David Llewellyn-smith is Chief Strategist at the MacroBusiness Fund which is currently allocated 70% offshore so he is unquestionably talking his book. The MacroBusiness Fund has been put together to help readers of the blog take advantage of its themes and put the power of MacroBusiness to work in their portfolio. You can invest directly in the local or international share portfolios or let us determine the appropriate risk mix between them and other assets for you. If you’re interested then submit your details below and we’ll be in touch.

Last night DXY roared and the odds are growing that it has bottomed:

The Aussie dollar broke lower against DMs and the odds are rising that the super spike is over:

Advertisement

And EMs:

Gold was smacked:

Brent flamed out:

Advertisement

Base metals fell:

Big miners too:

EM stocks eased some more:

Advertisement

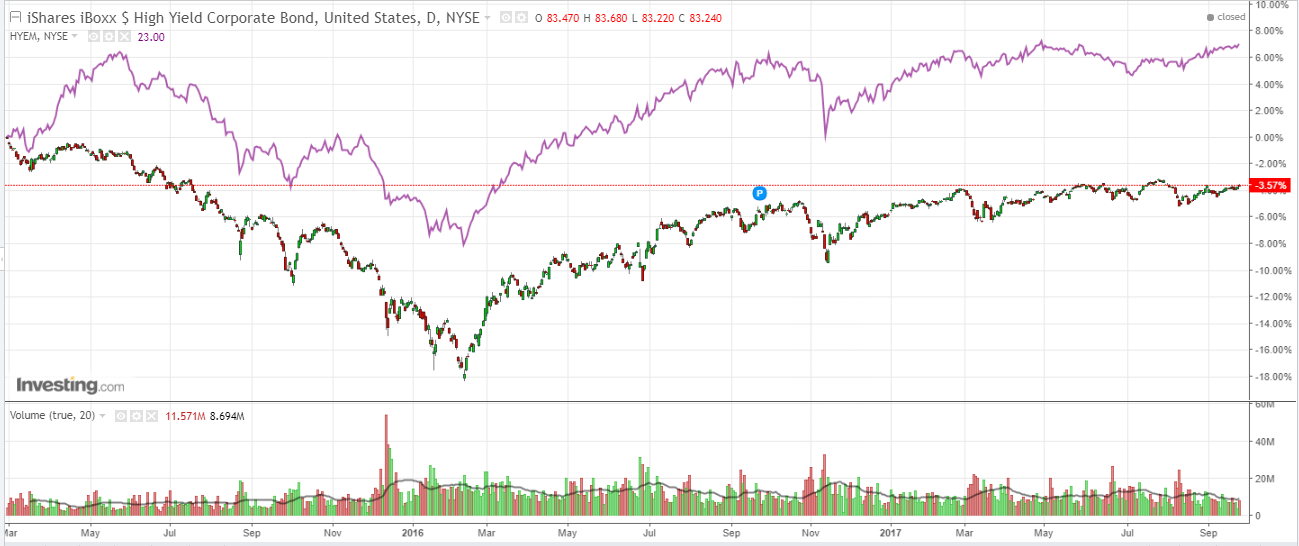

High yield firmed:

