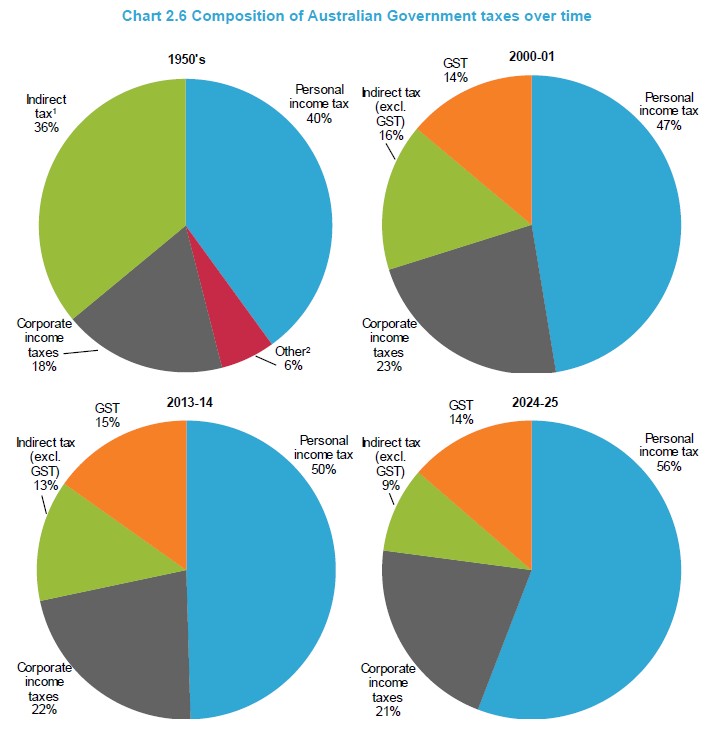

The Australian Treasury’s tax discussion paper, released in March 2015, forecast that Australia’s reliance on inefficient personal income taxes would rise inexorably over the next decade (to 56% of taxes by 2024-25), making reform an imperative as the population ages and the share of workers across the economy declines:

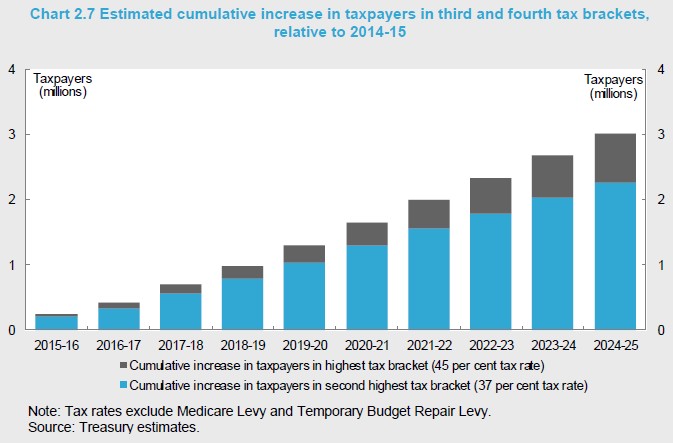

Between 2014-15 and 2024-25, the percentage of taxpayers in the top two tax brackets (that is, with taxable income in excess of $80,000) is estimated to increase from around 27 per cent to 43 per cent under current policy settings. It is estimated that over 2 million more taxpayers will be in the third income tax bracket (taxable income from $80,000 to $180,000) in 2024-25, compared to 2014-15. There is also estimated to be around 750,000 more taxpayers in the fourth tax bracket (taxable income above $180,000) in 2024-25 compared to 2014-15 (Chart 2.7).

Treasury also noted that this bracket creep is highly regressive and inefficient:

Advertisement

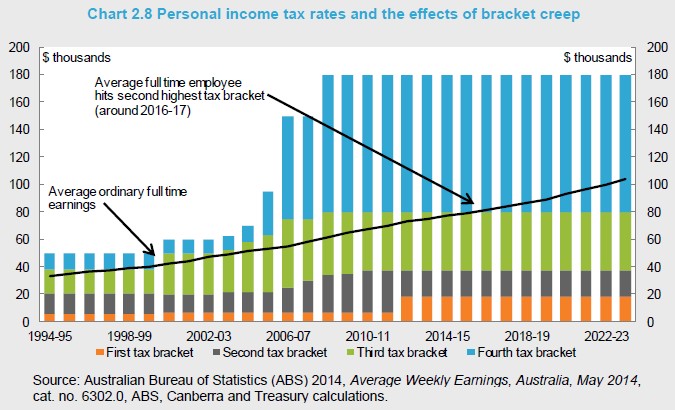

…average ordinary full-time earnings were around $75,000 in 2013-14, and are expected to be around $104,000 in 2023-24 (see Chart 2.8). Someone on average full-time earnings therefore had an average tax rate of 22.7 per cent in 2013-14, increasing to 27.4 per cent by 2023-24. By contrast, someone with only half that income earned $37,500 in 2013-14, increasing to $52,000 in 2023-24. However, their average tax rate will increase from 10.3 per cent to 17.8 per cent. Someone earning twice the average full-time wage is on $150,000, increasing to $208,000 in 2023-24, but their average tax rate will only increase from 30.5 per cent to 34.3 per cent.

For some people, particularly those on relatively low incomes, bracket creep can reduce incentives to work. At higher incomes, bracket creep increases the incentives for tax planning and structuring, and even overseas relocation. Bracket creep is therefore not just an issue because of its effect on progressivity, but because over time it exacerbates the other problems in the individuals income tax system.

Yesterday, Wayne Wanders from The Wealth Navigatorsent me through a Media Release showing that ordinary income earners have incurred (and are facing) the biggest increase in tax owing to bracket creep:

Mr Wanders said that bracket creep has meant that Australian taxpayers have paid billions of dollars in more tax than they realise.

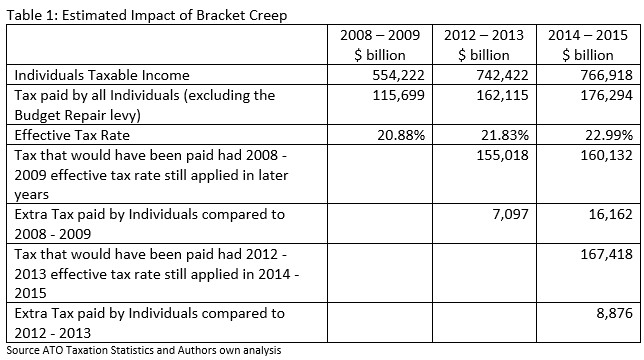

For example, using data recently released by the Australian Taxation Office, Mr Wanders estimates that because of bracket creep, in 2014 – 2015 Australian taxpayers paid:

An extra $16.2 billion dollars in tax than they paid in the 2008 – 2009 year.

An extra $8.9 billion dollars in tax than they paid in the 2012 – 2013 year.

“This is substantially more than the $8.0 billion dollars in extra tax revenue that the increase in the Medicare levy is budgeted to raise in its first two full years” said Mr Wanders.

“And what’s worse is that whist the largest share in dollar terms of the extra $8.0 billion in revenue from the Medicare levy increase will come from high income earners, the bulk of the extra revenue from bracket creep in dollar terms comes from low and middle income earners.”

Advertisement

As I have argued frequently, the most obvious path to fiscal repair is to first fundamentally reform Australia’s world-beating tax concessions (e.g. superannuation, negative gearing, the capital gains tax discount, and fringe benefits), which cost the Budget many billions of dollars in foregone revenue and are skewed towards the wealthy and higher income earners. Fundamental reform in these areas would dramatically improve the progressiveness of the tax system and would counter concerns that budgetary reform is unfair and is placing the burden of adjustment unfairly on lower income households.

Second, Australia must look to broaden the tax base so that it is built around more efficient and equitable sources. This requires a shift in sources from productive effort (e.g taxes on labour) towards taxes on land, resources, and consumption, along with adequate compensation for the poor (in the case of raising/broadening the GST). Under this approach, the overall tax take could be raised at less economic cost than via bracket creep. The tax burden would also be shared more evenly across the population, rather than relying on a diminishing pool of workers to shoulder the load.

Unfortunately, neither the Coalition nor Labor have offered comprehensive plans for tax reform, and have instead offered piecemeal measures – the Coalition by cutting company taxes and Labor on unwinding negative gearing and the CGT discount.

Advertisement

The end result is that instead of trying to broaden the tax base, both sides are doing the opposite by relying on never-ending increases in personal income tax via bracket creep, while the base of workers shrinks as the population ages and the proportion of retirees rises.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.