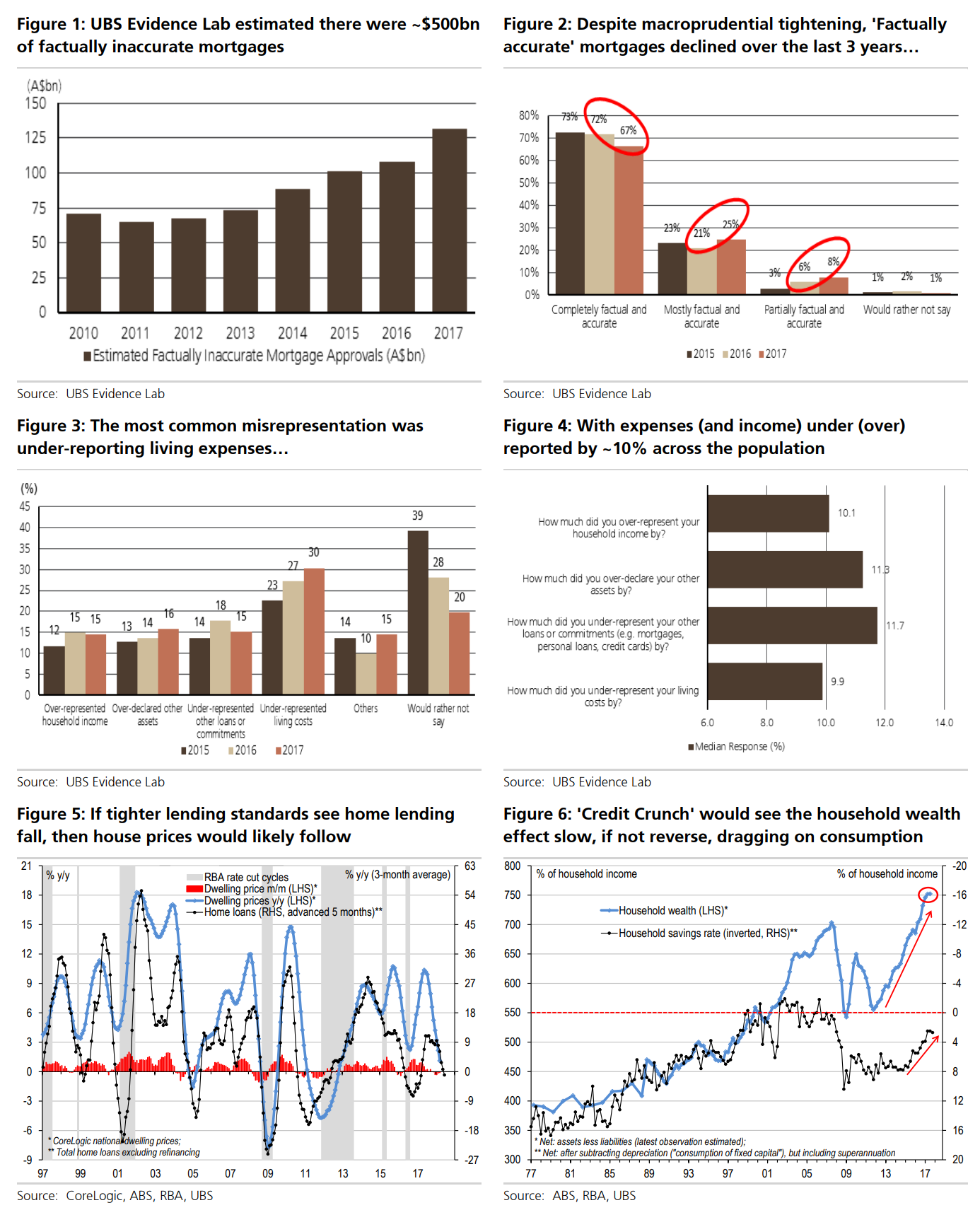

Mortgage (and other consumer credit product) underwriting standards in Australia seem to have been lax for some period of time. APRA is moving to tighten underwriting standards. However, given the evidence presented so far to the Royal Commission we believe there is a material way to go to ensure the banks fully comply with the National Credit Act regarding Responsible Lending. This is exacerbated by the rollout of Comprehensive Credit Reporting (CCR) which ensures all customer liabilities are disclosed to potential lenders (from 1 July 2018).

