Via the AFR:

Australia’s most successful and well-known stock pickers are under pressure as active managers fail to perform and investors opt for the safety and certainty of passively managed index funds.

More than three-quarters of active large cap equity funds in Australia underperformed the indices they are measured against in calendar 2016, according to S&P Dow Jones Indices.

…Among those to feel the heat now are the very same names that used to populate the top of the fund management leaderboards including former Macquarie Bank chief investment officer Greg Matthews.

…The last monthly update put out by the firm shows that the fund was up 8.4 per cent over the year but underwater over three years, five years, seven years and since inception.

It also shows that nine of the fund’s top 10 positions were large cap resource stocks and that funds under management had declined to $450 million. The fund charged a management fee of 99 basis points and a performance fee of 23.83 per cent on returns above the benchmark.

…Hyperion’s Australian Growth Companies Fund is another example of a strategy that has suffered in the current environment.

With large holdings of once-hot growth stocks such as Dominos and REA Group it delivered investors annual returns as high as 39 per cent in 2013 and topped the Mercer tables for one and five-year returns during the same year.

Following the election of US President Donald Trump the environment has proved challenging for growth stock acolytes as investors have gave the sector a wide berth in exchange for financials and other cyclicals.

…Another stock picker to suffer from the swings and roundabouts in cycles is high-profile stockbroker turned fund manager Marcus Padley. Mr Padley is the author of the popular Marcus Today sharemarket newsletter and a frequent commentator.

In September of 2016 Mr Padley announced plans to disrupt the funds management industry and launched a pair of separately managed account strategies – one aimed at long-term growth and the other at income.

While the income fund has performed strongly, delivering a return of 6.2 per cent since inception, compared with the losses of 1.6 per cent from the benchmark ASX 200 Accumulation Index, the growth fund has proved more troublesome.

Since inception in March 2016, the fund has lost 6.1 per cent compared with the benchmark ASX 300 Accumulation Index return of 20.1 per cent leading to an underperformance of 26.2 per cent to March 30.

Mr Padley said that the fund – which started out with a mid cap focus – has been forced to change its strategy to move up the market capitalisation curve.

Cut my legs off and call me shorty. Is it any wonder these guys are failing? Long Australia. Long mining. Long uber-concentrated growth stocks. Long capitalisation for growth. Long huge fee structures!

None of it makes any sense from a top-down perspective. Indeed, all of it looks like the perfect recipe to lose money, which it is!

The fundamental problem with these dills is that they are a school of very fat goldfish trapped in a very small and shrinking bowl. Trying to pick winning stocks within an environment of shrinking profits is impossible. And that’s Australia where the economy is busted.

