And this time it is going to win, via the AFR comes the $640 billion British funds management giant Aviva Investors:

“We are short the Aussie dollar, we are long Australian interest rates and we are also long protection on the Australian banks,” James McAlevey, a senior portfolio manager at Aviva’s AIMS fixed income fund told The Australian Financial Review.

The London-based portfolio manager of the fixed income unit within Aviva’s $194 billion multi-strategy division said it has being eyeing the build-up in leverage in Australia for two years before placing the trades that will profit if Australia comes unstuck by a housing unwind.

Mr McAlevey said the fund has paid close attention to the Hayne commission and said it could provide the catalyst in the form of tougher lending standards.

Known as the “widowmaker” trade by some, Australian banks have been through two previous bouts of heavy shorting that they managed to see off without lasting damage. The first was in the lead up to the GFC and the second during the European debt crisis. On both occasions the “protection on the Australian banks” (CDS prices) soared while equity and the currency crumbled. Here’s CDS on CBA:

Interestingly, the third spike in 2015 happened when Jonathon Tepper and John Hempton conducted their now infamous sting on Western Sydney mortgages which is worth reprising given the royal commission:

The Reserve Bank of Australia and the Australian Prudential Regulatory Authority (APRA) all insist that there are almost no low-doc or no-doc loans. They also insist there are few high loan-to-value ratio loans. The truth is much worse.

Underwriting standards are poor in banks. The regulators trust the big four banks’ statistics, but we’ve seen that underwriting standards are much worse than advertised.

In our due diligence, we told mortgage brokers and bank managers that we required a 95% loan-to-value mortgage at 10x our gross household income to buy our dream house, and we were consistently told it was not a problem at all. All we needed were two payslips and mortgage insurance. We asked if the bank would call our employer, and both reputable and disreputable brokers said banks rarely verified payslips. Also, “most of the people checking documents are in Indian call centres.” Furthermore, we were told that as long as the payslips had the right Australian Business Number (ABN) and the business checked out, that was enough.

This is not how it has to be. In the UK, for instance, after the credit crunch, banks are far more thorough when verifying income. The bank cross-checks payslips with one’s bank account to see the net amount received corresponds to the gross amount paid. A lengthy affordability questionnaire must be filled out to make sure that pay is sufficient to cover mortgage payments, that are also stress-tested for higher rates. Bonuses, once nonchalantly taken as regular income, are much more strictly dealt with. No-deposit and minimal-deposit loans are much rarer and harder to obtain. Similarly, the US has tightened lending standards since the financial crisis.

But in Australia, more alarmingly, we were informed from various sources that disreputable brokers had software to make authentic looking tax returns for clients who needed mortgages. We were encouraged to lie about our incomes by multiple brokers in order to get dodgy loans past bank loan officers.

It should come as no surprise that lending standards have fallen as third-party origination of mortgages has risen. This was typical of standards in the US in 2005-07. Today, almost half of new housing loans are originated by third parties.

But our biggest surprise came when we visited a building society (a thrift). The bank manager told us her lending standards were conservative compared to the big banks. She would check our income more thoroughly. She then encouraged us to take a 95% loan to value ratio at 10x our gross income because, “It isn’t worth saving another 5% when house prices will rise more than 5%. By the time you save the 5%, prices will rise exponentially.” Those were her words, not ours.

Needless to say, John Hempton of Bronte Capital and your dumbfounded analyst from Variant Perception wandered around Sydney in shock and amusement after every meeting.

It’s now fact in a court of law which kind boosts Aviva’s positioning. Every Australian should be hedged against the Aviva outcome. It can be done by replicating its trades:

- getting capital offshore for AUD exposure;

- reducing exposure to property or taking out shorts on banks;

- or getting long Aussie bonds.

———————————————–

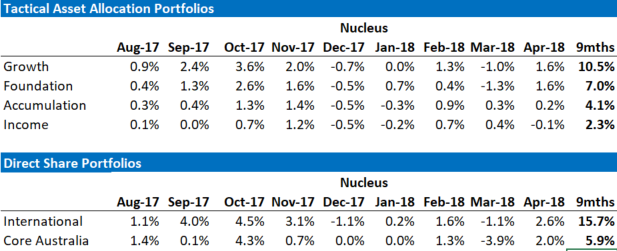

David Llewellyn-Smith is the chief strategist at the MB Fund so he is definitely taking his book!

The recent performance is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.