While a tightening of mortgage underwriting standards is prudent, especially as the banks move to fully complying with Responsible Lending, it has a material impact on the economy. It must be remembered that house prices are determined by the demand and supply of credit (not the demand for and supply of housing).

As a result we believe there are two potential scenarios

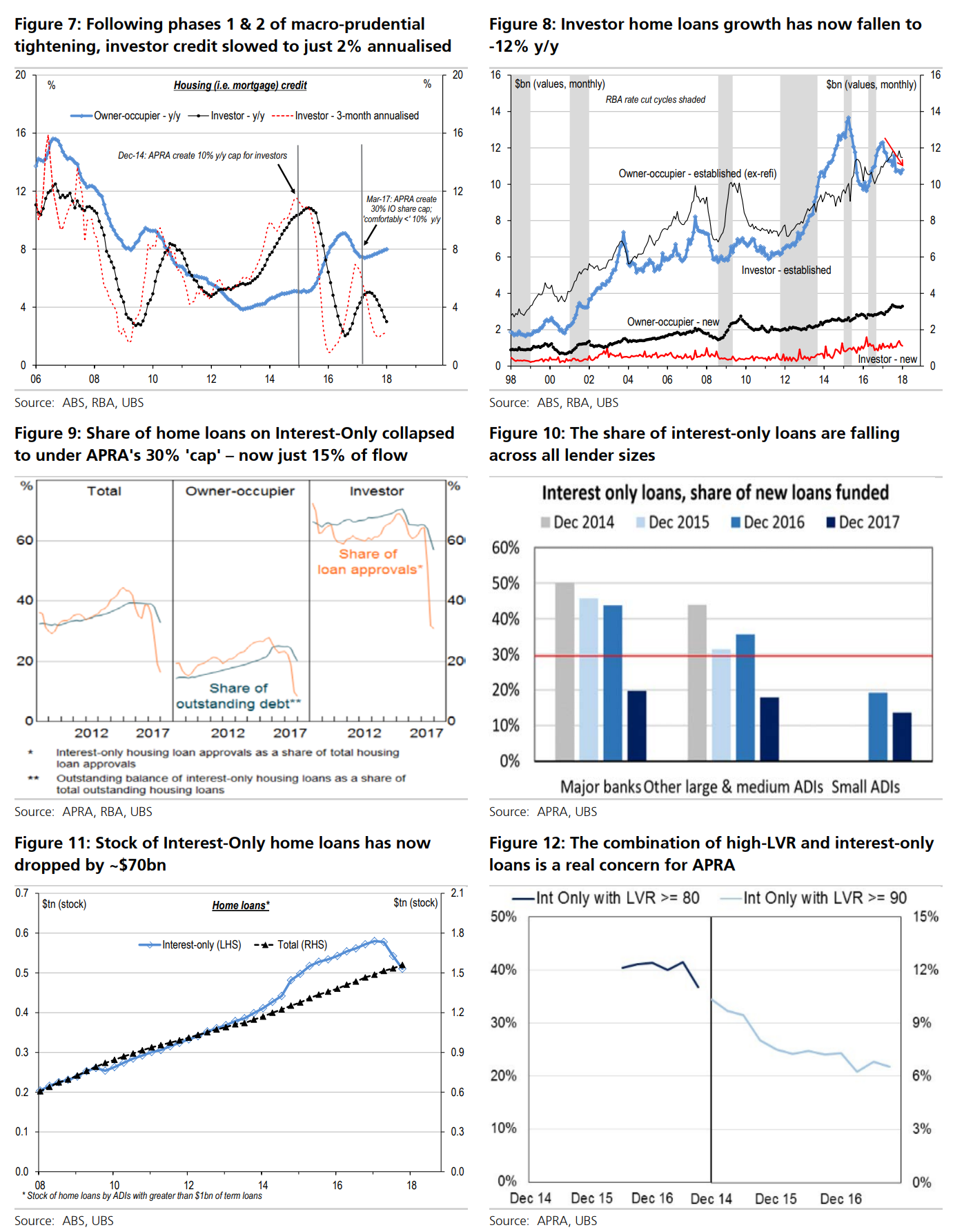

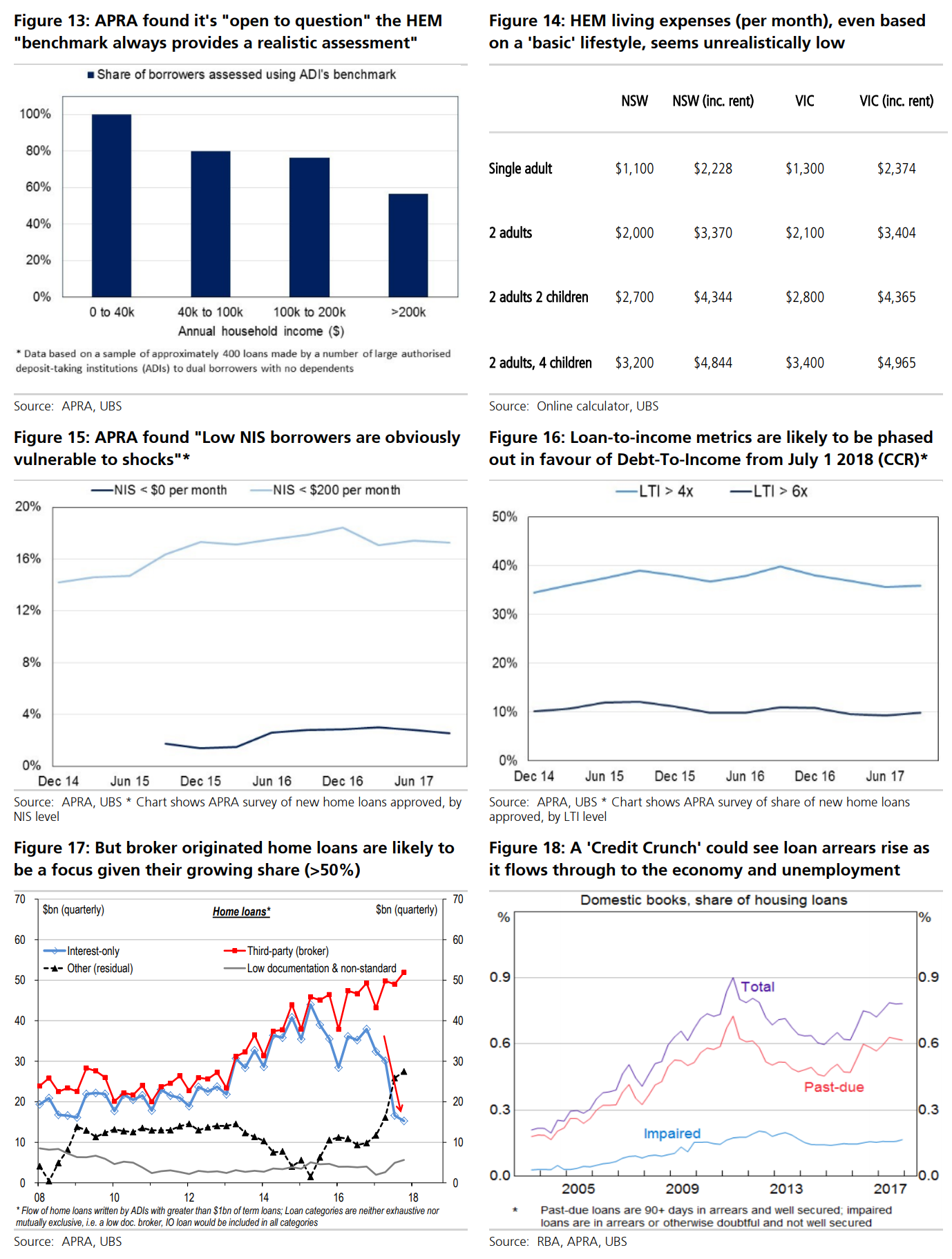

(1) As the banks tighten underwriting standards assessed household income is reduced. The banks will need to undertake more detailed analysis of customers’ individual living costs and the Household Expenditure Measure (HEM) benchmark is increased slowly over time. As the banks gradually move towards fully complying with the Responsible Lending laws the flow of credit is steadily constrained and the housing market slowly deflates;

(2) The Royal Commission sets a strict definition of the “reasonable inquiries” and lenders are required to immediately comply with Responsible Lending obligations (eliminating ‘predatory lending’). Income assessment is tightened, the banks are required to undertake a full review of each borrower’s living costs The back-up HEM benchmark is increased to realistic levels which borrowers could be expected to live off during the full life of the loan (including ‘lumpy’ items). This leads to a sharp reduction in the Net Income Surplus and false applications are largely eliminated. However, in this scenario fully complying with Responsible Lending laws would result in a sharp reduction in credit availability ie a ‘Credit Crunch’ especially for lower income households. RBA rate cuts would not help credit availability as borrowers are assessed using the 7.25% interest rate floor. This could potentially result in a significant economic downturn.

