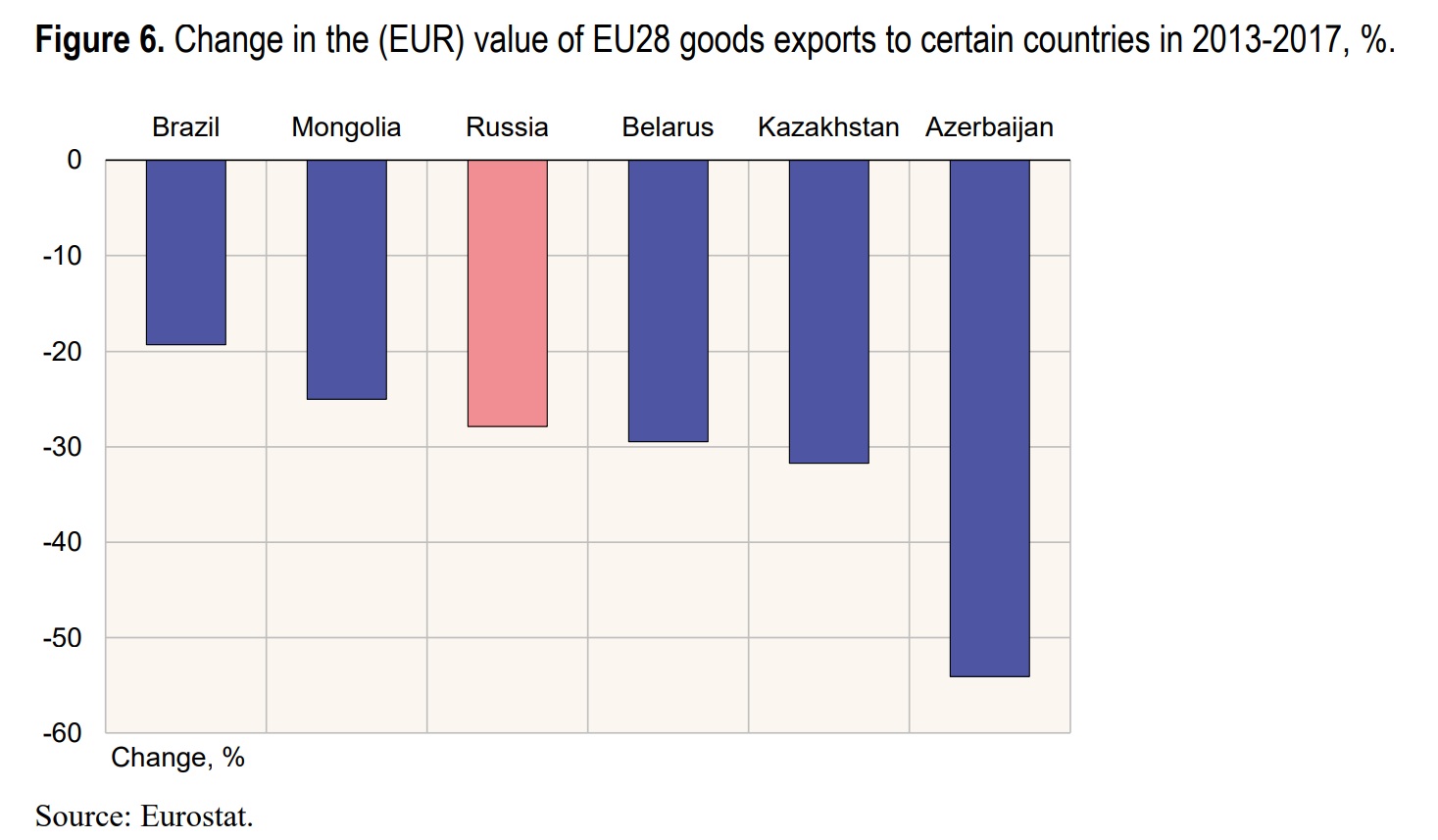

Europe – Selected markets changes to exports

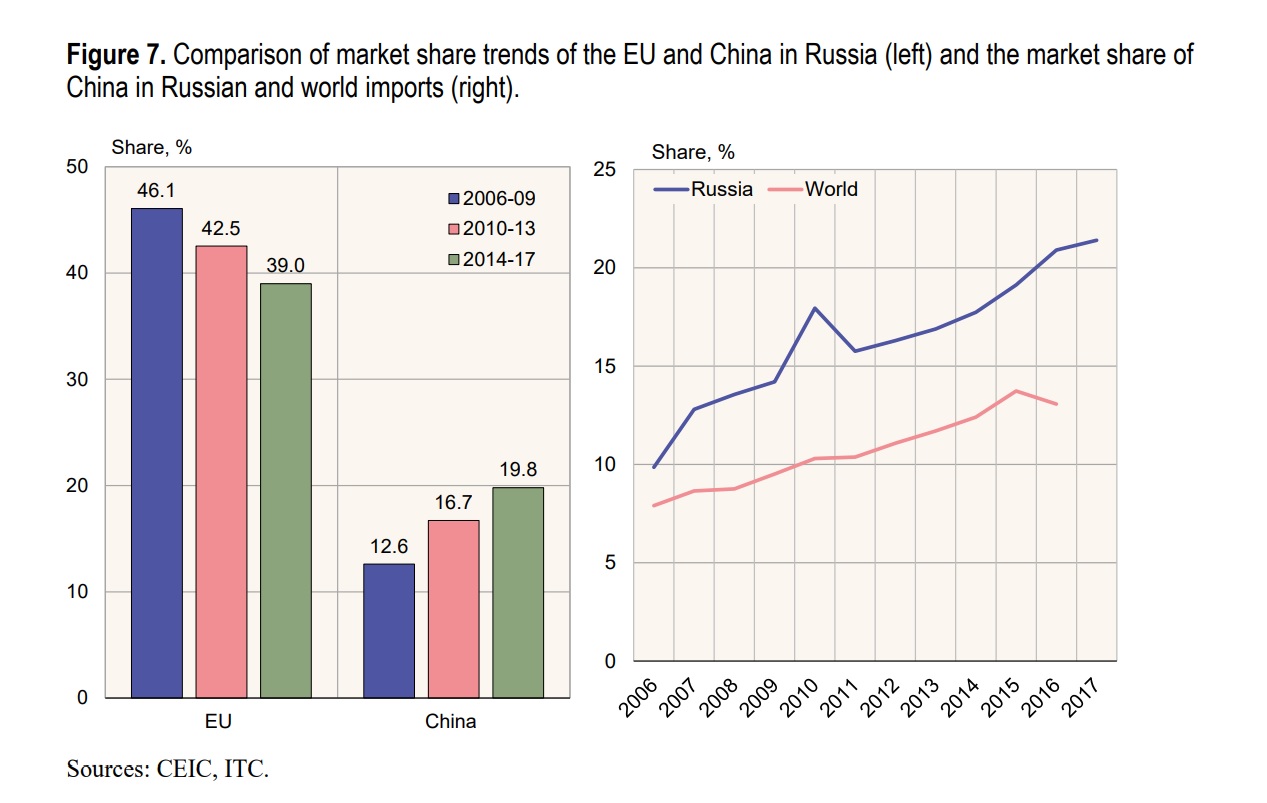

Russia – looking East

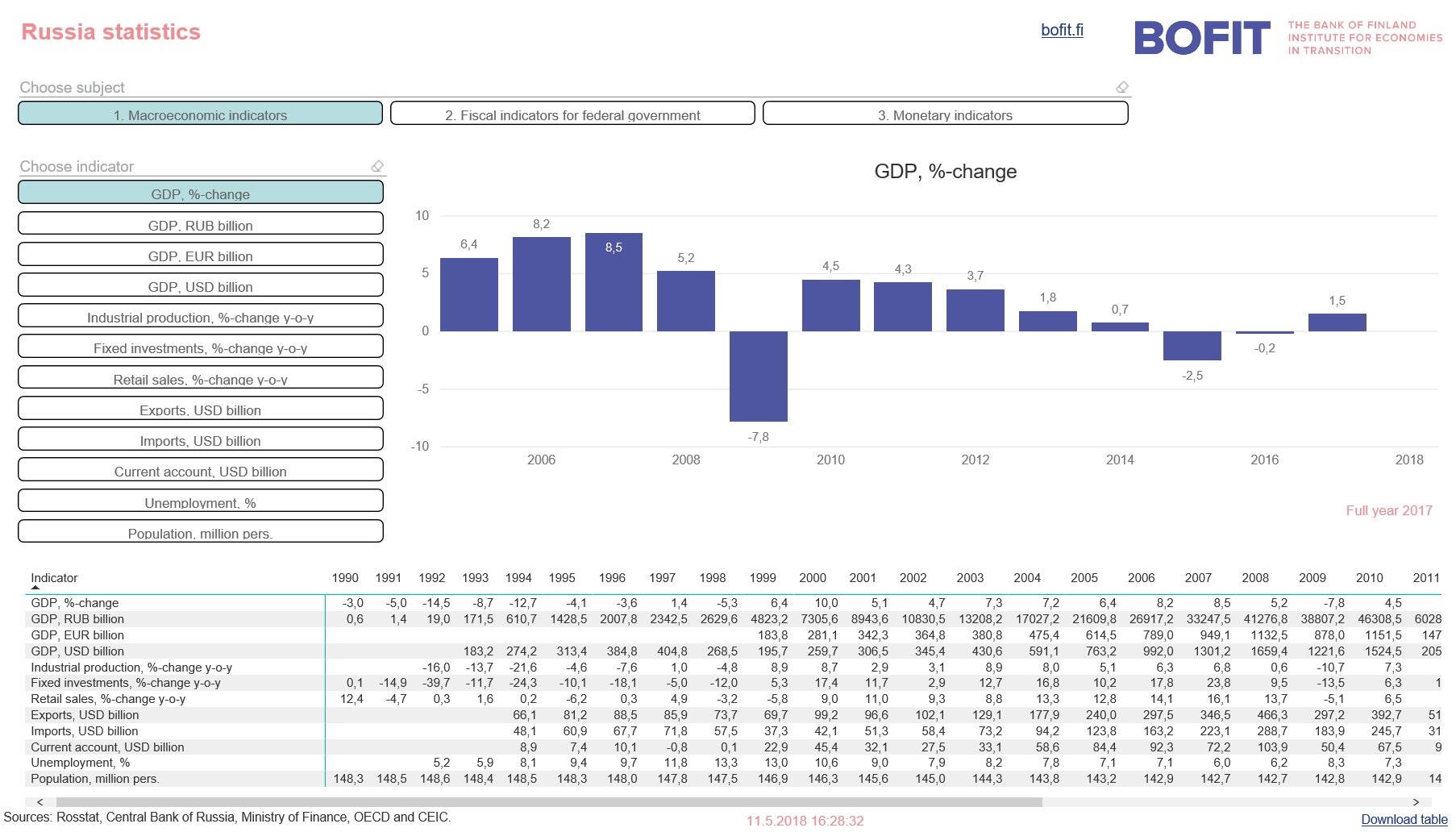

Russia GDP

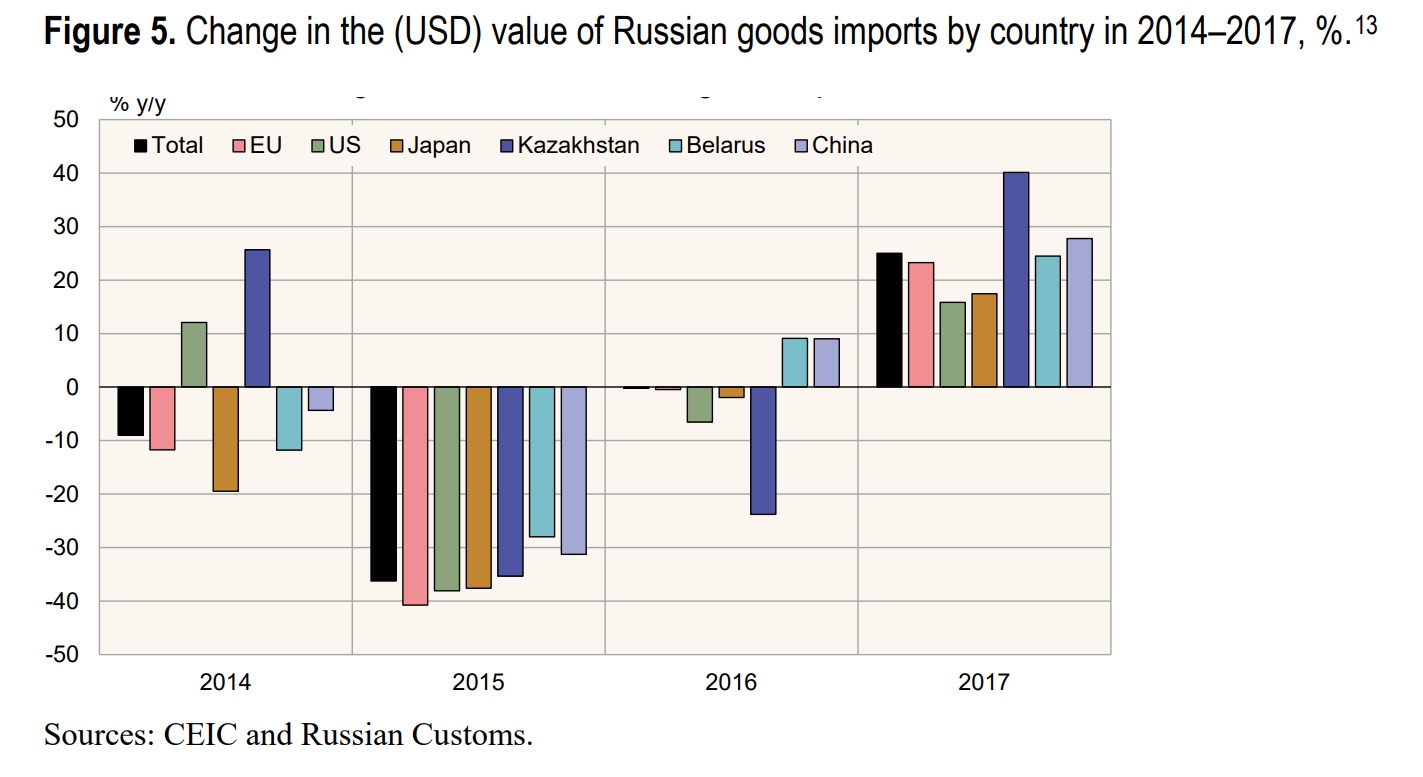

Russian Goods Imports – Selected nations by value

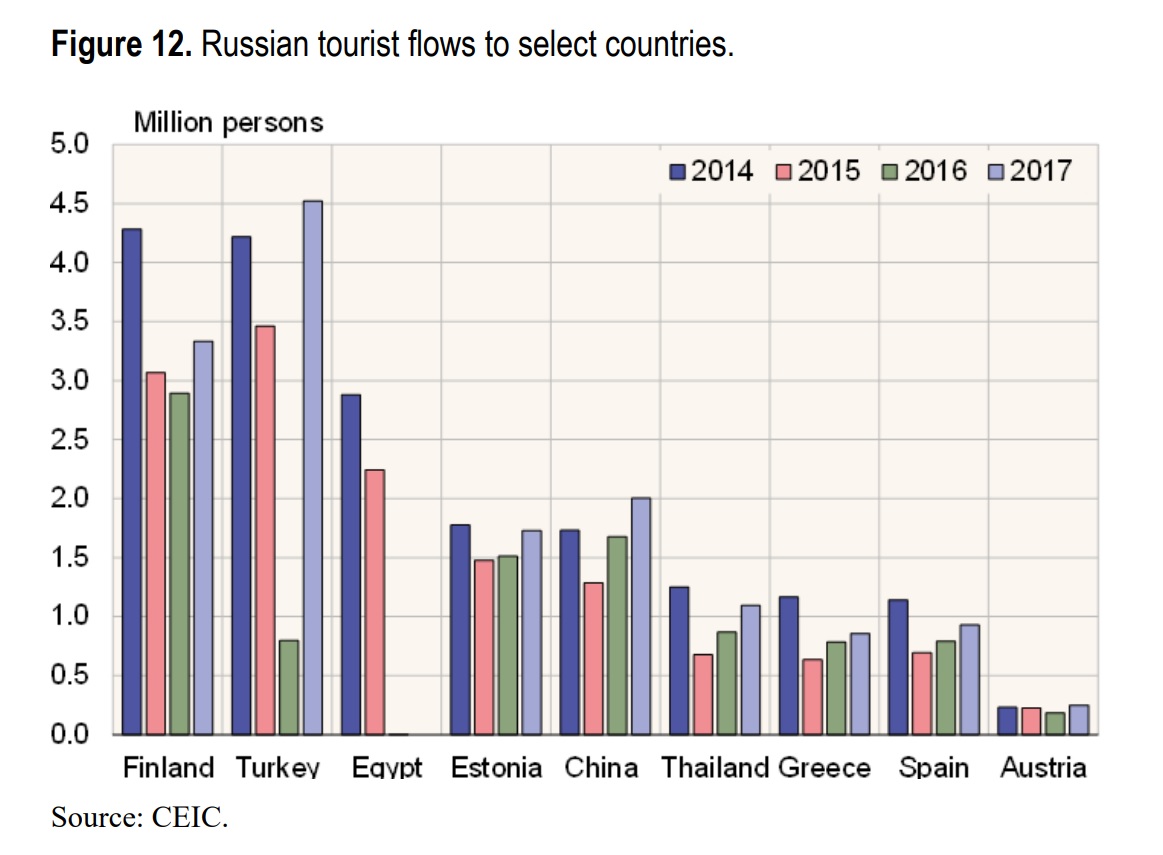

Russian Tourists (explains some of Erdogan’s actions)

