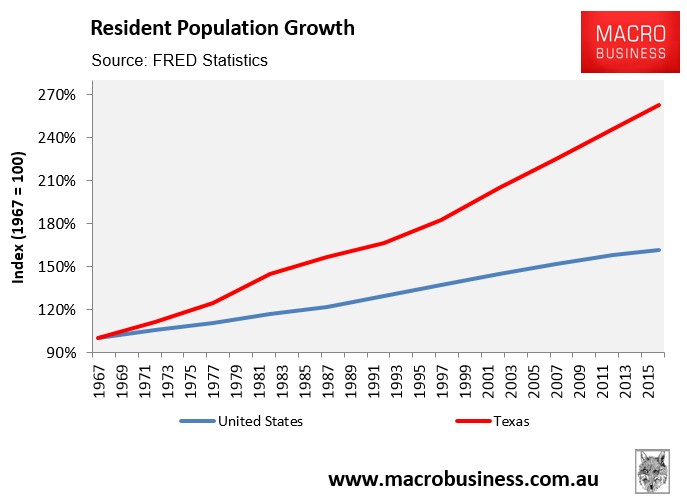

For years I have argued that Australia should look to Texas to solve Australian housing supply.

This view was based primarily on the fact that Texas has been able to achieve stable and affordable housing in the face of extreme population growth (see next chart).

In his latest Global Housing Watch newsletter, Hites Ahir has published an interesting interview with Joseph Gyourko – a Professor of Real Estate, Finance and Business Economics, & Public Policy at The Wharton School – who discusses how regulations and zoning affects housing supply and affordability.

Below are some key extracts:

Joseph Gyourko: Strong demand itself is not enough. Dallas has very strong demand, as population has grown substantially over many decades; yet, its constant quality house prices have not risen much at all in real terms. What is different about Dallas is plentiful building whenever prices rise enough for developers to supply new homes and make a normal profit… Note that higher demand is essential, not just regulatory constraints on new supply. A market could dramatically limit the ability of builders to build, and it would not matter for price unless demand were strong enough to bid up house values.

…markets with more elastic supplies should have fewer and shorter bubbles than markets with inelastic supply sides… it is the interaction of strong demand with inelastic supply that leads to high prices and affordability problems. Supply restrictions themselves lose their policy relevance in the face of weak demand…

What we do know is that prior to 1970, differences in local regulation and in house prices themselves, were not nearly as wide as they are today. Something changed in the 1970s, with California coastal cities initially imposing binding constraints on new residential development. Other cities on both coasts followed over the next decade…

Hites Ahir: Is there a city or a country that gets zoning and regulations right?

Joseph Gyourko: Yes, most American housing markets, especially those not located along our east and west coasts get it right. In forthcoming work, Ed Glaeser and I conclude that most housing markets in the interior of the country function so that the price of housing is no more than the sum of its true production costs (the free market price of land plus the cost of putting up the structure) plus a normal entrepreneurial profit for the homebuilder. That is what we teach should happen in our introductory microeconomics courses—namely, that price paid by consumers in the market should equal the real resource cost of producing the good (housing in this case). These well-functioning housing markets exist in a broad swath of the country outside of the Amtrak Corridor in the Northeast (Washington, D.C. to Boston) and the major West Coast markets from Seattle all the way down to San Diego. The bulk of the population lives in these well-functioning markets, by the way. They just are not focused on by the media…

The simple answer is to undo the regulations that are inefficiently constraining new housing unit production. Unfortunately, that does not happen. One reason is that political support for limitations on new housing supply is strong once the restrictions are in place. The Washington, DC, market in which you live tends to be fairly restrictive. Ask your colleagues who own homes if they would vote for politicians who eliminated restrictions that resulted in a substantial increase in housing production that, in turn, lowered the value of their own homes at the same time. And, that is what substantial new supply would do (all else constant)—lead to a fall in house values…

Hites Ahir: “Economic Implications of Housing Supply”—is your new paper with Edward Glaeser. The paper says: “The older, richer buyers in America’s most regulated areas have experienced significant increases in housing equity. The rest of America has experienced little growth in housing wealth over the past 30 years.” Can you talk about that a little?