Economic implications of a possible ‘Credit Crunch’

Base case outlook

Our base-case economic outlook assumes only a slow and modest tightening of credit conditions – due to phase 1 and 2 of macroprudential tightening from caps on investor credit growth & interest only loans. We have been looking for credit growth to ease, and house price growth to moderate to 0% to -3% y/y in 2018 & 2019. This is consistent with a fading – but not reversal – of the ‘household wealth effect’. This follows the household savings rate collapsing by >5%pts in the last 3 years to a post-GFC low of ~2½%, and hence has provided a material boost to nominal consumption growth of over 1%pt per year over that period.

For our outlook, this expected fading wealth effect is balanced against the upside from household tax cuts and booming global growth – leading to a modest recovery of real GDP growth to a ‘trend-like’ pace of 2.8% y/y in both 2018 and 2019. Our RBA view has long been on the dovish side, with the cash rate on hold for all of 2018, and no rate hike until 2019.

Scenario 1: Credit tightening

However, we are now more concerned about the possibility of a ‘tighter credit’ scenario. Specifically, phase 3 of macro-prudential tightening – given the focus of regulators and the Royal Commission on lending standards – could lead to a longer period of sub-trend GDP growth. A reduction in credit availability and a persistent fall in the flow of home loans would likely cause a larger decline in house prices (Figure 1). This would likely halt the fall in the household savings rate, causing weaker than expected consumption and housing activity (and hence GDP).

