That’s the question the AFR asked on the weekend, sensibly enough, given it is a near certainty:

The newest of Shorten’s policies is a 30 per cent minimum tax rate on distributions to the adult beneficiaries of discretionary or family trusts. With farms exempt, the change will affect 2 per cent of taxpayers and 318,000 trusts. Yet the independent Parliamentary Budget Office estimates it would raise $4.1 billion over four years. Shorten’s beef is with the use of trusts for income streaming, which is not available to ordinary earners.

Beneficiaries under the age of 18 can only receive $416 a year tax-free from a trust in any case, with every dollar above $1307 effectively taxed at the top marginal rate of 47 per cent. So, under the current system, the ideal beneficiary is over 18 and not earning much – a university student, for example – because they will have a low marginal rate and possibly even room under the $18,200 tax-free threshold. Eligible beneficiaries include children, parents, grandparents, brothers, sisters, spouses, nephews and nieces. Uncles, aunts and cousins are ineligible.

…Aaron Fuda, a mortgage broker with Omniwealth, is advising investors who are intending to borrow in their SMSF to bring those plans forward. “The next federal election is due to be held in late 2018 or early 2019, and if Labor wins it has plans to introduce legislation to stop SMSF lending,” he says. “This is a significant change, and places uncertainty around SMSF lending until the next election. Something you hear a lot when a major change occurs is, ‘Oh darn, I was planning to do that’.”

…”It’s obviously a long hold, generally 10 years and usually more, so you’re through several property cycles before you look at selling,” he says. “I’ve got clients in their mid-30s who are buying property inside super. By the time they are 65, they are going to have an appreciated asset they can sell without any tax. You don’t know where property prices are going, but you’d assume upwards in the next 25 to 30 years.”

Which brings us to another of Labor’s policies: limit negative gearing to new property and halve the capital gains tax discount. Cortis says he is urging more caution about investing in real estate than he has for many years. This is the result of a combination of likely interest rate rises and the prospect of a Labor government. “The general consensus is that interest rates will rise by another half a per cent next year,” he says.

The macro-economic consequences of this are obvious. Property prices are going to fall. So are interest rates as the economy weakens. And the Australian dollar will follow both.

Labor will respond with fiscal spending and sustained mass immigration. More building in other words. However, the Labor strategy will run into trouble fast if and when the next global shock arrives which will threaten to turn the property correction disorderly just we run out of rate cuts. If they have any brains at all they will also smash the east coast gas cartel with much stronger domestic reservation.

For investors, the top priority, then, is to sell property. For local shares, sell banks and energy, hold building materials, education, tourism and dollar-exposed industrials. Miners are already a sell on a slowing China.

To me, the easiest and most obvious way to position yourself is unchanged with the arrival of Labor. Get your money offshore to benefit from growth in other already deleveraged economies and exploit your weak currency.

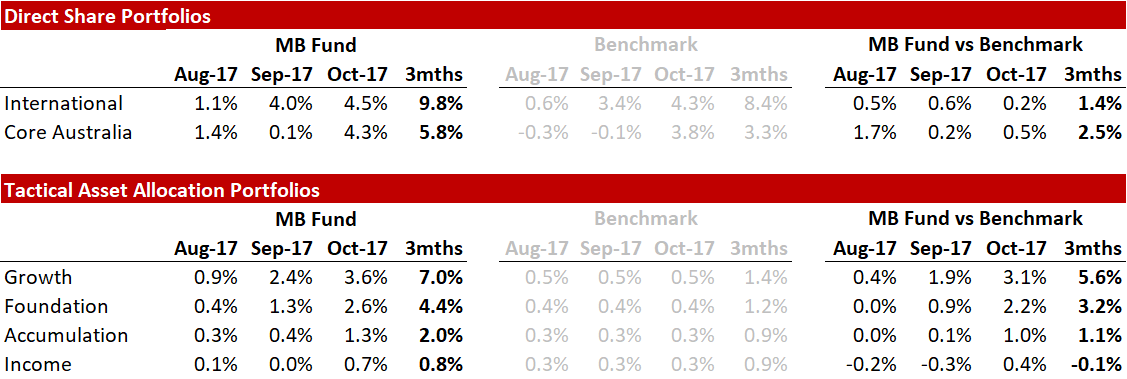

David Llewellyn-Smith is chief strategist at the MB Fund which is currently overweight international equities so he is definitely talking his book. The MB Fund offers one way to profit from a falling dollar:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If these themes and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.