From Bloomberg comes news that London’s house prices are falling at their fastest pace since the Global Financial Crisis:

Early data point to home values in London declining 2.7 percent in September from a year earlier, the most since 2009, according to Acadata and LSL property Services. A 0.7 percent fall in August marked the first negative reading since 2011 as sellers in some of the city’s most expensive boroughs, including Westminster, Wandsworth and Hammersmith, were forced to cut prices…

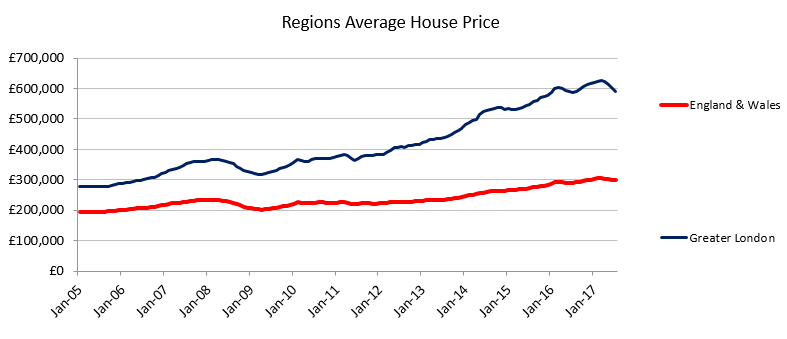

In London, values fell for a sixth consecutive month. If the provisional estimates are confirmed, the average price of a home in the capital was less than 582,000 ($773,000), the lowest since the end of 2015…

The downbeat picture was confirmed in a separate report from Rightmove Plc, which said asking prices in London fell an annual 2.5 percent in October. While they rose 3.1 percent on the month, driven by owners of more expensive properties, achieving these prices is far from assured as buyers now have more choice, according to Rightmove director Miles Shipside…

This looks legit, with Academetrics – considered the most accurate index since it comprises all sales lodged with the UK Land Registry – also showing that London’s house prices had fallen in the four months to July (latest available):

Advertisement

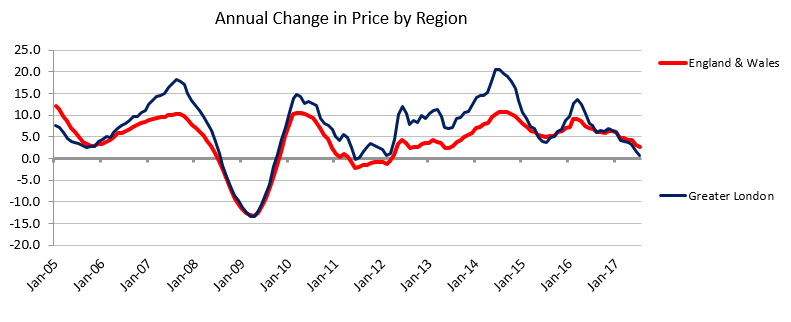

With London’s annual price growth about to turn negative as at July:

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.