From April 17, Westpac and its subsidiaries, BankSA, St George Bank and Bank of Melbourne, are increasing the number of expense categories from six to 13 to enable “more detailed conversations to better understand their financial situation”.

Customers will also have to produce more documentation with their local applications to support their stated outgoings and debts.

In addition, a ‘financial acknowledgment’ form the customer will be asked to sign that details their income, expenses and liabilities.

Mortgage brokers, who act as intermediaries between borrowers and the banks, are being asked to make detailed enquiries from their clients and capture the response.

They are also asked to provide “acceptable verification documents” for applicable outgoings and debts.

This is the thin end of the wedge if there was ever one. As UBS wrote this week about the consequences of the Royal Commission:

What could be the implications?

Mortgage (and other consumer credit product) underwriting standards in Australia seem to have been lax for some period of time. APRA is moving to tighten underwriting standards. However, given the evidence presented so far to the Royal Commission we believe there is a material way to go to ensure the banks fully comply with the National Credit Act regarding Responsible Lending. This is exacerbated by the rollout of Comprehensive Credit Reporting (CCR) which ensures all customer liabilities are disclosed to potential lenders (from 1 July 2018).

While a tightening of mortgage underwriting standards is prudent, especially as the banks move to fully complying with Responsible Lending, it has a material impact on the economy. It must be remembered that house prices are determined by the demand and supply of credit (not the demand for and supply of housing).

As a result we believe there are two potential scenarios

(1) As the banks tighten underwriting standards assessed household income is reduced. The banks will need to undertake more detailed analysis of customers’ individual living costs and the Household Expenditure Measure (HEM) benchmark is increased slowly over time. As the banks gradually move towards fully complying with the Responsible Lending laws the flow of credit is steadily constrained and the housing market slowly deflates;

(2) The Royal Commission sets a strict definition of the “reasonable inquiries” and lenders are required to immediately comply with Responsible Lending obligations (eliminating ‘predatory lending’). Income assessment is tightened, the banks are required to undertake a full review of each borrower’s living costs The back-up HEM benchmark is increased to realistic levels which borrowers could be expected to live off during the full life of the loan (including ‘lumpy’ items). This leads to a sharp reduction in the Net Income Surplus and false applications are largely eliminated. However, in this scenario fully complying with Responsible Lending laws would result in a sharp reduction in credit availability ie a ‘Credit Crunch’ especially for lower income households. RBA rate cuts would not help credit availability as borrowers are assessed using the 7.25% interest rate floor. This could potentially result in a significant economic downturn.

Advertisement

I still think we’ll see the easier scenario from our captured regulators. The open question is will they lose control of the process as markets take over? As Credit Suisse has been arguing:

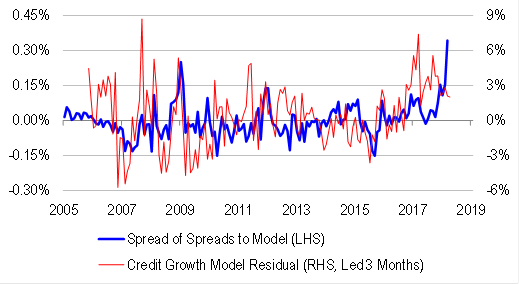

AUD interbank credit spreads have widened very aggressively, and this widening cannot be explained by conventional macro factors. But we have looked at something unconventional – the excess of credit growth relative to banks’ reported lending standards. We find that when credit growth is excessive, interbank spreads tend to rise, presumably because excessive credit growth brings about default risks. And over the past few years, credit growth has been well ahead of our proprietary credit conditions index. Widening USD LIBOR-OIS spreads may not be systemic – but it is an open question as to whether widening AUD spreads might be.

Regardless of why credit spreads are widening, they are likely to have a negative impact on Australian growth via the cost, and availability of credit.

…This sort of macro environment carries with it de-leveraging risks. And de-leveraging risk undermines the efficacy of naïve value factors. Earnings, dividends and book values stop anchoring asset prices during de-leveraging episodes. Rather, asset prices drive fundamentals. Perversely, higher multiple stocks may actually do well to the extent that they carry strong quality, or defensive characteristics.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.