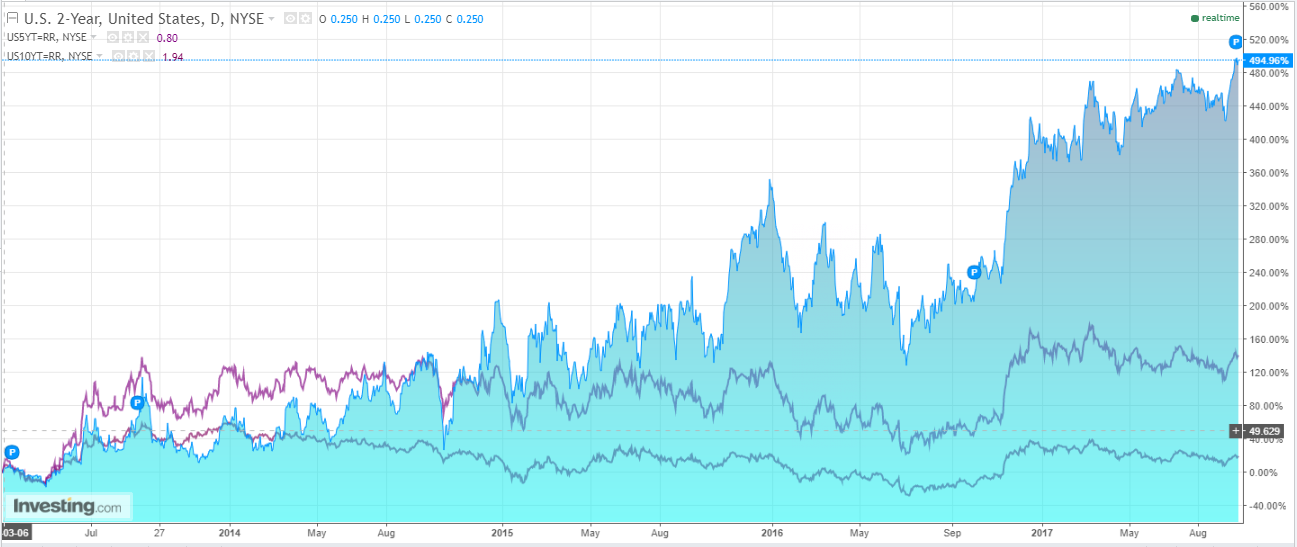

The US curve flattened:

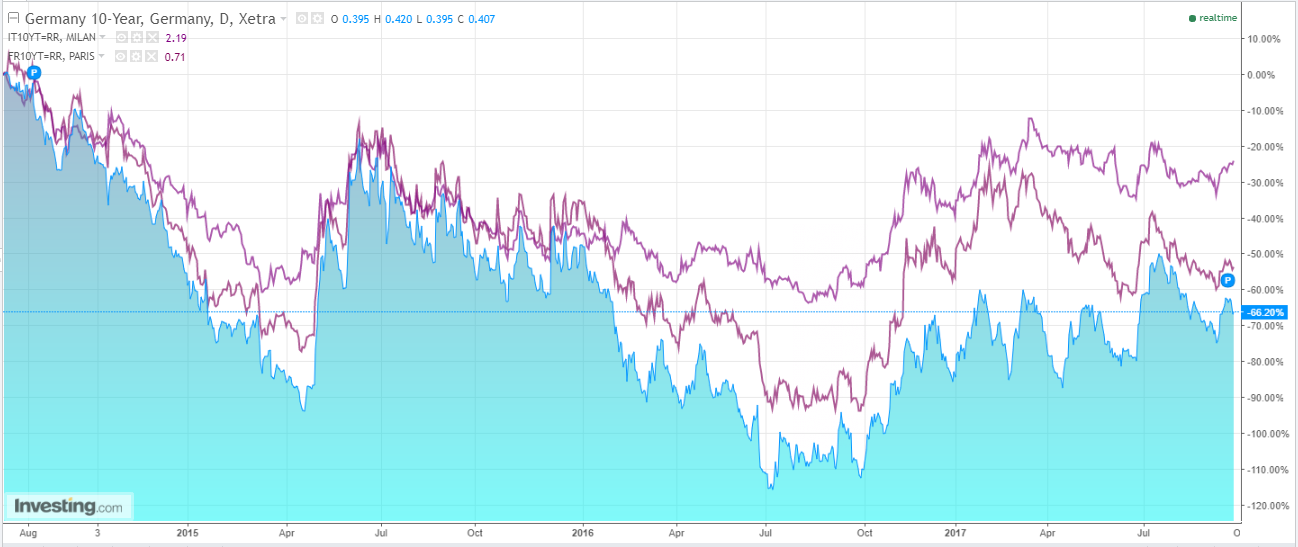

European spreads blew out:

Advertisement

And stocks eased:

The USD/EUR oil tanker is turning and with it the Australian dollar. Last night the ECB signaled more concern with the strong EUR:

The euro zone economy is gaining momentum but the euro’s firming has a dampening impact on inflation and the European Central Bank should consider both factors when deciding on its next policy move, Governing Council member Jozef Makuch said.

