Why the Australian dollar might crash to 40 cents (or below!)

Regular readers will know that ever since the AUD was sitting at $1.11 against the USD, MB has held the view that there was a material risk that the currency would not only fall but keep falling to record lows. Yesterday’s Aviva Big Australian short explains how it might happen:

“We are short the Aussie dollar, we are long Australian interest rates and we are also long protection on the Australian banks,” James McAlevey, a senior portfolio manager at Aviva’s AIMS fixed income fund told The Australian Financial Review.

“The royal commission has shone a light on lending practices and could potentially tighten credit conditions when profitability is somewhat challenged and high US interest rates are having spillover impacts.”

…you can short the Aussie dollar in US dollars and be paid for doing so. It’s the first time in my career that that has happened.”

He says a “rebalancing” in China could also lead to reduced demand for iron ore which would further weigh on the currency.

The combination of a positive carry on a short Australian dollar position, the impact of a China slow-down would force the currency lower, but he said if there was an issue for the banks you would see “record lows”.

That’s been the MB risk thesis for Australia ever since the mining bust began. Sadly for our country, the RBA and Treasury decided that the best way to see-off the end of a mining boom – that they’d predicted would last thirty years and instead went bust in three – was to pump up the housing bubble.

Having happily appeared on Sunrise in 2010 to tell Australians to stop leveraging up on mortgage debt, Glenn Stevens pulled one of the most destructive public policy back-flips of our time and instructed everyone to do the opposite.

The result was what MB labelled the “Dumb Bubble“; a frenzy of interest-only mortgage borrowing that sent the eastern property bubble mad to float the economy over the mining investment cliff. It not only undid all of the back-filling of the property bubble by the fabulous serendipity of the mining boom, it made household and national leverage eminently worse than it had ever been given interest-only is pure sub-prime or ponzi-borrowing.

Meanwhile the Chinese post-boom adjustment has marched on. Yes, that nation stimulates every so often to keep its construction interests satisfied. But it’s resulting debt problem means that all it is really doing is taking an unavoidable slowdown in a series of cascades rather one giant adjustment. This truth is now acknowledged even by the buffoons at the RBA.

And so, here we are, entering another of those steps down in Chinese growth just as Glenn Steven’s Dumb Bubble goes bust.

Which brings us to today and the Aviva big short. The risk case for post-float lows in the AUD arrives if Dumb Bubble pops just as China slows again and the terms of trade crash resumes. I stress it is a tail risk but cannot be discounted given:

- China is slowing and unless there is another big wave of stimulus then bulk commodities are going to materially undershoot everybody’s rosy forecasts next year;

- the Australian housing market is under pressure on multiple fronts: the interest-only cliff, rising lending standards, rising funding costs, supply glut, negative gearing reform, exhausted monetary policy and constrained fiscal policy, and

- the US business cycle is already nine years old with clear imbalances in corporate credit and late cycle fiscal stimulus. It will go bust sooner rather than later as the Fed hikes.

If the three variables come together in the next few years then the Australian dollar could easily hit record post-float lows as the macro mistakes of a decade and more converge in one big adjustment that triggers serious capital flight.

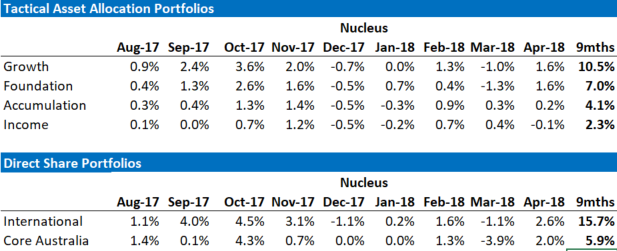

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.