Russian Tourists – become a big factor when crude prices rise

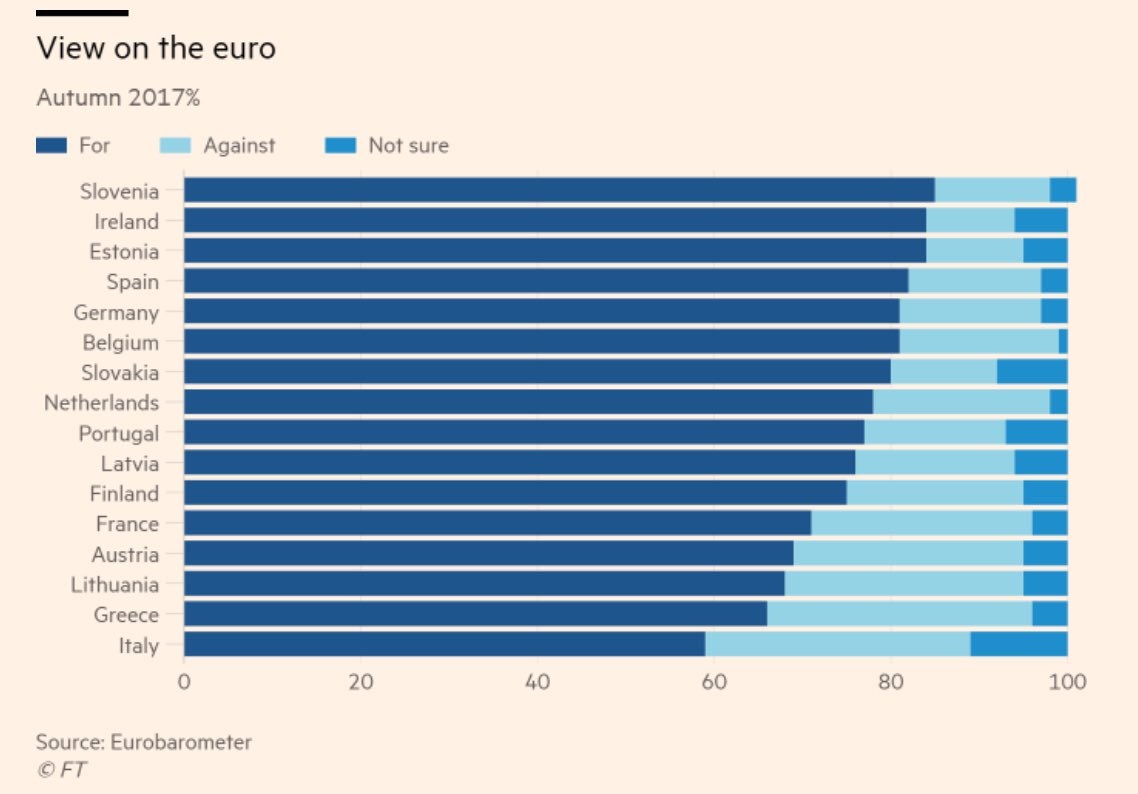

Europe – sentiment on the Euro

Switzerland – GDP Growth

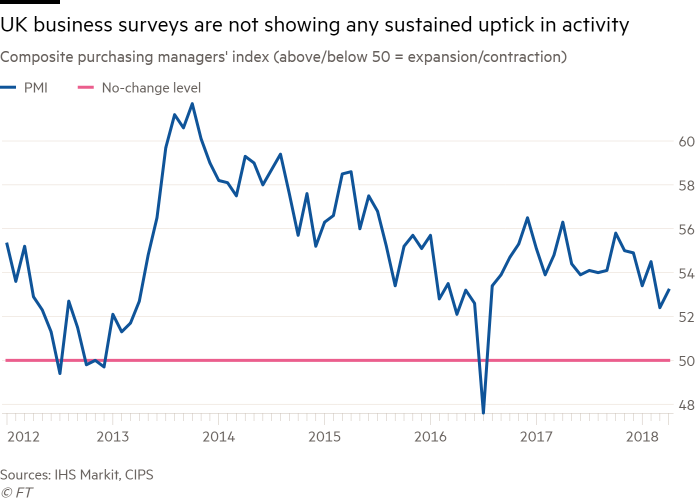

United Kingdom – composite PMIs

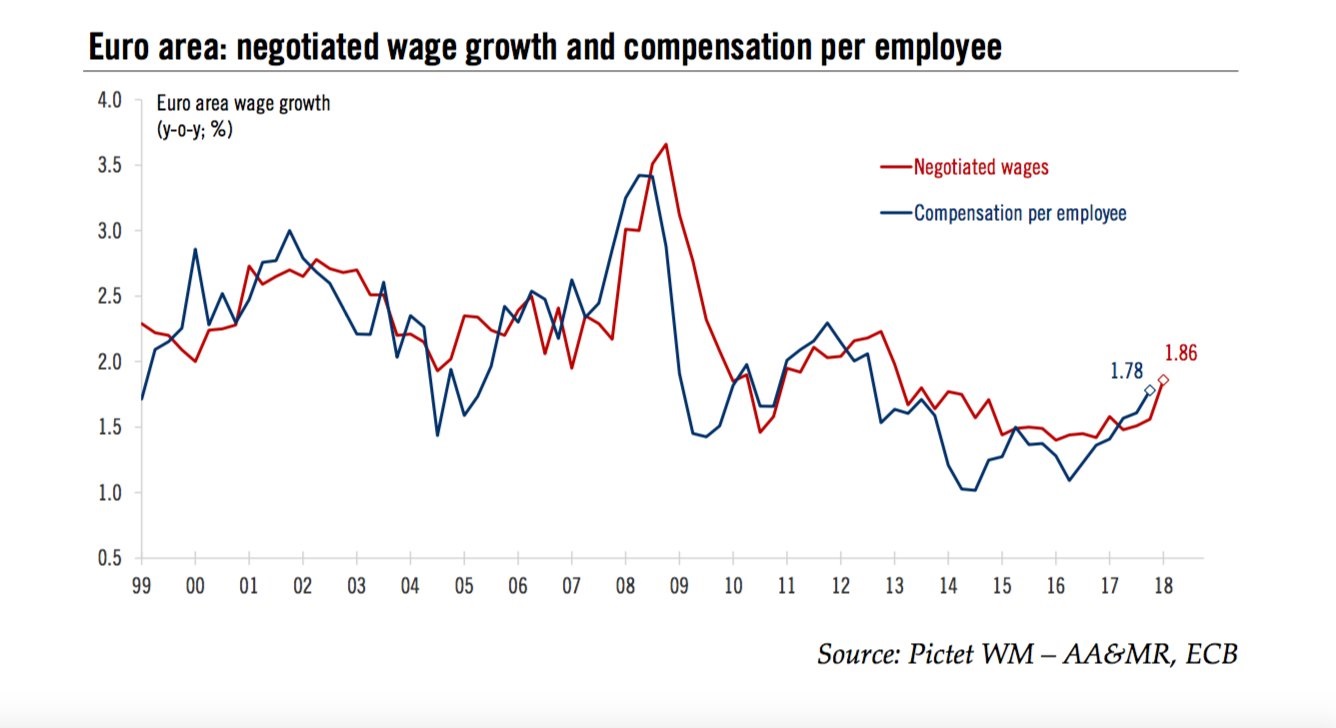

Euro Area – Negotiated Wage growth

Commodities

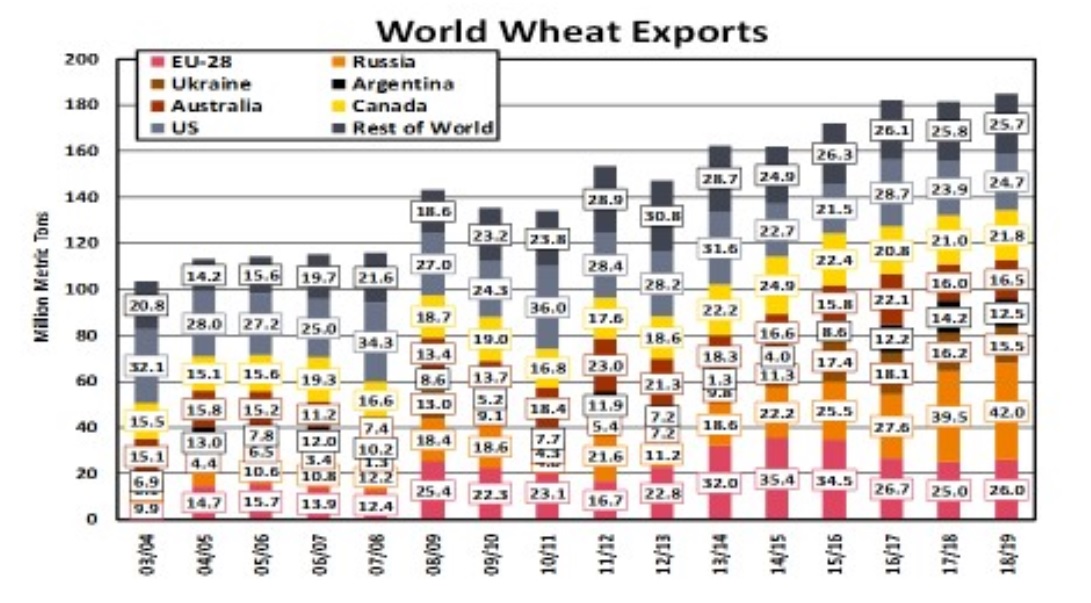

Wheat Exports

Wool

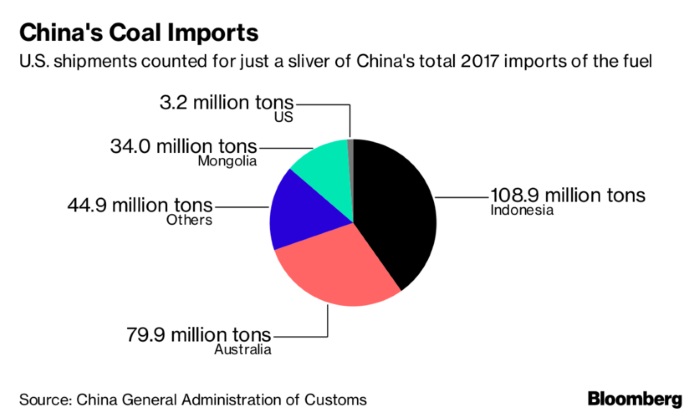

China Coal Imports

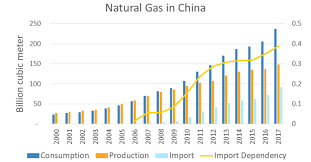

China Natural Gas – production & imports