“As for the discussion on when ECB should decide on recalibration of quantitative easing: the economy is improving, on the other hand the euro exchange rate is getting stronger,” Makuch told a news conference on Tuesday. “The risks are on both sides, the ECB has to consider them carefully.”

Advertisement

While across the pond Janet Yellen hawked it up:

Today I will discuss uncertainty and monetary policy, particularly as it relates to recent inflation developments. Because changes in interest rates influence economic activity and inflation with a substantial lag, the Federal Open Market Committee (FOMC) sets monetary policy with an eye to its effects on the outlook for the economy. But the outlook is subject to considerable uncertainty from multiple sources, and dealing with these uncertainties is an important feature of policymaking. Key among current uncertainties are the forces driving inflation, which has remained low in recent years despite substantial improvement in labor market conditions. As I will discuss, this low inflation likely reflects factors whose influence should fade over time. But as I will also discuss, many uncertainties attend this assessment, and downward pressures on inflation could prove to be unexpectedly persistent. My colleagues and I may have misjudged the strength of the labor market, the degree to which longer-run inflation expectations are consistent with our inflation objective, or even the fundamental forces driving inflation. In interpreting incoming data, we will need to stay alert to these possibilities and, in light of incoming information, adjust our views about inflation, the overall economy, and the stance of monetary policy best suited to promoting maximum employment and price stability.