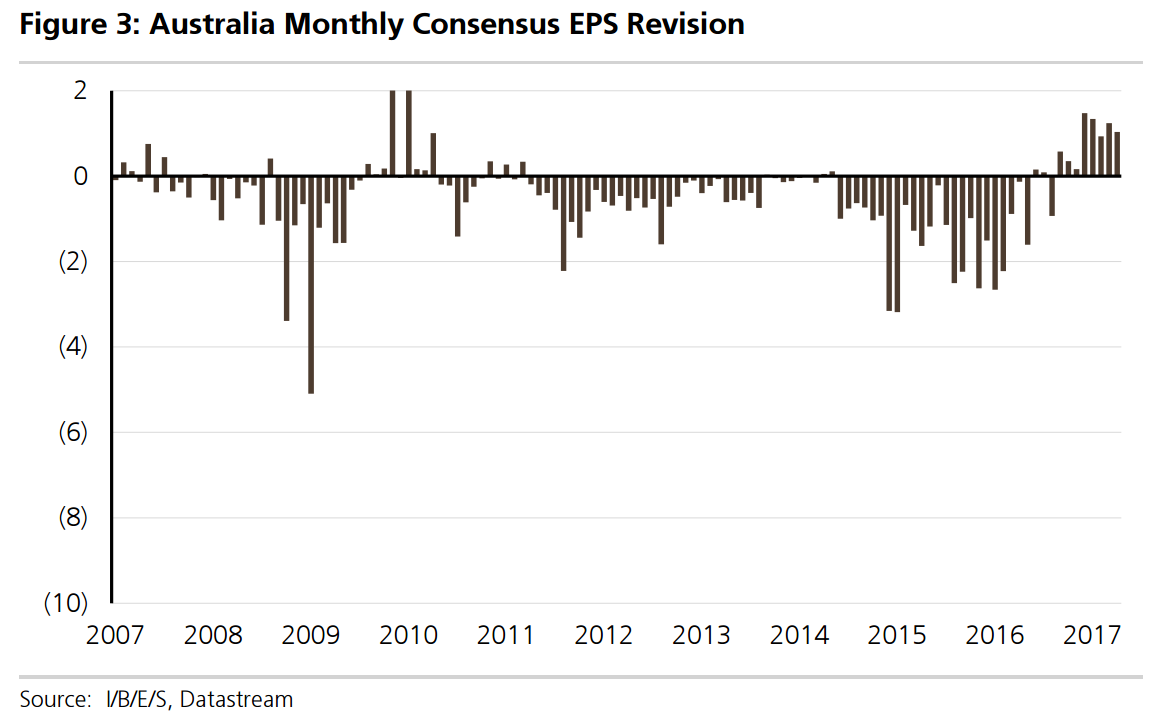

As UBS recently noted, the post-GFC history of EPS revisions is appalling:

The recent rebound was all mining driven and is now reversing:

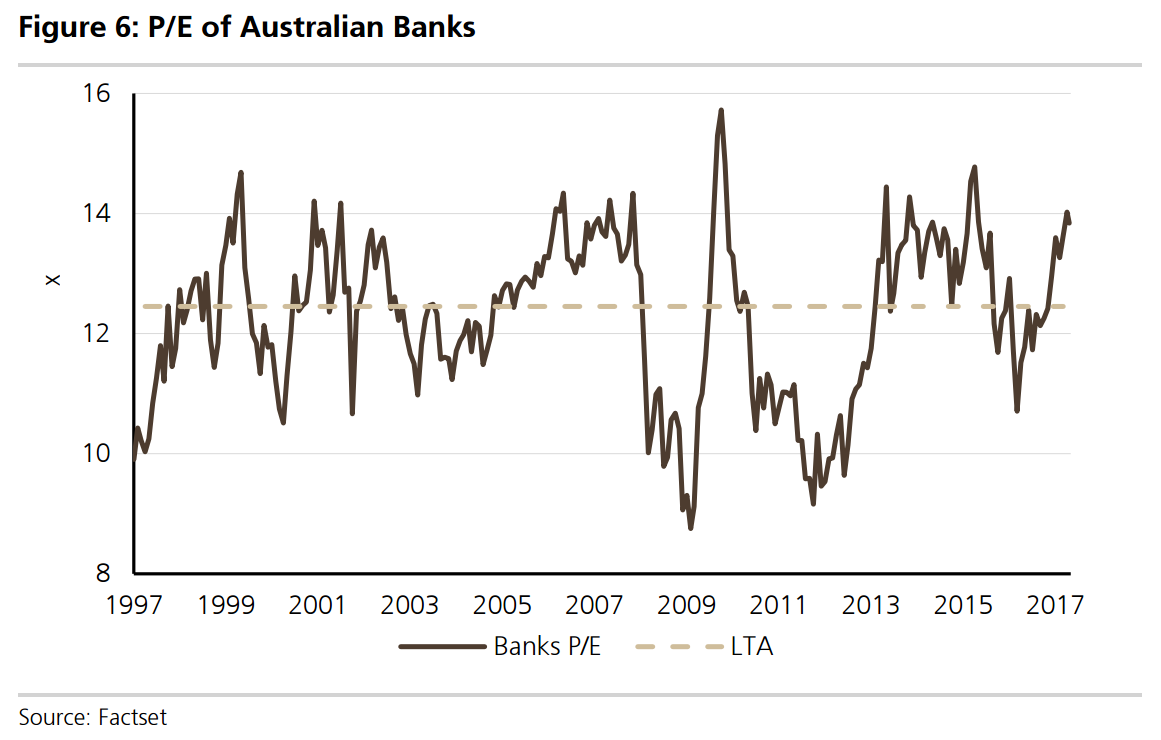

Banks are expensive:

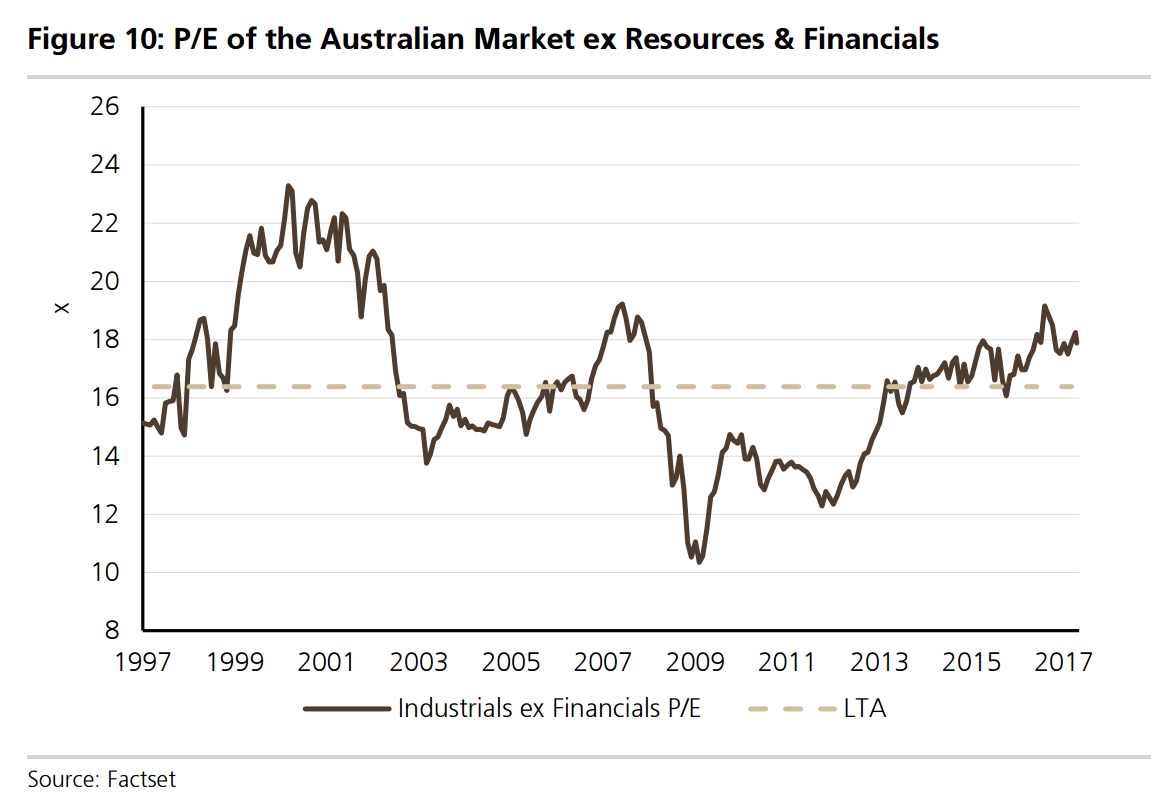

Industrials are expensive:

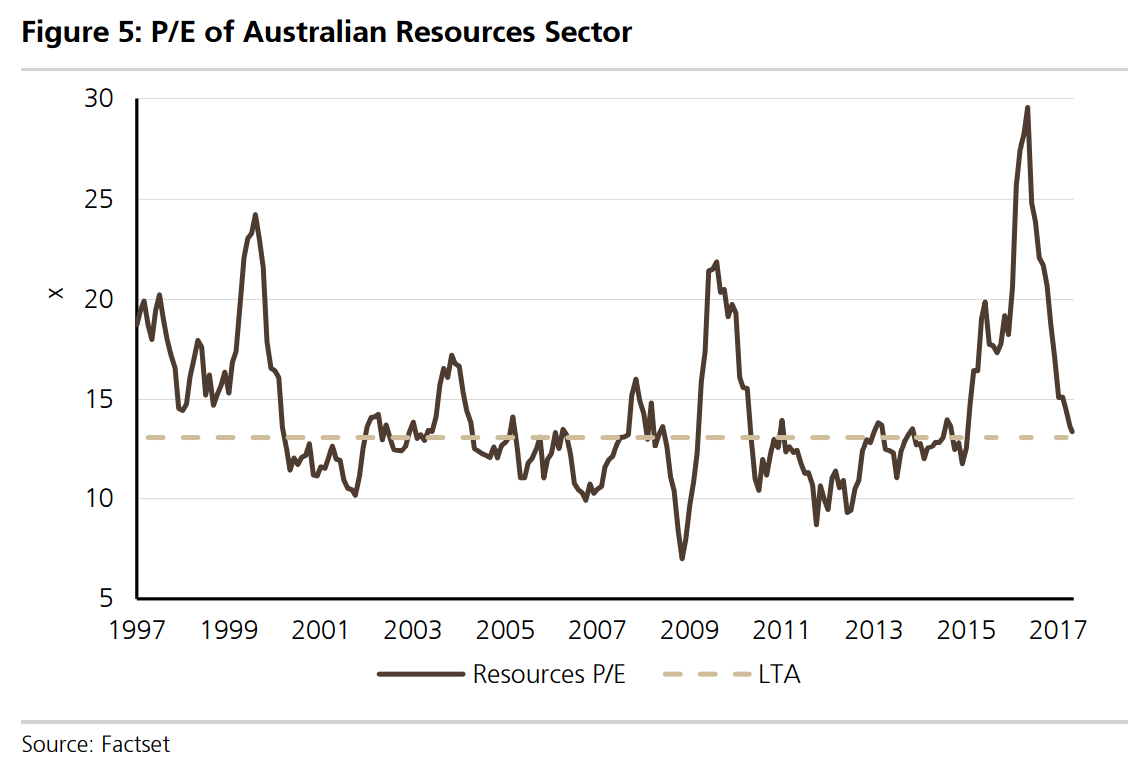

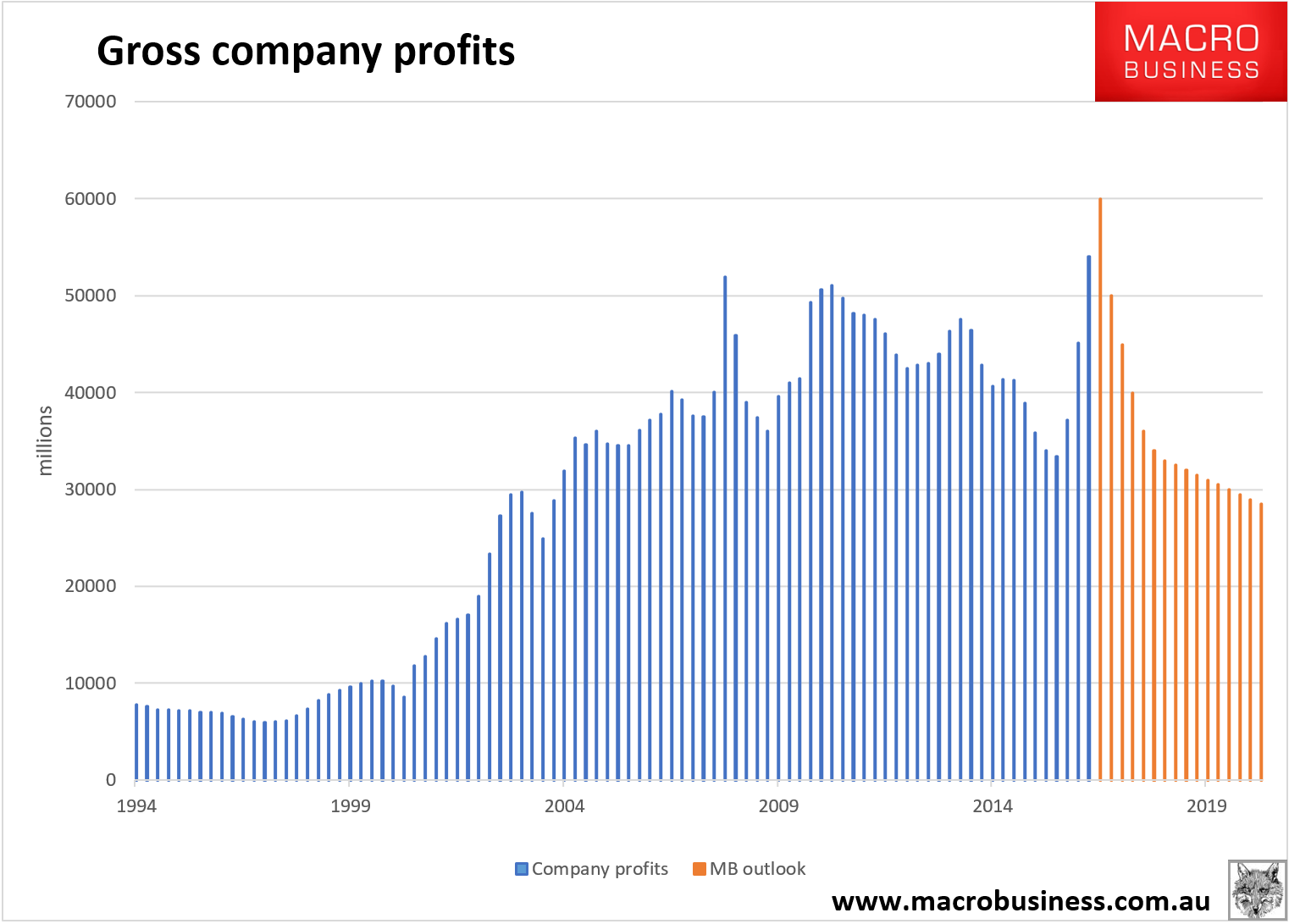

And mining is about to suck all of that recent good fortune straight back out again as coking coal and iron ore revert to mean (in my view in the $30s for the former by late year and $100 for the latter). That will do this to corporate profits from 2018-2020:

Meaning Australian under-performance versus the globe will worsen:

Local fundies are failing because the economy is failing and its great adjustment has barely even started with household debt peaking at records and the dirt income tide still going out.

The top-down view of Australian funds is very clear: invest somewhere else where there is actual growth and not in some school of overfed goldfish gulping at shrinking levels of oxygen.

We can help you do that with the MB Fund which is 70% allocated to international equities. It launches next month so register your interest today (if you have not already):