LNG blew its own bubble and bust. Time to wear it

Via the AFR today:

Santos’s $US18.5 billion ($24 billion) GLNG project in Queensland will swallow about 20 per cent of the gas expected to be available this year for users on the east coast, piling pressure on the venture to ease the squeeze by increasing output or restricting exports.

The latest estimate from consultancy Wood Mackenzie hones attention on how the project is straining the east coast supplies of gas, where local manufacturers are being left short as more gas is shipped to Asia as LNG.

…”GLNG is in a difficult spot here, having to choose between complying with the pressure to supply to the domestic market, and maintaining gas feedstock to salvage what value it can from its investment in GLNG,” said Wood Mackenzie analyst Saul Kavonic.

“And as long as GLNG keeps hoovering up gas from the domestic market, it is a struggle to see how additional domestic gas supplies from the neighbouring LNG projects will alleviate the shortage. Those volumes may just end up being exported via GLNG anyway.”

Still GLNG secured government approval for its $US18.5 billion gas export project on the basis it could buy extra gas.

“GLNG was originally sanctioned (and approved by government) on the assumption on buying third-party gas,” said Citigroup analyst Dale Koenders.

“We don’t think this will change either.”

I don’t know if it will change but the risk is high and rising given it is by far the most logical solution. Australia does not have domestic reservation or an overall energy regulation regime, nor regulator, so government did not “sanction” the project at all. It approved it on the basis of its environmental impacts and that’s all, via the QLD government:

All applications for major coal seam gas (CSG) production, gas pipeline and liquefied natural gas (LNG) processing plant projects are subject to a strict assessment and approvals process through an environmental impact statement (EIS) process.

The EIS may be carried out under the State Development and Public Works Organisation Act 1971 (PDF, 1.4MB) or through the Environmental Protection Act 1994 (PDF, 3MB).

A regional interests development approval (RIDA) may also be required where a resource activity is proposed in an area of regional interest. Find out more about applying for a RIDA under the Regional Planning Interests Act 2014.

Three projects have already achieved conditional approval from this process with numerous conditions imposed on each.

The EIS must include an environmental management plan that identifies potential impacts on the surrounding environment, and proposes actions to minimise and manage those impacts.

The GLNG EIS did not mention third party gas beyond one contract, via Credit Suisse:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31

It may be stupid for Australia to have no energy management regime but the LNGers knew it so they can’t blame official project approvals for the shortage now.

The fact is that GLNG is, all by itself, doing enormous damage to the east coast economy and fixing it is bloody easy with a tiny loss of $600m shared among four partners. What will it cost us to not fix it?

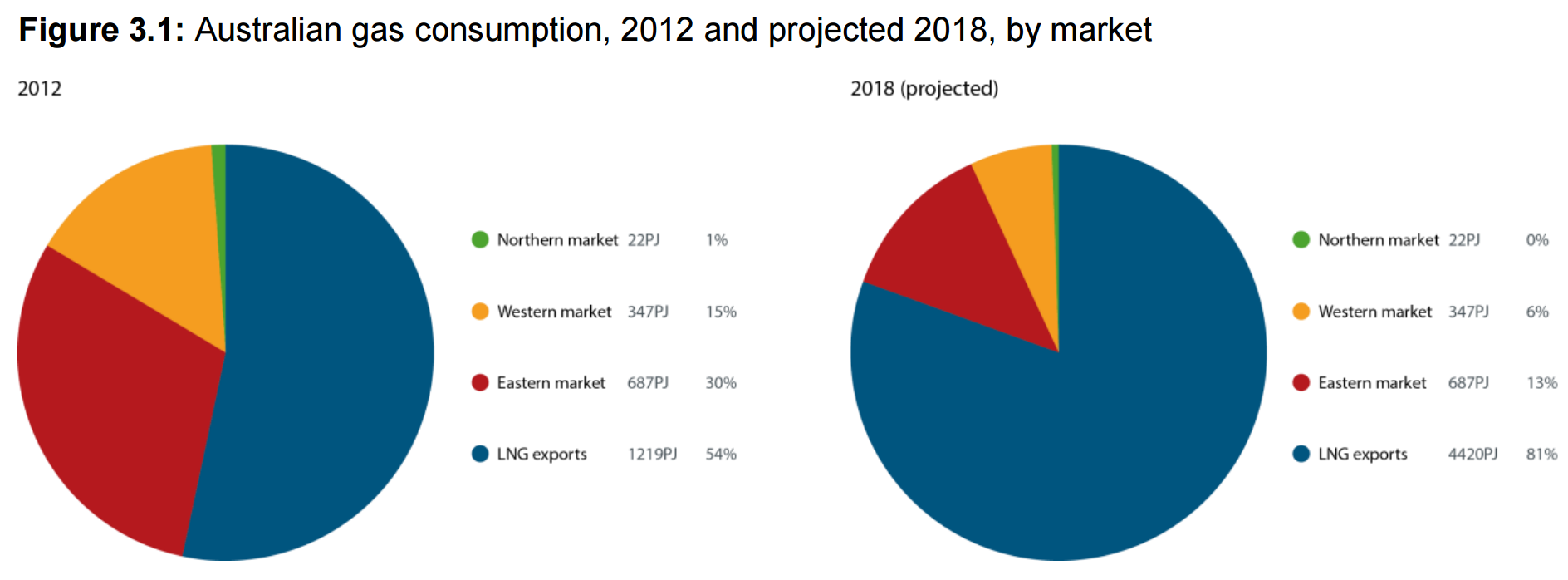

We need to hold back a tiny 160Pj of gas to balance the domestic market. That amounts to a fantastically paltry 2.9% of total national demand or 3.6% of total export volumes in 2018. 80% of Australian gas production would still go to Asia.

At current rates of consumption, east coast gas of 1100PJs will cost $13.2bn at $12GJ. If we held back the 160Pj we could halve that. Electricity prices have also doubled to $100mWh on the gas price and we currently pay out roughly $5bn for our two terrawatts of electricity consumption. So that’s another $2.5bn saving if we can halve it. It is the effective equivalent of a $9bn tax (before we consider the knock-on effects of further capital mis-allocation) levied on east coast households and industry by the foreign shareholders and governments that own Curtis Island LNG. Pure economic rents siphoned off just because they can be.

But that’s not the end of it. These same firms and governments lose money on every tonne that they ship offshore. They buggered up their investment metrics so horribly that when you include the cost of capital for building the plants, they are losing money hand over fist. This even includes the west coast LNG plants. As a result they can claim huge depreciation and write-offs on massively inflated investments and they pay no tax.

Australian LNG blew an enormous bubble that has now burst. It did it all by itself. The fallout is being redirected onto the east coast economy via a cartel gouge when the only rightful place for it is the projects themselves.

Time to hand it back. Ban third party exports.