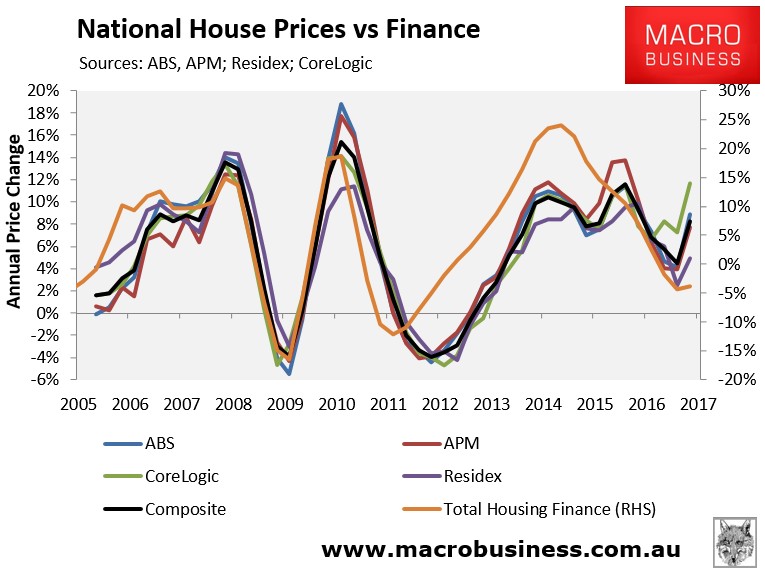

Over the past year, I have presented data showing that the historical relationship between dwelling prices and the value of housing finance commitments (excluding refinancings) has broken down somewhat over the latest housing cycle:

I have also offered two potential explanations for this breakdown:

- falling transaction volumes, whereby falling finance commitments are chasing even fewer homes, thus resulting in still-rising prices; and

- the potential for cash buyers, such as buyers from overseas, whom are not captured in the housing finance statistics.

Today, I want to focus on the first explanation: falling transaction volumes, which are illustrated below using the latest ABS data, released on Tuesday.

