The Australian Treasury has today released its Tax White Paper discussion paper, which outlines its blueprint for tax reform and seeks community feedback.

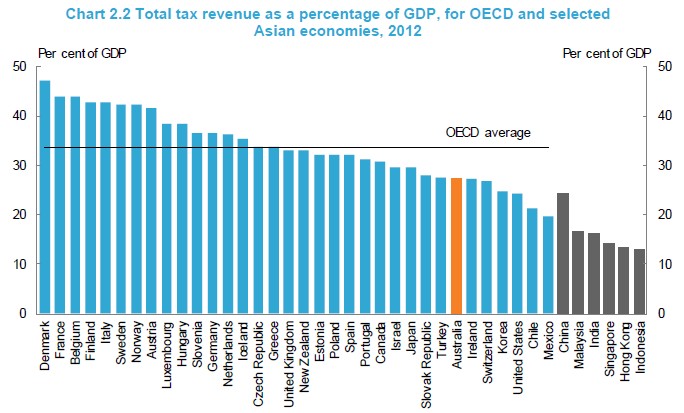

According to the discussion paper, Australia has one of the lower tax burdens in the OECD, at around 27.3% in 2012:

Advertisement

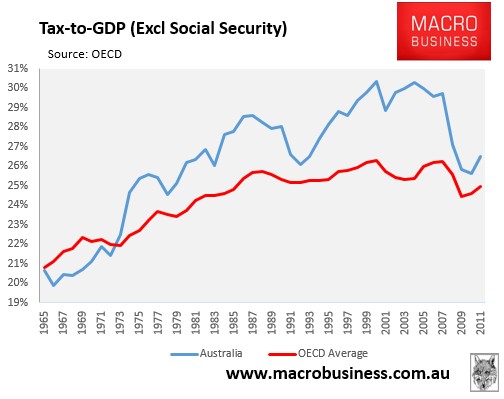

However, as noted previously, the figures are perhaps skewed by the fact that Australia does not include compulsory superannuation as a tax, whereas compulsory social security levies are included for other nations, which effectively act like superannuation. Thus, an apples-with-apples comparison, whereby compulsory social security levies are excluded, suggests Australia is actually a high taxing nation (see next chart).

