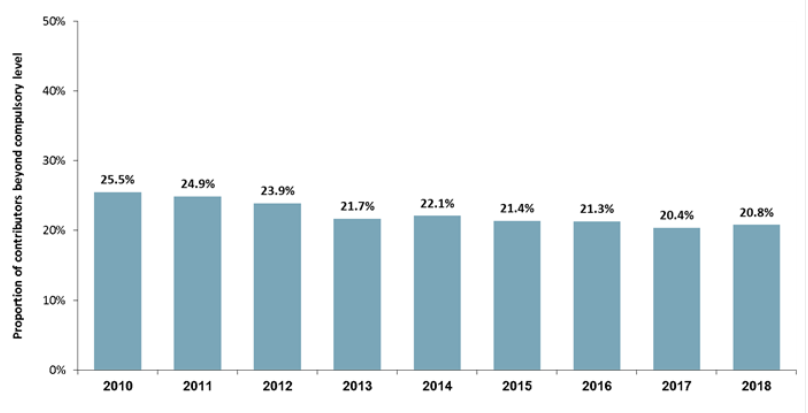

Roy Morgan Research (RMR) has released a new survey showing that 20.8% of Australians contributed extra towards superannuation in the 12 months to January 2018, way down on the 25.5% who did so in 2010:

The chart below shows the proportion of superannuation members contributing more than the compulsory level has declined substantially since 2010. In 2010, 25.5% of superannuation contributors were making payments beyond the compulsory level, this declined down to 21.7% in 2013. In 2014 the level was up marginally 22.1% but since that date it has struggled to stay above 20%…

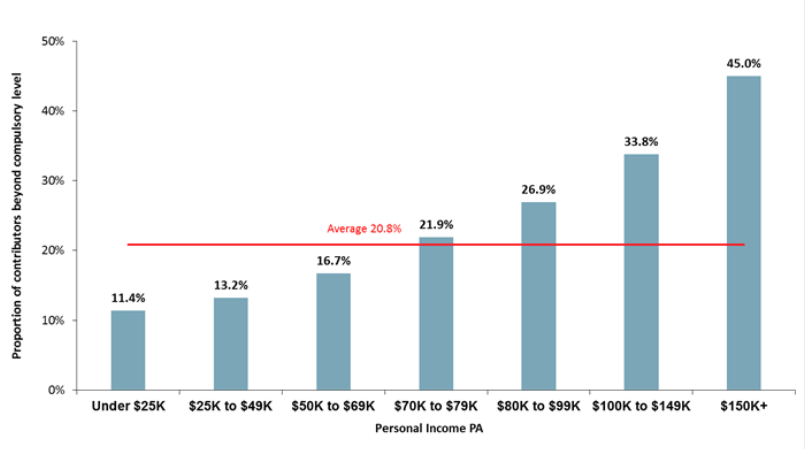

Moreover, the lion’s share of extra contributions are coming from higher income earners:

Superannuation members with personal incomes of over $70k per annum have an above average proportion of their contributors paying above the compulsory level. The highest are those earning more $150k per annum in which 45% are paying beyond the SG rate, followed by those on incomes of $100k to $149k per annum where the average is around a third (33.8%).

Those earning below $25k per annum are well behind the market average with 11.4%, followed by the $25k to $49k per annum group with 13.2%.

Advertisement

Whereas, baby boomers are also contributing the lion’s share of contributions:

As well as income, life stage is also a major factor impacting on superannuation contribution levels, particularly when it involves other priorities such as mortgage repayments, lifestyle choices and family expenses. This is shown by the fact that 40.8% of Baby Boomers who contribute to superannuation pay more than the compulsory level, compared to only 26.8% for Gen X, 12.2% for millennials and only 5.0% for Gen Z.

Norman Morris, Industry Communications Director at RMR, sees the declining voluntary contributions and the current compulsory superannuation rate (9.5%) as a problem:

Advertisement

“The Federal Government has announced that the SG rate will ultimately need to go to 12% to provide adequate superannuation in retirement but reaching this level has been delayed and is planned to start in July 2025.

“With the Government delaying the time for the SG rate to reach 12%, it will be even more important for individuals to voluntarily increase their level of contributions (within the current limits), otherwise they are more likely to fall behind in their retirement funding.

“We have seen that there are major competing priorities when it comes to people choosing to increase retirement funding options. Young age groups may be more focused on exciting lifestyle options. Young families often see the priority needs of their children to be more immediate and don’t have discretionary spending or saving capacity. In addition, the recent changes announced by both parties relating to superannuation have the potential to reduce the confidence in the long term nature of superannuation which has to potentially cover a period of fifty or sixty years.

“The Government’s changes have involved a number of major reforms, including a $1.6m balance cap in the retirement phase, and reduced contribution levels to $25,000. The Opposition has said that they will make major changes to dividend imputation which will place more pressure on superannuation, particularly SMSF’s.

Our recently released Superannuation and Wealth Management in Australia report details the opportunity for superannuation funds, to gain a greater share of more household investments currently held outside of superannuation. Australian households now hold only 27.4% of their net wealth in superannuation.

“This analysis is from the extensive Roy Morgan Single Source database which covers retirement funding, including superannuation, in much greater depth over nearly two decades.”

The cost of compulsory superannuation contributions falls on the employee, not on the employer, so any increase in the superannuation guarantee will lower one’s take home pay.

Forcing lower income earners to sacrifice more of their pay into superannuation would necessarily lower their living standards.

Tax concessions on superannuation already cost the Budget an inordinate sum, and are growing rapidly. So, raising the superannuation guarantee to 12% would mean they become an even bigger Budget drain over time.

Australia’s superannuation system is highly inefficient, as evidenced by the huge fees charged despite ever-growing balances.

Advertisement

Therefore, reforms to fix the underlying problems in the system (e.g. excessive fees, unequal distribution of concessions on contributions/earnings, etc) are critical before policy makers even consider extending compulsory superannuation or raising the rate.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.