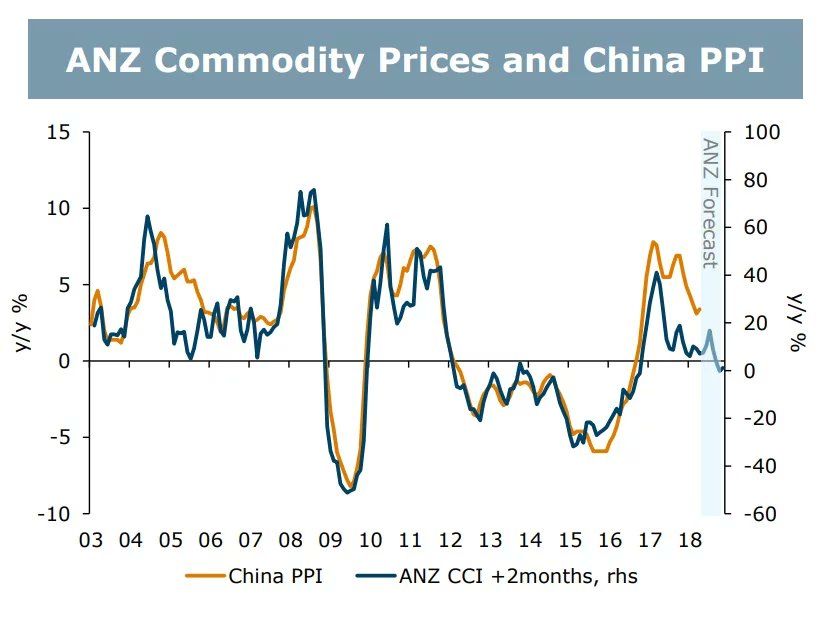

Commodities & China PPI

China Steel Margins

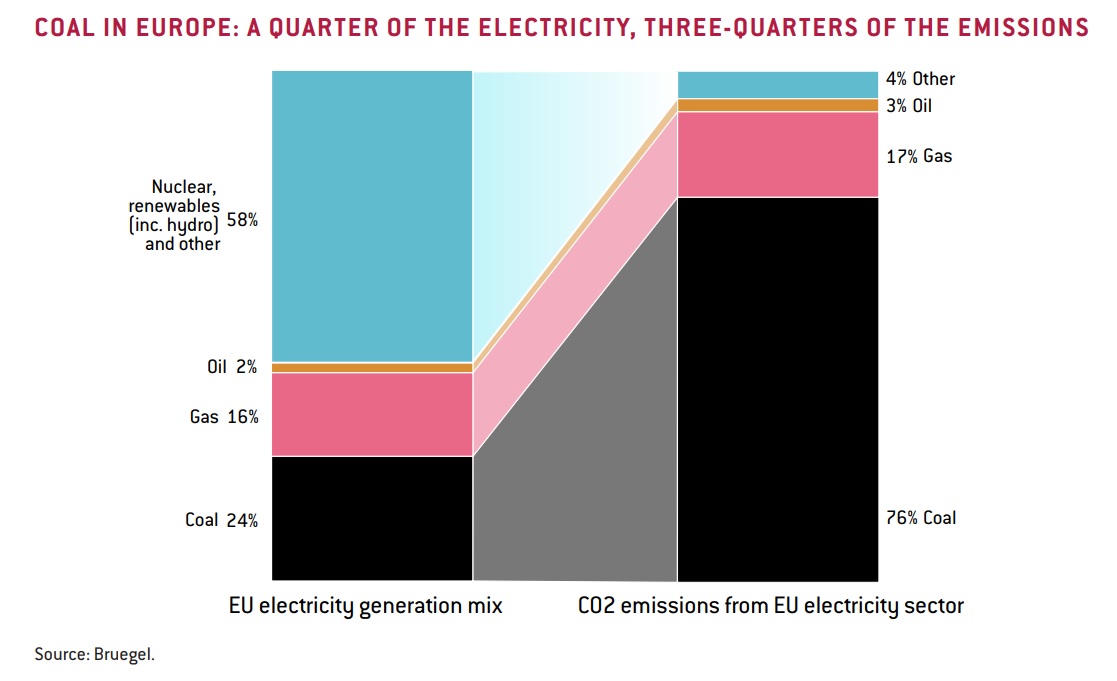

Eurozone – electricity production sources

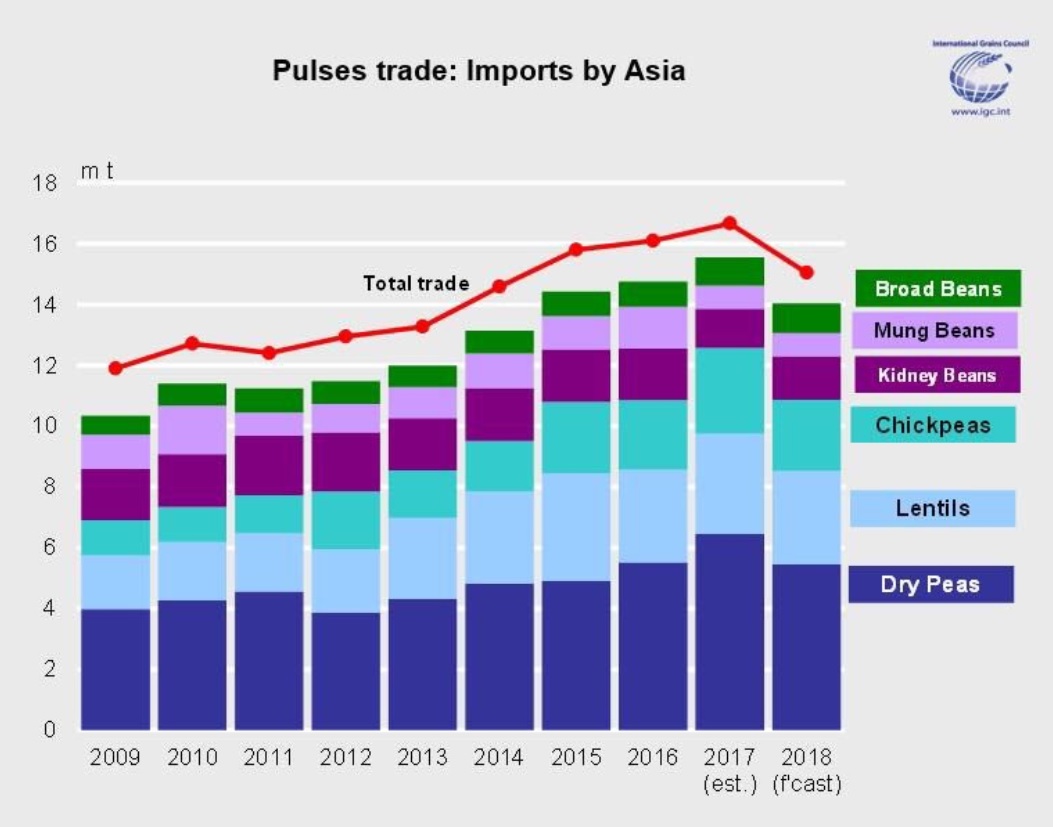

Asian Pulse imports

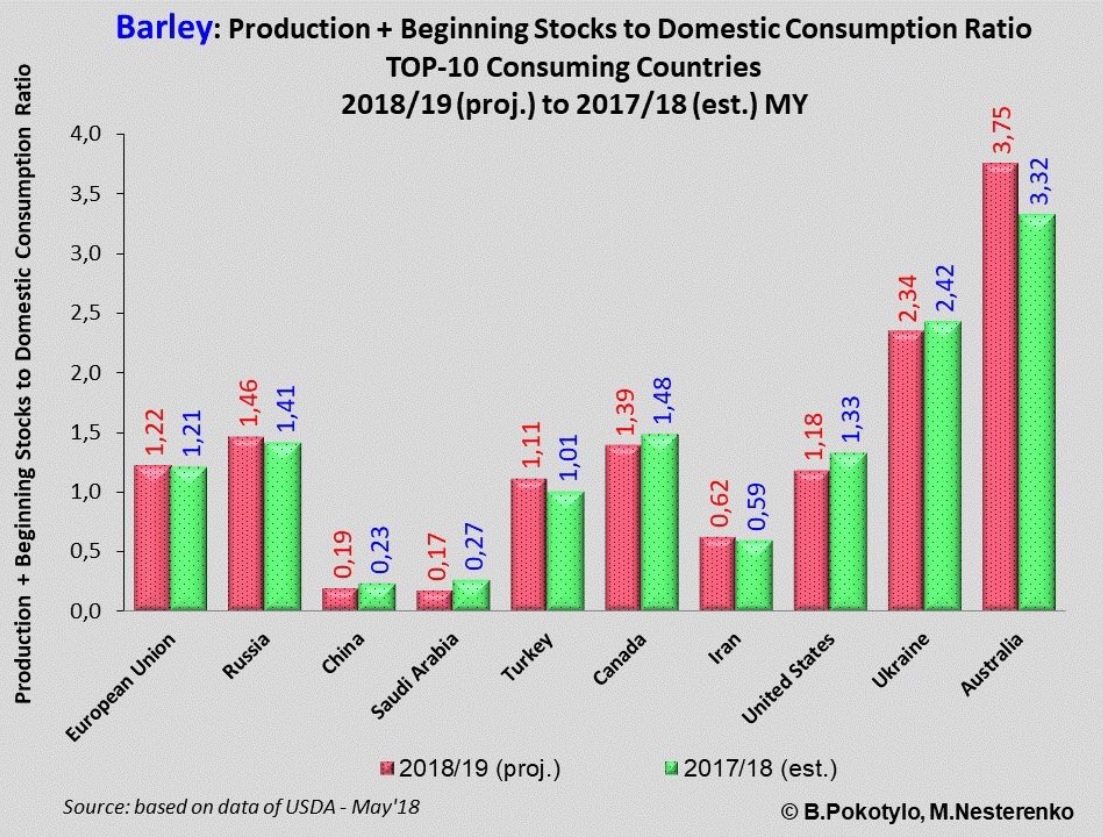

Barley production

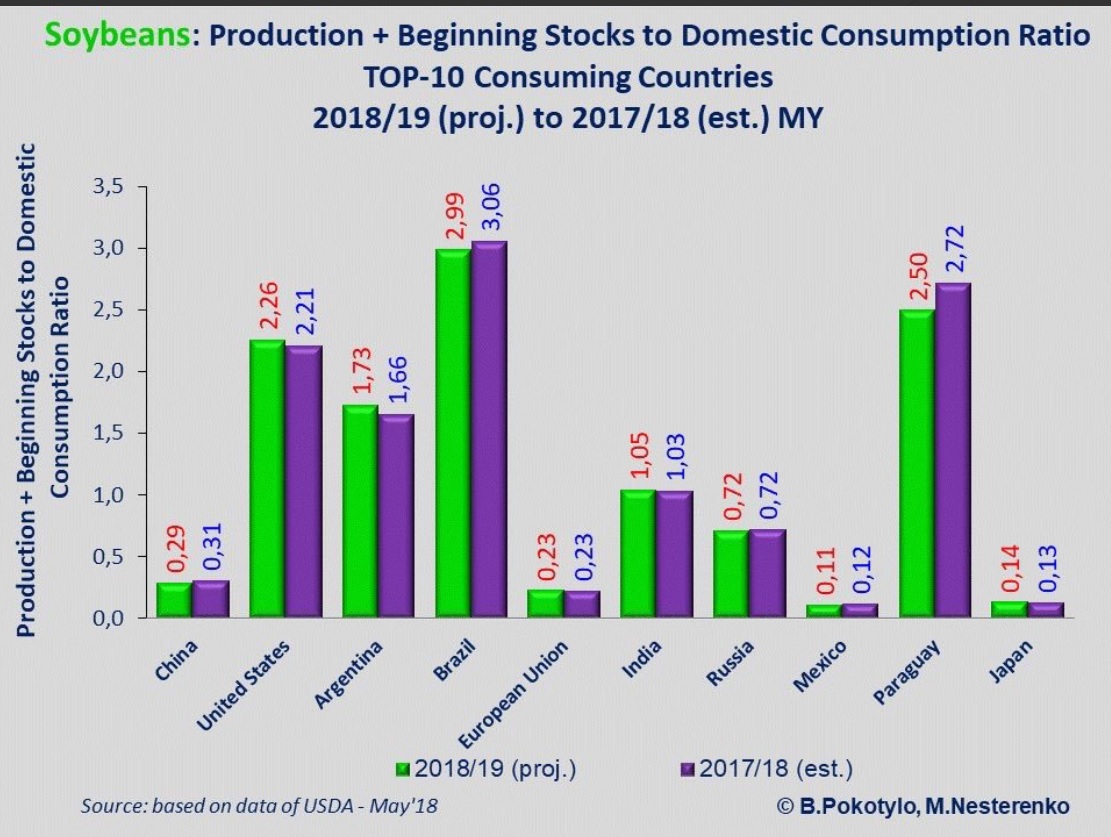

Soybean Production

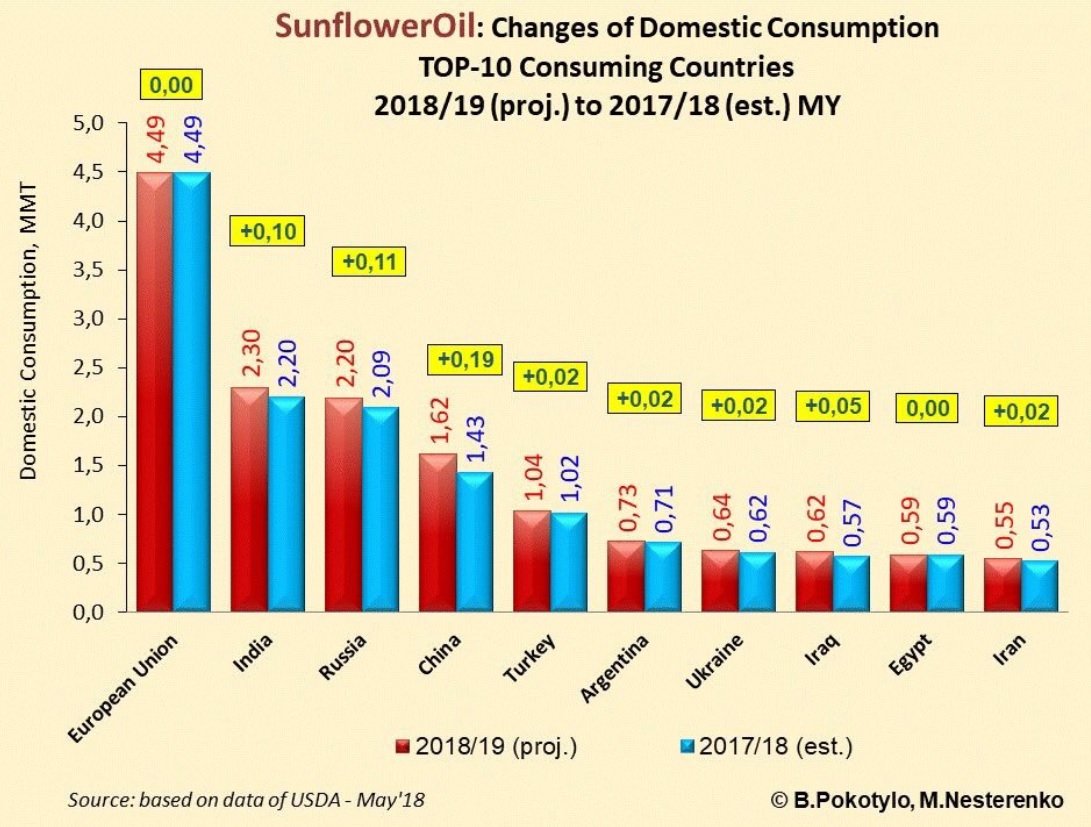

Sunflower oil consumption

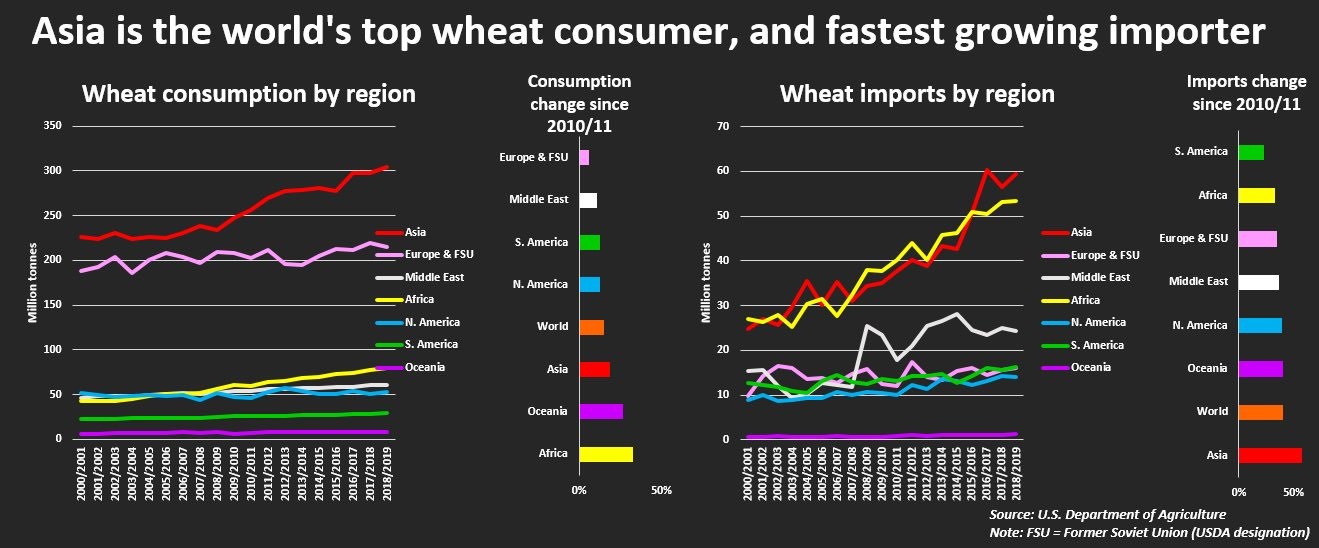

Asian wheat consumption & imports

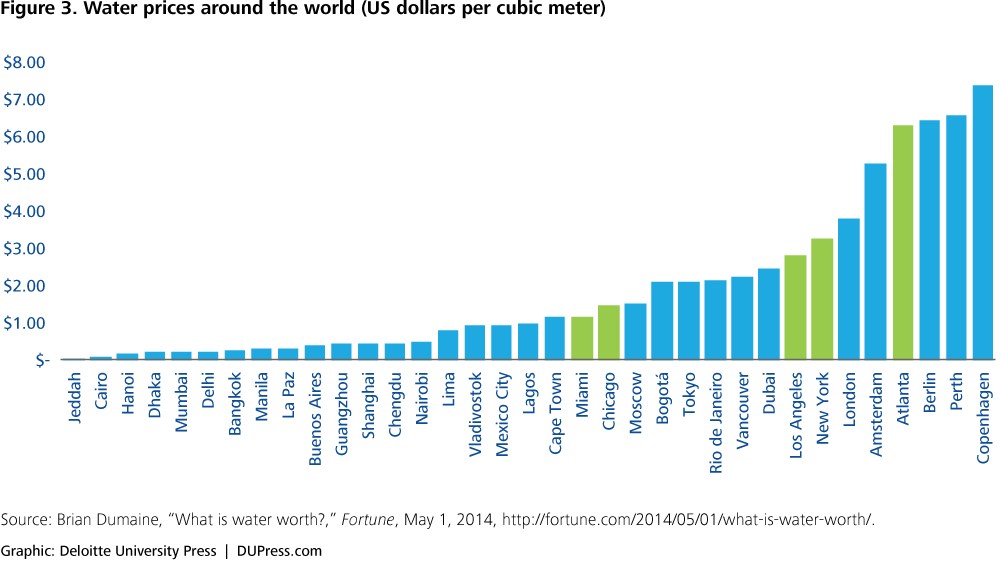

Global Water prices

