Following former treasurer Peter Costello’s call last week for compulsory superannuation contributions to be taken out of the hands of bank-run retail super funds and union-backed industry super funds, who are gouging members with excessive fees, and instead be invested in a government-run fund, commentators at The Australian have unloaded on the giant superannuation rort.

Yesterday, Adam Creighton questioned why Australia has the world’s most expensive superannuation:

Here’s a fun fact: a family in Australia with a combined superannuation balance of $300,000 is paying more in fund management fees than it is on electricity — even after the latest 20 per cent price jump in power prices.

You might expect electricity to be expensive… But super? There’s no production of anything; other people and businesses are doing the hard work. Super is the allocation of savings; it’s the management of dots on a computer screen, of which advances in computing power should have slashed the cost.

We hear a lot about the importance of low-cost energy; we’d also be better off with low-cost finance…

No one asked for 9.5 per cent of their wages and salaries to be siphoned off into abstract, untouchable accounts where fees are taken out of future rather than the current, salient income…

As Costello urged, it would be nice if the government kindly “showed some interest” in ensuring people’s savings were managed “in a cost-efficient way”…

Downunder we have about 44,000 fund options, no default fund at all, coupled with utter confusion about fees. No wonder we have the most unnecessarily expensive super in the world…

The lowest hanging fruit in Australia’s reform agenda should be directing the superannuation contributions of those who don’t choose into one or a small handful of default funds with fees capped by legislation. The arrangement now is an unconscionable and highly inefficient subsidy to one part of the economy…

Today, Judith Sloan argues that the beneficiaries of Australia’s compulsory superannuation system are the industry, not the superannuants:

The superannuation funds, the trustees, the fund managers and the workers more generally who are employed in the industry think compulsory superannuation is the bee’s knees. But the reality is that superannuation is a dud product for pretty much every present and past superannuation member and, deep down, the government knows this…

The arguments that were used to justify the introduction of compulsory superannuation were twofold: Australia needed to raise its rate of savings, as well as overcome people’s short-sightedness in order to provide for a comfortable, dignified retirement. The alternative was to compel people to save to achieve this outcome.

The first rationale was quickly discredited and is no longer used as an economic argument. The second line of reasoning has a series of weaknesses, most of which were discussed last week by former treasurer Peter Costello…

The present final balances of superannuants are relatively meagre, on average $148,000 for men aged 60 to 64 and $124,000 for women…

Moreover, 80 per cent of those 65 or older rely on the pension, in full or in part.

And even in the context of a lift in the rate of the superannuation guarantee charge — from the existing 9.5 per cent to 12 per cent, heaven forbid — the rate of reliance on the pension doesn’t change overall, although more retirees will be on part pensions…

Let’s be clear, Costello is not proposing the nationalisation of superannuation. Rather, he is saying it would make sense for the default funds to flow to a national investment body — think Canada, Singapore — where the economies of scale and scope can ensure lower fees and charges as well as a global reach of investment. One of the biggest flaws of the investment side of our system is the overweight position of local equities, particularly the big banks.

Sadly, it seems unlikely that our system of compulsory superannuation will be dismantled anytime soon, even though it cheats so many people. In all likelihood it has induced higher levels of household debt as people anticipate being able to use their final superannuation balances to pay down outstanding debts, including mortgages.

The key now is to ensure that the super charge remains where it is (at 9.5 per cent); that we have a better way of directing default funds; and that the raft of other reform measures is acted on — sooner rather than later.

Both make valid points.

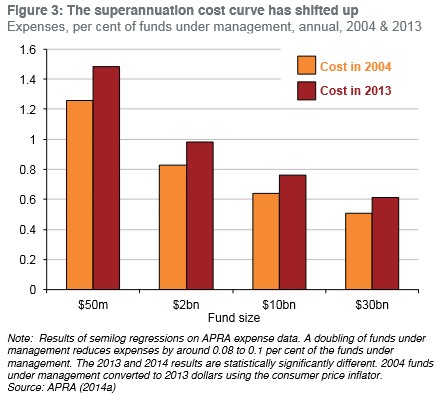

If superannuation was a well functioning and competitive market, average fees would have fallen as the value of funds under management has risen. This is because it should not cost ten times more to manage $1 billion of funds under management than it does to manage $100 million – the economies of scale argument cited above.

