And US stocks went bananas for carefree record closes:

Perhaps it was the US dedicating itself to the extinction of the species that did it (as Trump withdrew from Paris Agreement). Might as well go up on the way out.

Advertisement

Thinking a little more short term, US data was good. ISM was firm enough:

“The May PMI® registered 54.9 percent, an increase of 0.1 percentage point from the April reading of 54.8 percent. The New Orders Index registered 59.5 percent, an increase of 2 percentage points from the April reading of 57.5 percent. The Production Index registered 57.1 percent, a 1.5 percentage points decrease compared to the April reading of 58.6 percent. The Employment Index registered 53.5 percent, an increase of 1.5 percentage points from the April reading of 52 percent. The Inventories Index registered 51.5 percent, an increase of 0.5 percentage point from the April reading of 51 percent. The Prices Index registered 60.5 percent in May, a decrease of 8 percentage points from the April reading of 68.5 percent, indicating higher raw materials prices for the 15th consecutive month, but at a noticeably slower rate of increase in May compared with April. Comments from the panel generally reflect stable to growing business conditions, with new orders, employment and inventories of raw materials all growing in May compared to April. The slowing of pricing pressure, especially in basic commodities, should have a positive impact on margins and buying policies as this moderation moves up the value chain.”

And ADP strong:

Advertisement

Private sector employment increased by 253,000 jobs from April to May according to the May ADP National Employment Report®. … The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.

“May proved to be a very strong month for job growth,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “Professional and business services had the strongest monthly increase since 2014. This may be an indicator of broader strength in the workforce since these services are relied on by many industries.”

Mark Zandi, chief economist of Moody’s Analytics said, “Job growth is rip-roaring. The current pace of job growth is nearly three times the rate necessary to absorb growth in the labor force. Increasingly, businesses’ number one challenge will be a shortage of labor.”