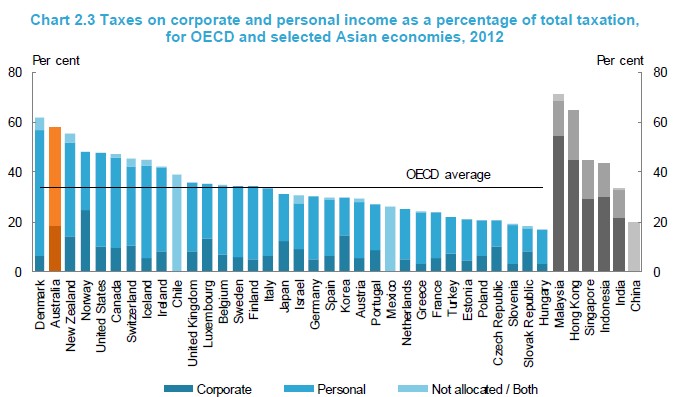

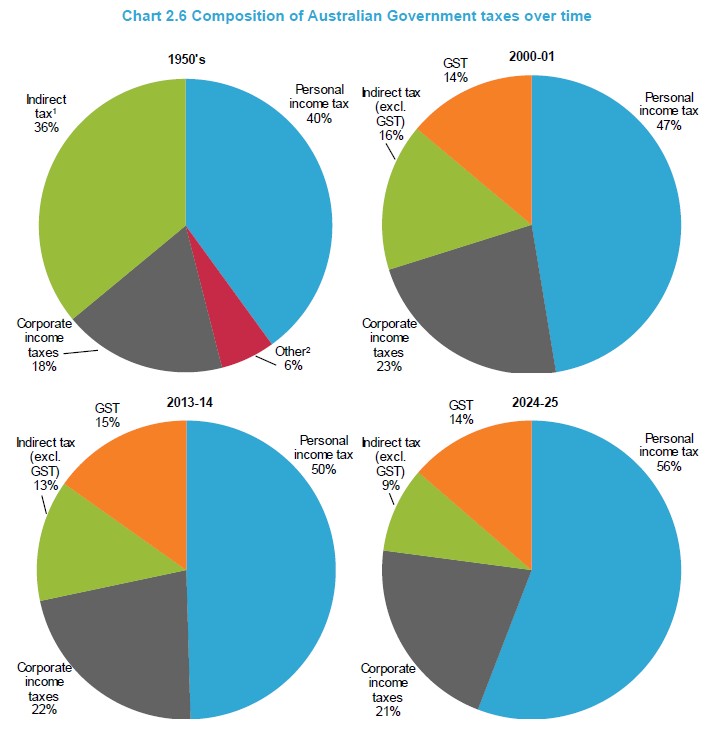

Regardless, the Treasury believes that Australia’s tax system has an over-reliance on taxes levied on productive effort – specifically personal labour and company profits – which is highly inefficient:

Advertisement

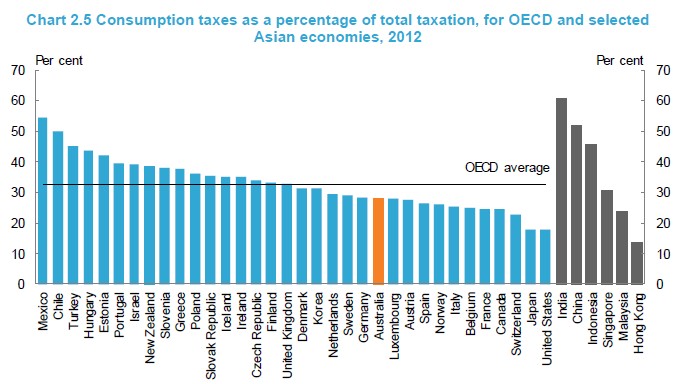

Meanwhile, Australia has an under-reliance on consumption taxes:

The reliance on personal income tax is also set to grow without reform, hitting a record high 56% by 2024-25 because of bracket creep:

Advertisement

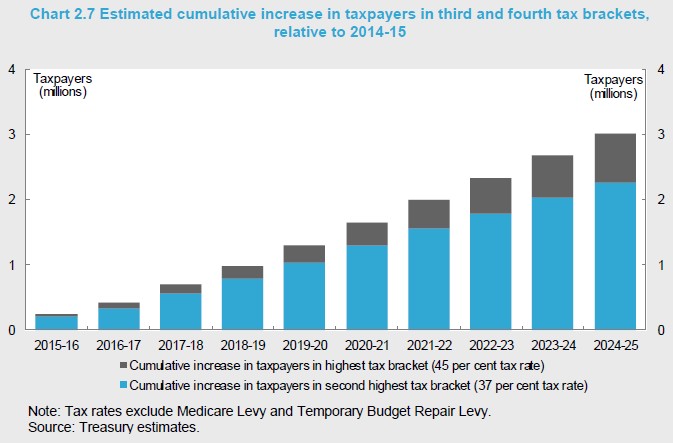

Between 2014-15 and 2024-25, the percentage of taxpayers in the top two tax brackets (that is, with taxable income in excess of $80,000) is estimated to increase from around 27 per cent to 43 per cent under current policy settings. It is estimated that over 2 million more taxpayers will be in the third income tax bracket (taxable income from $80,000 to $180,000) in 2024-25, compared to 2014-15. There is also estimated to be around 750,000 more taxpayers in the fourth tax bracket (taxable income above $180,000) in 2024-25 compared to 2014-15 (Chart 2.7).

