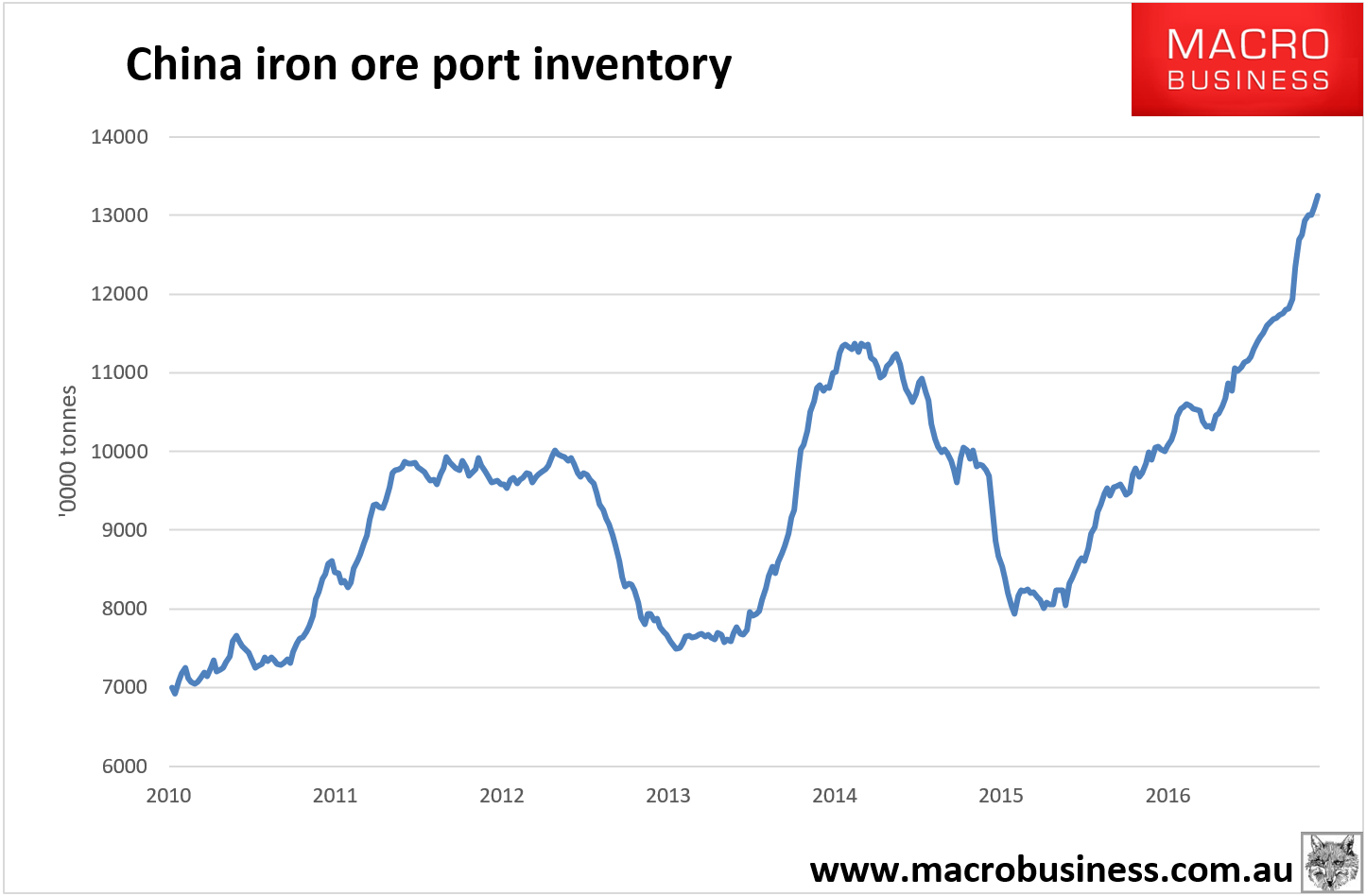

It’s funny, you know, I’ve never described iron ore as a bubble. Not even when it was trading at $200 per tonne. But it is a bubble today. Bartho chimes in today:

Goldman Sachs may have provided part of the explanation as to why stocks at ports have been rising. In a note issued yesterday, the group’s analysts estimated that about a third of the 37 million tonnes of stocks added over the past year and nearly a third of the total stocks are held by traders, who can use the ore as collateral for loans.

While it is relatively new, there is a massive derivatives market in iron ore. Last year, according to an earlier Goldman analysis, the turnover in iron ore futures averaged $US7 billion a day.

With the prices on the Dalian exchange are generally higher than the prices at the ports and, in a market dominated by individuals rather than institution, s there may be a purely speculative element to the build-up in stocks.