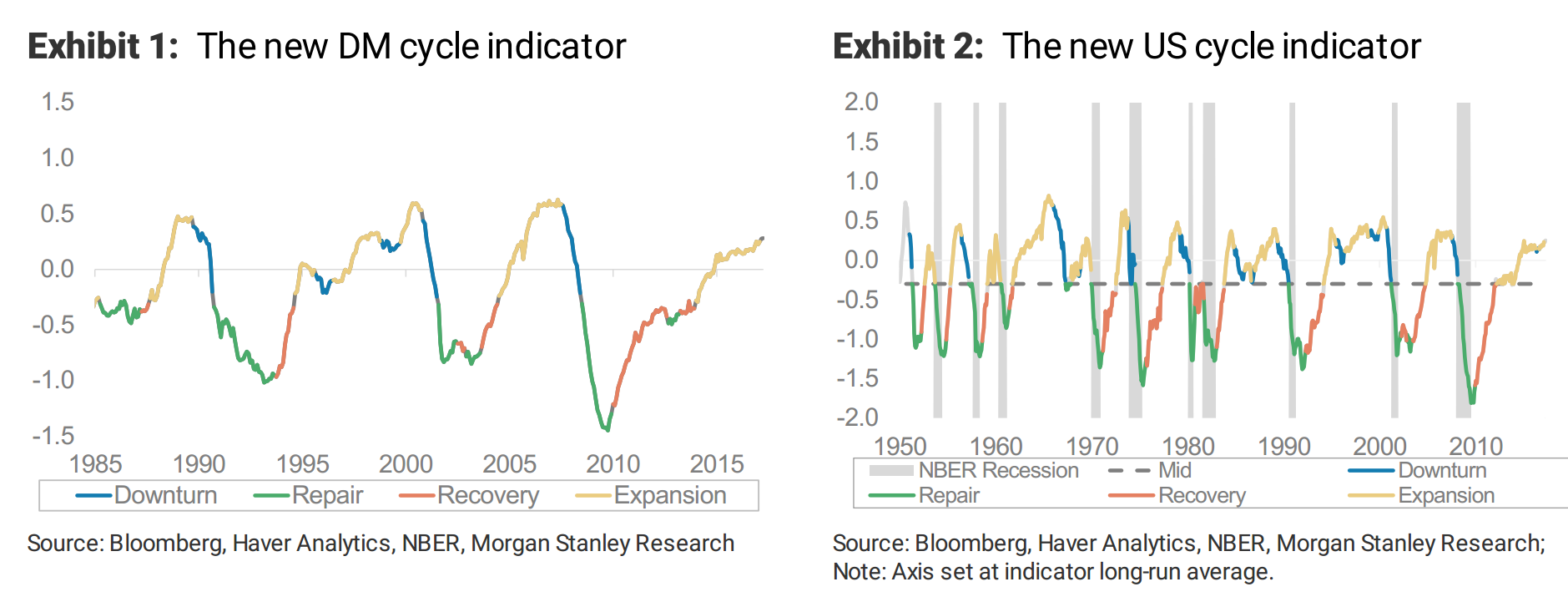

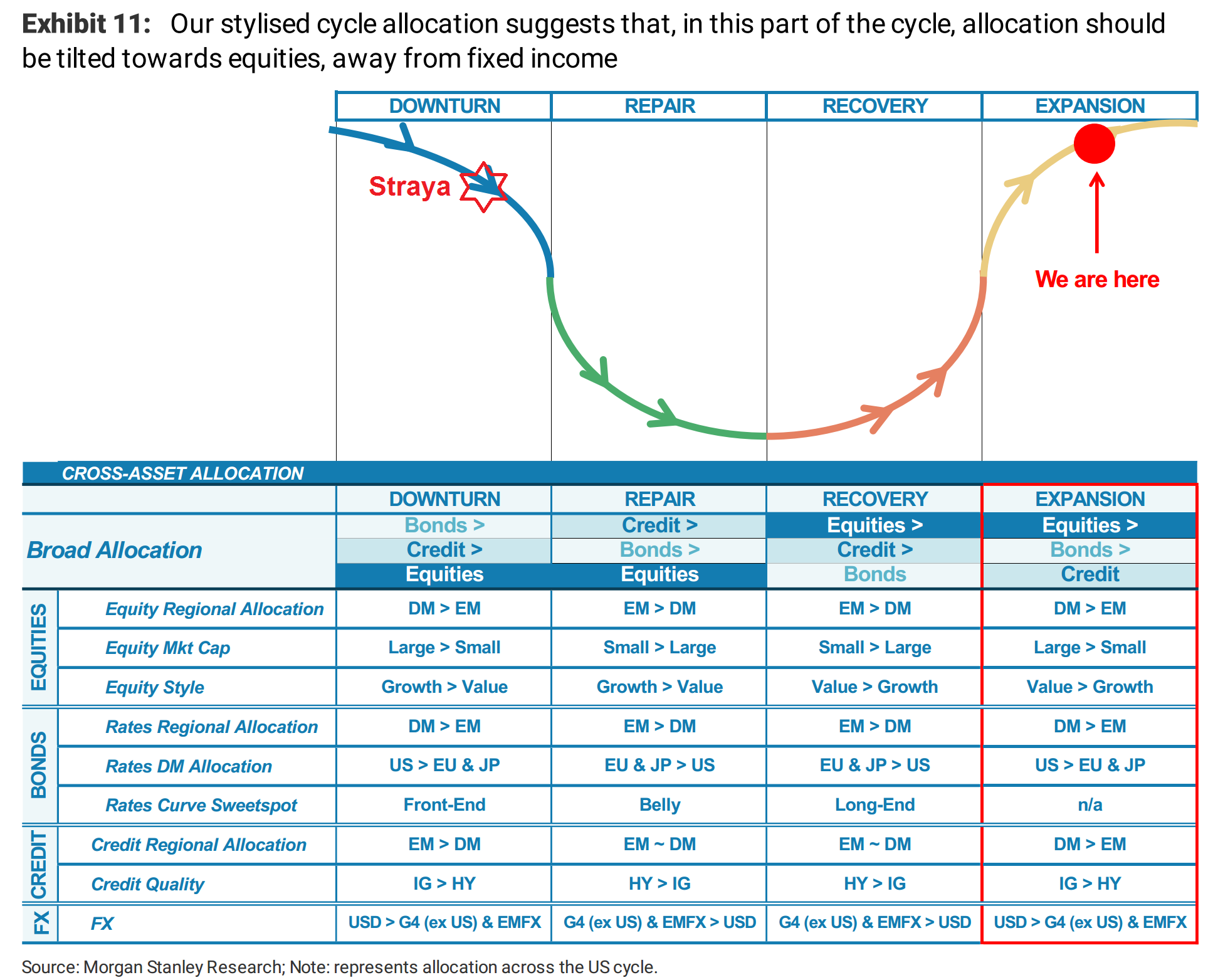

How long can the US expansion continue? Morgan Stanley addresses that question:

DM late-cycle’expansion’ continues: Our new cycle indicators confirm that the DM market ‘expansion’ remains intact,after a pause last year. The ‘expansion’ is particularly strong in Europe and Japan, driven by synchronous, buoyant macro data. The changes to our methodology mean that the US cycle indicator is now back in the ‘expansion’ phase,after a transitory dip into ‘downturn’ territory last year.