Advertisement

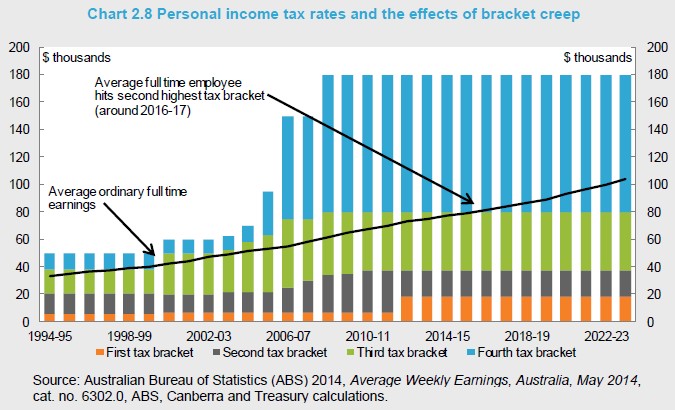

And this bracket creep is highly regressive and inefficient:

…average ordinary full-time earnings were around $75,000 in 2013-14, and are expected to be around $104,000 in 2023-24 (see Chart 2.8). Someone on average full-time earnings therefore had an average tax rate of 22.7 per cent in 2013-14, increasing to 27.4 per cent by 2023-24. By contrast, someone with only half that income earned $37,500 in 2013-14, increasing to $52,000 in 2023-24. However, their average tax rate will increase from 10.3 per cent to 17.8 per cent. Someone earning twice the average full-time wage is on $150,000, increasing to $208,000 in 2023-24, but their average tax rate will only increase from 30.5 per cent to 34.3 per cent.

For some people, particularly those on relatively low incomes, bracket creep can reduce incentives to work. At higher incomes, bracket creep increases the incentives for tax planning and structuring, and even overseas relocation. Bracket creep is therefore not just an issue because of its effect on progressivity, but because over time it exacerbates the other problems in the individuals income tax system.

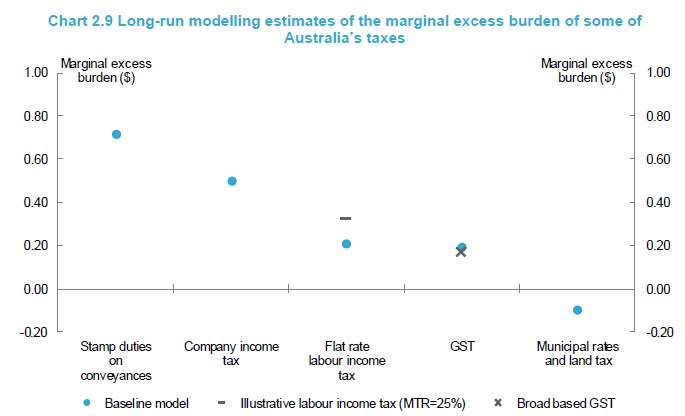

Australia’s heavy reliance on company taxes and stamp duties is also highly inefficient:

Advertisement

Company income tax has a high marginal excess burden because of the relatively high company tax rate of 30 per cent in Australia, combined with the high level of mobility of the underlying tax base. Conveyancing stamp duties also have a high excess burden because they discourage the exchange of residential and business properties.

And the incidence of high company taxes tends to fall on workers:

Advertisement

Recent research by the Treasury indicates that, in the long run, much of the burden or incidence of company tax falls on Australian workers. This is because, over time, the amount of capital investment in Australia (for example, the construction of buildings and purchase of equipment for production) is affected by the company tax rate. Lower amounts of capital investment in the Australian economy will reduce the output or productivity of labour and, in turn, reduce the real wages of workers.