Joseph Gyourko: Sure. The point we are making is straight out of an intermediate microeconomics class. The answer to the question of who benefits from higher prices that result from binding restrictions on the supply of new housing is the owners at the time the restrictions were imposed. Restrictions began to be imposed in many west coast markets in the 1970s, with east coast markets in the northeast following the next decade. Thus, it is the people who owned in those markets at those times who enjoyed the most appreciation in their homes. Those people tend to be senior citizens today, and even if they do not earn relatively high incomes, they are wealthy because of the real capital gains on their homes…

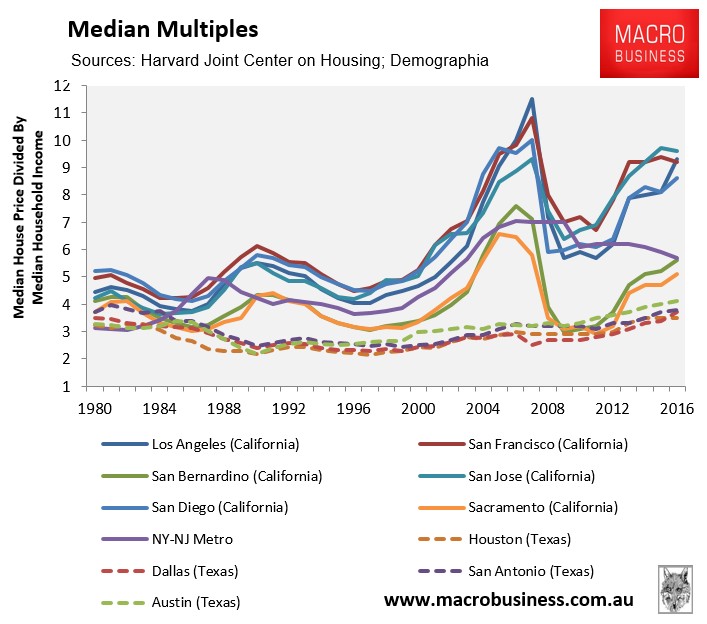

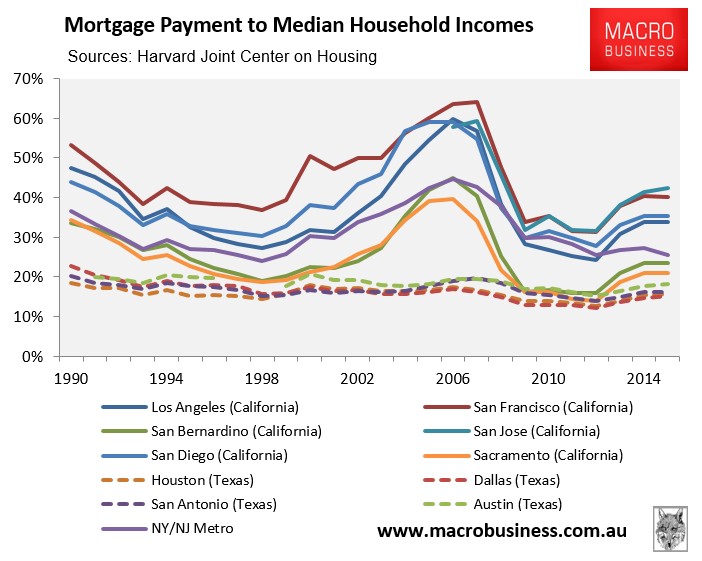

A comparison of Texas’ housing affordability (where land supply is considered very elastic) and California’s (where land supply is considered very inelastic) highlights the issues discussed above.

As you can see, Texas’ big metros remain highly affordable (and less price volatile) against California’s, which has in turn driven strong internal migration to Texas:

The above discussion highlights why reforms need to be made on both the demand and supply sides of the housing market.

Demand-side reforms can be implemented relatively quickly by the federal government (e.g. tax reform, cutting immigration, and clamping down on foreign investment), whereas supply-side reforms are the primary responsibility of the states and require a much longer time frame.

unconventionaleconomist@hotmail.com