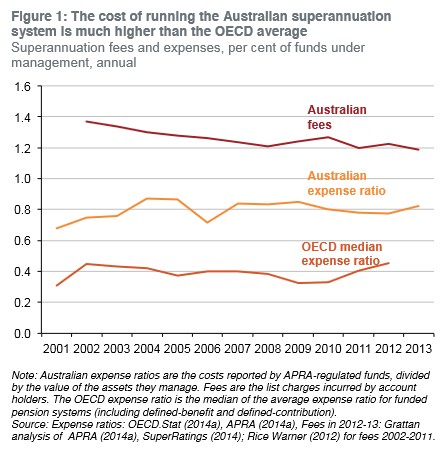

Instead, despite the huge explosion of superannuation balances since the superannuation guarantee (compulsory super) was introduced in 1993, average fees and expenses have barely changed and are way above the OECD average, according to the Grattan Institute (see below charts).

As noted by Grattan:

A larger system of larger funds should have incurred lower costs and charge lower fees, because big funds have lower costs…

Australian funds charge fees that are three times the median OECD rate, on average… Many countries have superannuation pools much smaller than Australia’s, yet their funds charge customers much less.

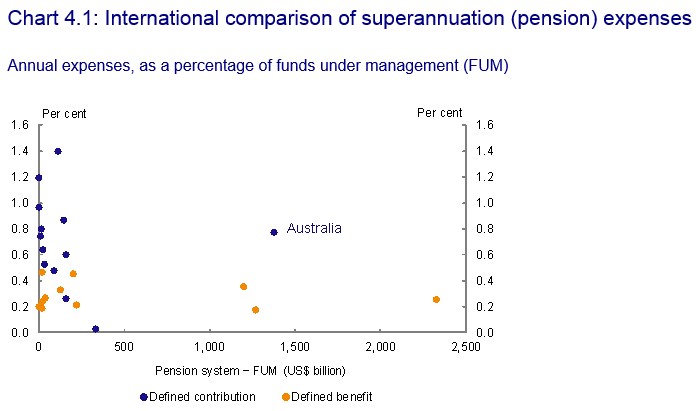

The Draft Report of the Murray Financial System Inquiry noted similar concerns, as illustrated in the below charts:

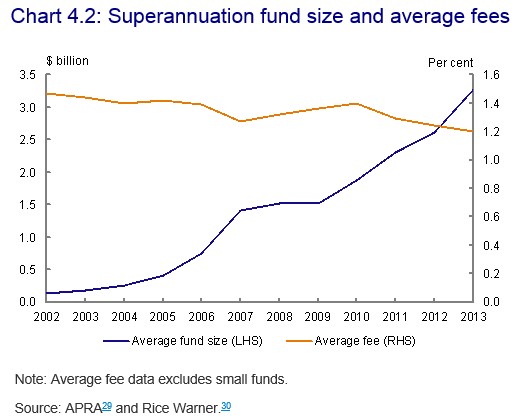

And that super fees had not fallen in line with what could have been expected given the substantial increase in scale:

Clearly, then, Australia’s superannuation funds are not just inefficient, but are also gouging members. And this has been facilitated by Australia’s compulsory contributions (currently set at 9.5% of employee wages), which has provided the industry with a “sheltered workshop” by which to operate.

Indeed, there are arguably few better businesses to be in than Australian superannuation. What other industry is guaranteed through policy an ever-growing pool of funds under management to ‘clip the ticket’ and earn fatter profits without even trying?

The above, yet again, highlights why reforms to fix the underlying problems in the system (e.g. excessive fees, unequal distribution of concessions on contributions/earnings, etc) are critical before policy makers even consider extending compulsory superannuation or raising the rate.