DXY was flat Friday night:

Commodity currencies were mostly up, not Aussie:

Gold tried but failed to rally:

Brent was up a little:

Base metals fell:

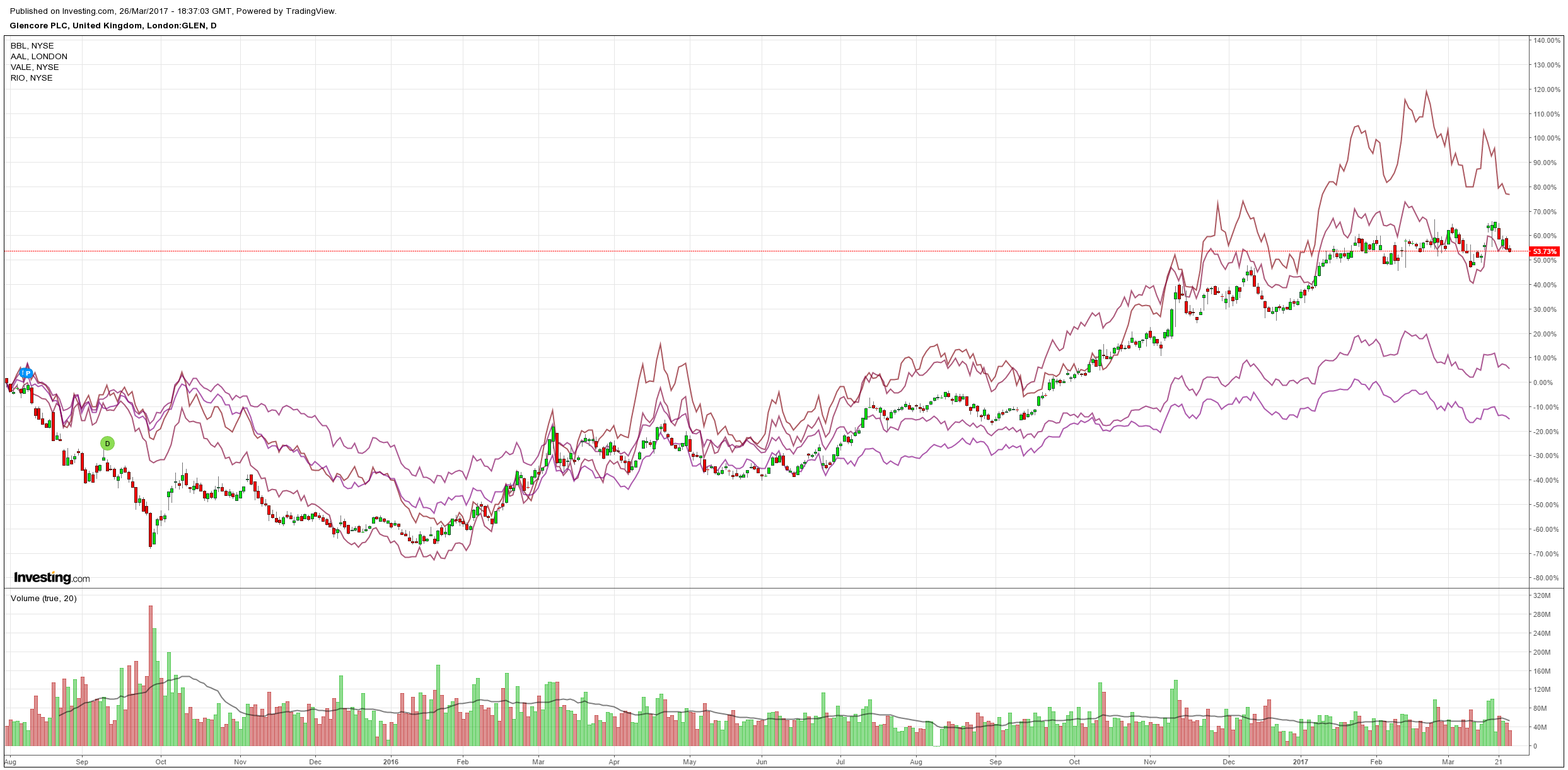

Big miners too:

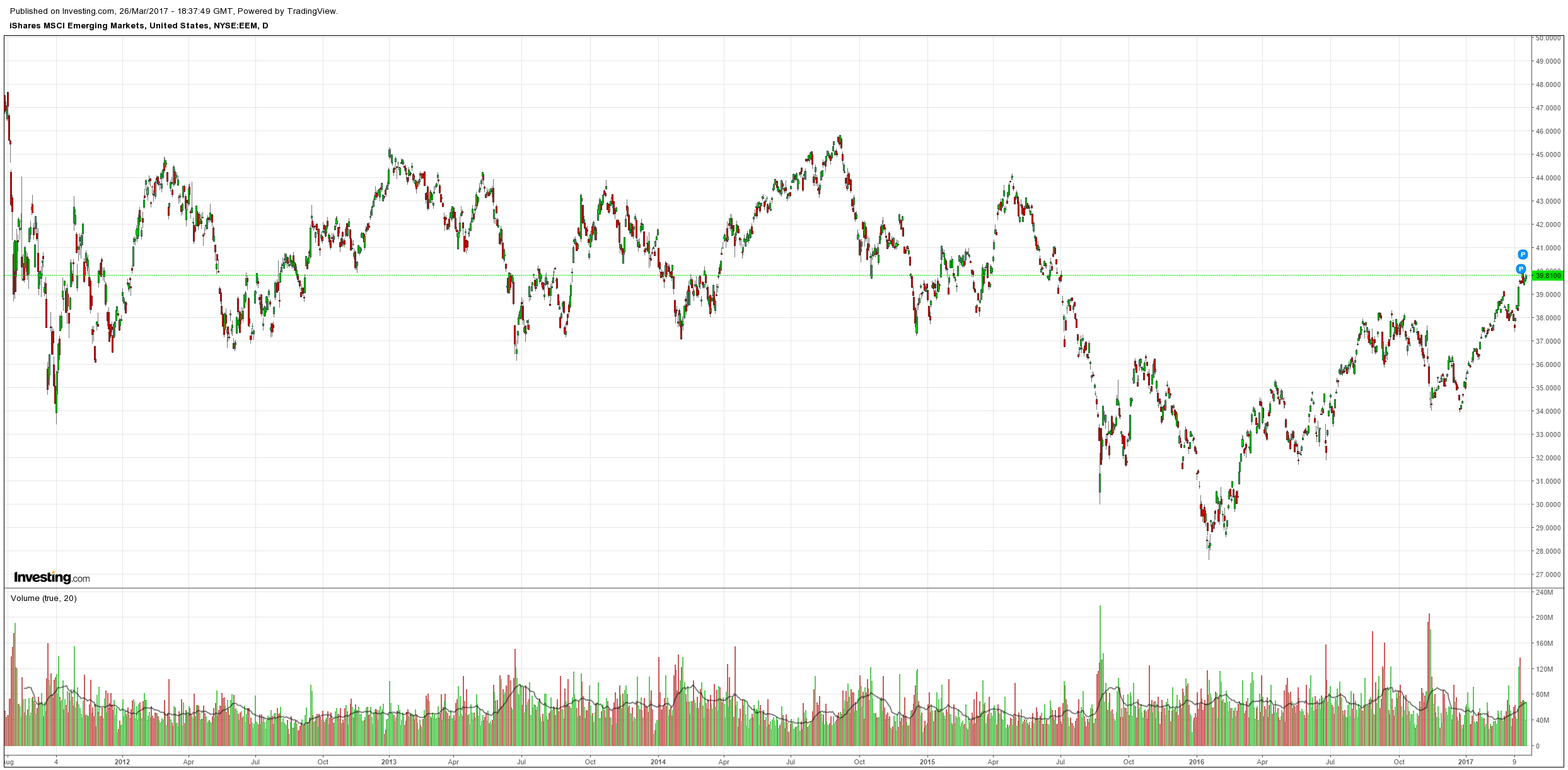

EM stocks bounced:

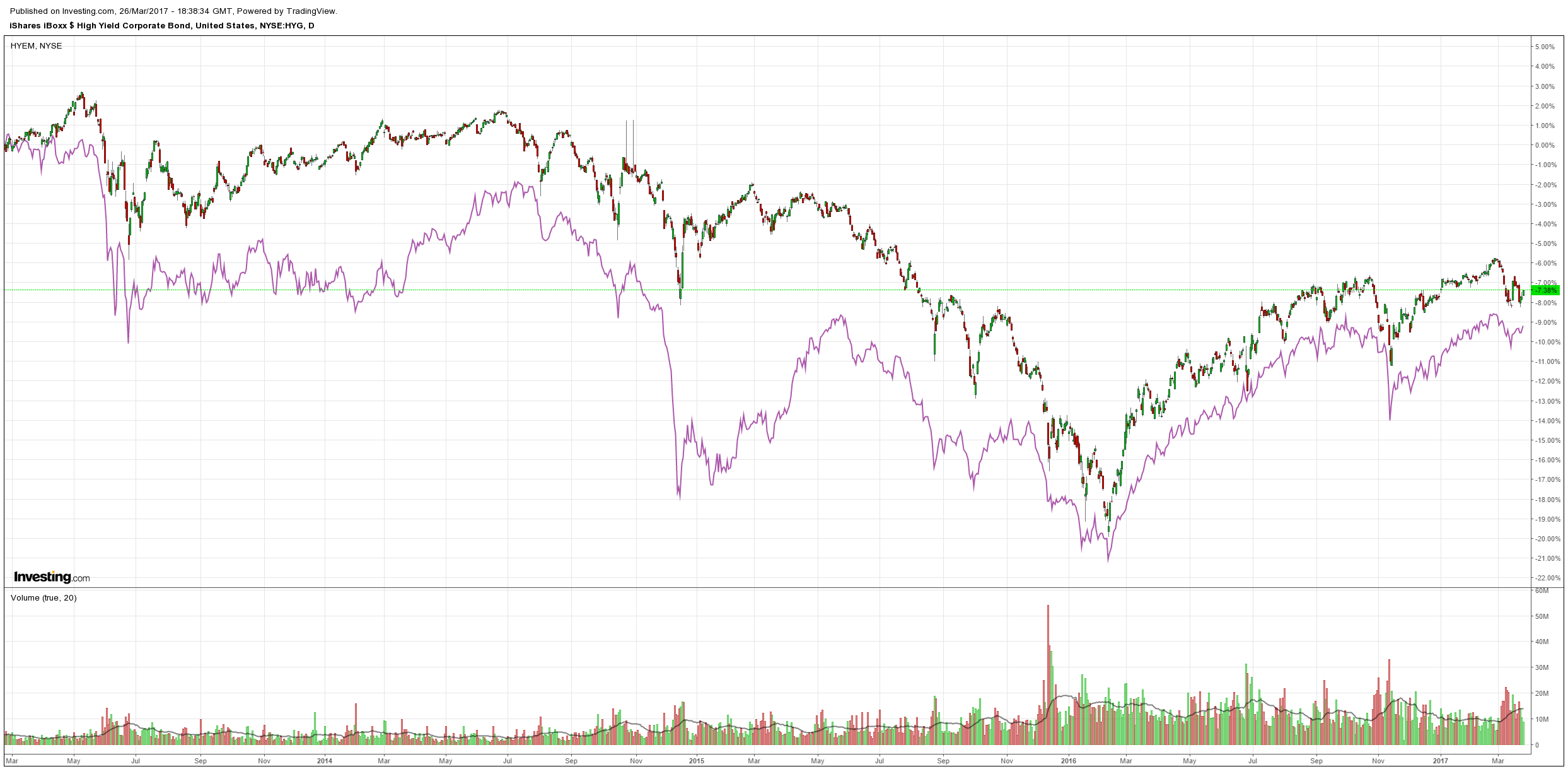

And high yield:

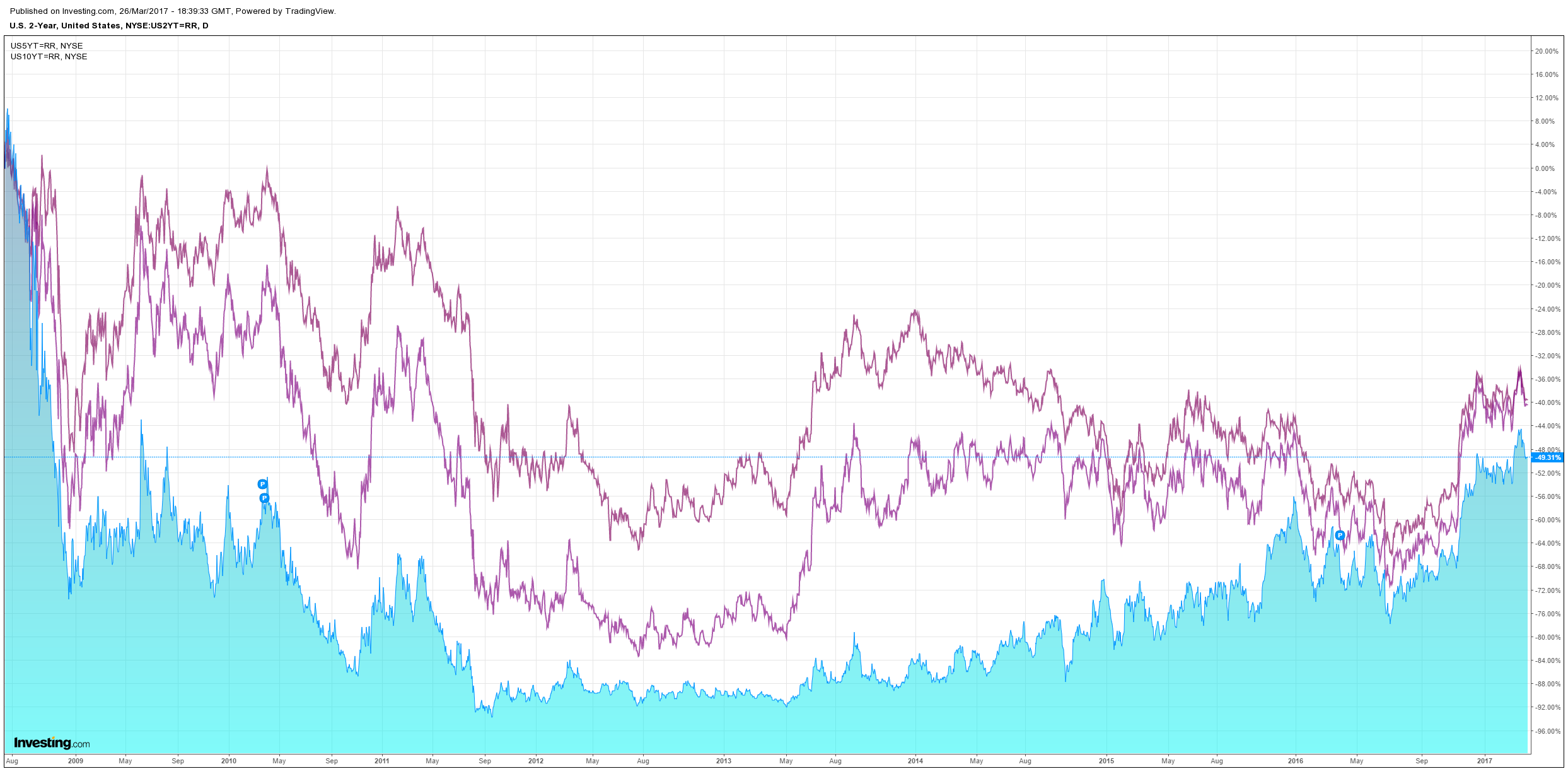

US bonds were stable:

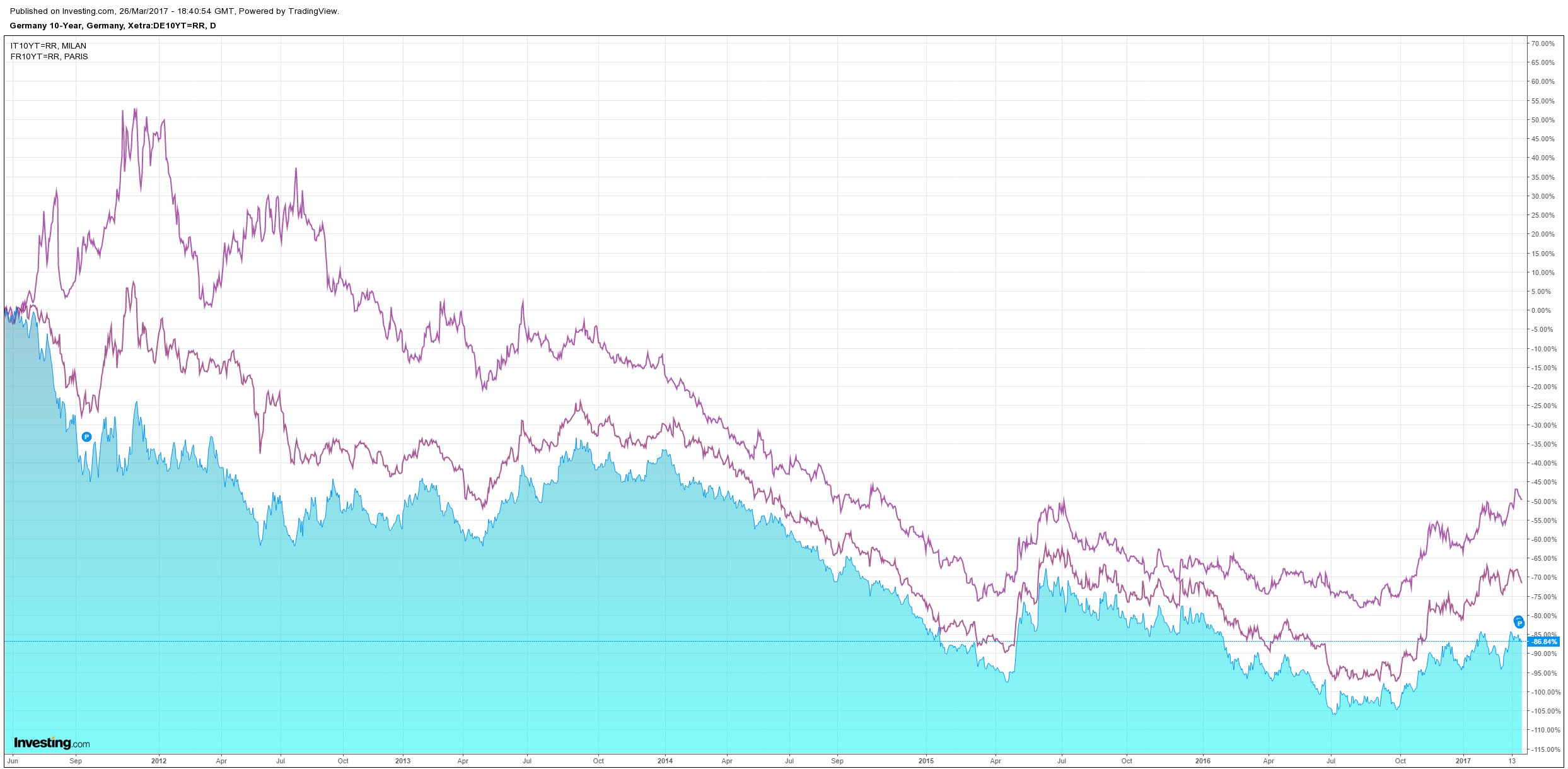

European spreads contracted:

Stocks were flat:

The big news was the failure of the Trump Obamacare bill which was so complete that it has been pulled entirely. Markets have taken this as a mild positive given it may clear the decks for what they really want, which is tax reform. Goldman’s take is typical:

Preliminary discussions on tax reform could begin soon but we do not expect legislative action on tax reform until June. This week’s events do not change our expectation that tax legislation will be enacted within the next year and actually suggest that enactment could come slightly sooner than we previously expected.

