Advertisement

In our last report on the Brisbane property market, released in March 2015, I argued that investment fundamentals and valuations in Brisbane property were sound relative to the other major capitals, but that the economic outlook was mixed, thus posing some risks to potential investors.

With Sydney’s and Melbourne’s housing markets continuing their bull runs and in clear bubble territory, we thought it was time to revisit the Brisbane housing market to see if now could be a good time to invest.

A decade of stagnation:

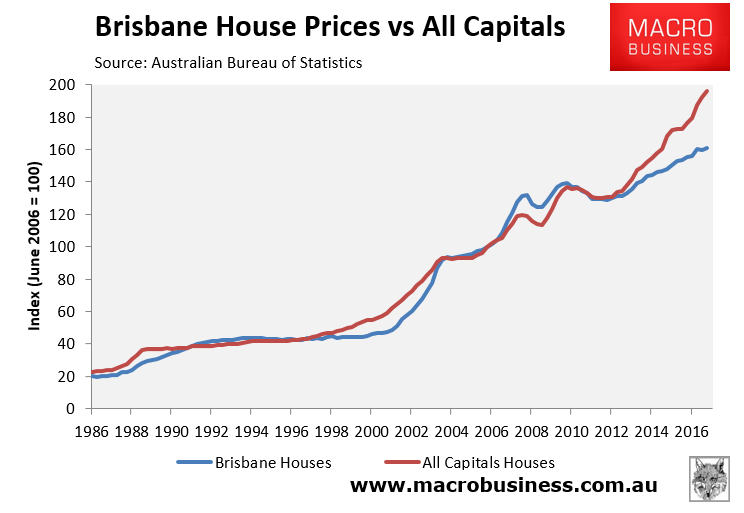

The below chart tracks detached house prices, as reported by the Australian Bureau of Statistics (ABS), to June 2017:

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement