It has been an interesting start to 2017 for commodity markets, with a maturing industrial recovery, rising inflation expectations and a surprising degree of economic confidence all combining to offer an upward price bias.

However, the start of March has certainly seen some cracks starting to appear, notably in China as the government continues to tighten monetary policy at the margin. While demand is clearly significantly better than this time last year, current indicators aren’t showing the aggressiveness we might have expected. Moreover, we are starting to see signs of supply response, and inventories are already elevated.

We have raised our 2017 forecasts across the majority of metals and bulk commodities we cover. However, after the run we have had, from current levels we are generally neutral to bearish on most prices into mid-year, as Chinese tightening starts to show wider impact. As we noted at the start of the year, this year is all about duration of the cyclical support for commodity prices, particularly for resource producers looking to de-lever further.

Iron ore – awaiting the whip lower

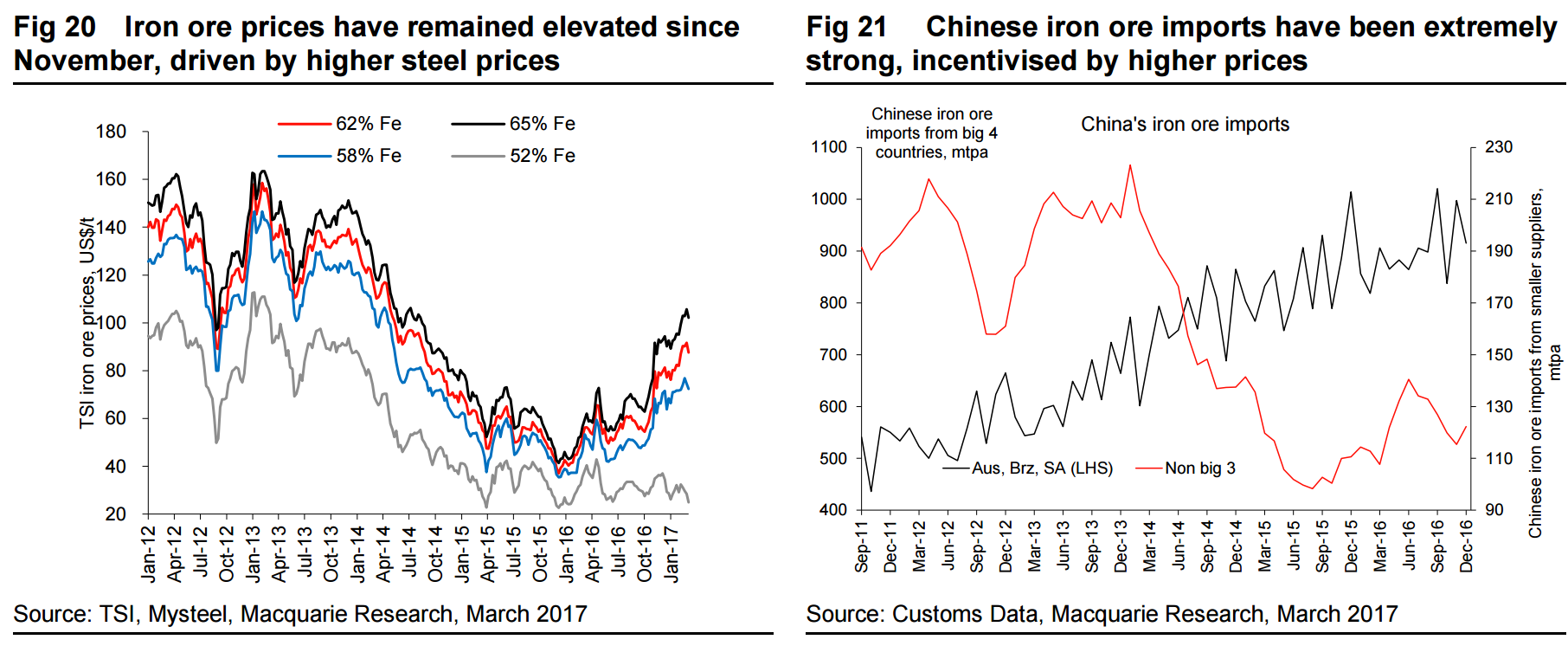

Iron ore prices have far outpaced our expectations since November 2016, and given that it has taking longer than we expected for fundamentals to feed through to prices, we have upgraded near-term iron ore forecasts on a mark-to-market basis to $85/t for 1Q17 and $65/t for 2Q17. This lifts our full year price forecast by 16.3% to $63/t. However, we make no changes to our expectation that prices will revert back to a $50/t average in 2H17, and a $47/t average in 2018 as market conditions continue to worsen next year.

Fundamentally iron ore supply has already responded strongly on the seaborne market to the higher prices seen last year. China’s total iron ore imports rose 71mt, or 7.5% YoY, to 1.025bn tonnes, while we estimate iron ore consumption rose by less than 1% last year. Chinese domestic mine output, while responding clearly to the rally in prices in 1H16, has been held back by winter weather conditions from responding to the widening margin incentive since spot prices accelerated above $80/t in November. However, we maintain very high confidence that supply will respond soon, especially as Chinese domestic mining costs have fallen by 5% over the past year in local currency terms, and by over 11% in US$ terms once factoring in RMB depreciation.

The excess supply of iron ore is most clearly evidenced by the surge in iron ore inventory at both mills and ports. Indeed the latest iron ore inventory data from Mysteel shows iron ore stocks at 45 major Chinese ports has increased to a record high of over 131mt, up 16mt since the start of 2017 alone. Iron ore prices have sustained higher than we expected due to a combination of three factors: First, high expectations of demand for steel and consequently iron ore this year, which have led to mills and traders to build inventory. Second, weaker shipments out of Australia in recent weeks due to heavy rains have slightly reduced cargo availability in the spot market. Finally, the strong profitability at steel mills has meant that mills are chasing higher grade iron ore supply to lift productivity. However, once steel margins begin to weaken and mills enter a destocking cycle and start to look back to low grade ore to save costs, we expect the inventory of iron ore to prove a drag on market prices, and result in a fast correction back to a more sustainable price range of $50-60/t.