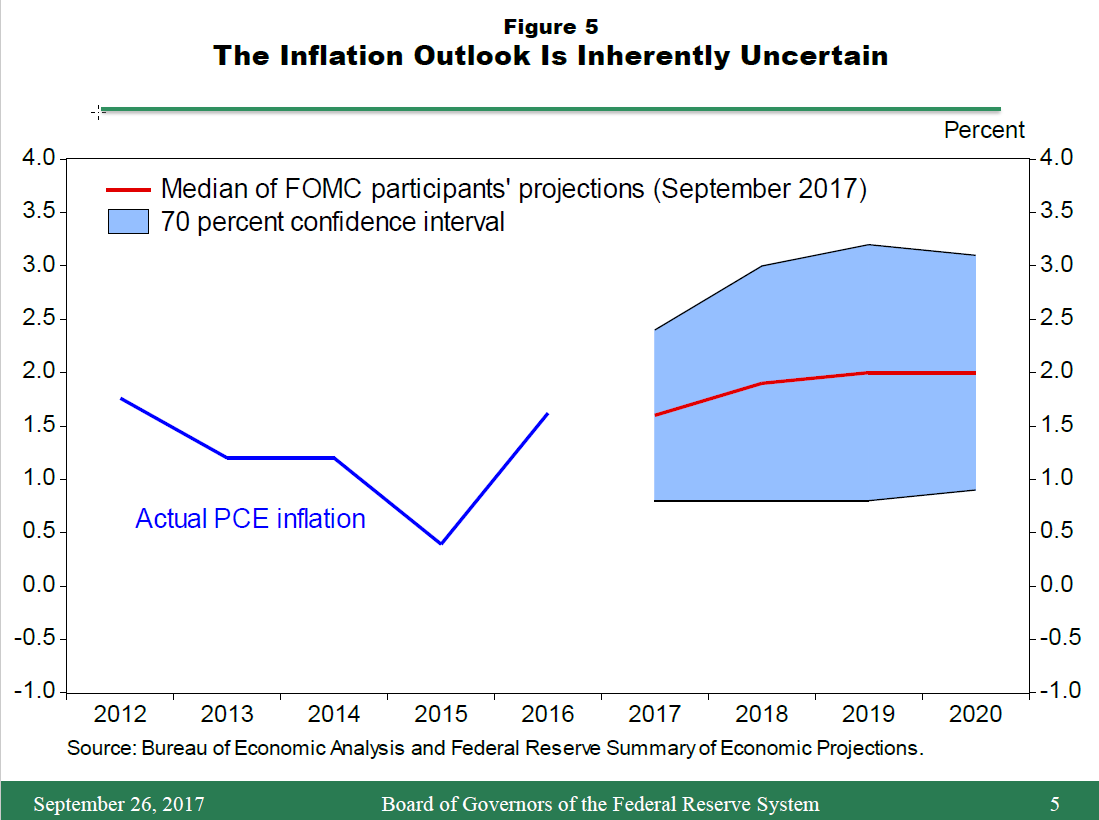

…Although we judge that inflation will most likely stabilize around 2 percent over the next few years, the odds that it could turn out to be noticeably different are considerable. This point is illustrated by figure 5. Here the red line indicates the median of the latest inflation projections submitted by FOMC participants that I showed previously. The pertinent feature of this figure is the blue shaded region around the red line, which shows a 70 percent confidence interval around FOMC participants’ median outlook. The width of this region reflects the average accuracy of inflation projections made by private and government forecasters over the past 20 years. As the figure shows, based on that history, there is a 30 percent probability that inflation could be greater than 3 percent or less than 1 percent next year.

Most of this uncertainty reflects the influence of unexpected movements in oil prices and the foreign exchange value of the dollar, as well as that of idiosyncratic developments unrelated to broader economic conditions. These factors could easily push overall inflation noticeably above or below 2 percent for a time. But such disturbances are not a great concern from a policy perspective because their effects fade away as long as inflation expectations remain anchored.

For this reason, the FOMC strives to look through these transitory inflation effects when setting monetary policy. Such was the case when rising oil prices pushed headline inflation noticeably above 2 percent for several years prior to the financial crisis. Similarly, the Committee substantially discounted the reductions in inflation that occurred from 2014 through 2016 as a result of the decline in oil prices and the effects of the dollar’s appreciation on import prices.

How should policy be formulated in the face of such significant uncertainties? In my view, it strengthens the case for a gradual pace of adjustments. Moving too quickly risks overadjusting policy to head off projected developments that may not come to pass. A gradual approach is particularly appropriate in light of subdued inflation and a low neutral real interest rate, which imply that the FOMC will have only limited scope to cut the federal funds rate should the economy be hit with an adverse shock. But we should also be wary of moving too gradually. Job gains continue to run well ahead of the longer-run pace we estimate would be sufficient, on average, to provide jobs for new entrants to the labor force. Thus, without further modest increases in the federal funds rate over time, there is a risk that the labor market could eventually become overheated, potentially creating an inflationary problem down the road that might be difficult to overcome without triggering a recession. Persistently easy monetary policy might also eventually lead to increased leverage and other developments, with adverse implications for financial stability. For these reasons, and given that monetary policy affects economic activity and inflation with a substantial lag, it would be imprudent to keep monetary policy on hold until inflation is back to 2 percent.

…To conclude, standard empirical analyses support the FOMC’s outlook that, with gradual adjustments in monetary policy, inflation will stabilize at around the FOMC’s 2 percent objective over the next few years, accompanied by some further strengthening in labor market conditions. But the outlook is uncertain, reflecting, among other things, the inherent imprecision in our estimates of labor utilization, inflation expectations, and other factors. As a result, we will need to carefully monitor the incoming data and, as warranted, adjust our assessments of the outlook and the appropriate stance of monetary policy. But in making these adjustments, our longer-run objectives will remain unchanged–to promote maximum employment and 2 percent inflation.

December rate hike odds jumped to 80%. With the lower dollar, tax reform, oil restive, tightish labour market and reconstruction all set to boost the US next year the USD is starting to swing.

The nervous ECB, German election of AfD and forthcoming Italian election are undermining EUR.

Advertisement

Add a slowing China and very long market and the Aussie dollar looks like a sitting duck.

Advertisement

{kind=link}