Cocoa

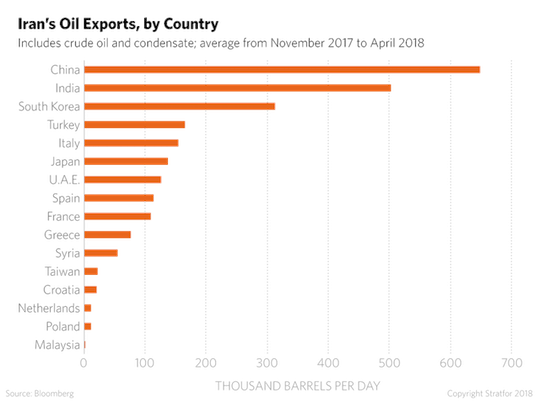

Iran – Oil Exports

Capital Markets

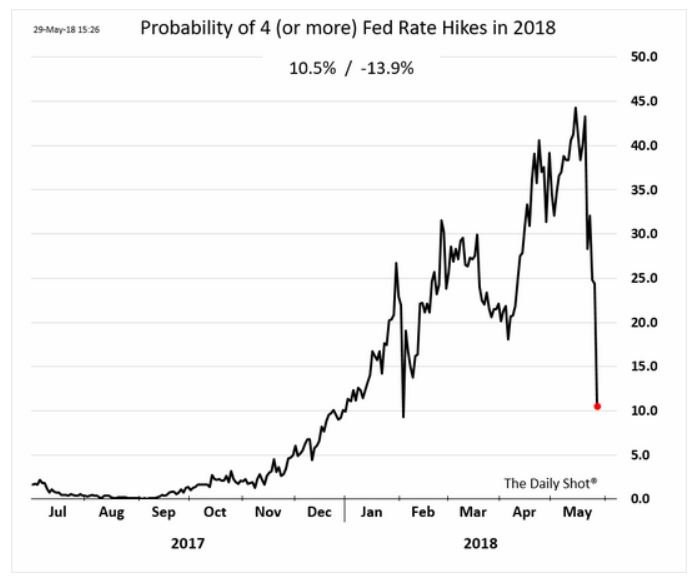

4 or more Federal Reserve Rate Hikes this year – Probability

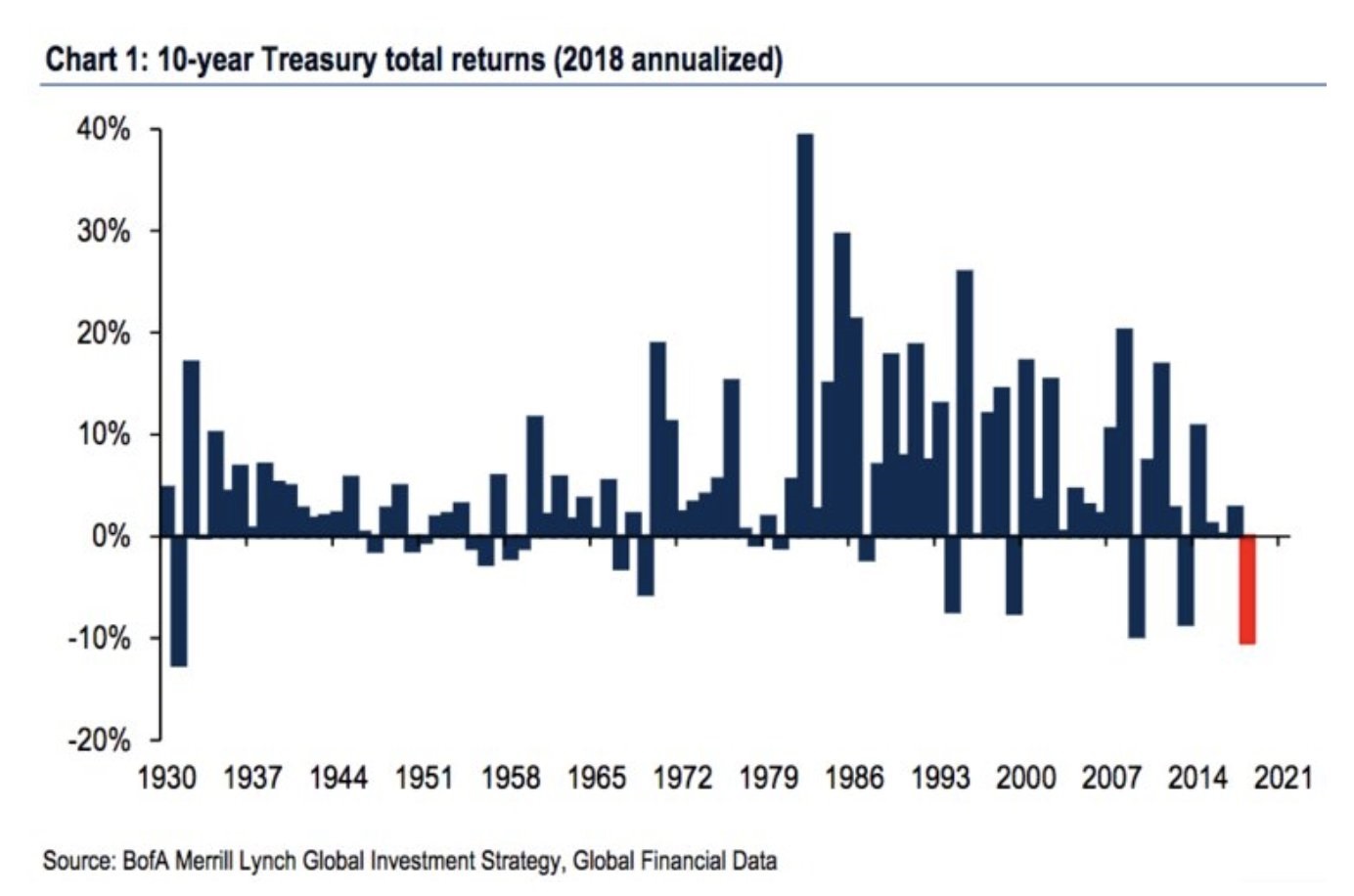

10 Years Returns

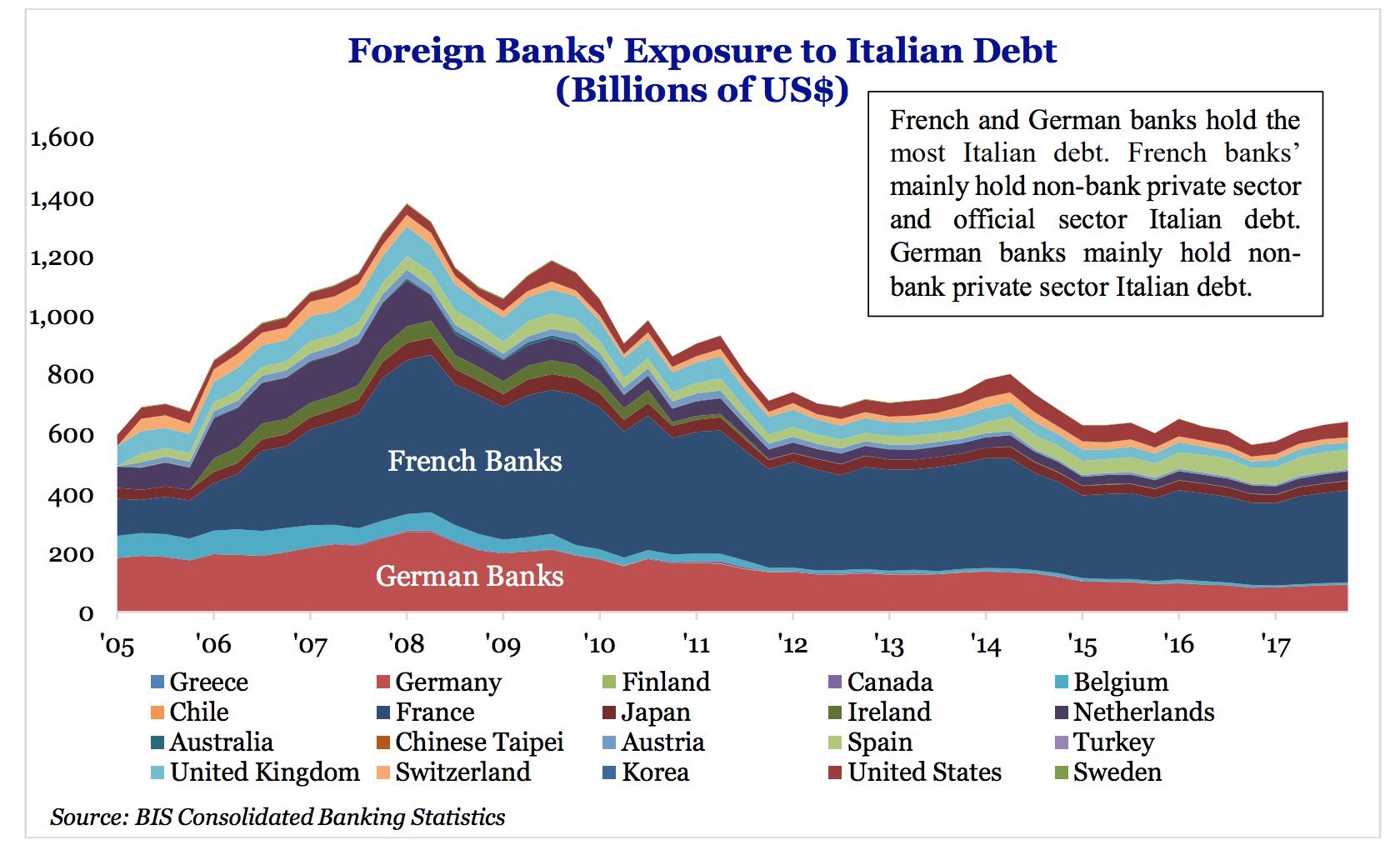

Exposure to Italian Debt

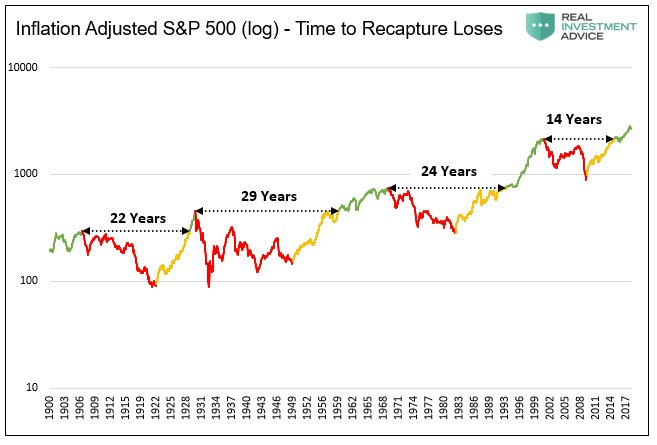

Inflation Adjusted S&P 500

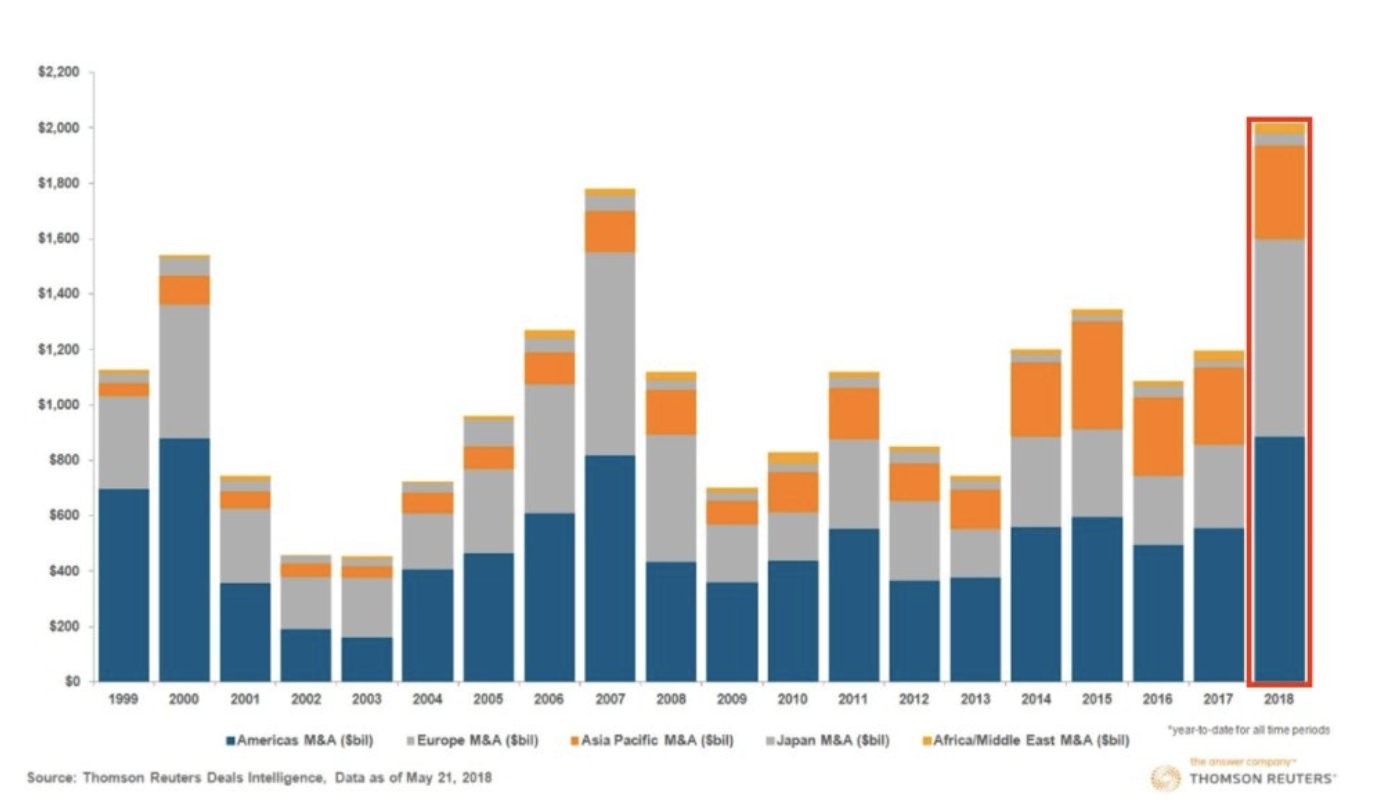

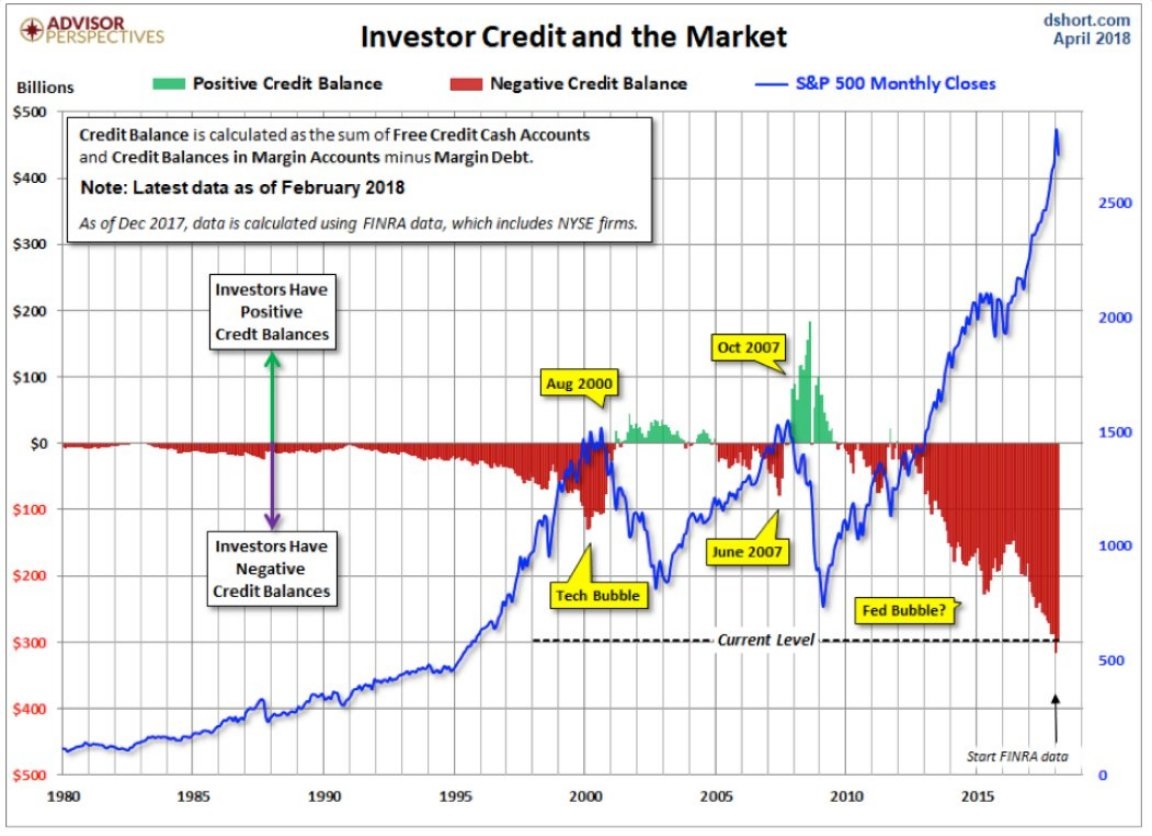

Merger and Acquisition activity reaching another peak (after 2000 & 2007)

