DXY was hammered in the past few days:

It was largely a move in the euro post French election that did it.

Commodity currencies are firm:

Gold weak:

Base metals firm:

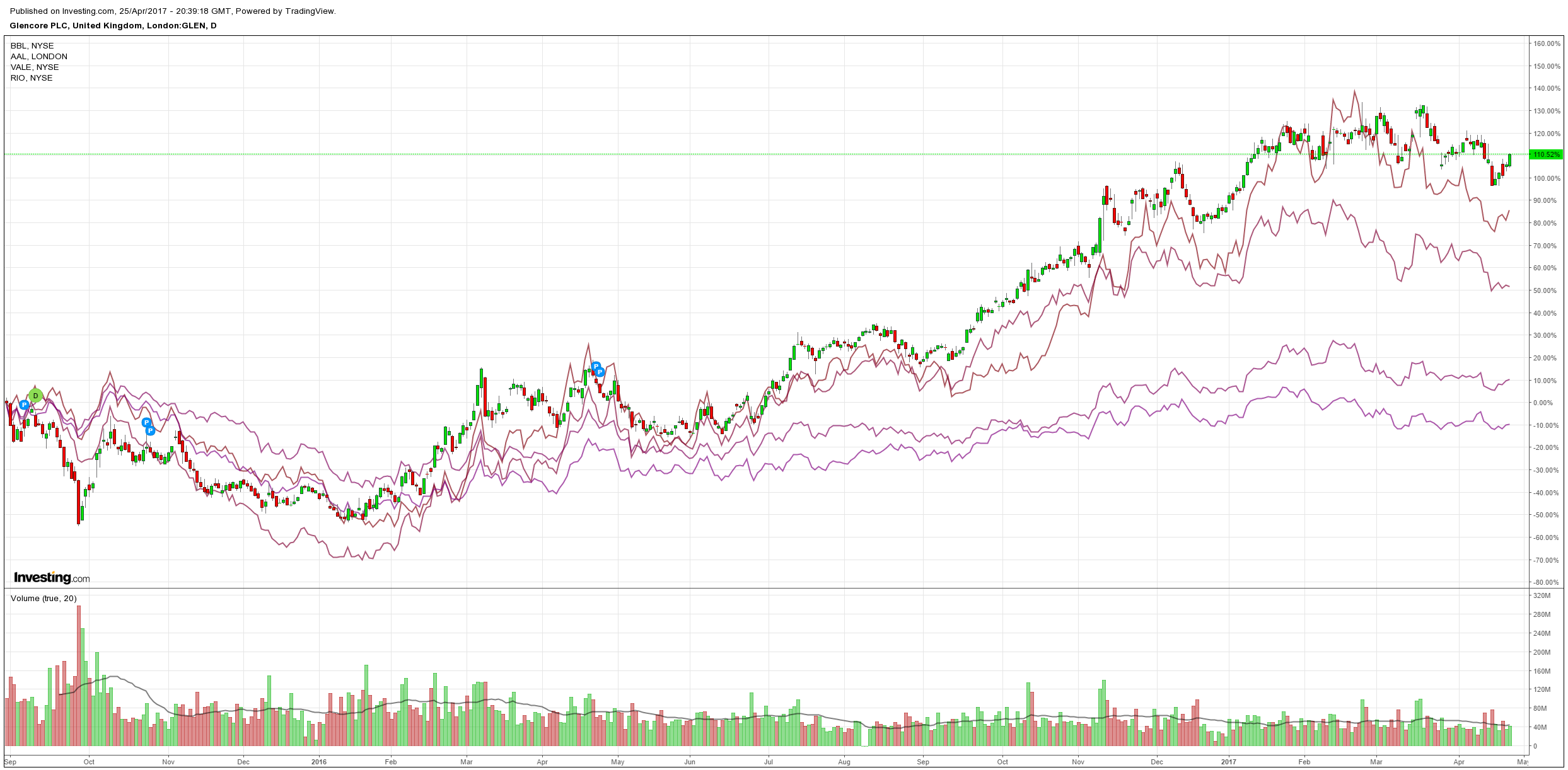

Big miners too:

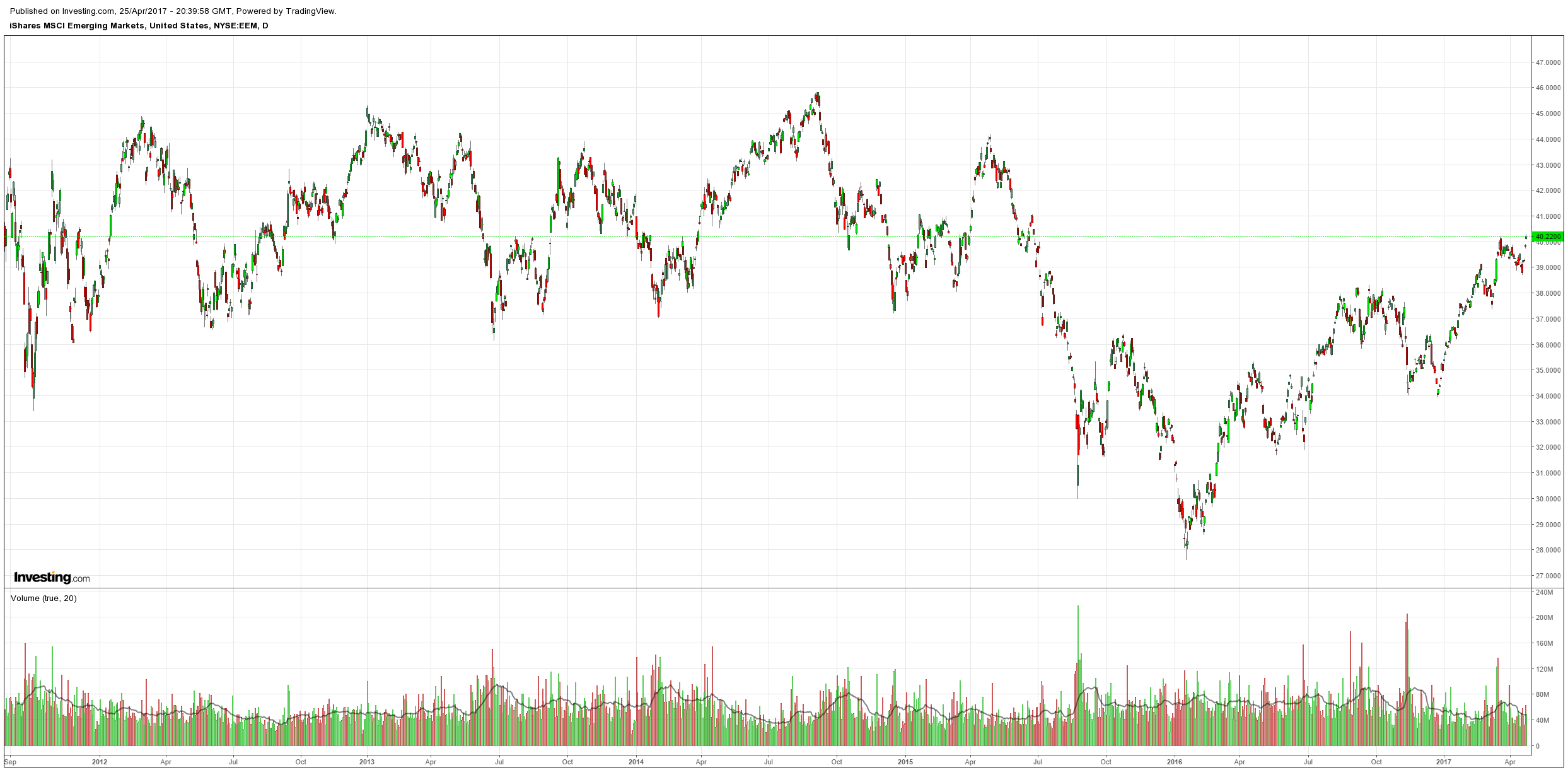

EM stocks launched:

High yield too:

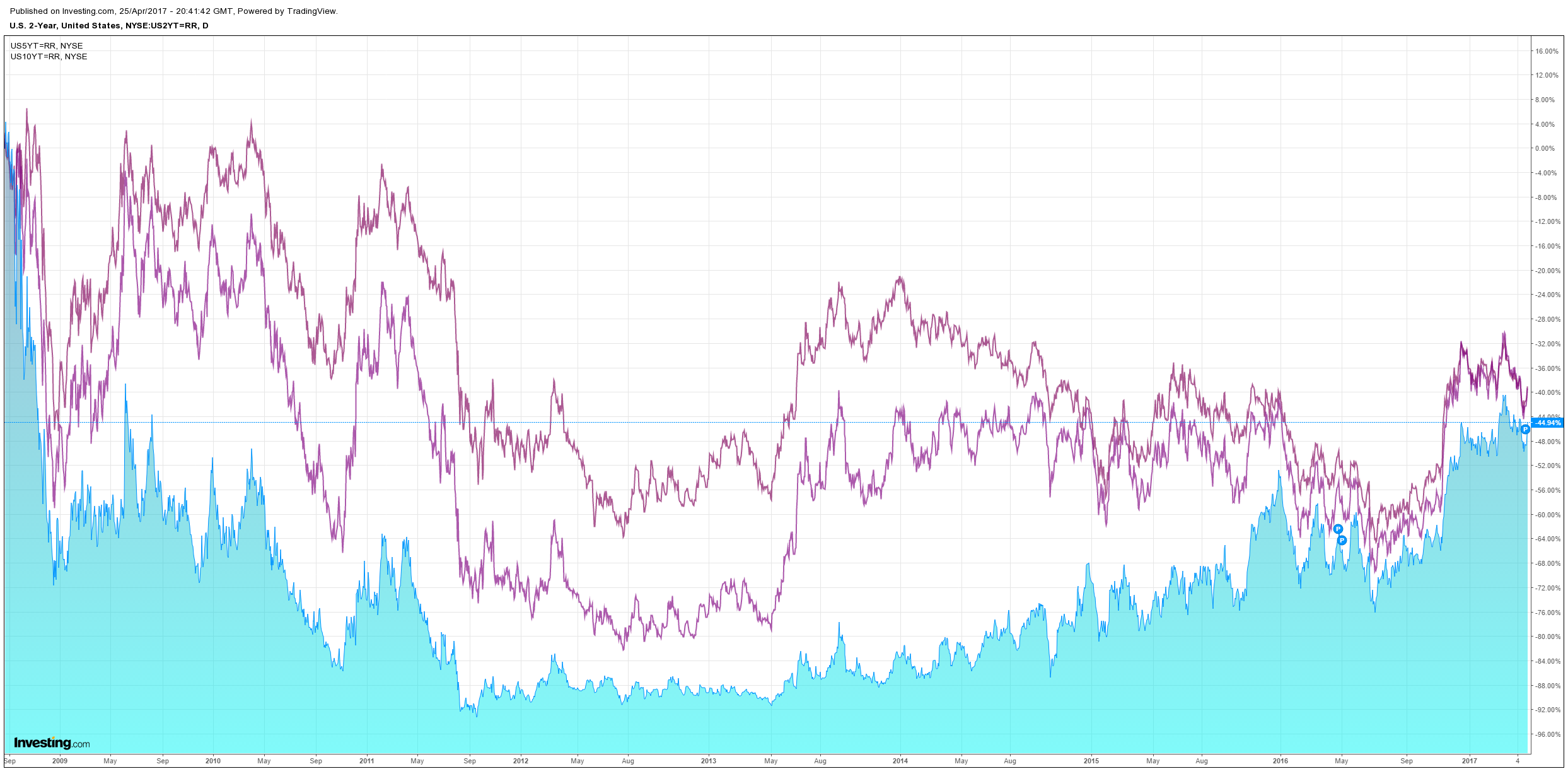

US bonds were bashed:

European spreads crashed:

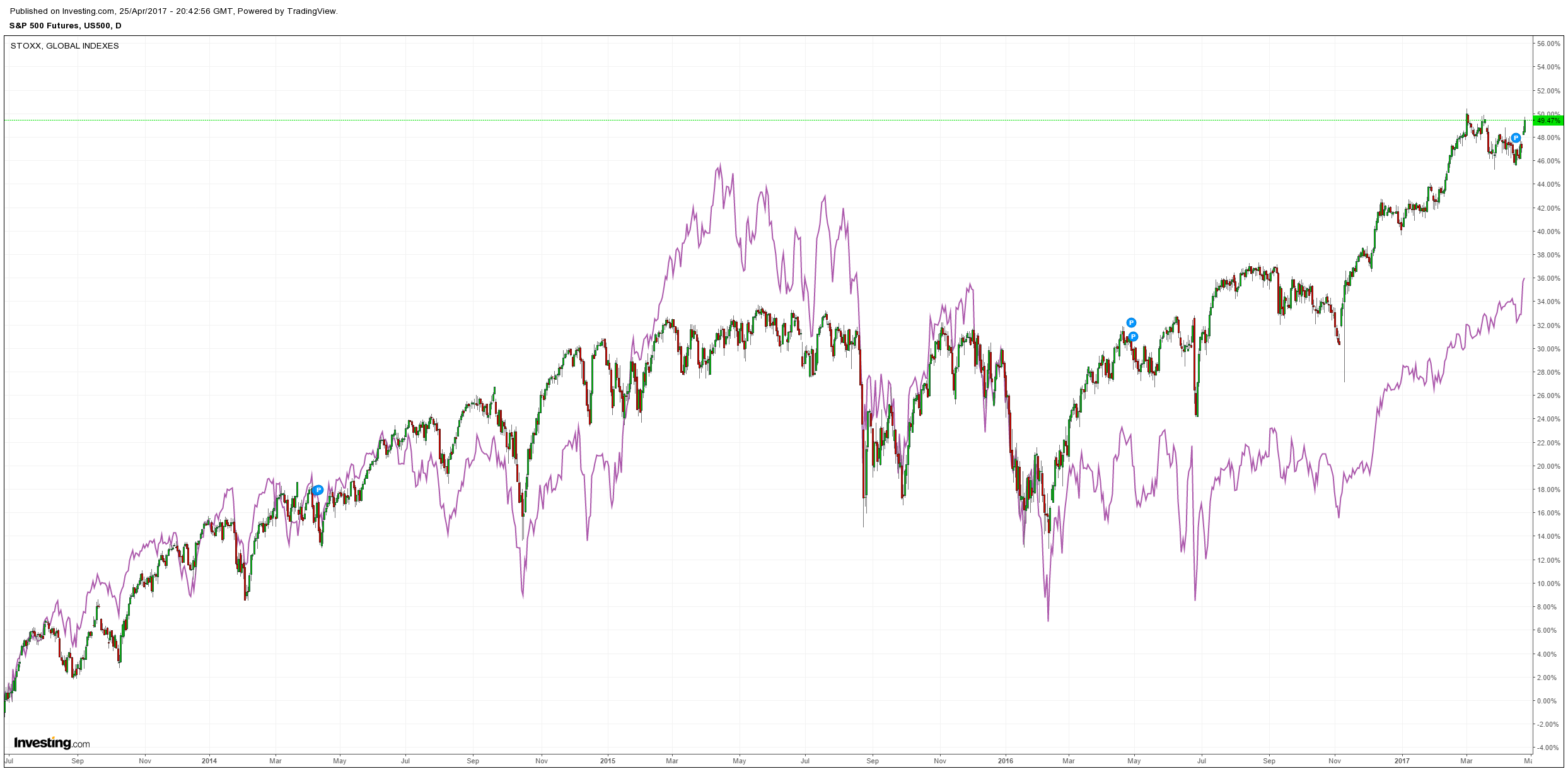

European stocks rocketed, US too but not as much:

The great European rotation is on as euro risk ebbs for now. It was benefited by two news points overnight. First, the Trump tax plan is unconvincing, via FT:

In seeking to scythe the corporate tax rate to 15 per cent Donald Trump can claim to be pursuing longstanding campaign pledges to make the US more competitive and revive economic growth.

But whether the president’s expected tax-cutting demand will bolster the chances of reform actually happening this year in Congress is a very different question. Attempting such a steep cut in the key rate would raise a host of procedural questions within Congress if the headline-grabbing reduction is not offset with revenue-raising measures elsewhere. It would also sound alarm bells among deficit hawks in the GOP given the US is facing a renewed ballooning of its budget deficit.

The tax reform process is already bogged down following the legislative chaos surrounding attempts to repeal and replace Obamacare last month. Wrangling within the party over the border-adjusted tax — a key component of House Speaker Paul Ryan’s tax plan that has to date failed to win White House backing — has further complicated the process.

GOP lawmakers have been demanding presidential leadership on tax reform as they seek to regain momentum, and Mr Trump has said he will wade into the debate as soon as Wednesday. But some congressional aides and tax lobbyists worry that the president’s ideas will end up further muddying the waters.

A cut in the US corporate tax rate from 35 per cent to 15 per cent would cost $2.2tn in lost revenue over 10 years, according to Alan Cole of the Tax Foundation think-tank. Rather than paying for this by broadening the tax base, the Trump administration has suggested it thinks tax cuts can pay for themselves by generating higher growth.

The biggest disappointment is that they seem to be sacrificing tax base reform for a simple rate cut Aide to Utah Senator Mike Lee Mr Cole says the US would need to see a sustained 0.9 percentage point increase in its growth rate over 10 years to make up for this kind of revenue loss. That does not look realistic to him: he would expect an uplift of less than half that size. The upshot would be an increase in the budget deficit that worries fiscal conservatives in the GOP who are already fretting at the scale of America’s borrowings.

That’s ludicrous. It will be a one-off growth lift not ongoing. It will also be pray to reversal the moment the Dems regain power, just as G.W. Bush cuts were. Markets rallied but this kind of deficit blowout is not going to get the Freedom Caucus over the line in my view. It looks more like a Hail Mary pass.

Second, Reuters reported that the ECB is ready to signal a little tightening:

Three sources on and close to the bank’s Governing Council told Reuters that with the threat of a run-off between two eurosceptic candidates in France averted, and with the economy on its best run in years, there may be tweaks to the ECB’s opening statement in June.

So, the great rotation to Europe identified by MB some months ago is, for now, the trade de jour. It has one other great advantage. If the Germans turn from Merkel to Schultz later this year – and polls are neck and neck – then Germany will have a eurobonds fiscal hand-off in prospect as well.

For now, we’re going to stick with US leadership in the cycle. It is far ahead of Europe in its business cycle and Trump still only needs to succeed moderately with tax cuts to lift inflation and tightening expectations materially. But Europe is off the bottom and running now so we’re going longer there as well. Since we allocated our first tranche, the euro has already handed the MB Fund a 4% forex dividend and there’s more to come I suggest:

We still expect that the better things get in developed markets, the worse they’ll get in emerging given it gives China a free hand to address its imbalances.

Allocations today are:

- buy the dips in the S&P500 and USD (waiting for a decent pullback);

- buy the dips in selected European stocks;

- sell rallies in commodities and AUD;

- buy the dips in Aussie bonds (creeping out the curve now);

- buy the dips in gold miners;

- sell property!