The USD index tumbled to three year lows last night:

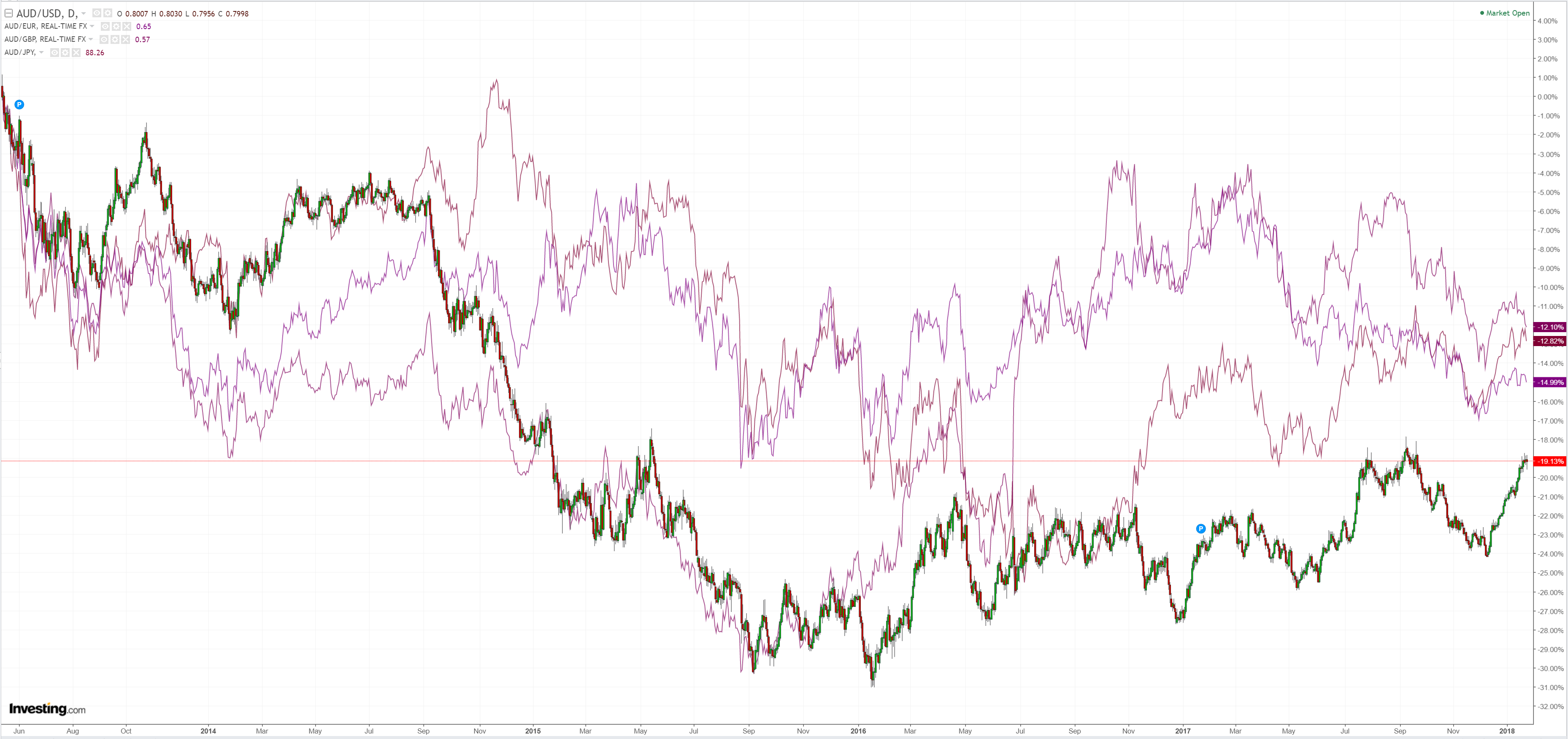

But the Australian dollar was sold anyway. Indeed it was dumped against all DMs:

Advertisement

The reason was iron ore which took a tumble. Confirmed by weakness as well in the Brazilian real:

Gold firmed:

Advertisement

WTI hit news highs:

But base metals fell and copper slumped as its inventories resemble the iron ore Everest:

Advertisement

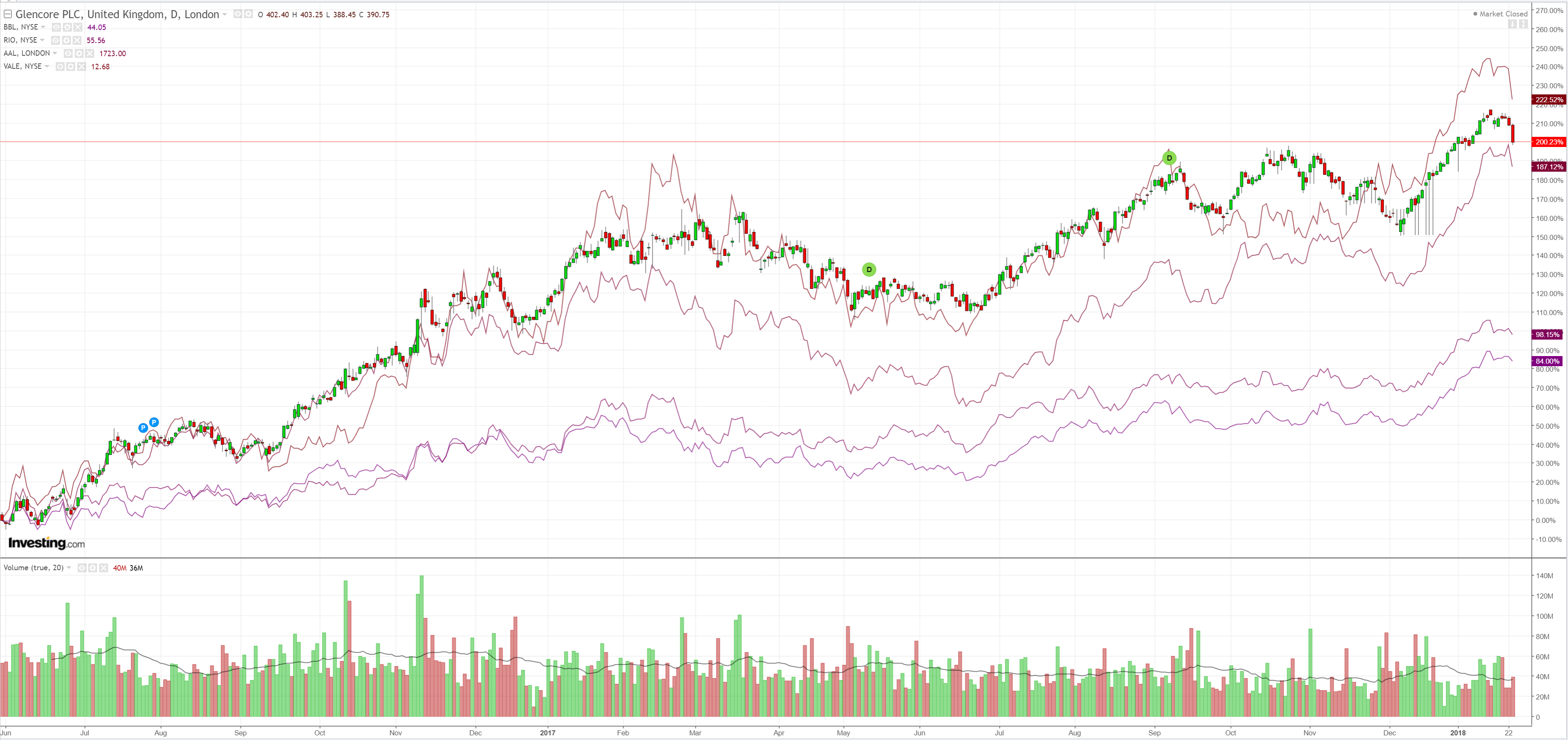

Big miners were thrashed:

EMs stocks are aimng straight at the 2008 high:

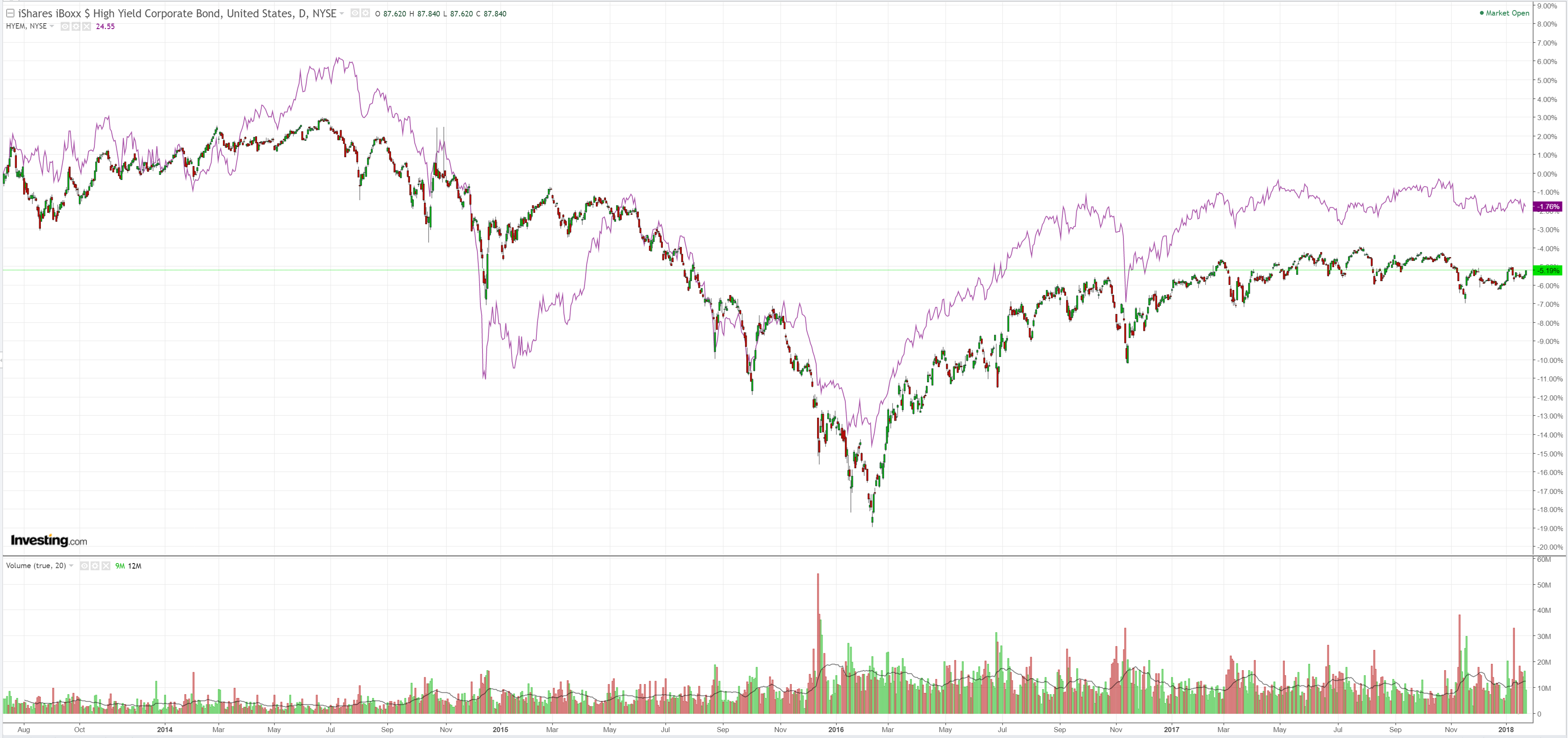

Junk is not:

Advertisement

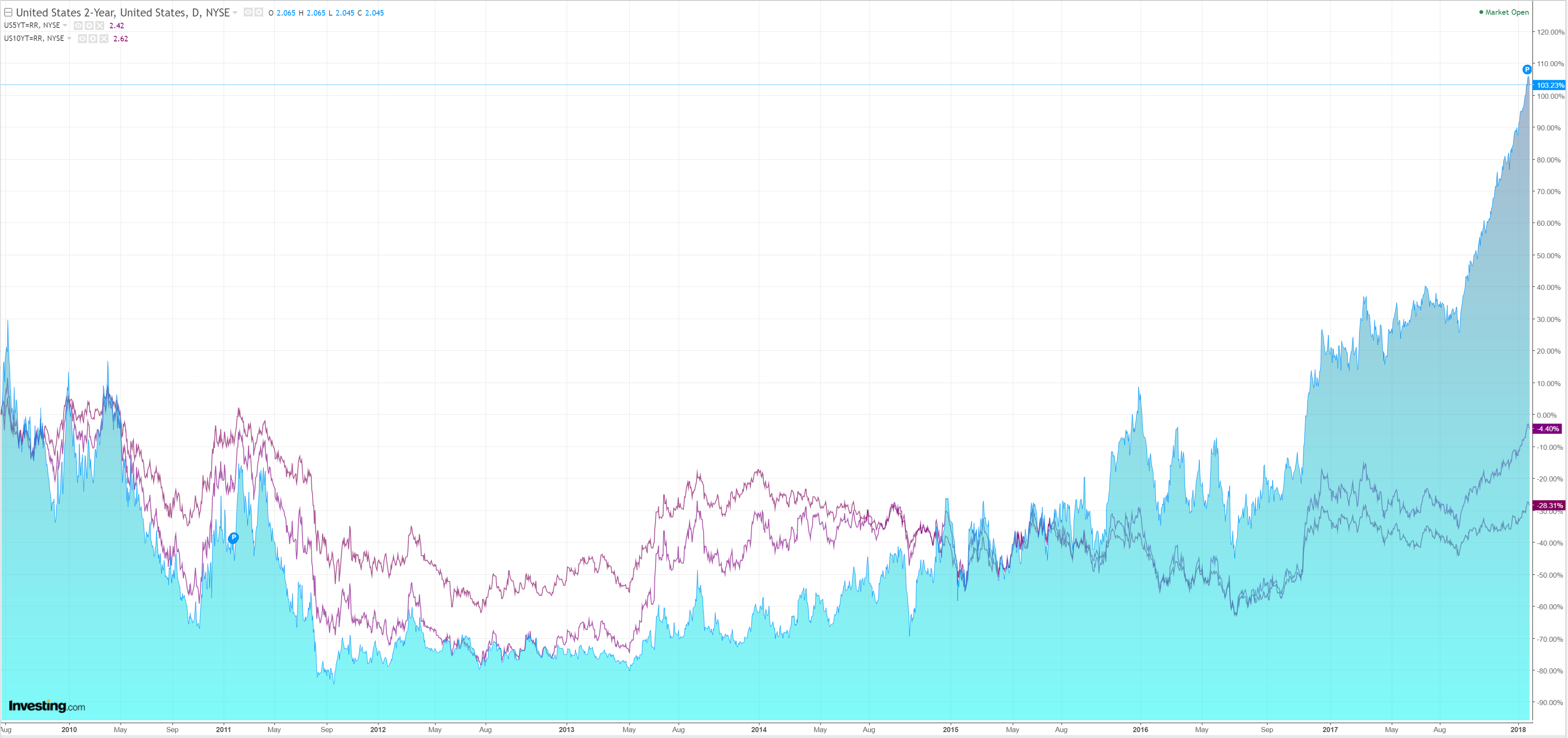

Treasuries were bought:

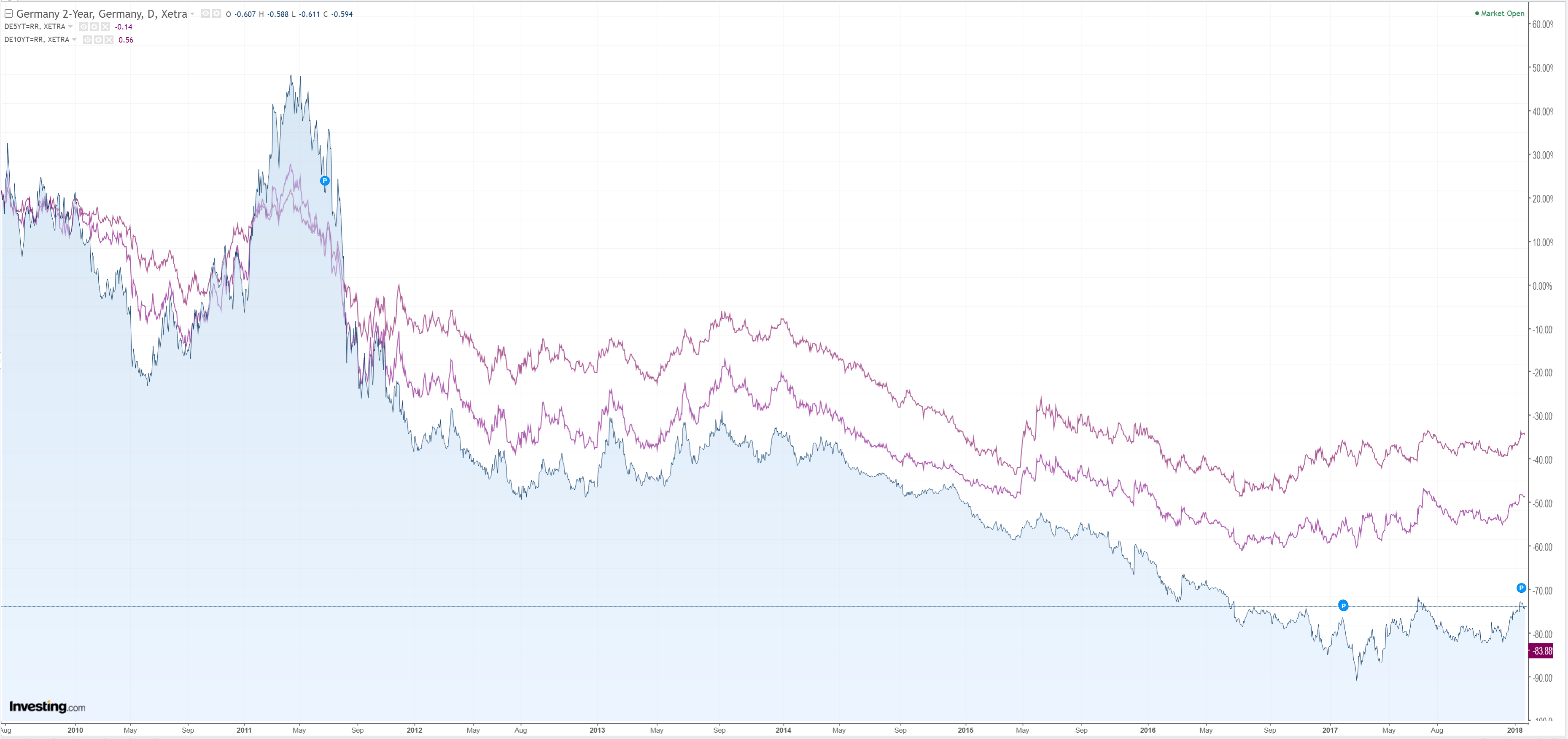

Bunds remain bogged:

And stocks hit new record highs:

Advertisement

This is the pattern we expect to be repeated throughout this year. A global boom passing Australia by as our key commodity prices actually fall with Chinese growth.

The weak USD is still being driven by excellent EUR data with ZEW, consumer confidence and ECB bank lending all ripping. Policy convergence remains the trade de jour.

And that still has US stocks in the sweet spot with tailwinds building all over the place:

Advertisement

Trump tax cuts generating short term investment and asset market inflation on capital management;

solid housing and consumption;

infrastructure and The Wall;

a weak currency;

a looming shale boom as oil hits new highs, and

tightening labour markets.

JPM has been run over by the stock market so upped its outlook:

We here raise our 2018 year-end S&P 500 target to 3000 (from 2800), reflecting upside forecasted by four of our five target models, as well as our 6% higher normalized EPS forecast reflecting the recurring impact from tax reform.

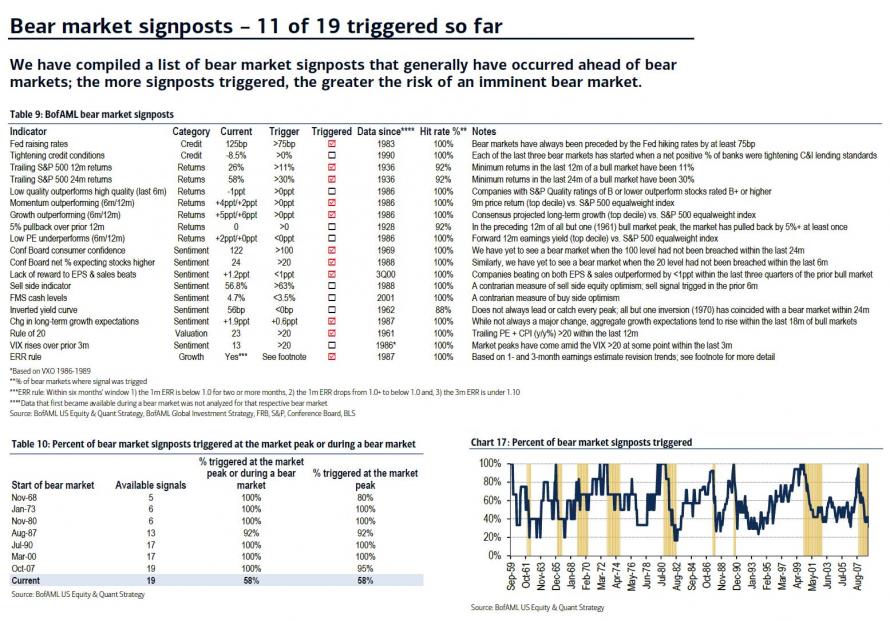

We are watching for signs to temper our enthusiasm on the S&P 500. And with 11 of our 19 bear market signposts having been triggered, the risk-adjusted reward of stocks appears less compelling. But note that since 1968, at least 80% of our signposts have been signaled ahead of prior market peaks.