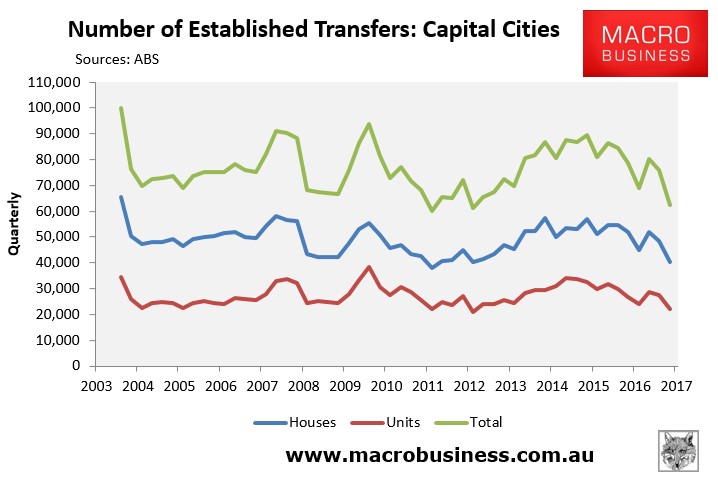

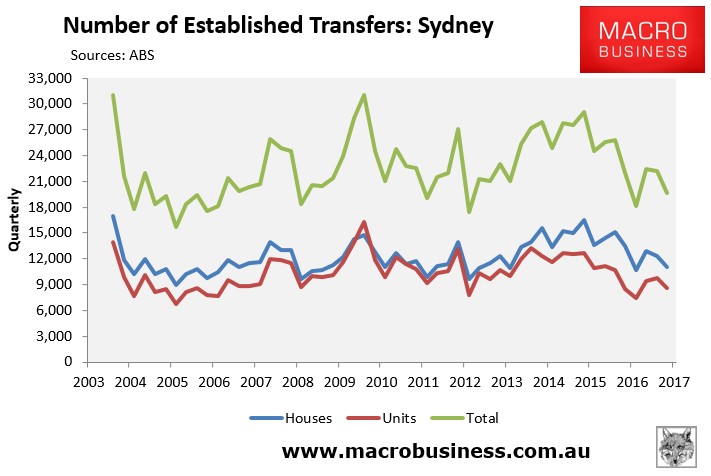

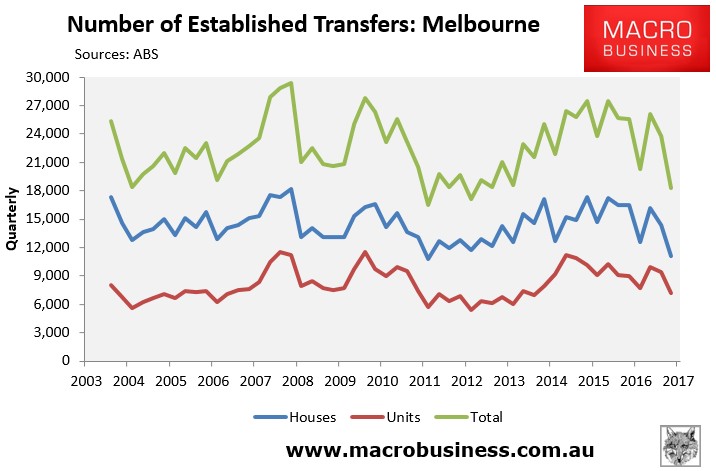

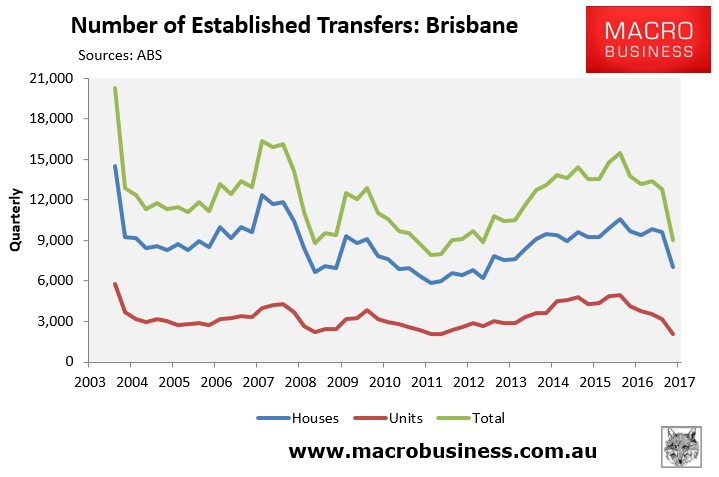

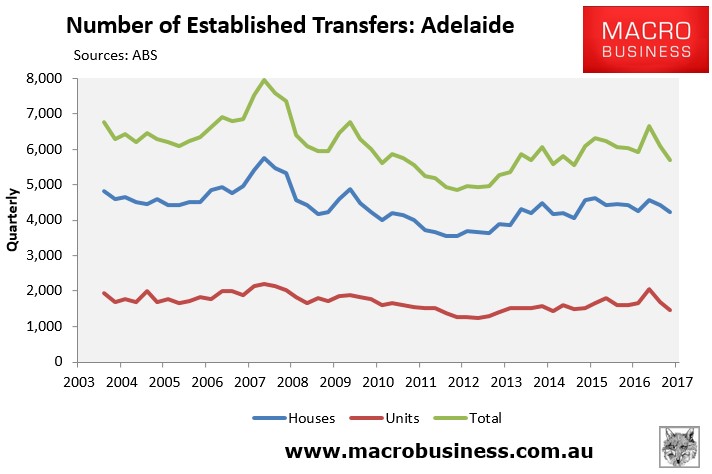

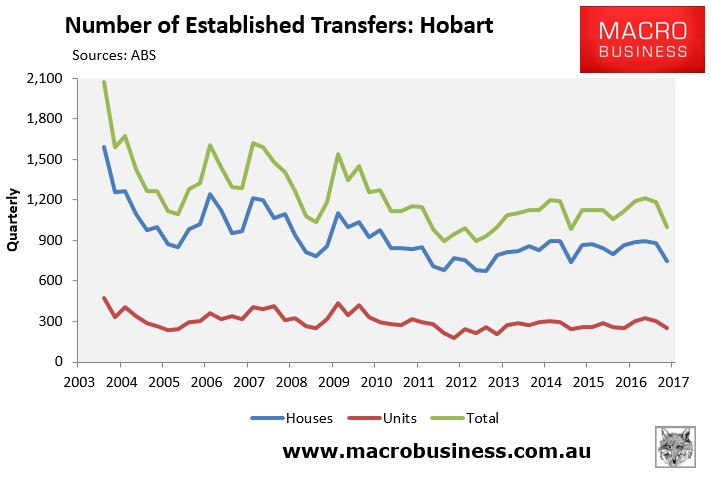