Land taxes, by contrast, are among the most efficient tax of all:

Modelling also suggests that broad-based land taxes, such as municipal rates, have a low economic cost (Chart 2.9). This is because land is immobile (unlike other capital) and cannot be moved or varied to avoid tax. The model applies this assumption to both domestic and foreign ownership of land. Land taxes paid by foreign and domestic landowners are only redistributed to the domestic households, providing a benefit to Australian households and generating a negative marginal excess burden for a broad-based land tax shown in the chart.

Advertisement

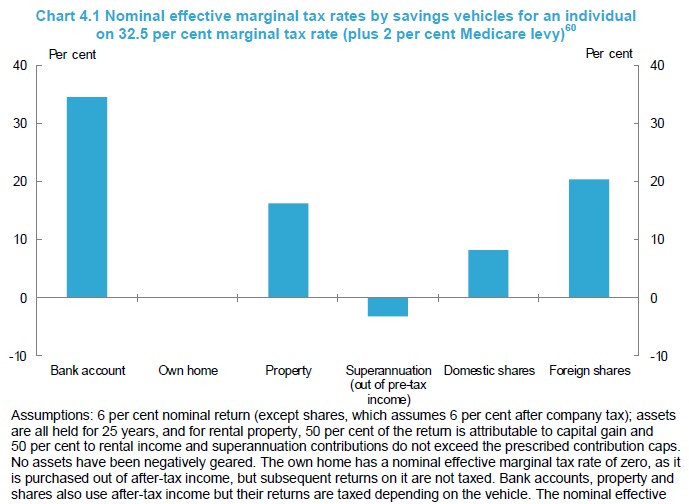

Meanwhile, taxes on deposits are inefficient and unfair:

Australia’s tax system treats alternative forms of saving differently. At one end of the spectrum, savings held in the family home are taxed at average effective tax rates approaching zero. At the other end of the spectrum, savings held as financial deposits are taxed at full marginal rates, without any recognition for the costs of inflation.

The policy rationale for these differences is not always clear and can distort taxpayers’ savings decisions. This has implications both for efficiently allocating savings in the economy and distributing risk across households…

Higher-income earners tend to be more capable of taking advantage of more favourable tax treatments (like superannuation), while those with the lowest ability to pay tend to save more in the more heavily taxed vehicles (such as bank accounts).

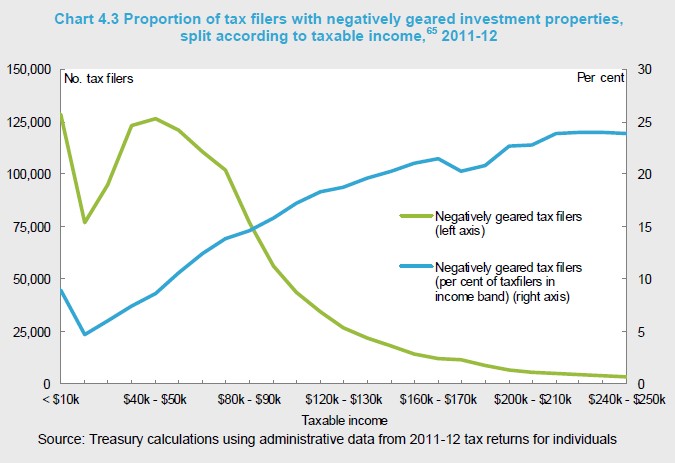

Treasury has also questioned the merits of the 50% capital gains tax (CGT) discount, which has made negative gearing profitable and help drive leveraged investment into housing, in particular:

Advertisement

Negative gearing does not, in itself, cause a tax distortion, but it does allow more people to enter the market than those who might have had the equity alone to do so. Purchasers can make bigger investments in property by borrowing, in addition to using their own savings. This behaviour is encouraged by the CGT discount, as larger investments can result ingreater capital gains and therefore benefit more from the CGT discount.