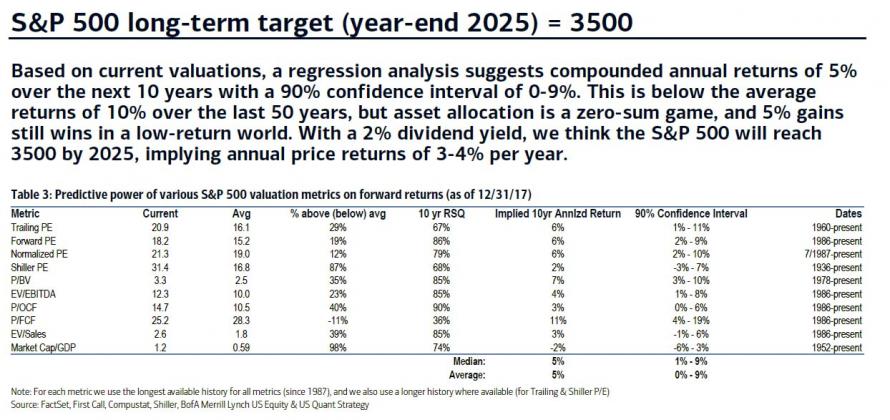

Based on current valuations, a regression analysis suggests compounded annual returns of 5% over the next 10 years with a 90% confidence interval of 0-9%. This is below the average returns of 10% over the last 50 years, but asset allocation is a zero-sum game, and 5% gains still wins in a low-return world. With a 2% dividend yield, we think the S&P 500 will reach 3500 by 2025, implying annual price returns of 3-4% per year.

But no need to panic yet…these indicators are still not at the extreme levels of bullishness that typically coincide with the end of bull markets…the great rotation out of bonds into stocks still has yet to occur, and while valuations for equities are elevated on most measures, stocks still appear historically cheap – by a wide margin – relative to bonds.

Advertisement

You can analyse these ratios all you like but it can’t capture the essence of what’s happening. Central banks have been whining about a lack of animal spirits for years now. Well… now they’ve got some and it ain’t going to stop until they run mad to exhaustion.

This is an outrageous short term US boom in the making. Of course afterwards is another matter entirely!

Advertisement

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long US growth equities so he is definitely talking his book.

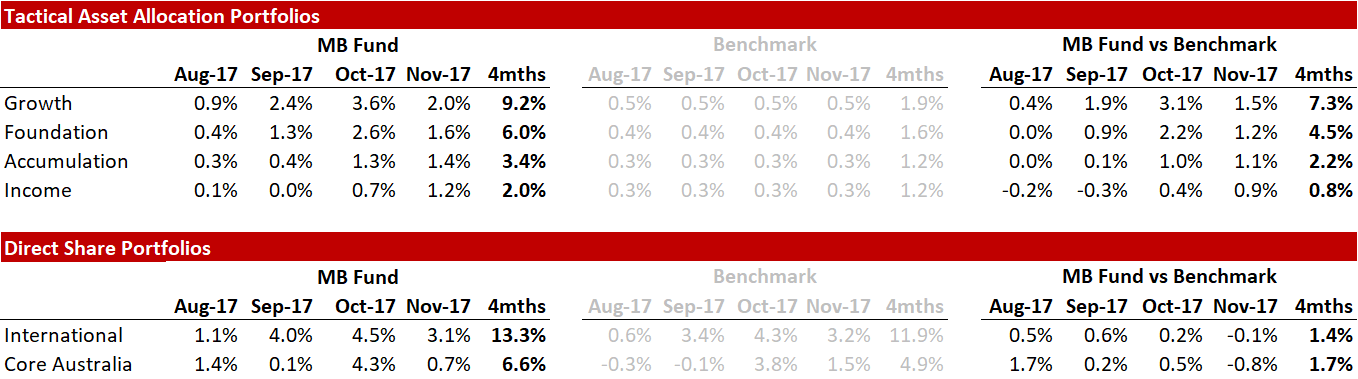

Here’s the recent fund performance:

Advertisement

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Source: Linear, Factset

Source: Linear, Factset