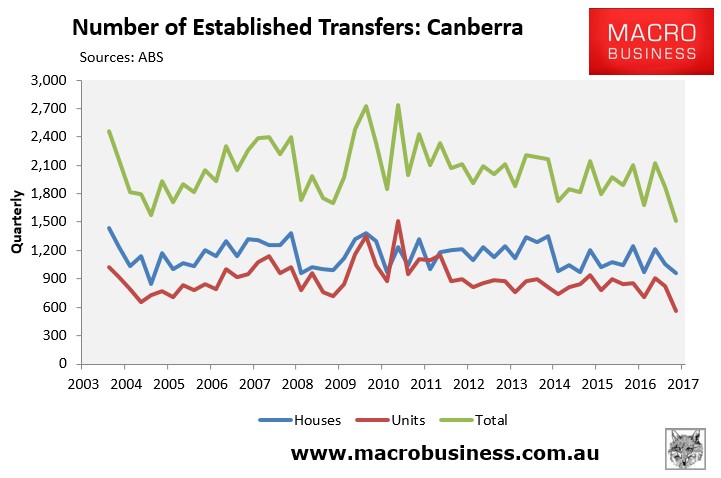

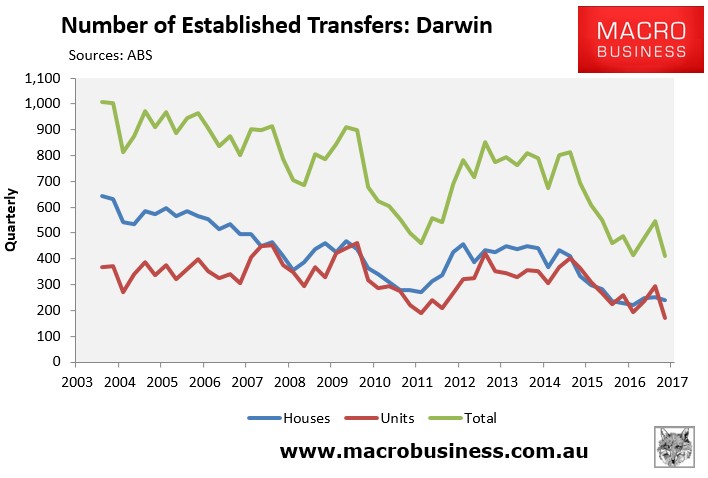

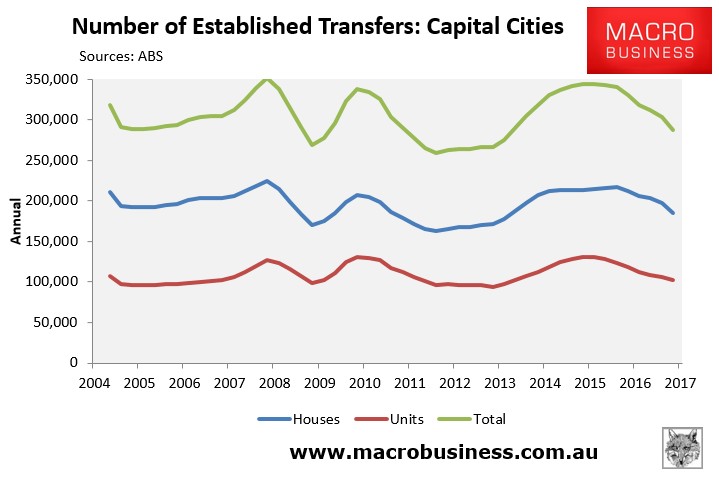

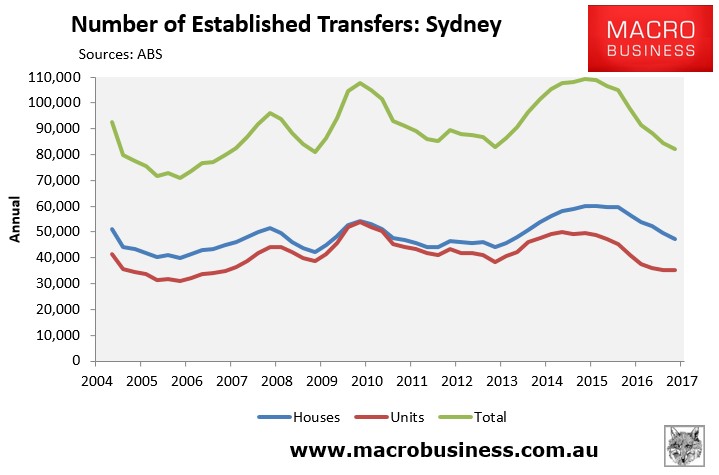

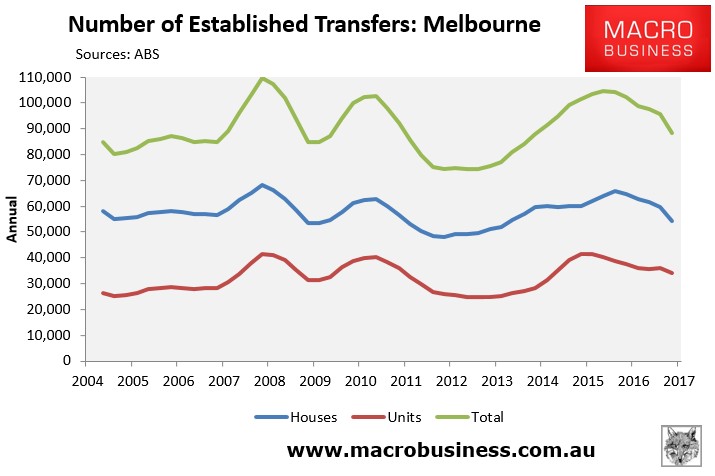

First, the below charts show the quarterly number of dwelling transfers at the national capital city level, as well as at the individual capital city level:

As shown above, transfer volumes have fallen everywhere in recent quarters.

