From Santos CEO Kevin Gallagher today on the domestic reservation mechanism:

We believe there are better ways to manage this situation than government intervention that might expose the taxpayer to compensation payments while not delivering any public benefit.

Remember this crisis is about pricing not supply, which is why I have questioned the net contributor measure as not the right measure.

It potentially distorts the market to make expensive gas available. It represents neither the lowest cost form of Government intervention nor delivers the greatest public benefit in terms of policy options available to the Government.

And even more importantly, gas market intervention could have serious unintended consequence for the gas industry and the east coast manufacturing industry. It will not solve the long-term problem of falling supply.

We believe it (the ADGSM) is targeting the wrong LNG producers for the wrong reasons.

All of GLNG’s gas is contracted overseas, GLNG has no cheap, surplus gas — indeed it’s all contracted at premium prices.

The ADGSM, if it is triggered, will therefore force the most expensive gas (for LNG buyers) to be diverted back into the east coast market. GLNG, if required to do this, will obviously seek an equitable commercial outcome from domestic customers as anyone who had made an $18 billion investment in a project would.

The mechanism certainly looks flawed but not because of any of this rubbish. It simply isn’t tough enough, from Credit Suisse:

■ Santos Horizon contract seemingly counts as ‘own gas’, not third-party which will reduce the size of any net deficit for GLNG: ‘own gas’ for the purposes of determining a net contributor means gas produced from one or more tenements:(a) owned by the LNG Project; or (b) wholly or partly owned by one or more entities of the LNG Project, where: (i) the gas is contracted directly to supply the LNG Project; and (ii) the gas was primarily developed for the purpose of the export. At face value there looks like potentially only ~250TJ/d (~91PJa) that could even be up for debate of available to divert domestically. What exactly happens if the shortage is bigger than this?

■ Process seemingly rules out use for Winter 2017: under the draft, where possible the minister will declare that a forthcoming calendar year is up for consideration as a ‘shortfall year’ on or about 1 July but no later than October 1. The Minsters declaration of whether the forthcoming year is a shortfall year must then be made between 30 to 60 days after the declaration.

■ Mechanism will make it very difficult for customers to secure gas supply for greater than one-year calendar terms: clarity on the availability of gas supply for the next calendar year will not be known before the September prior, making it difficult for both intermediaries and suppliers to provide quotes prior to this. Let’s say you want to buy gas for 2019 and there is a shortage in 2019, a buyer finds that out now as it physically can’t source the gas. The required gas is however not physically going to be made available for sale (under the ADGSM) until September 2018. How can anyone sign a long-term contract under this environment?

■ Consideration of ‘past performance’ limits ability to curtail production in response to export restrictions: the draft allows for the minster to consider any projects past compliance with any conditions and any “gamin”: of the ADGSM. Seemingly this rules out curtailing production below forecast levels in response to export controls; as such any restriction to exports will result in the gas being diverted to domestic to market.

■ What does net-back actually mean? The shortage is to be assessed on the basis that the consumer pays no more than net-back pricing. It is unclear, if you believe in export price parity, what the reference point for net-back is. Is it Gladstone and then it is actually a net-plus price to deliver that gas to customers. Or a true net-back price. To put in context, the price differential for a Victorian customer between these two scenarios is a A$6–$7/GJ delta. Of course this can be solved with an import terminal… .Although, is this net-back price contract or spot? Again a $4–$6/GJ differential might exist

■ No clarity on price or physical obligation to actually sell the gas: Other than the above net-back price comment, which is seemingly just for assessing demand (and has wide interpretations anyway), there is no reference to a price mechanism for the ADGSM. There is also no clarity on what the obligations actually are for the volumes that are banned from export. Do they have to be sold, or just made available? One interpretation, when considering the reference to the “past performance clause” the gas just has to clear (i.e. forced seller). However, another interpretation is that you just have to make it clear at a net-back price and if it doesn’t clear then you can keep it in the ground.