But how long can this ‘expansion’ last? The current US cycle stands as one of the longest in history. A large deterioration in macro data is needed to move our cycle indicator towards ‘downturn’and, looking beyond, metrics which have had a good track record of ‘calling’ cycle turns like M2growth, capacity utilisation and credit spreads all still look quite relaxed compared to prior end-of-cycle experiences. We believe we’d need to see a sustained widening in credit spreads, as well as further policy tightening, before this cycle ends.

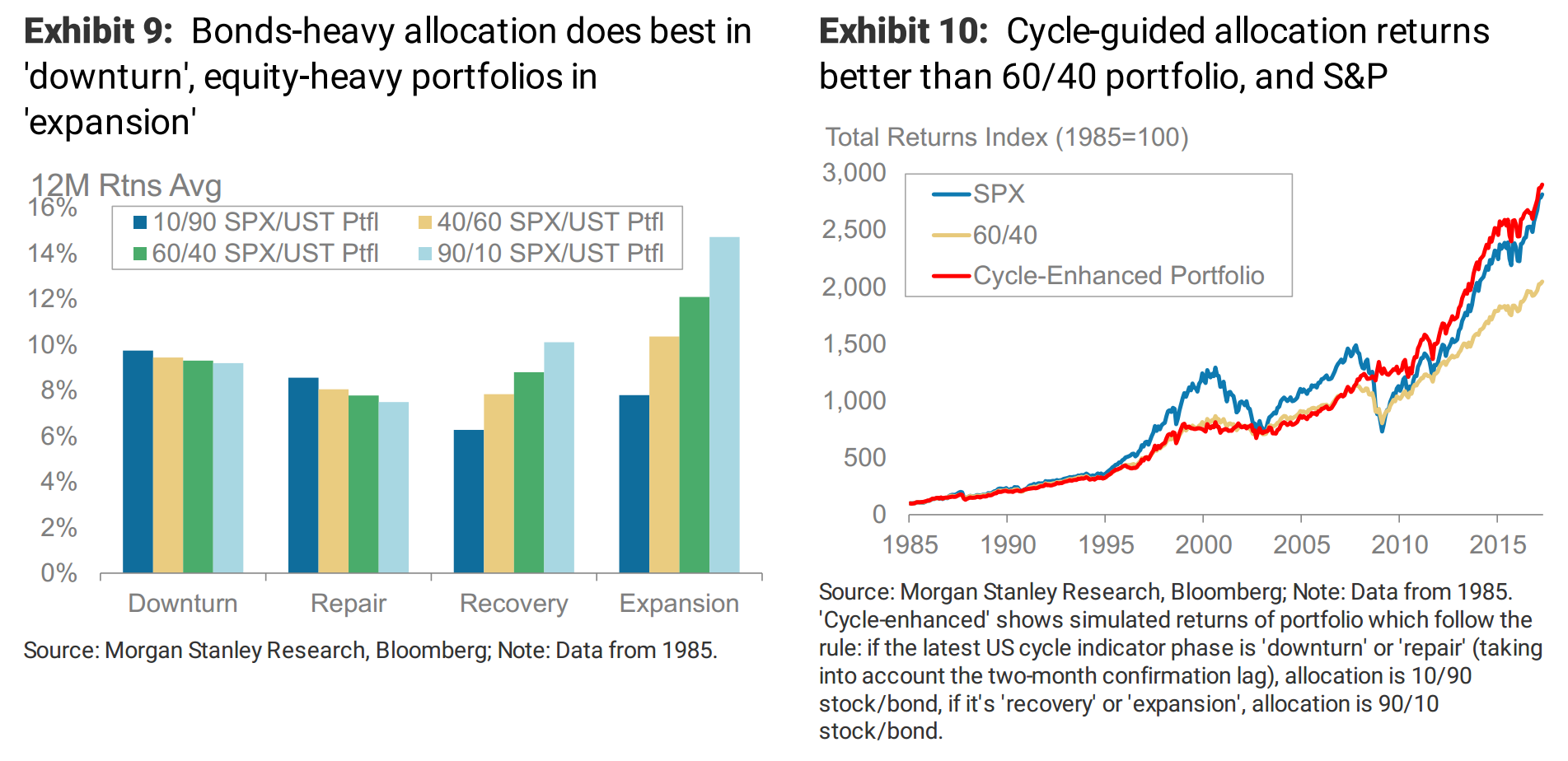

The cycle matters for returns and portfolio allocation: Our analysis suggests that bonds outperform in ‘downturns’, while high equity weights do best in ‘expansions’. Armed with this stylised strategy,a simple ‘cycle-enhanced’ portfolio would have seen much better risk/reward than stocks or 60/40 stock/bond portfolios. We introduce our stylised cycle allocation and returns scorecard, which summarises the best allocation strategies and asset return boosts across the cycle.