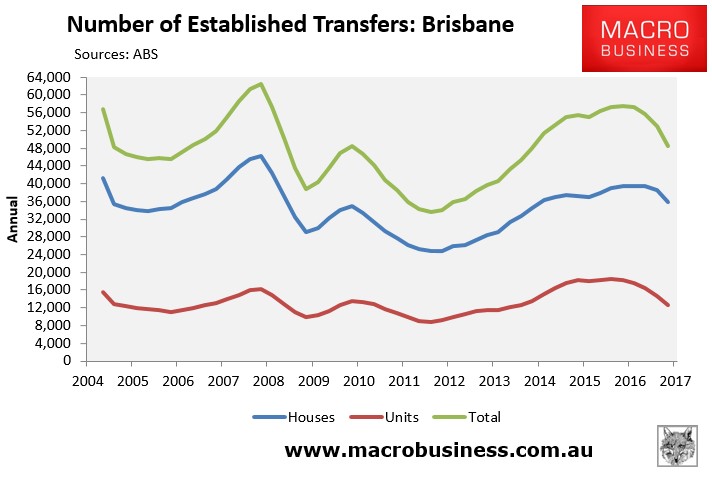

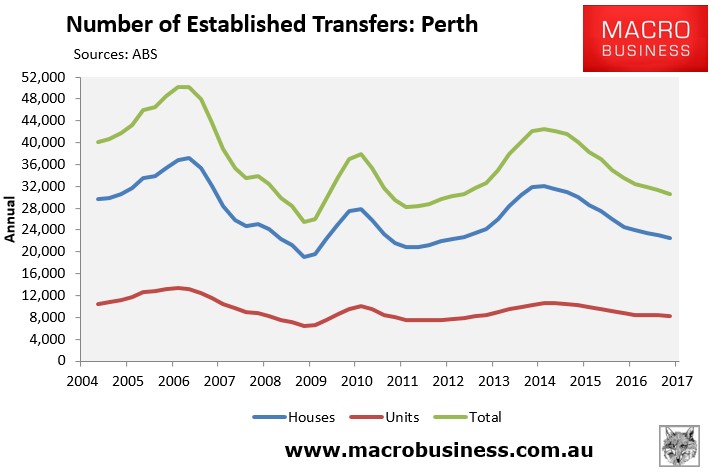

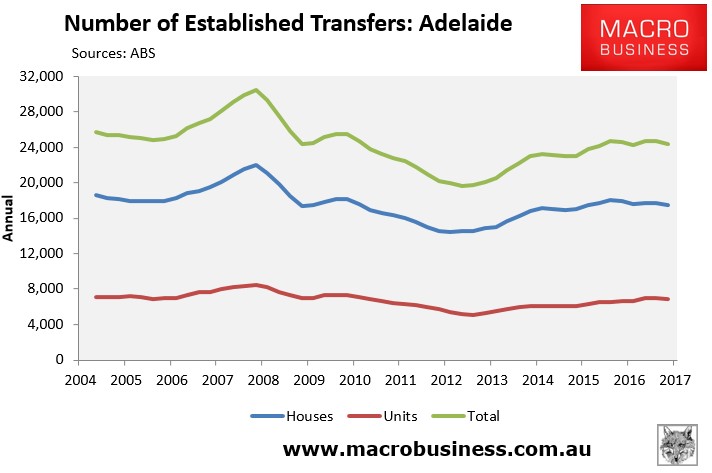

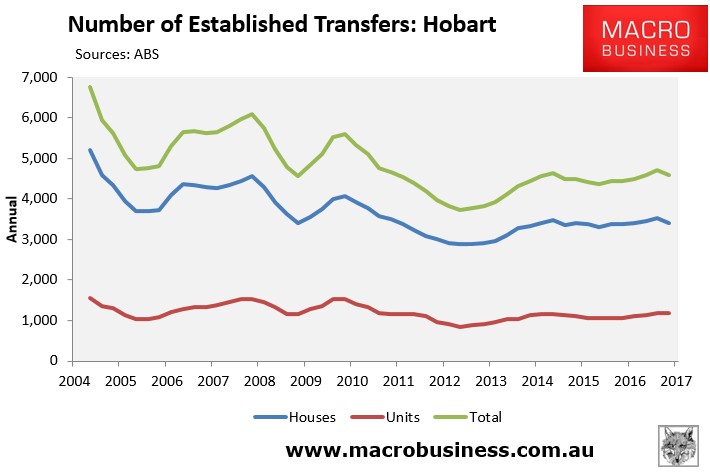

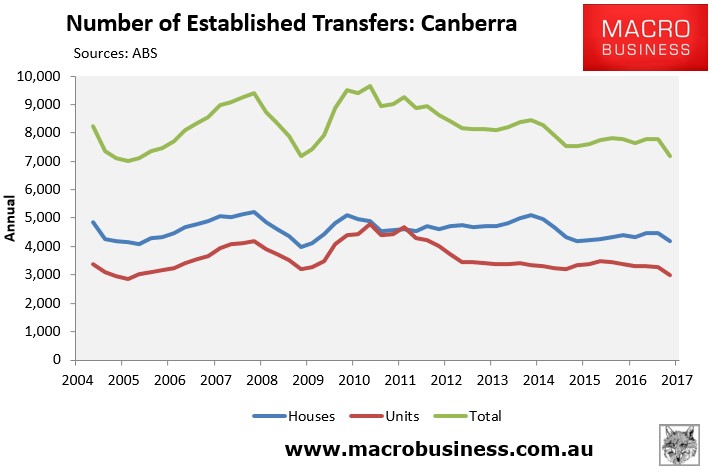

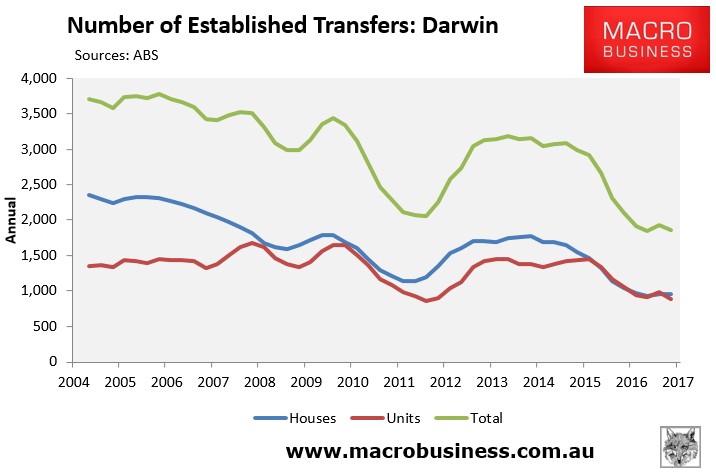

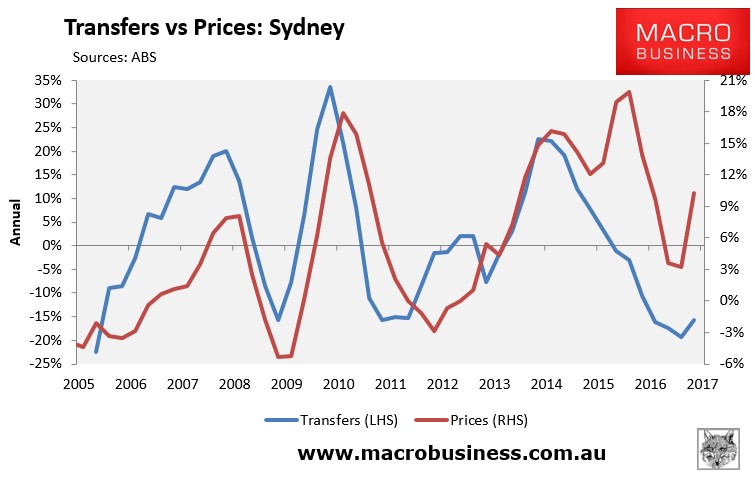

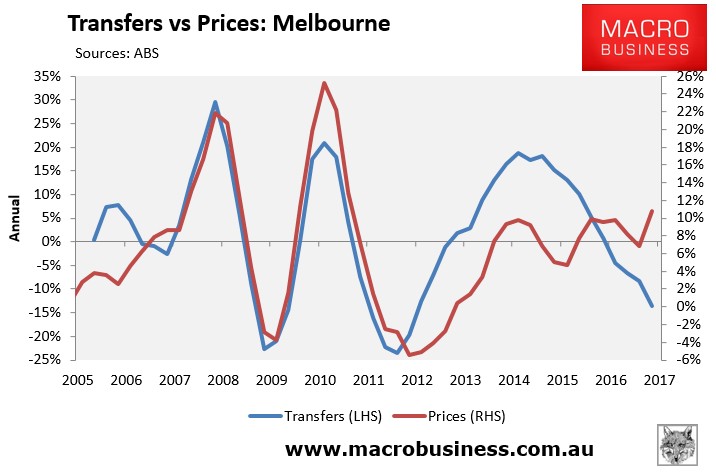

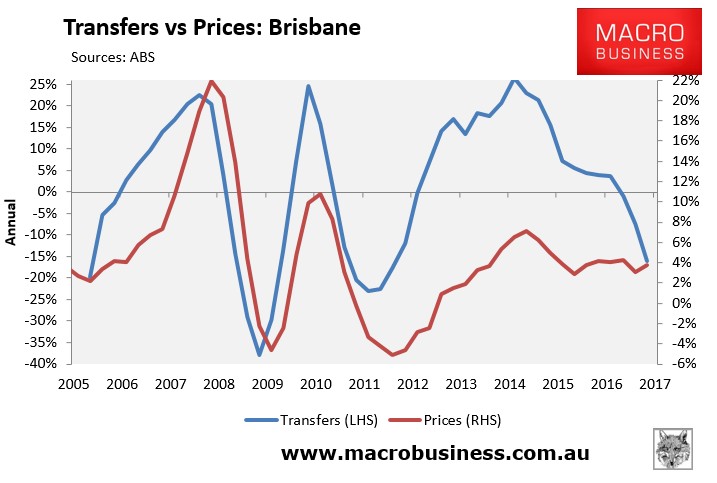

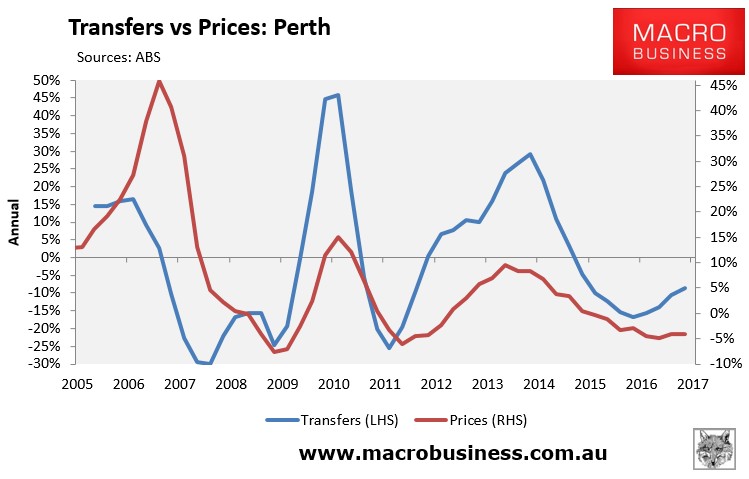

Next, the below charts present the same data, but this time on a rolling annual basis:

It’s much the same story, with transfer volumes falling quite heavily across the major markets.

Therefore, falling transaction volumes do appear to have offset falling finance commitments, thus ensuring prices have kept rising.

The RBA’s latest bulletin made similar observations:

Over the past two years, its [turnover’s] contribution to new housing finance has been declining. Over the same period, housing prices have been making a large contribution to growth in housing finance. The decline in turnover of existing housing goes some way to explaining why housing credit growth has been relatively muted, despite rapidly rising housing prices.

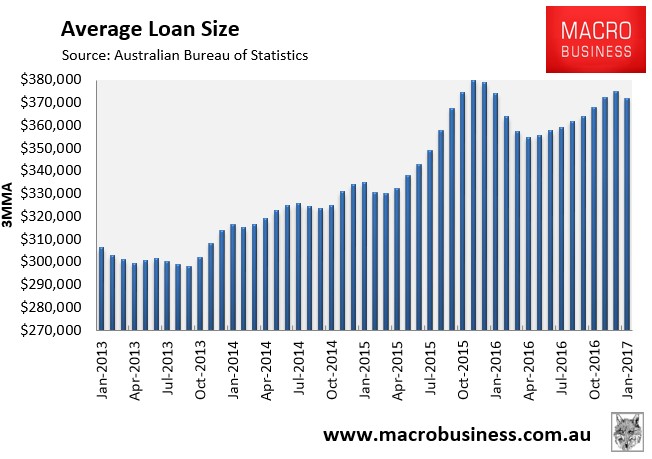

That said, average loan sizes have fallen over the past year – down 0.5% in the year to January – despite rebounding recently:

Thus, we cannot discount the fact that there may also be significant cash sales occurring, such as to foreign buyers, although we have no conclusive evidence.