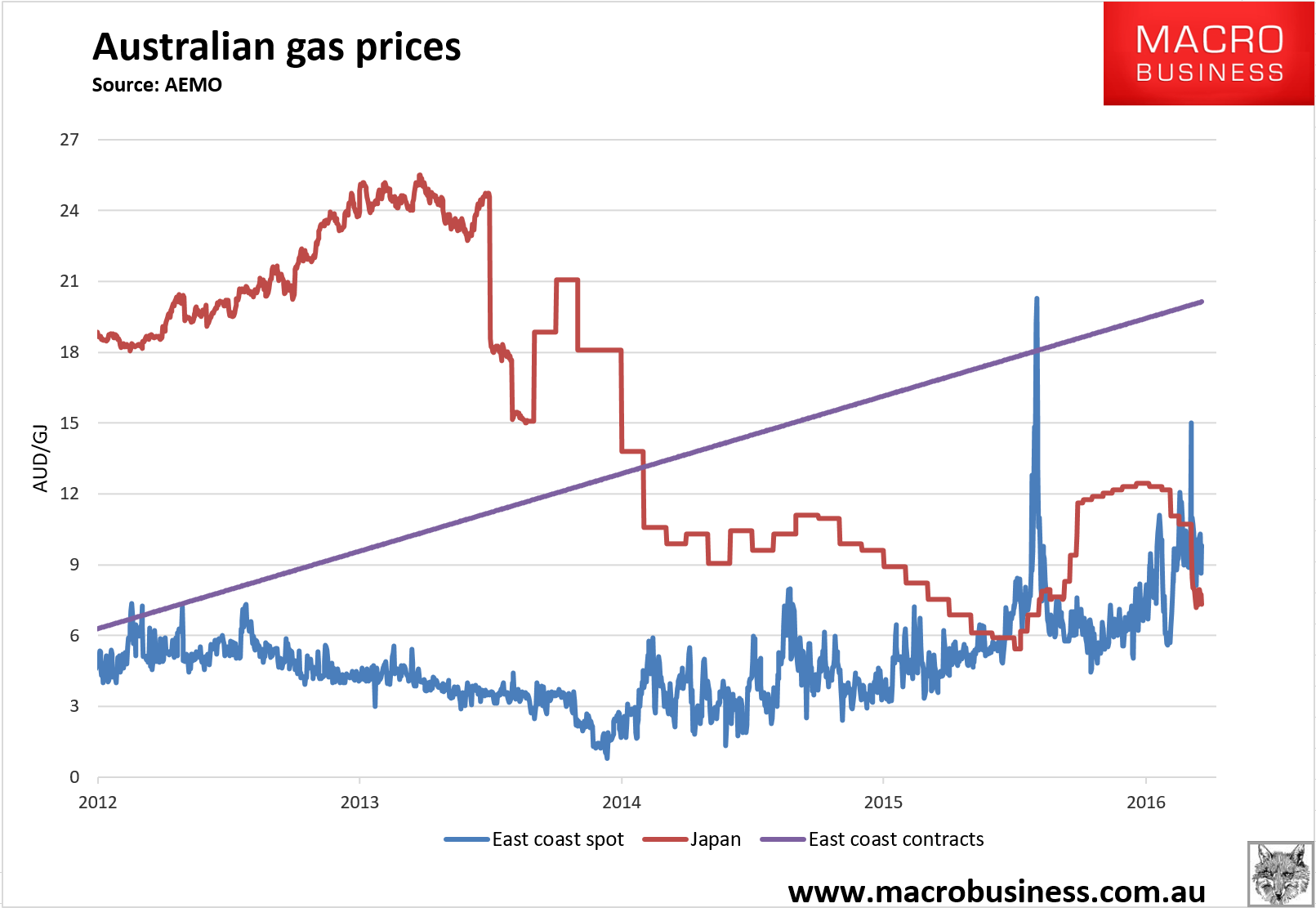

STO customer’s are not paying premium prices at all. They’re paying roughly $7.50Gj for spot LNG and $9Gj for oil-linked contracts. Anyone in Australia would die for those prices with spot at $9Gj and contract at $20Gj:

The ADGSM should be activated and target at least export net back on these prices meaning roughly $7.20Gj for spot and $7.80 for contracts.

Anyway, it appears rorting your country does not always pay as STO sinks through 40 year lows:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.