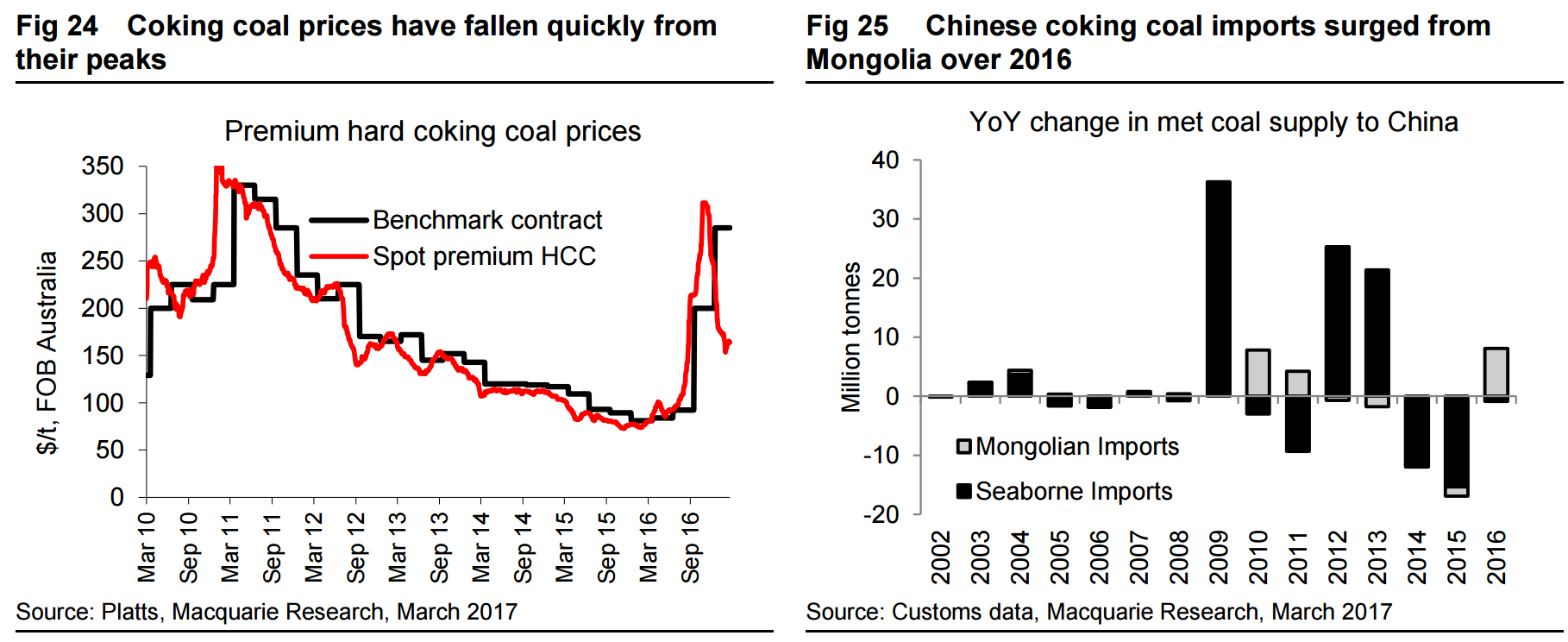

Met coal – a rapid supply response = a rapid price fall

In contrast to our higher iron ore price forecasts, we are cutting our coking coal price forecasts by 11% for this year and 9% for 2018, as Chinese coal policy increasingly looks like exempting coking coal from any production restrictions this year. Additionally, there have been minimal supply disruptions due to weather in Australia in 1Q17, and the supply response to higher prices has happened quicker than we previously expected from the US and Mongolia.

Coking coal prices are being supported near term as Chinese steel mills look to lift production into their peak 2Q17 season; however, the abundance of material available on the seaborne market looks likely to result in lower prices before long. We expect 2Q17 contract settlements for HCC in Japan to be at $175/t, but it is likely that we will see increasing discounts to the benchmark price as miners look to guarantee more cargoes given the excess supply currently on offer. By the end of the year, however, we expect HCC prices to return below the top of the marginal cost curve at $140/t, as the market no longer needs to encourage further supply from marginal producers in places such as the US.

Thermal coal – Still underwritten by China

While recent statements on coal policy from the NPC and our meetings in China last week with coal industry professionals lead us to believe there will not be any restrictions on coking coal supply this year, we still firmly believe that the presence of a “Beijing Put” will continue to underwrite thermal coal prices globally. Thermal coal supply has jumped since November following the postponement of the “276 days” restrictions until the end of March, but prices have remained resilient above RMB600/t as inventory has remained lean through peak power demand season.

The Chinese government recently outlined their targeted thermal coal price range based around the annual contract price of RMB535/t. Supply interventions remain highly likely if prices fall below RMB470/t, but given that prices remain above the higher end of the governments desired range, expectations are increasing that there will be minimal reapplication of the 276 days policy at the end of March.

RMB535/t equates to around $70/t FOB Newc, and we still expect seaborne prices to come down to this level by mid-year, as coal supply in China should outpace demand in its weaker season in 2Q17. However, with prices having held up higher than we expected, we raise our price forecasts for spot Australian thermal coal by 4.2% for this year to $75/t. We remain concerned, however, about potential for China to restrict coal imports should domestic coal prices weaken to the lower end of the government’s target range, but we do not factor any restrictions into our forecasts. Given the strength in current prices, we have raised our Japanese annual contract price by ~7% this year and ~11% next to $87.5/t and $80/t FOB Australia respectively. We have made no change to future years, with a downward trajectory as Chinese import restrictions drive a two-tier market with lower seaborne pricing.

I am of course a little more bearish on iron ore, quite a bit more on coking coal and the same on thermal.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.