The speculative component of trading almost certainly explains why, after running up to about $US95 a tonne earlier this year, the price dropped back towards $US80 a tonne against a backdrop of falling steel futures.

It’s also why it will fall much further. Hoarding is classic sign of a speculative bubble, from Paul Krugman in 2011:

During the last commodity price spike, less than three years ago, many people laid the blame at the feet of speculators. I never accepted that as the prime cause, mainly because so many of the speculation-did-it people seemed confused about the difference between buying a futures contract and actually hoarding physical stocks; as a very useful analysis by Sanders and Irwin (pdf) puts it,

Index fund buying is no more “new demand” than the corresponding selling is “new supply.”

True, high futures prices can provide an incentive to accumulate physical stocks. But during the 2007-2008 price surge there was little evidence of such accumulation.

What about this time?

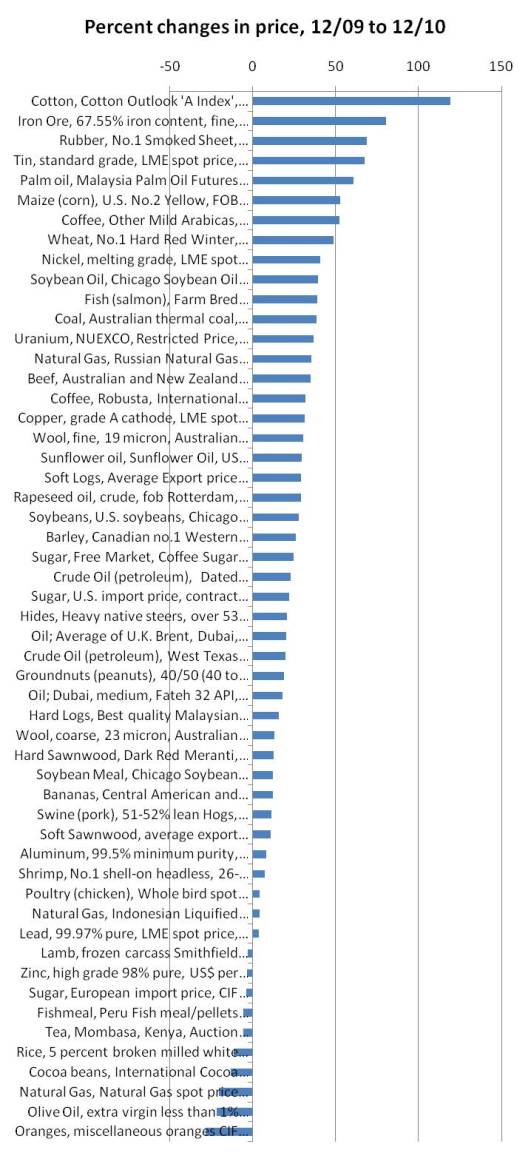

I find it illuminating to take the IMF commodity data and rank commodities by the percentage price increase during 2010:

Up at the top are cotton and iron ore. What’s going on up there?

First and foremost, China: it’s clear from news coverage that Chinese demand is driving the markets. As I and others have been pointing out, we’ve got a bifurcated world right now, with advanced economies still depressed but emerging economies in an inflationary boom; commodity prices are reflecting the boom part of the picture.

But Chinese demand isn’t just a matter of fundamentals: all the evidence suggests that there’s a lot of physical hoarding going on. Chinese farmers are apparently hoarding lots of cotton, while China is holding record stockpiles of iron ore.

So the case for a speculative component is a lot stronger this time around. But — and this is important — the speculation is not being driven by financialization, by all those index fund investors going long.

This time it is driven by financialisation. As UBS noted today:

Iron ore futures have proven very popular since their introduction to the DCE in 2013 becoming the most traded iron ore derivatives in the world. They make up a significant amount of total DCE contracts (23% in 2016). In 2016 the accumulative trading volume of iron ore reached 34.227 billion tonnes, with a daily trading volume of 1,402,700 contracts and a daily open interest of up to 871,000 contracts. To put this in perspective, this volume is 29 times what is being traded on the Singapore exchange and 1.2 times the open interest.

Of the 477,200 market participants there are now 11,605 corporate accounts, and over 800 industrial clients (717 trading houses, 88 Chinese steel mills and 10 Chinese iron ore companies). While these corporate accounts make up just over 2% of accounts they make up 28% of volume and 34% of open interest. These corporate accounts do have a strong influence over the market due to the magnitude of their individual market shares however the bulk of volume is controlled by the retail traders, who operate through brokers, also giving them significant influence.

Which has led to this hilarity:

And the outcome is as predictable as the tides. When the demand/supply balance shifts, the great hoard will panic and dump its pile. Prices will crash accordingly, even lower than otherwise would have been.

Futures are supposed to reduce volatility but sometimes they increase it.