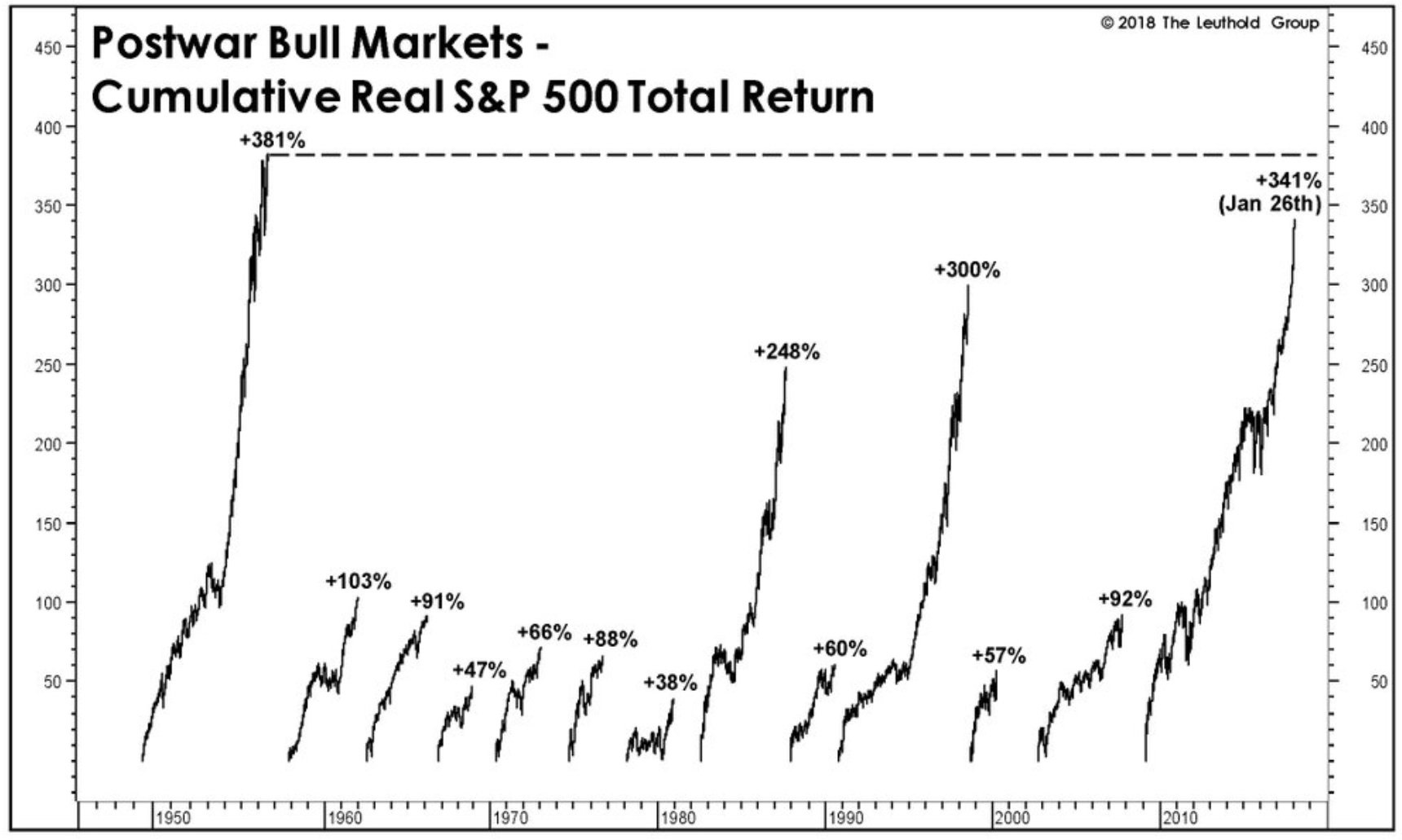

The Post War Bulls

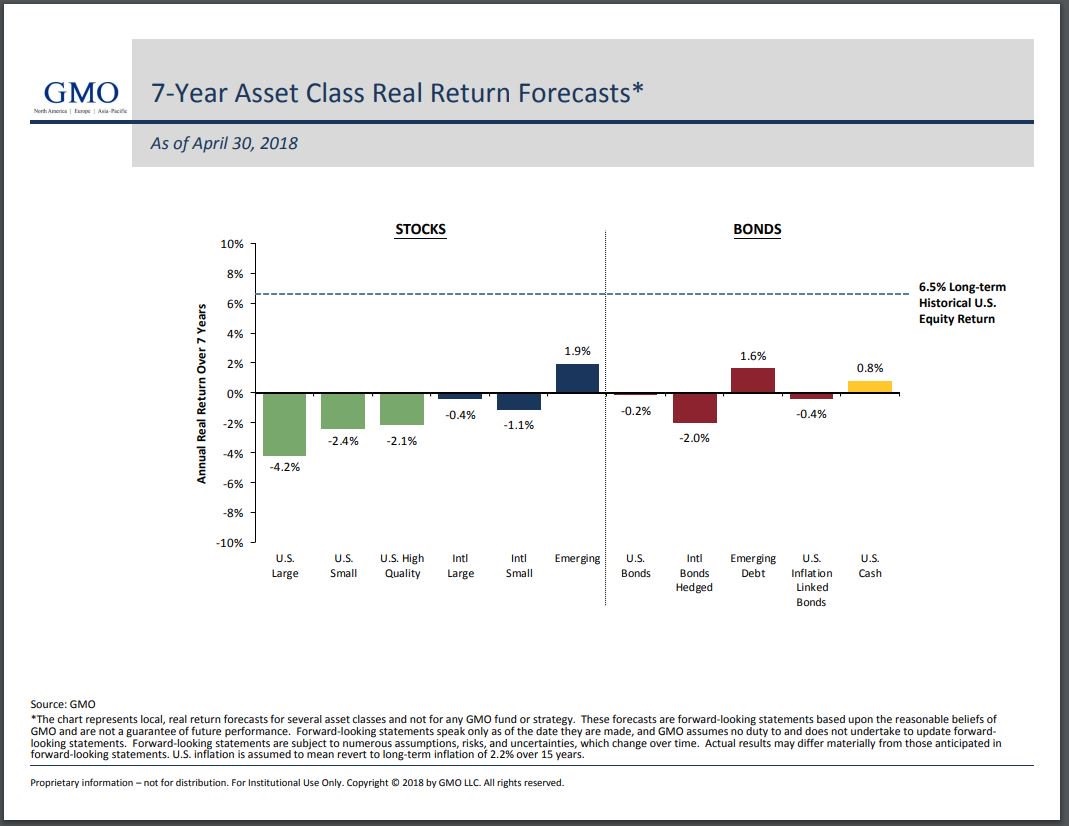

Asset Class Real Return Forecast (Emerging Debt and Equities or US Cash)