If this negative scenario plays out, the RBA would likely avoid hiking rates for even longer into 2019; and regulators would probably end Phase 1 & 2 of macroprudential tightening (i.e. caps on investor credit growth & interest-only), albeit probably to little positive effect, given the greater drag from tighter lending standards.

Scenario 2: Credit Crunch

We also cannot rule out a ‘Credit Crunch’ scenario – even though it would clearly be unintended by regulators and policy makers (and banks for that matter). If credit tightening lasts for longer than we anticipate, and evolves into a ‘Credit Crunch’, there is potential for an economic downturn. Under a Credit Crunch scenario, house prices would likely fall over a prolonged period across a few years. This is because the price of money (i.e. ~record low interest rates) becomes less relevant compared with the supply of money (i.e. credit availability) or demand for money (i.e. employment, income, population) – particularly for the marginal new borrower (especially on lower incomes) which sets the price of the stock of existing housing.

There is a great deal of uncertainty over how ‘bad’ this could become, simply because Australia has never had a fall in house prices of 10%+ (even during the GFC prices ‘only’ fell to -8% y/y, but the RBA slashed rates by 425bp and reflated the housing market), and neither have we had a domestic recession in almost 3 decades. If a Credit Crunch feeds through to the broader economy and results in rising unemployment, this could see the RBA even consider cutting rates if they became concerned the slow-down was turning into a recession. In this scenario there is a risk of a pick-up in arrears as existing borrowers become financially stressed, and could precipitate a broad-based credit event.

Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry

Round one of public hearings in the Royal Commission began on Tuesday 13th March with an initial focus on consumer lending. So far the Royal Commission has been presented with substantial evidence based on a number of case studies into banking misconduct. The following are a series of quotes from the Royal Commission transcript which illustrate the extent of these issues:

Fraud and Bribery

Counsel Assisting, Ms Rowena Orr, QC: “I want to put to you is that NAB knows, & you know, that there were unsuitable loans, there was false documentation, there was dishonest application of customers’ signatures on consent forms & there was the misstatement of some loans in loan documentation.

The whistleblower is recorded as saying: ‘One customer recently said at a particular branch, they told him he could borrow $800,000, but the valuation was only $450,000. The whistleblower said the money exchanges hands in cash, in envelopes, white envelopes usually over the counter. Money is deposited at CBA, so NAB can’t detect the deposits’. Now, this is the information provided by the second whistleblower. Is that right?”

Mr Waldron, NAB – “That’s correct”

Counsel Assisting, Ms Rowena Orr, QC – “And the whistleblower tells NAB that these people are making up fake payslips, fake ID, fake Medicare cards … They charge $2,800 bribery for each customer for home loans”.

Failure to verify customer income

Counsel Assisting, Ms Rowena Orr, QC – “And it wasn’t just the fact for Mr Meehan, that had submitted more than 50% to a single lender; it was also the fact that the particular lender that he had submitted them to was Westpac because Aussie [Home Loans] had formed the view that the credit assessment processes at Westpac were more lax than at other lenders; is that right? Aussie had formed the view that the fact that they [Westpac] were just requiring a letter of employment, as opposed to payslips, would be something that brokers would become aware of to be easier to provide the documentation that was necessary. And do you mean, by that, a letter of employment is an easier document to falsify?”

Lynda Harris, Aussie Home Loans – “Yes”.

Failure to assess customer expenses

Counsel Assisting, Ms Rowena Orr, QC – “The first issue I think that’s worth mentioning this across home loans…it’s a lack of questions & verifications about expenditure. When we ask for copies of their assessment, is that it looks much more likely that a benchmark has been used than they looked at the consumer’s actually expenditure, which can vary considerably from a benchmark figure. There is also very little evidence that expenditure has actually been verified in any way.”

Mr Ranken, ANZ – “ANZ recognised there were instances where it lacked evidence to show that genuine inquiries had been made”

Failure of internal controls

Counsel Assisting, Mr Dinelli – “The remediation paid demonstrates that processing errors occur across a variety of credit products. They occur predominantly by reason of the application of automated processes, but human errors left unchecked often underlie them.”

Mr Van Horen, CBA – “It was the error we made in our serviceability calculation and the mapping the data flows … without overstating it, doomed to fail … having robust change processes, I think, was our failing and it’s clearly an area of ongoing work.”

Failure to report misconduct to ASIC

Counsel Assisting, Ms Rowena Orr, QC – “NAB knew enough to sack five employees for dishonesty and for conflict of interest, is that right? It knew enough by November to sack people for those reasons. Are you telling me it didn’t know enough to tell ASIC that there was a problem?”

So there you have it, the heart of the great Australian bubble, arteries choked solid with control fraud. This is absolutely no different to US sub-prime, Spanish lunacy, Irish madness or Icelandic suidice.

No doubt Australia’s captured regulators, which are still denying knowledge of the above total collapse of banking practice, won’t allow a credit-crunching reset of lending rules. Equally, the RC cannot be ignored and the reset must come, just over more time.