Investment implications – keep the faith in equities: Given the late-cycle environment, we recommend an overweight in equities to reap the higher-than normal returns typical in an ‘expansion’. Where we are in the cycle also supports our current underweight position in bonds,and more cautious view on corporate credit, in anticipation of the poor risk/reward usually seen by the asset class late cycle.

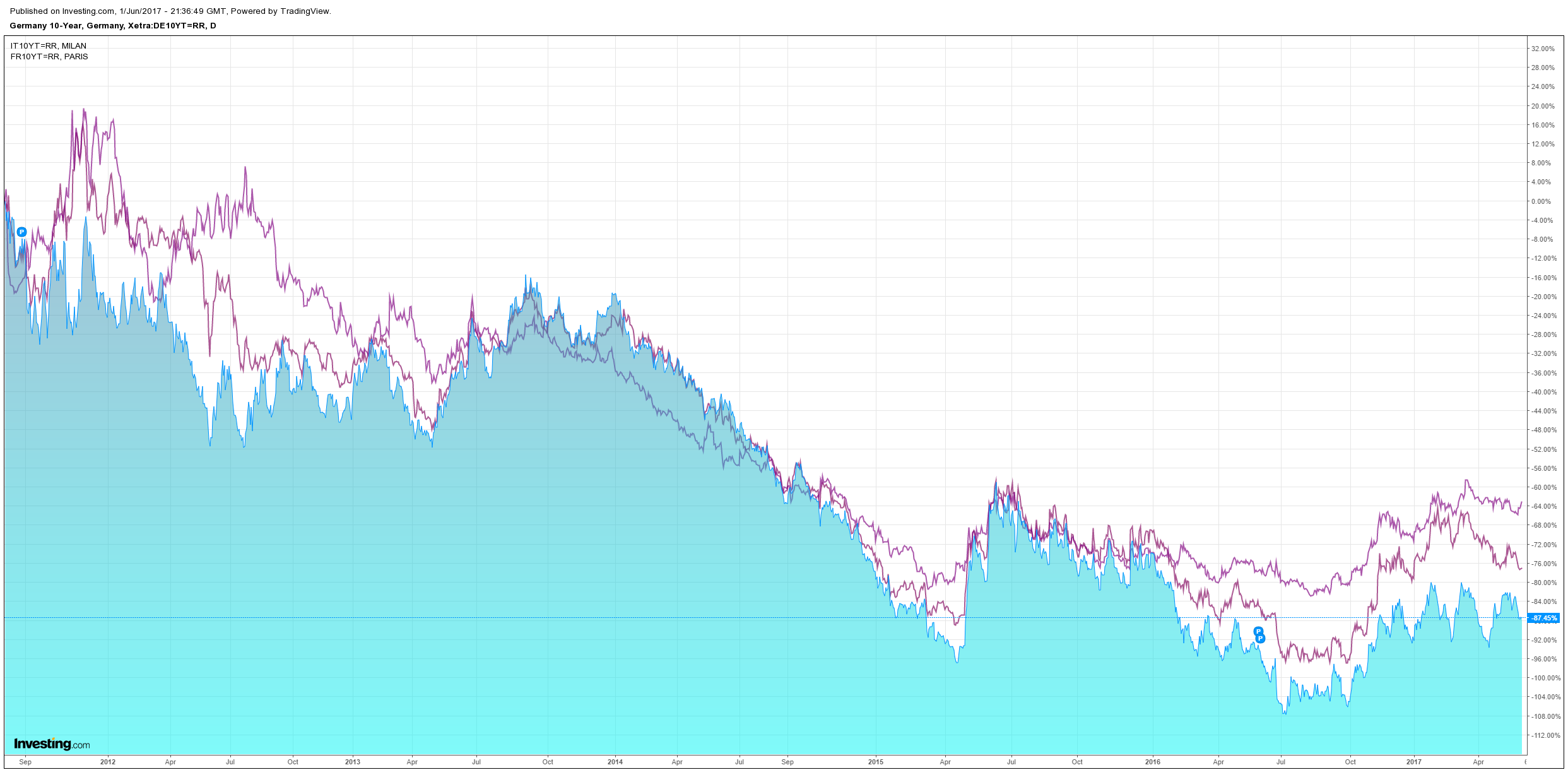

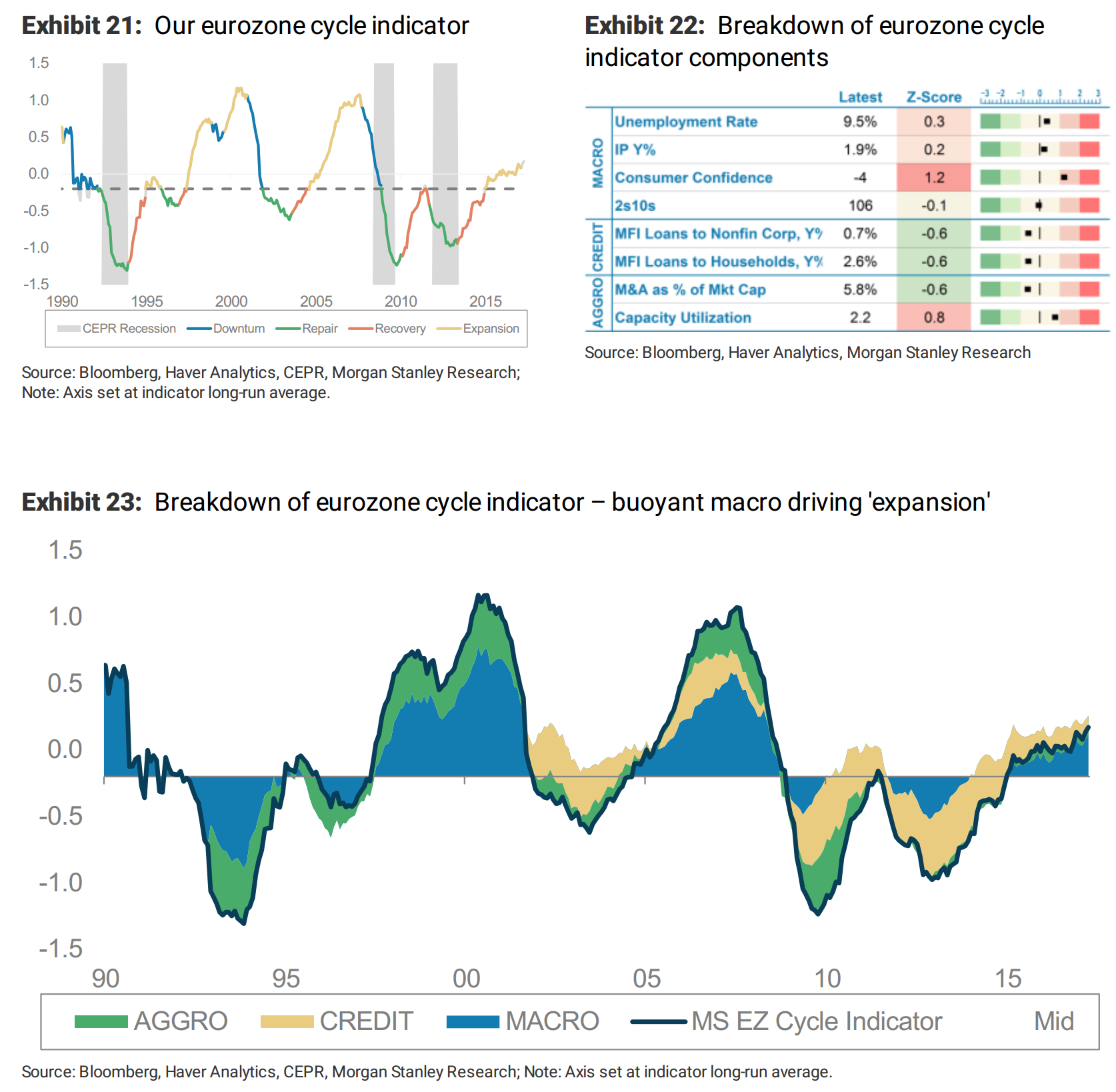

Quite right. A couple of extra charts fill out the picture. The European cycle has more room to run than the US:

Advertisement

And the Australian cycle has completely the wrong end of the stick (I’ve added the star):

Advertisement

MB Fund is allocated accordingly. We’re mulling the risk of the Italian election but for now remain (relative to MSCI):

overweight European stocks;

underweight US stocks;

underweight Australian stocks;

overweight Aussie bonds (creeping out the curve now);

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.