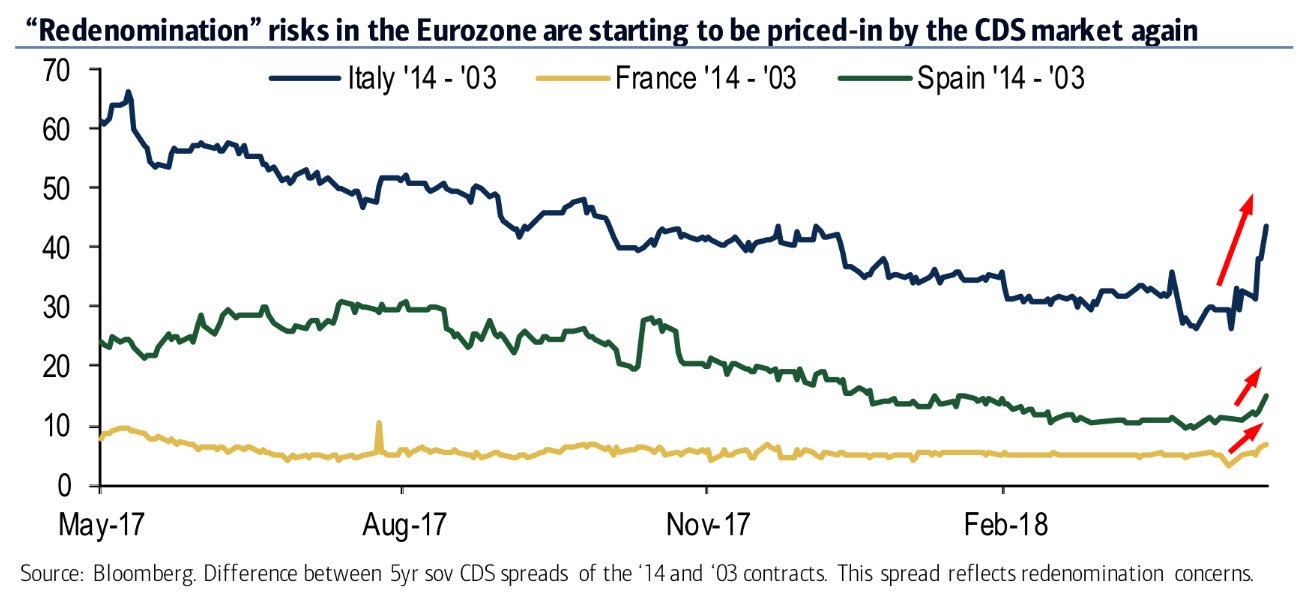

Eurozone – Redenomination Risks

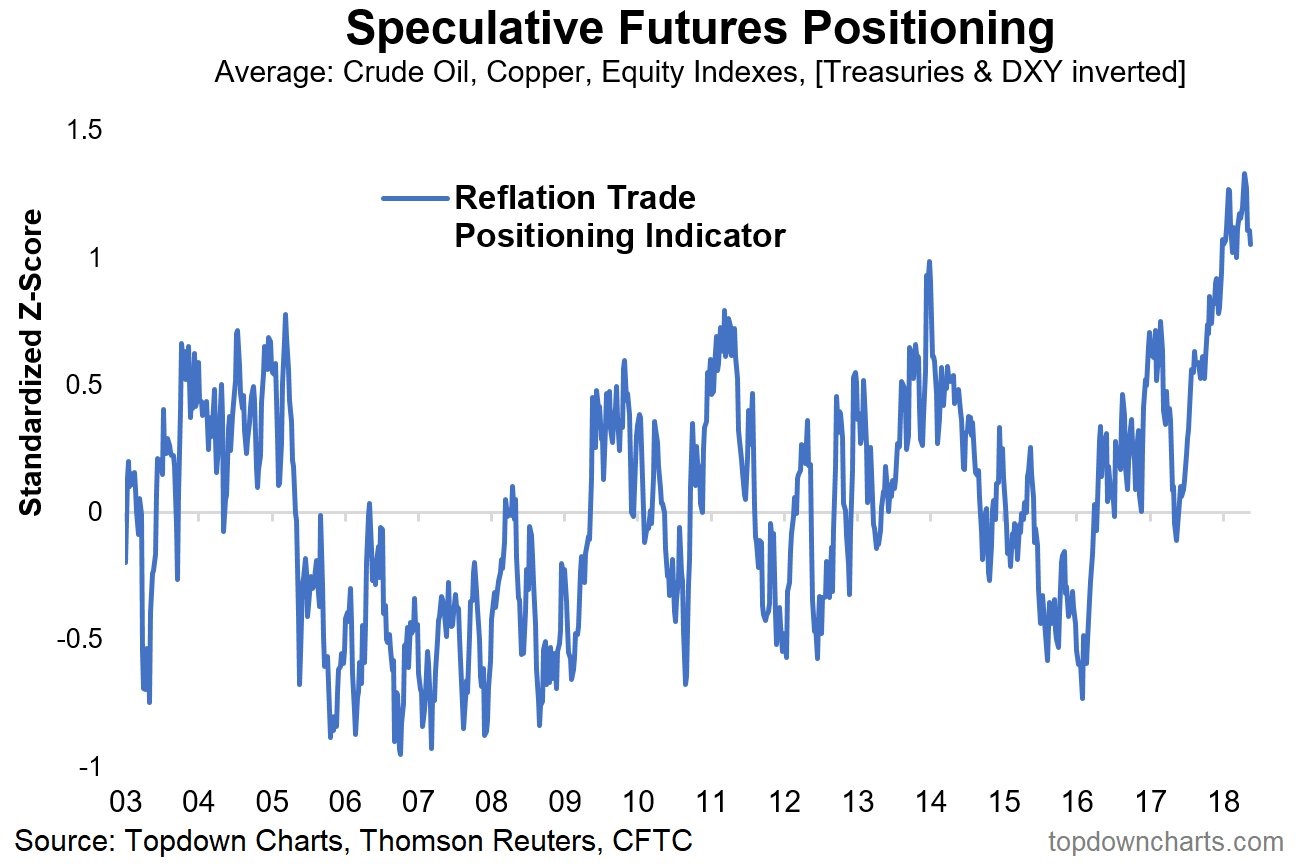

Speculative futures

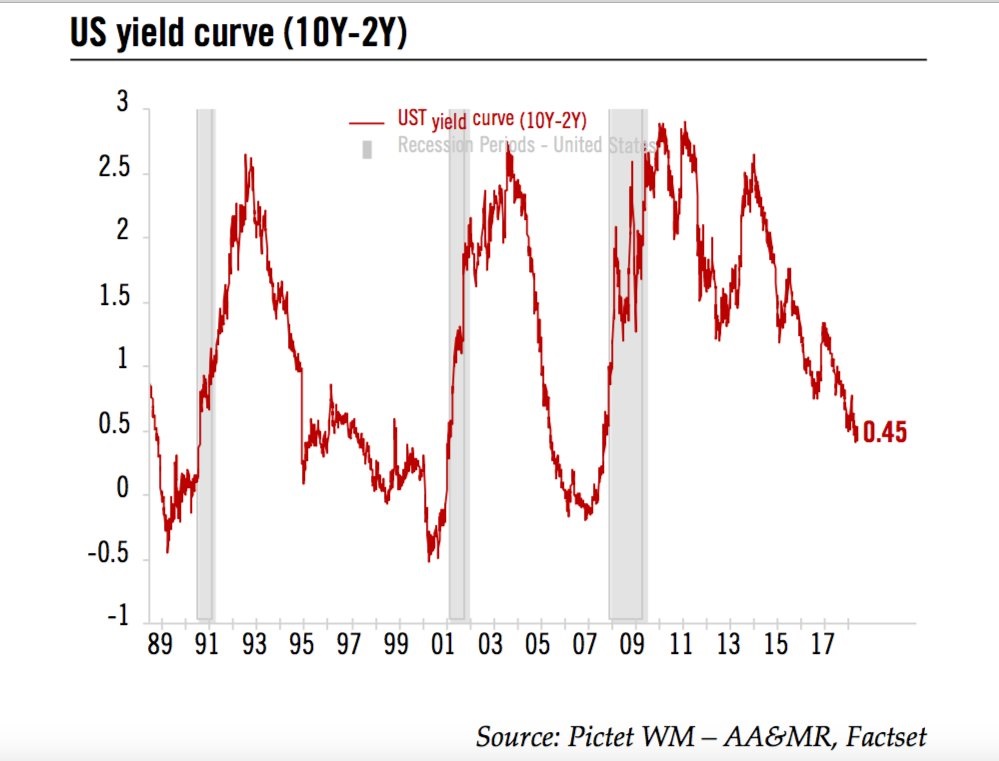

US 10s minus 2s

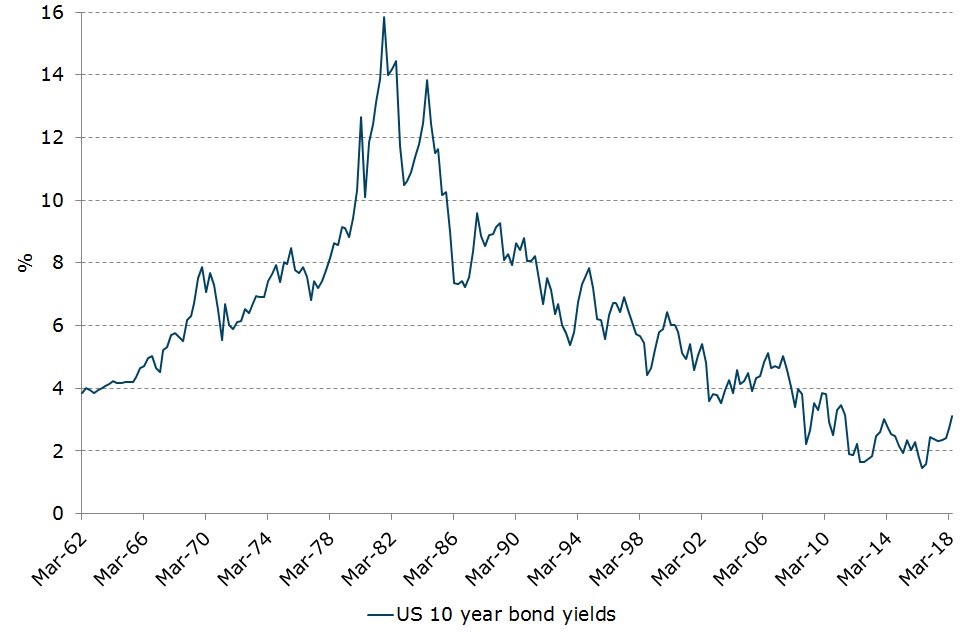

US 10 Year yields

Credit & Markets

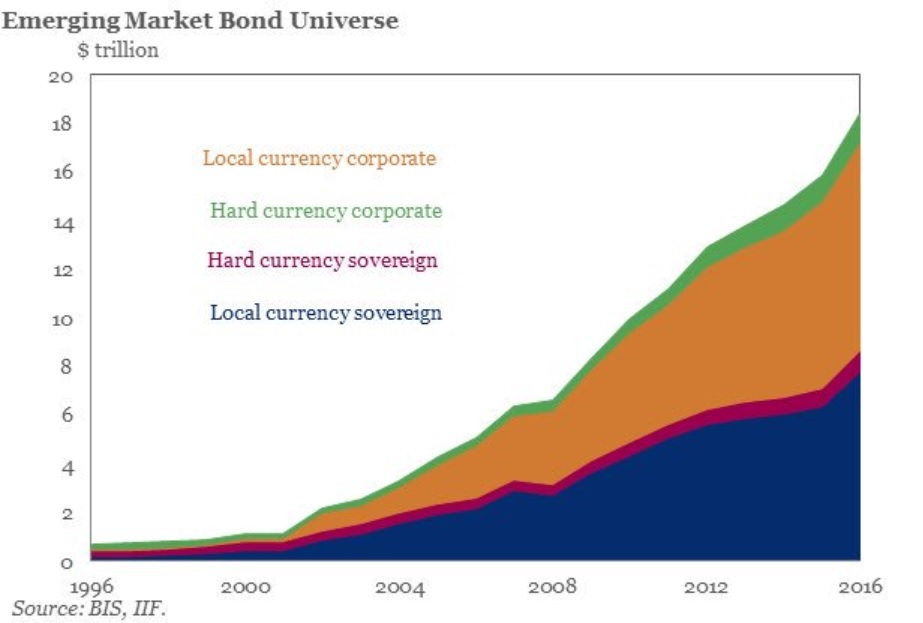

Emerging Market bonds

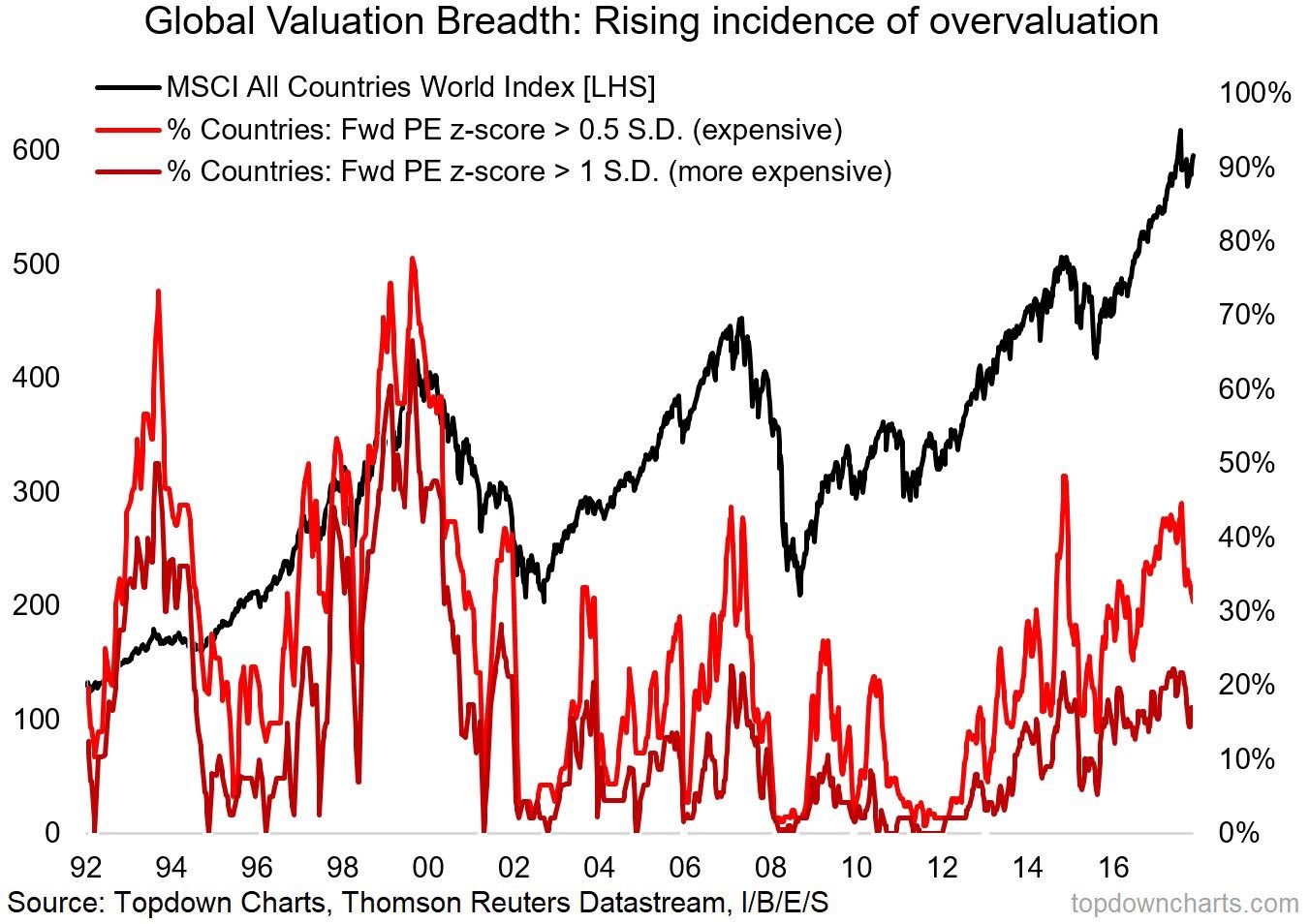

Global Valuations

Global Macro

Capital Labour Ratio

WTO and China related issues

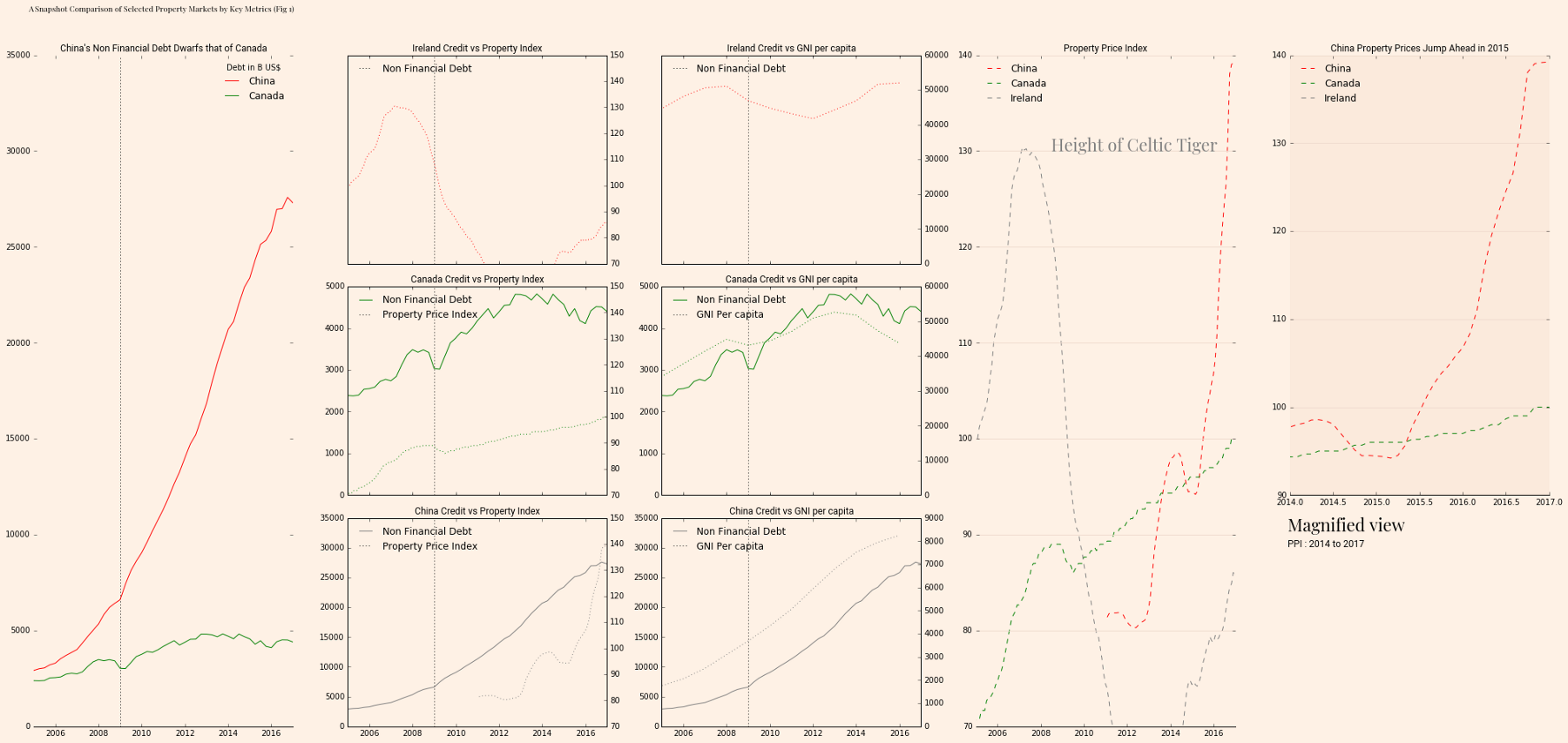

China, Ireland and Canada – Debt-Housing bubbles

Non Financial sector debt to GDP

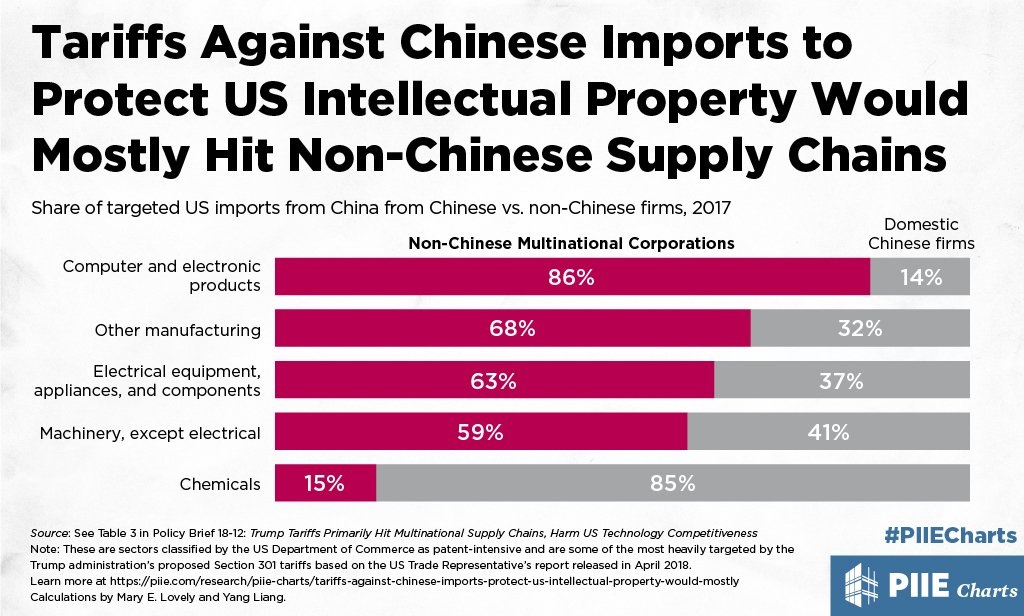

Potential Impact of China Tariffs

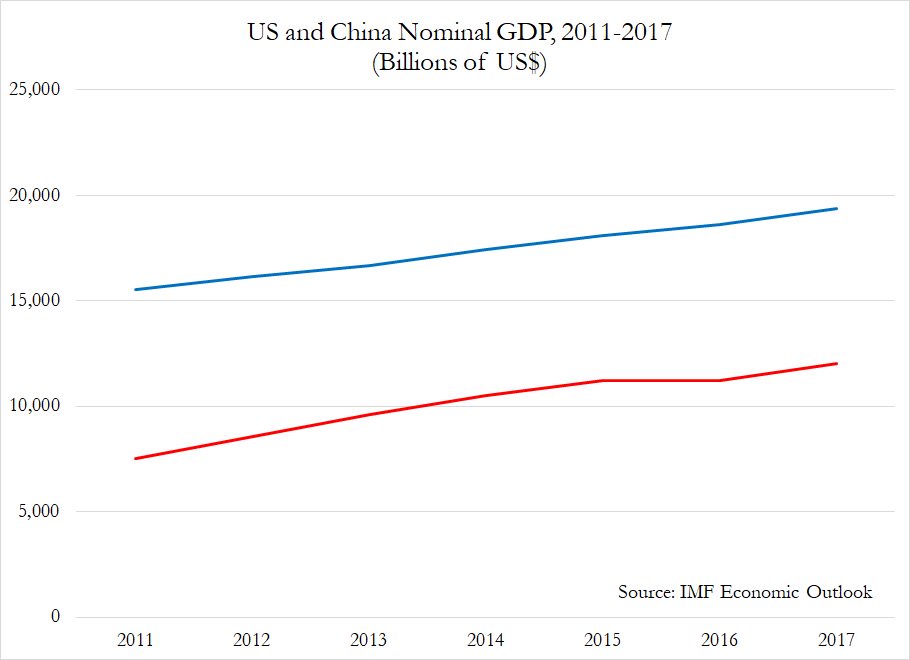

China and United States – Nominal GDP

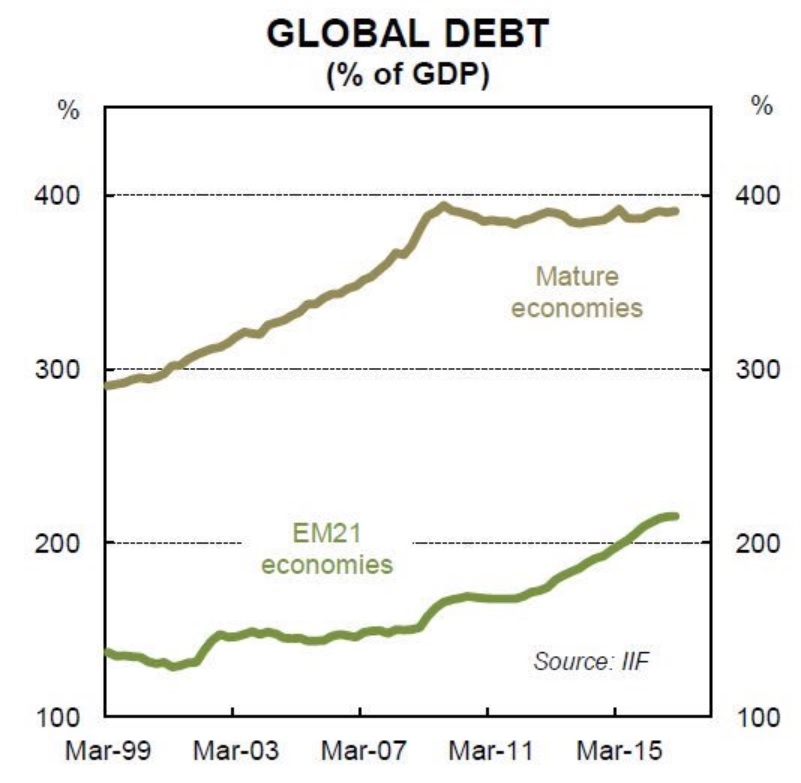

Global debt

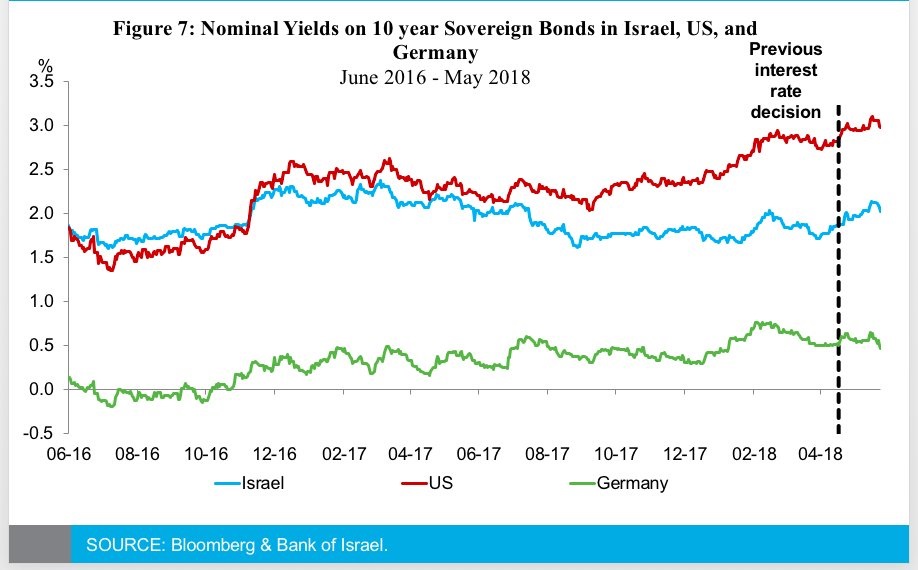

Nominal Yields – Israel, Germany & United States

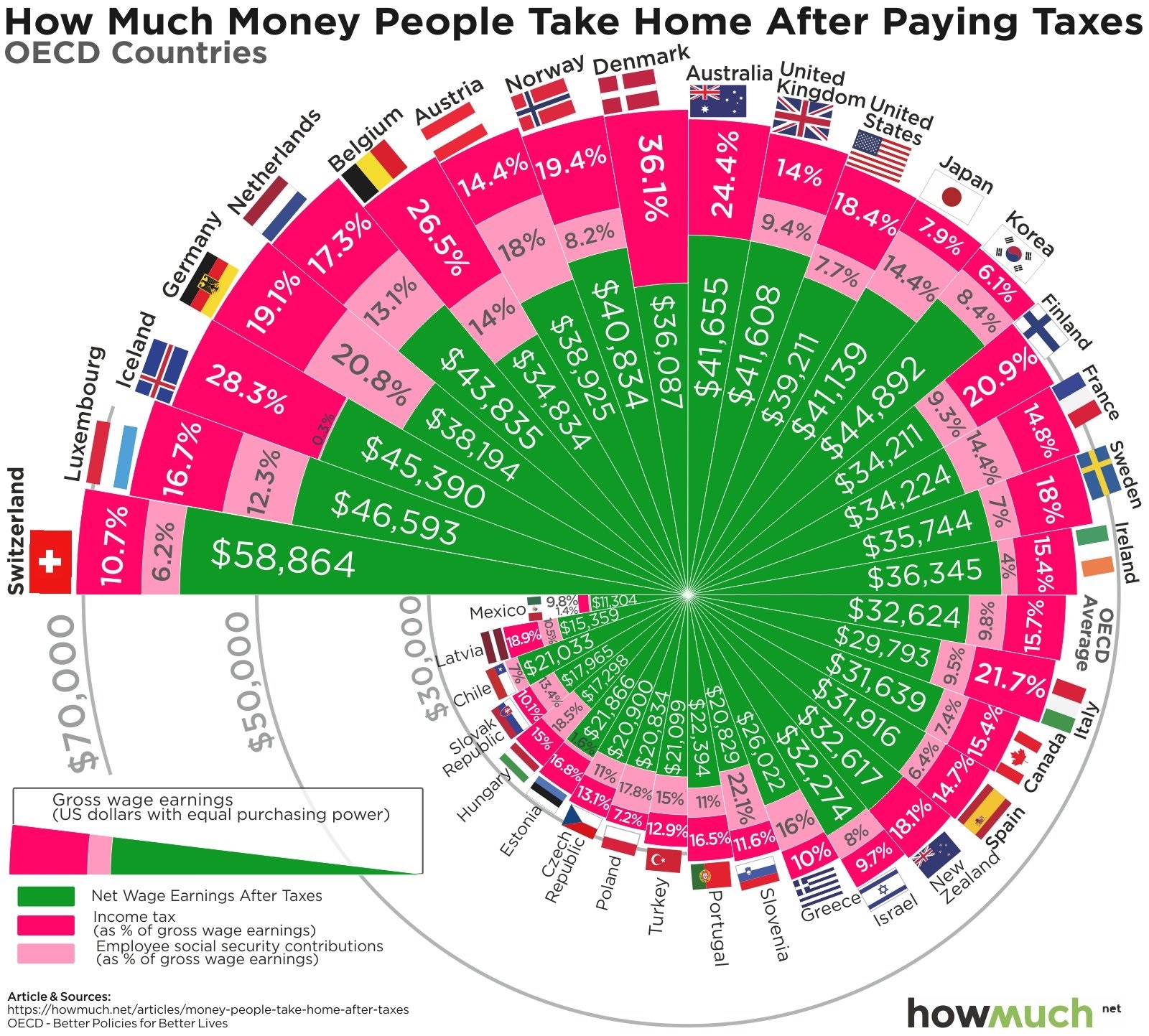

OECD Take Home Pay

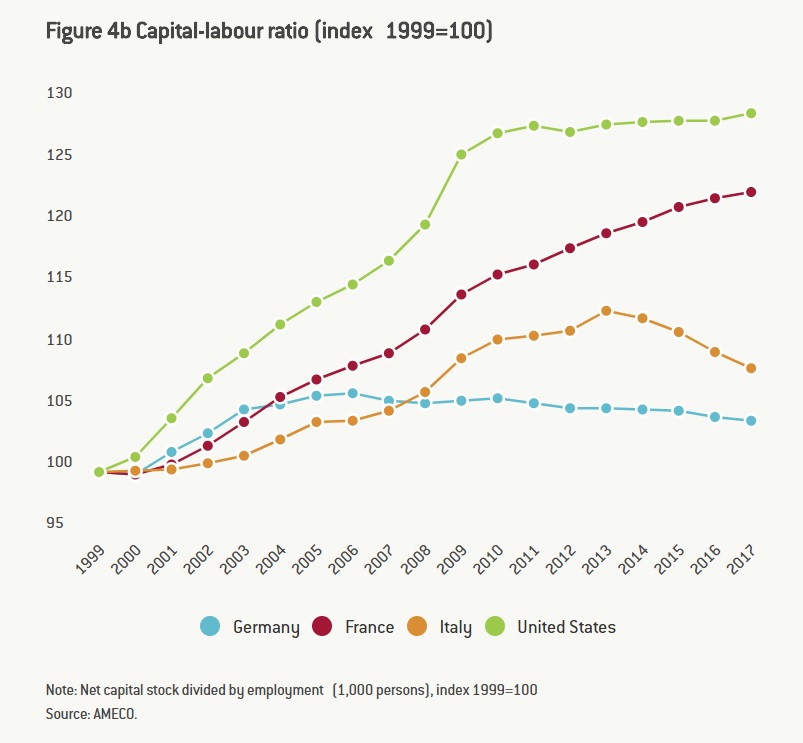

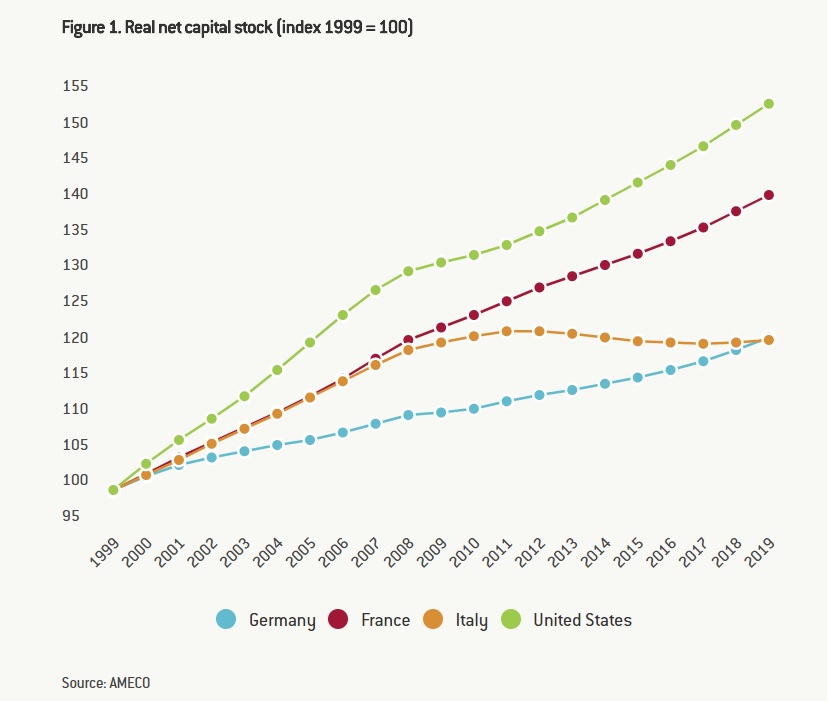

Net Capital Stock – Germany, France, Italy, United States

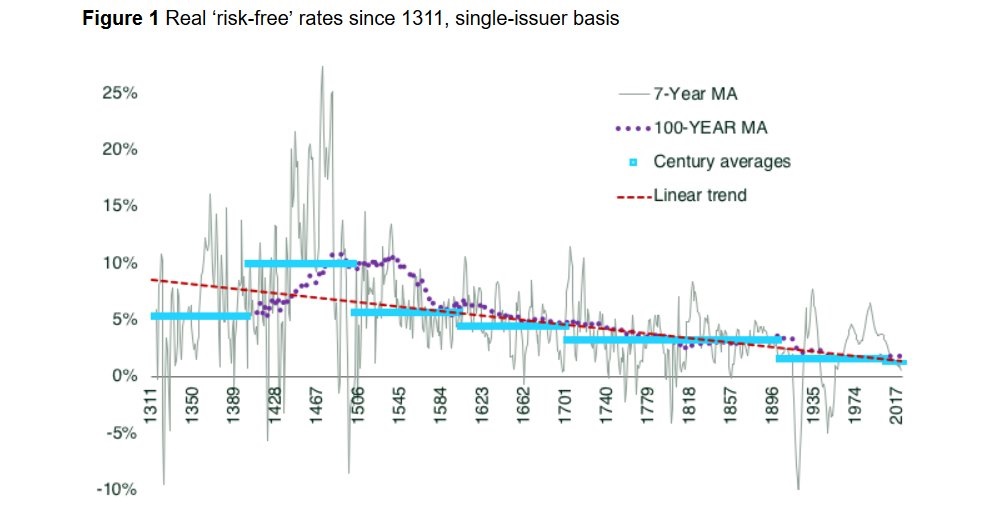

The Risk Free Rate through the ages

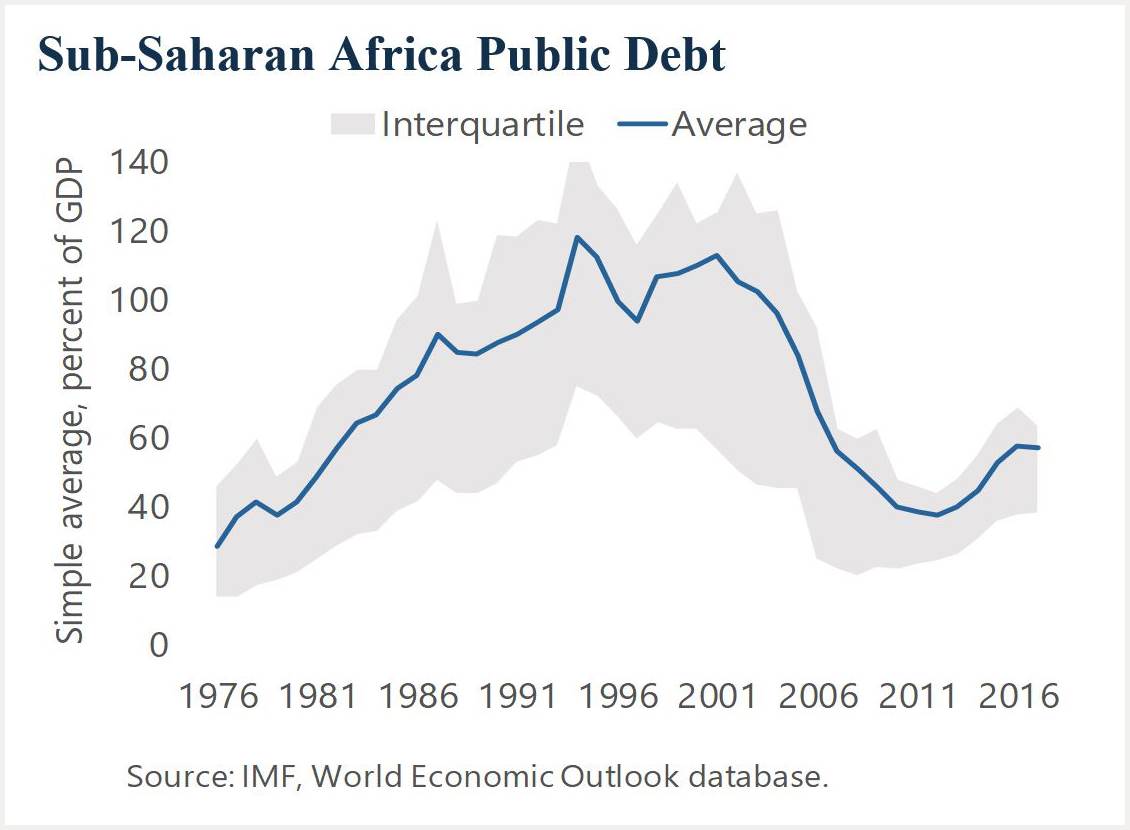

Sub-Saharan Africa Public Debt

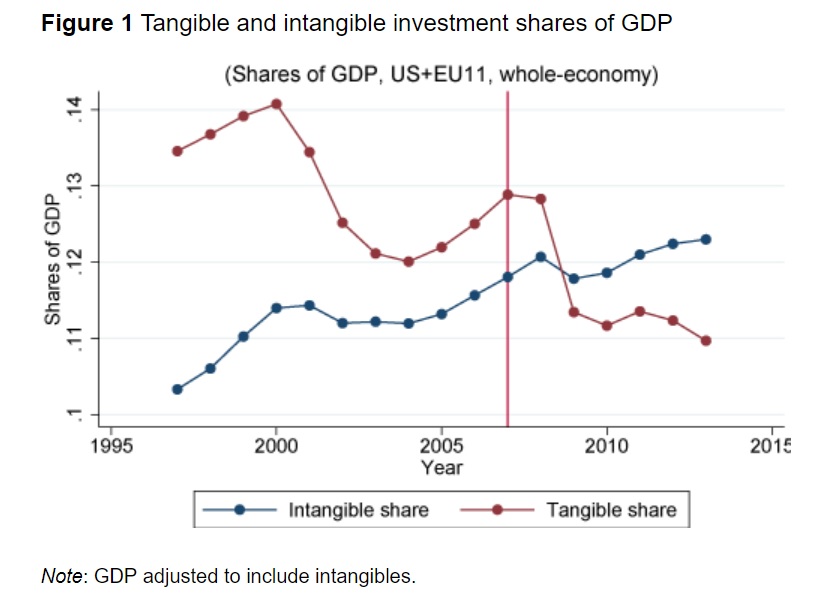

Tangible and Intangible shares of developed economies