But remember, it won’t be left up to them. None of the above touches on how markets will react. As explained Friday, there is good evidence that the exposure of the control fraud is already impacting funding costs and that it will get considerably worse as the business cycle pushes towards its end, from CBA:

Advertisement

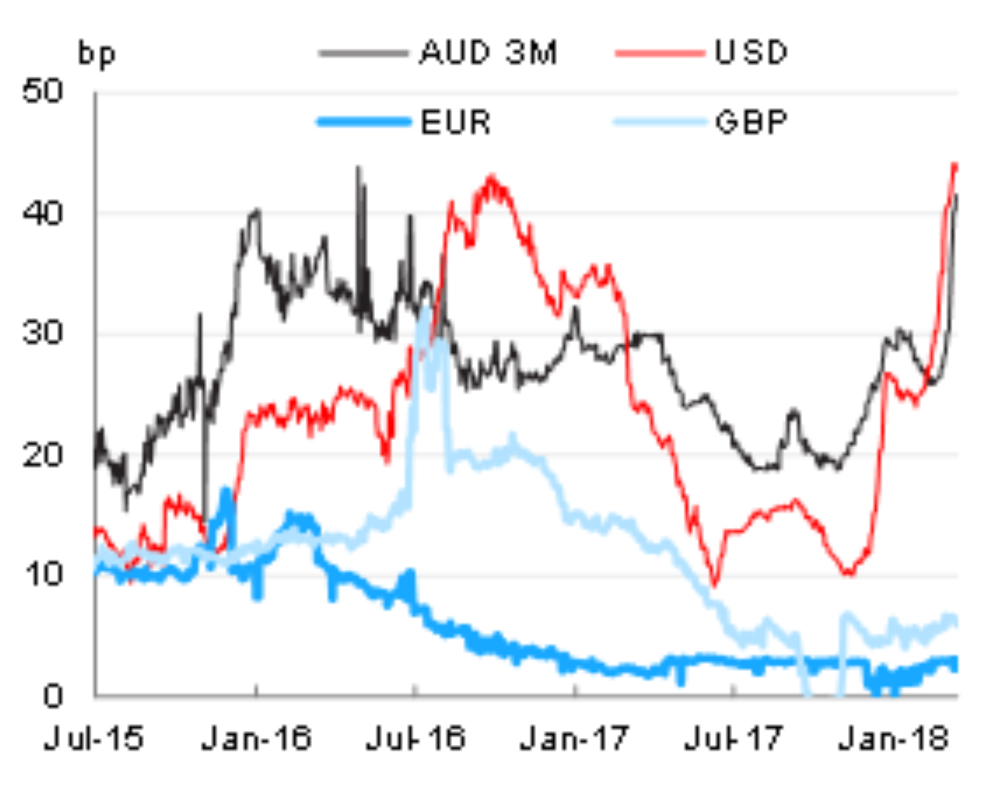

Australian repo and BBSW spreads have widened sharply in recent weeks.

Australia is a net borrower from the US and most of the move has been driven by that market.

The widening of US front‑end spreads appears to have been driven by a perfect storm: US Treasury Bills growing substantially; US Corporate cash behaving differently thanks to repatriation and the debt ceiling all coincided.

Some – not all – of these drivers will lessen in coming weeks, which should see spreads contract a little.

The US Treasury will likely to be able slow issuance once the Debt Ceiling and seasonal effects flow through the system. The increased deficits are here to stay, so some part of the increased issuance will likely persist, as will less accommodative monetary conditions.

Figure 9 shows that the pattern of the dual movement (once in December and once in February/March) in the USD LIBOR spreads is also shown in all three BBSW to OIS spreads. However, we also perhaps need to explain why the Australian market is being affected more than other international markets. The EUR and GBP markets are sitting slightly wider (Figure 1) while the NZ market has not yet been affected at all.

The key to the stronger reaction in Australian spreads versus everyone else is the extraordinary revelations in the RC driving risk through the roof. If the bubble is based upon predatory lending then the banks are liable and borrowers will be able to walk away from mortgages as prices fall. Even lenders mortgage insurance may be moot. This is the “jingle mail” moment.

The end of the Australian housing bubble is visible in plain black and white and the denouement is increasingly likely to be reach historically ugly proportions.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.