If you want iron clad proof that Malcolm Turnbull is a housing affordability phony, check out yesterday’s interview with 2GB’s Ben Fordham:

BEN FORDHAM: I’ve got a few other things I want to throw your way. Housing affordability. Every time we talk about it on the open line the phones just go into meltdown. One of the things that’s been floated so many times, but I know there’s been some denials out there as well, whether you’re considering allowing some people to access their superannuation to buy property. Now, you met with John Alexander on Monday night. He’s asked his economic adviser Peter Hendy, well I think that’s you have asked your c adviser Peter Hendy – I don’t know whether it’s John Alexander who has asked the question. But is it true that a question has been asked that they need to look into this idea, despite previously saying it was a bad one?

PRIME MINISTER: I’m not going to go into discussions with colleagues Ben. Obviously, John has got strong views on this matter and he puts them to me. He is a very accomplished and experienced Member of Parliament. He’s been a great sportsman, a great businessman. I listen to him and I pay a lot of attention to him, but I’m not going to go into speculation about what is, or will not be, or is being considered in the Budget.

BEN FORDHAM: So despite saying previously that it was a bad idea, there have been questions asked of Peter Hendy about it?

PRIME MINISTER: Ben, I know you’re more interested in politics than policy. But what I’ve announced today is the single greatest –

BEN FORDHAM: Well hang on a moment –

PRIME MINISTER: Hang on, just let me, Ben –

BEN FORDHAM: No hang on, when you say I’m more interested in politics than policy, I’m asking you about housing affordability policy and you started telling me that John Alexander was a good tennis player.

PRIME MINISTER: No, I said he was a very distinguished sportsman, and a very successful businessman.

BEN FORDHAM: Well I was asking you about housing affordability policy which is a big concern to my listeners.

PRIME MINISTER: Alright, well it’s –

BEN FORDHAM: They want to know if this is a bad idea or if it’s an idea that’s on the table.

PRIME MINISTER: What is –

BEN FORDHAM: I don’t expect you to confirm or deny.

PRIME MINISTER: What is the idea that you’re particularly referring to?

BEN FORDHAM: Whether there is a plan being considered for people, some, to be able to access their superannuation to buy property.

PRIME MINISTER: I’m not going to confirm, or I’m not going to discuss particular issues that are in consideration for the Budget. The fact of the matter is there are a lot of submissions being made by many different people, including very experienced and very capable colleagues like John Alexander, who has a long interest in this issue. He’s a very capable guy, a great businessman.

BEN FORDHAM: No worries. Great sportsman.

PRIME MINISTER: No, I said a great businessman.

BEN FORDHAM: I know it’s on the table anyway. It’s on the table.

PRIME MINISTER: No Ben, let’s just be quite clear. Everyone has got views on housing affordability. Let me tell you what the fundamental issue is. This is from my experience and I’ve paid a lot of attention to this issue over many years. The reason housing is not as affordable as it should be in Sydney in particular, is because we are not building enough dwellings. We’re not building enough houses and so forth. That’s because governments – local governments, state government s – have not provided the planning approvals, the zoning, to enable it to be done. So it’s basically a supply and demand problem. Now to their credit, the Liberal state government, Gladys Berejiklian’s government, Mike Baird’s before it, Barry O’Farrell’s have made a lot of progress in this area. But the supply – demand shortfall has taken a long time to catch up. That’s why, as part of our City Deals, we are working on agreements with state governments and city governments, to expand more housing supply. It’s very important.

BEN FORDHAM: I’ve been saying on this show for a while and I don’t know whether you are across this and you could be forgiven for not being across it because it’s been gathering dust on various bureaucrats and Ministers desks for about 10 years. But there is legislation sitting there in Canberra in regards to anti-money laundering legislation. There has been a big bust today, a big case today involving Tabcorp. But there is a second factor there of that legislation that’s been gathering dust for nine years, now that involves real estate agents. So if you’ve got people coming in from overseas, I’m talking about illegal buyers from overseas, from China specifically and elsewhere, that real estate agents should have to declare where that money has come from just like they have to do at the moment in banks and casinos and bullion dealers. Do you think that’s worth doing something about considering it’s been sitting there on someone’s desk for nine years now?

PRIME MINISTER: Look I haven’t seen the details of the particular case. I’ve been up in the Snowy Mountains today talking about the biggest change to energy supply in the east coast of Australia for many years. Really taking on this nation building project, the Snowy Mountain, that we’ve inherited from our grandparents and parents’ generations and carrying it forward.

Now that is what I have been focused on today so I haven’t caught up with the issue you referred to.

You’ll see from the above that Turnbull won’t rule-out allowing first home buyers (FHBs) to access their super for housing – an incredibly bad policy that would drive-up house prices, cost the Budget billions over the long-run, and put people’s retirement incomes at risk. It also comes despite Turnbull himself declaring the policy “a thoroughly bad idea” in 2015.

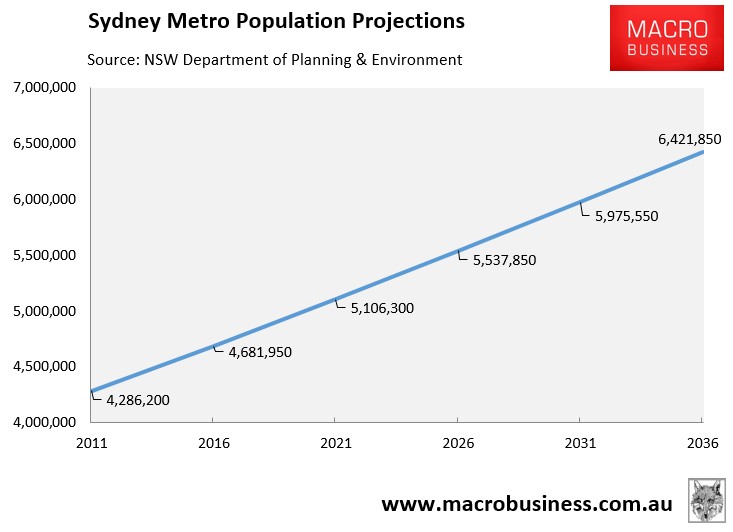

Next Turnbull tries to claim that Sydney’s housing is unaffordable “because we are not building enough dwellings… So it’s basically a supply and demand problem”. Conveniently, Turnbull refuses to acknowledge that the main reason why Sydney is not building enough dwellings is because of the mass immigration program run by the federal government, which has seen Sydney’s population surge by 800,000 people over the past decade and is projected to see Sydney’s population balloon by 87,000 people per year (1.74 million in total) over the next 20 years – equivalent to adding 4.5 Canberra’s:

Clearly, the best way to solve the shortfall in dwelling supply is for Turnbull to rein-in Australia’s mass immigration program.

Finally, we have Turnbull feigning ignorance over Australia’s refusal to implement the second tranche of anti-money laundering (AML) legislation covering real estate gate keepers, which has been gathering dust for a decade despite explicit criticism from the global regulator, the Paris-based Financial Action Taskforce (FATF), that Australian homes are a haven for laundered funds, particularly from China, as well as similar warnings from Austrac.

In the meantime, dodgy Chinese money continues to pile into Australian property, to the chagrin of the global AML regulator, FATF. In the process, young Australians are being priced-out of home ownership, in part due to hot Asian money.

In short, Do-Nothing Malcolm is a complete housing affordability phony. Any policies implemented in the May Budget are likely to further inflate housing and make housing affordability even worse.

unconventionaleconomist@hotmail.com