Earlier this month, The Grattan Institutepublished a report outlining in all its hideous glory how older Australians have gotten wealthy while the young have been left behind:

Data from the Australian Bureau of Statistics (ABS) shows that older Australians are capturing an increasing share of the nation’s wealth, and the house-price boom is a major cause of the growing divide between the generations.

As you can see in the following chart, households headed by 65-74-year-olds were on average A$480,000 wealthier in 2015-16 than households in the same age group 12 years ago. And that’s after taking inflation into account and despite the damage caused by the global financial crisis. Households headed by 45-54-year-olds are A$400,000 richer.

In contrast, households headed by 35-44-year-olds are on average only A$120,000 wealthier – and for 25-34-year-olds the figure is just A$40,000.

Property is a key factor for wealth disparity…

The next chart shows that for households headed by someone aged 75 or over, greater property wealth contributed about three-quarters of the increase in their total net wealth. For households headed by 65-74-year-olds and 55-64-year-olds, property contributed about half of the total increase in wealth.

But for younger Australians, again it is a different story.

Bigger mortgages largely offset the increase in property wealth for households headed by 25-34-year-olds and 35-44-year-olds. Baby Boomers have also used the superannuation system to build their wealth.

…home ownership rates among households headed by 25-34-year-olds fell between 1981 and 2016, from more than 60% to 45%. For households headed by 35-44-year-olds the fall was from 75% to around 62%. Home ownership rates are also falling for households headed by 45-54-year-olds…

Australia is becoming wealthier, but much of the increase is concentrated in the hands of older generations. The trend is unmistakable: unless something changes, the young will fall further behind and inequality will get worse.

Late last week, the Federal Reserve Bank of St Louis published a report revealing that older Americans too have made out like bandits while younger Americans have been left behind:

Key measures such as health insurance, poverty, wealth and income show that senior citizens are benefiting more than other age groups from improved living standards…

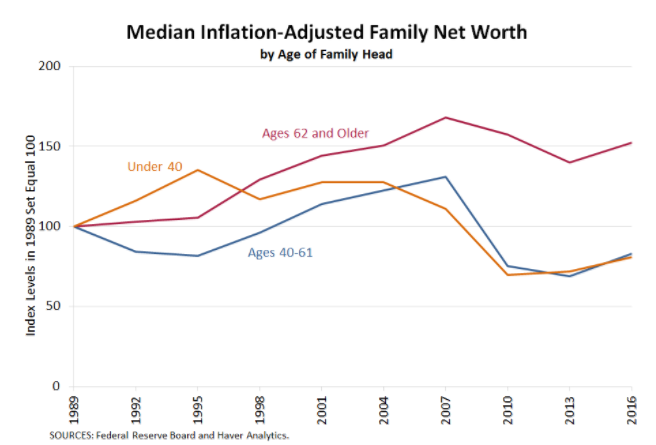

Median Household Wealth

The household wealth of a typical older American family is much greater today than the wealth of its counterpart of the same age a quarter-century ago. The median inflation-adjusted net worth of a family headed by someone aged 62 or older was 52 percent greater in 2016 than in 1989.

Meanwhile, among younger families, the typical family today has lower wealth than its counterpart a quarter-century ago:

The median family headed by someone aged 40-61 in 2016 was about 17 percent less wealthy than its counterpart in 1989.

The median wealth of a family headed by someone under 40 was about 19 percent lower in 2016 than its counterpart in 1989…

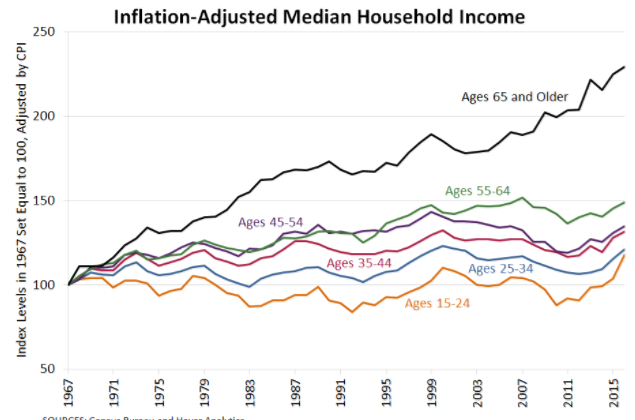

Median Household Income

…the exceptional nature of household income growth among older Americans extends far back in time. Beginning in 1967 (with the advent of the current Census Bureau data series), the median real income among households headed by someone 65 years old or older has increased much more than among any other age group.