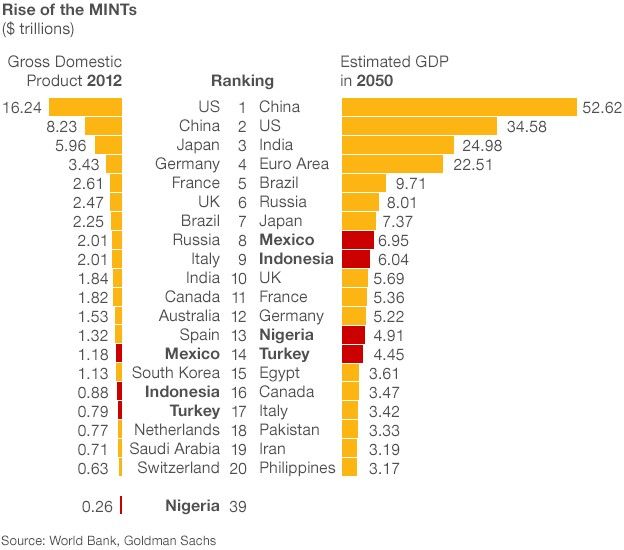

The rise of the MINTs (and the vanishing of Australia)

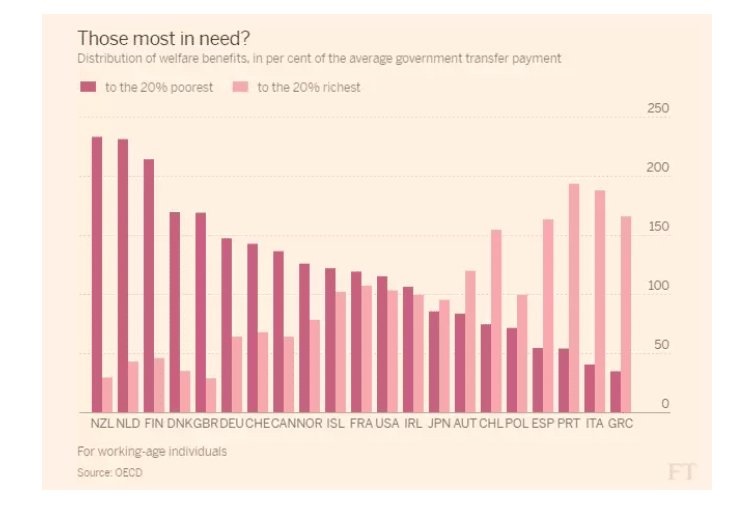

Transfer Payments – to whom?

…and Furthermore…

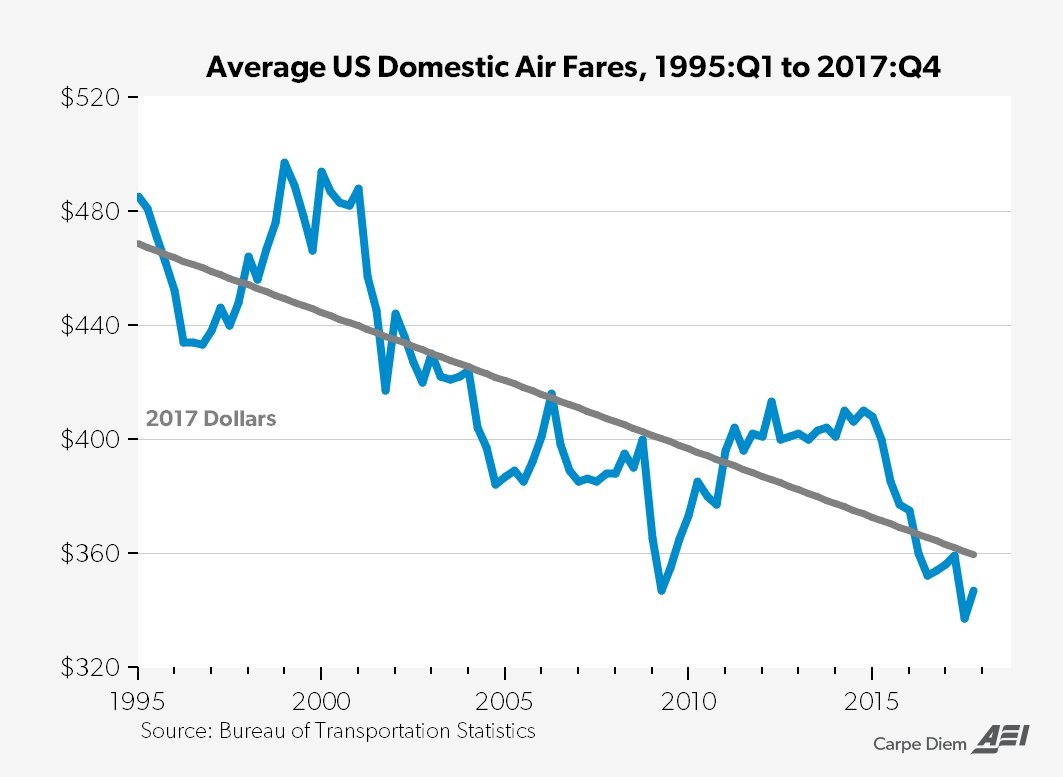

Airfares (or US airfares at least)

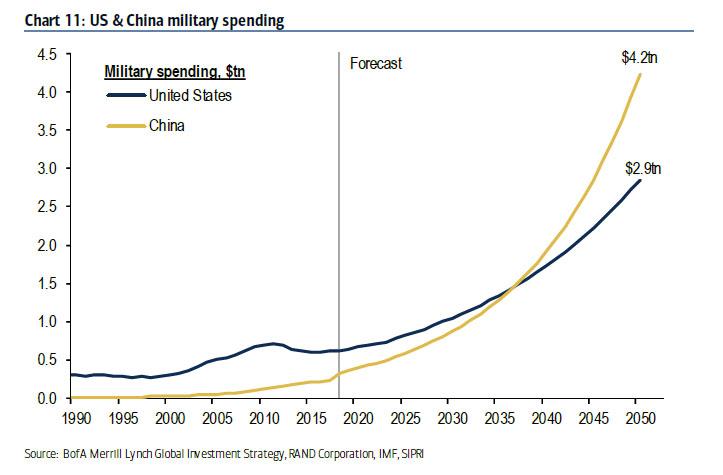

China & United States Military Spending (…and as that gap narrows?)

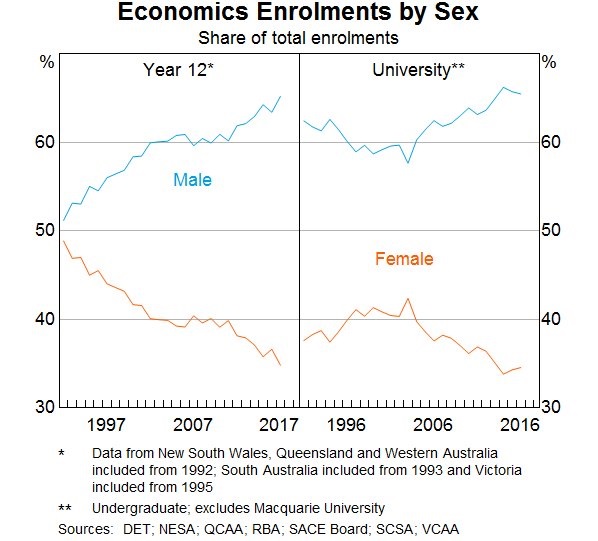

Economics and Australian Women

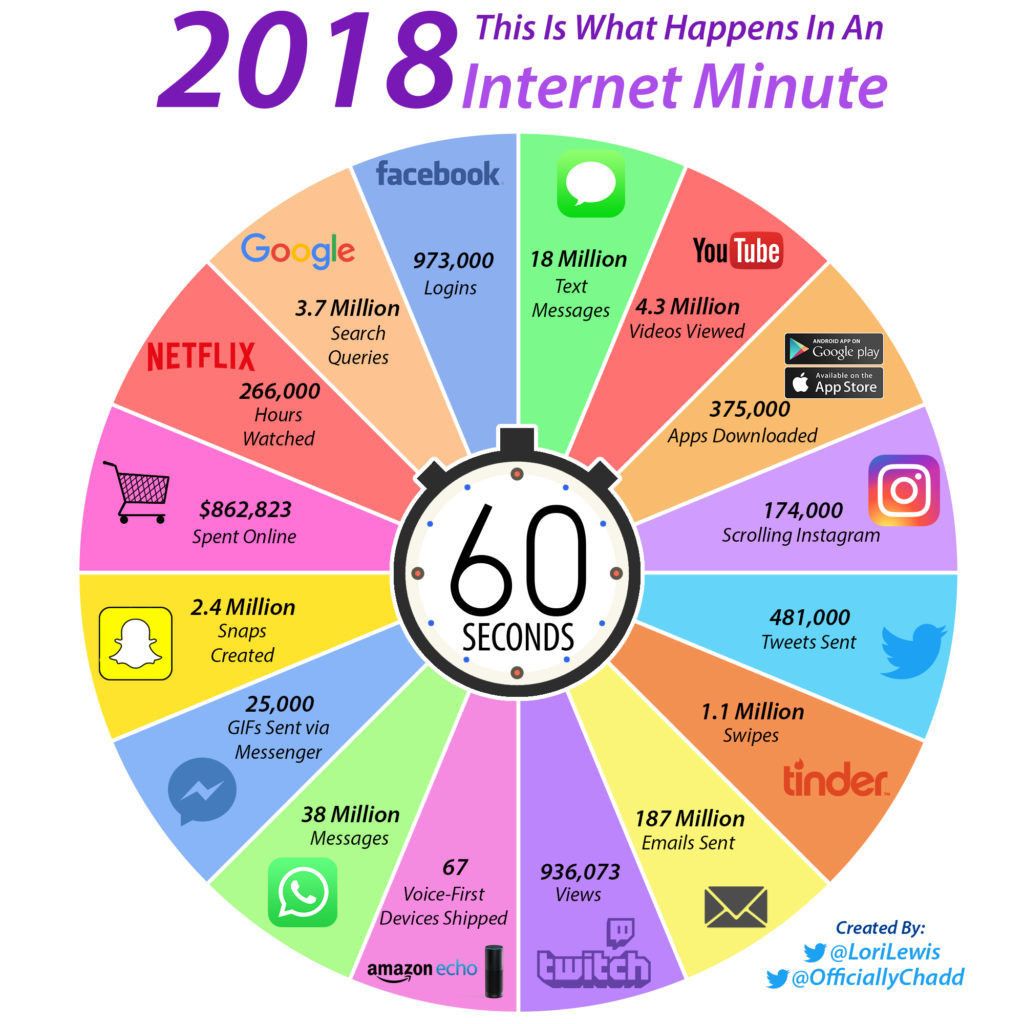

One Minute of Internet

The Potato Cake-Scallop Line

Top 10 Happiest nations

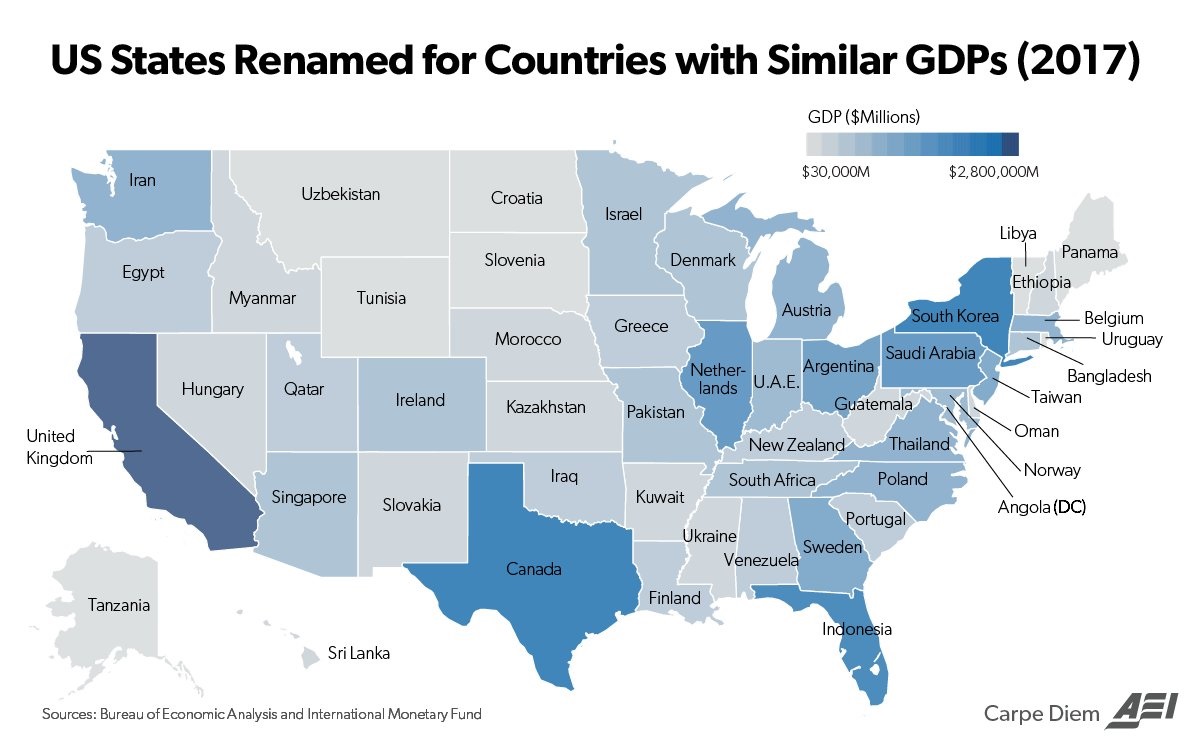

US States and global national comparisons