1. The American Health Care Act (AHCA) has no path forward for now. House Republicans appear unable to reach a consensus on any bill to repeal the Affordable Care Act (ACA, or “Obamacare”); we believe reaching a consensus among Senate Republicans would have been even more difficult in any case. This would appear to signal an end to the Republican effort to repeal the Affordable Care Act (ACA). That said, addressing health care in some way will be politically necessary, so we do expect health legislation to be considered again at some point later this year or next year.

2. Other issues must be addressed before Republican leaders can shift their full focus to tax legislation. The Senate is expected to consider the nomination of Judge Neil Gorsuch to the Supreme Court the week of April 3, which raises the risk of a Democratic filibuster, which Republicans might counter with a controversial rules change (the so-called “nuclear option” for Supreme Court nominations). Following a two-week recess, Congress will return the week of April 24 to consider extending spending authority, which expires April 28; inclusion of funding for the President’s proposed border wall would raise the risk of a government shutdown.

3. Congress will also need to address the FY18 budget resolution before it can act on tax reform. This is necessary to provide the “reconciliation instructions” that allow Republicans to pass tax legislation with only 51 votes in the Senate (and therefore no Democratic support). As we have noted before, reaching an agreement on the FY budget resolution will not be easy; in the past, conservatives have demanded a balanced budget within ten years but this would require endorsing spending cuts (in non-binding form) that some centrist Republicans might oppose.

4. Tax reform will probably not begin to move through the legislative process until June. In light of the other issues described above, we would not expect the House Ways and Means Committee to vote on a tax reform bill until late May (less likely) or June (more likely). The Committee is unlikely to release a detailed proposal until they are ready to vote, so details regarding the House proposal may not be known for at least another two months or so.

5. Enactment of tax legislation looks just as likely as it did before this week. The health bill faced much different challenges than tax legislation will face. While the health bill would have reduced benefits (tax credits and Medicaid eligibility) and the deficit, the tax bill is likely to provide new benefits (tax cuts) and will probably increase the deficit. Ultimately, we believe that there will be broad support among Republicans in Congress for legislation that reduces the corporate tax rate and cuts personal taxes modestly.

6. However, the defeat of the health bill indicates that complex and controversial tax reforms are likely to be difficult to pass and we note that the “Freedom Caucus” that opposed the health bill also opposes some of the most controversial aspects of the House Republican tax blueprint, like the border-adjusted tax (BAT). This suggests congressional Republicans might scale back their ambitions on tax reform, and pursue a simpler tax cut that includes selected reform elements (e.g. changes to the taxation of foreign profits of US multinationals and profit repatriation).

7. The timing on tax legislation might be pulled slightly forward. Compared to our prior expectation that a tax bill would not be enacted before Q4 2017 and could easily slip to early 2018, with the health issue no longer in play, our central expectation remains that it will be enacted in Q4 2017. However, the risk to that timing now appears more evenly balanced, since there no longer appears to be a risk that the health debate will drag out for several more months.

We’re happy to go along with that for now. We’ve already taken profits on the US long twice and reallocated to Europe so our US position is diminished and hedged. The clear risk at this point is that without the fiscal hand-off stocks and the USD will sell. If that were to happen in the near term while China is still powering along then it would also boost commodity prices and the Australian dollar might break out upwards. We’re hedged for that outcome via the portfolio gold holdings. We’re also moving out the bond curve a little as the global inflation pulse comes under pressure by Q3 as oil prices gains fade year on year (with more falls ahead). We expect wider commodities to follow. Further Fed hikes are only likely to flatten the curve from here as well.

We’re not in the US for any reason other than Trump engineering a short term boom. At this stage we can’t see why wider Republicans would object to such so we’ll remain long but allocations are being nudged around:

- buy the dips in the S&P500 and USD;

- buy the dips in selected European stocks;

- sell rallies in commodities and AUD;

- buy the dips in Aussie bonds (creeping out the curve now);

- buy the dips in gold miners;

- sell property!