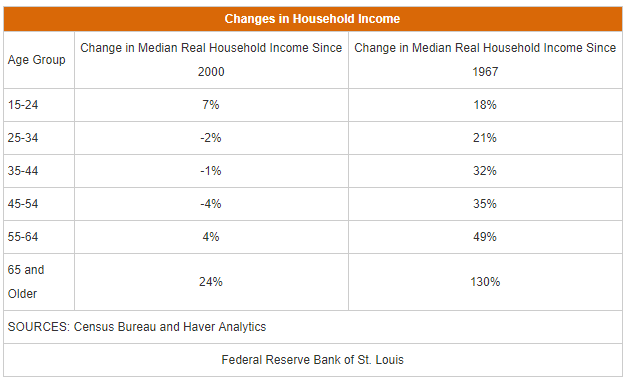

As seen in the table below, it’s not only the oldest age group that has benefited, though the older the age group, the greater the long-term gain in real median household income since 1967.

This time four years ago, legendary baby boomer investor and founder of Duquesne Capital, Stanley Drukenmiller, gave speaking tours to crowds of students at Berkeley, Stanford, Brown, U.S.C., Bowdoin, Notre Dame and NYU, urging them to take action against intergenerational unfairness:

“My generation — we brought down the president in the ’60s because we didn’t want to go into the war against Vietnam,” Druckenmiller told an overflow crowd at Notre Dame last week. “People say young people don’t vote; young people don’t care. I’m hoping after tonight, you will care. There is a clear danger to you and your children”…

With graph after graph, [Drukenmiller] show[s] how government spending, investments, entitlements and poverty alleviation have overwhelmingly benefited the elderly since the 1960s and how the situation will only get worse as our over-65 population soars 100 percent between now and 2050, while the working population that will have to support them — ages 18 to 64 — will grow by 17 percent. This imbalance will lead to a huge burden on the young and, without greater growth, necessitate cutting the very government investments in infrastructure, Head Start, and medical and technology research that help the poorest and also create the jobs of the future…

It seems deeply offensive to me that we will be asking these poor children from Harlem to subsidize a generation that is, by and large, more well-off than they are, and then leave them deeply indebted in an America that had eaten the seed corn of the next generation.”

Among the measures recommended by Drukenmiller included: increasing taxes on capital gains, dividends and carried interest – which currently overwhelmingly benefit the wealthy and retired – so that they more closely match taxes on wage and salary earnings; and means testing health care and social security so that they are needs-based not aged-based.

Sadly, it seems nobody listened in the proceeding four years, with the incomes and wealth of older Americans soaring. And the situation is set to worsen with President Trump’s tax cut agenda.

Of course, it’s the very same story in the UK, as well other developed nations like New Zealand.

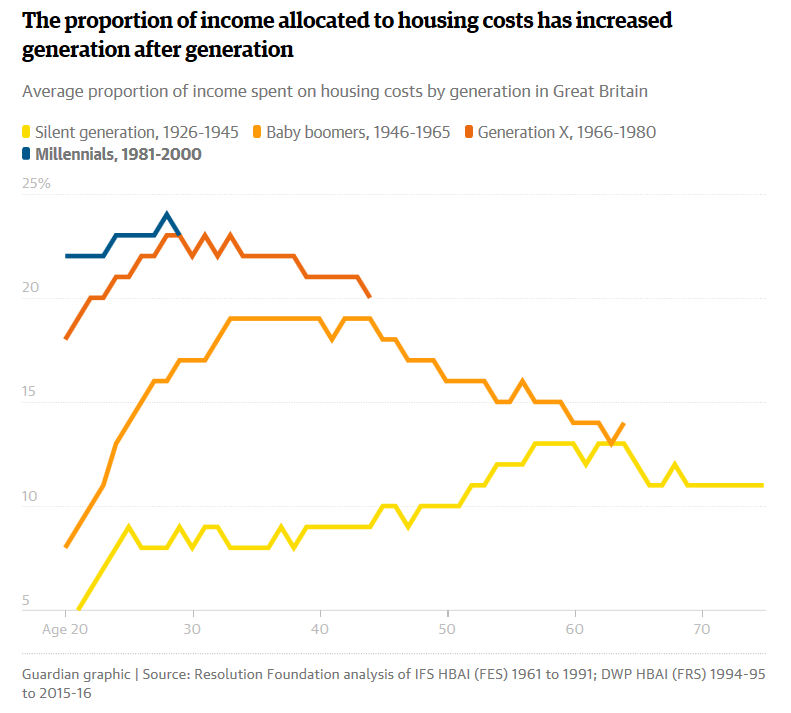

Just last month, The Guardian posted a depressing report on how UK Millennials are spending three times more of their incomes on housing than their grandparents and often living in worse accommodation:

The generation currently aged 18-36 are typically spending over a third of their post-tax income on rent or about 12% on mortgages, compared with 5%-10% of income spent by their grandparents in the 1960s and 1970s. Despite spending more, young people today are more likely to live in overcrowded and smaller spaces, and face longer journeys to work – commuting for the equivalent of three days a year more than their parents.

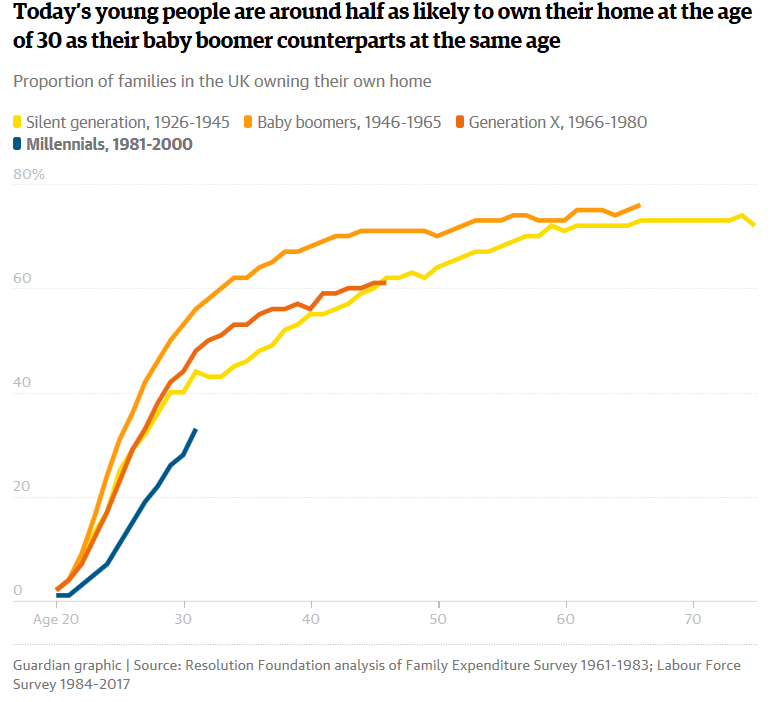

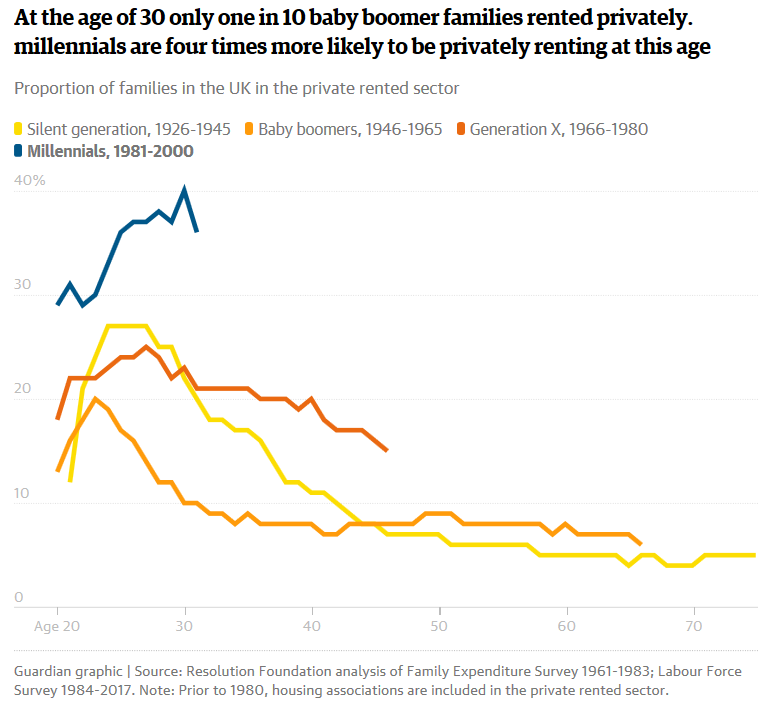

The research by Willetts’ intergenerational commission at the Resolution Foundation thinktank also reveals that today’s 30-year-olds are only half as likely to own their own home as their baby boomer parents. They are four times as likely to rent privately than two generations ago, a sector which has the worst record for housing quality, the report claims…

A young family today has to save for 19 years on average to afford a typical deposit compared with three years for the previous generation, the report states…

Parliaments world-wide desperately need to be occupied by a dedicated youth political party to apply a lightning rod and to educate and mobilise their ravaged young.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.