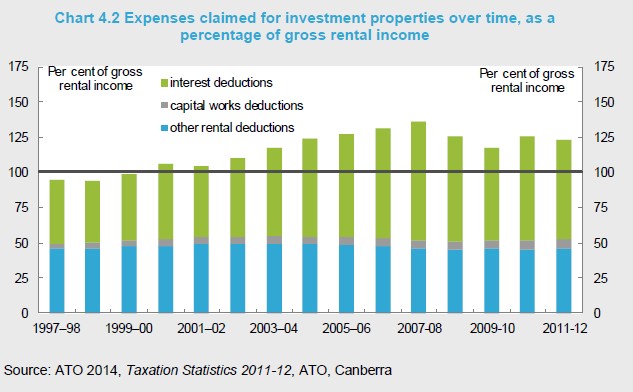

…investment properties constitute a substantial proportion of the total value of negatively geared assets. Chart 4.2 shows that deductions claimed for investment properties as a proportion of gross rental income have increased over the last 15 years and are nowgreater than gross rental income.

The potential tax advantage comes on the income side from the taxation of the capital gain earned from the asset. If the individual realises a capital gain when selling the property, only 50 per cent of this income is included in their taxable return.

The Treasury has also questioned the merits and sustainability of superannuation concessions:

Those with high incomes receive the greatest tax discount relative to their marginal tax rates, and will generally save a higher proportion of their income. As such they will receive the largest aggregate level of tax expenditure, measured against a benchmark of full nominal income taxation…

While there are policy grounds for superannuation being taxed at a lower rate than labour income, there are issues around the distribution of the impacts and their effectiveness in supporting higher retirement incomes, as well as their complexity…

The different rates of tax on earnings in the pre- and post-retirement phases add costs to the operation of the superannuation system. They also give rise to tax planning opportunities that are usually more accessible to high income earners. For example, it may be possible to delay realisation of a capital gain until the post-retirement phase so that no CGT is payable. Furthermore, it may also complicate the development of retirement income products.

With Australia’s ageing population, more individuals will enter the retirement phase where no tax is paid on earnings in superannuation funds. This will put pressure on the long-term sustainability of the superannuation tax arrangements, particularly given other long-term budgetary pressures as the population ages, such as calls for higher spending on health and aged care, and relatively lower revenue from personal income taxes…

Advertisement

Finally, the Treasury suggests that Australia’s dividend imputation system has past its used-by-date:

Australian investors therefore have an incentive to invest more of their savings in Australian shares rather than other investments (such as foreign companies). Further, because imputation does not offer relief from underlying foreign corporate taxes, it creates a bias against Australian-owned companies investing in foreign companies or engaging in foreign business activities…

These biases may be undesirable in an increasingly open and globalised world economy. The final report of the Australia’s Future Tax System Review in 2010 stated:

“… the benefits of dividend imputation have declined as the Australian economy has become more integrated into the global economy. In particular, benefits in relation to financing neutrality between debt and equity financing have fallen, while the bias for households to over-invest in certain domestic shares has increased”.

The imputation system has also increased the complexity of the tax system. Complex rules have been introduced to address integrity concerns arising from the imputation system. For example, specific rules address practices like franking credit trading, which involves franking credits being transferred to other entities that have not borne the economic risk associated with those credits, and dividend streaming, which involves franking credits being distributed to only the shareholders that value them…

The imputation system reduces the cost of investing in Australian companies for Australian residents. However, it provides little benefit for non-resident shareholders in Australian companies, other than exempting the dividend from dividend withholding tax, because Australian imputation credits do not reduce their tax liability in their home country.

At over 200 pages, the Treasury discussion paper includes much more, and I have only captured the key points. Nevertheless, its overall theme is that the current tax mix is becoming increasingly unsustainable and inequitable, and reform is required to broaden the tax base, shift the burden away from productive effort (principally labour and capital) towards more efficient and equitable sources (e.g. consumption and land), whilst closing some tax expenditures (e.g. superannuation and the CGT discount).

Advertisement

Hopefully, the paper will generate some much needed discussion and ultimately reform

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.