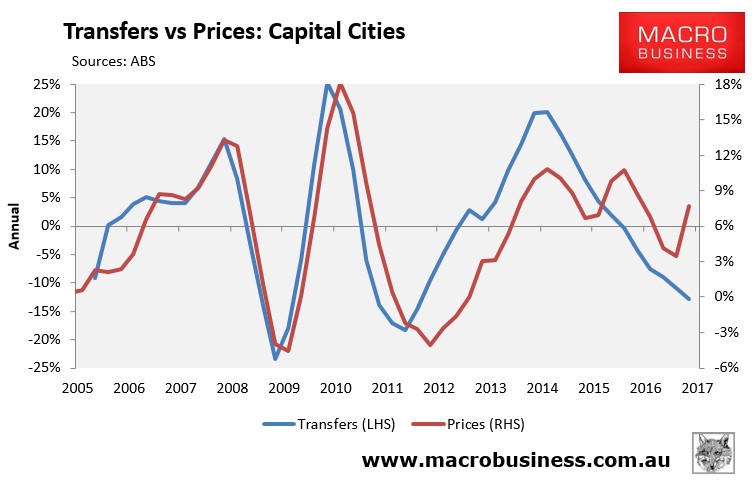

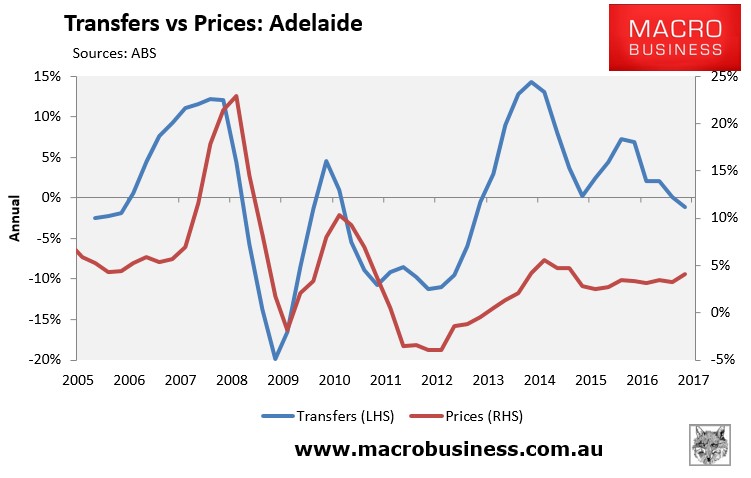

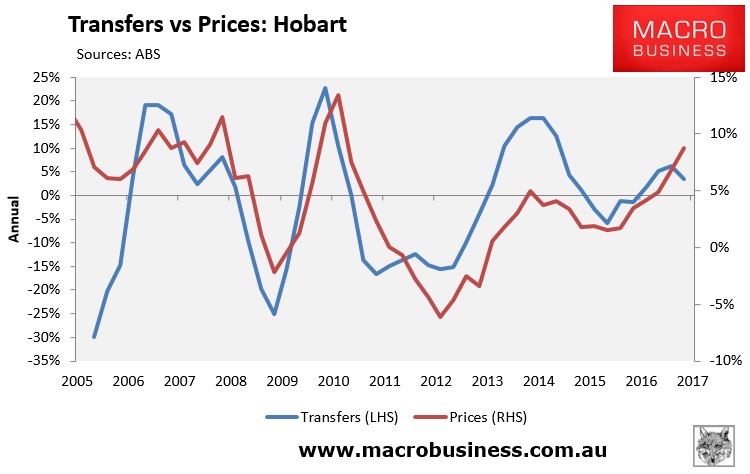

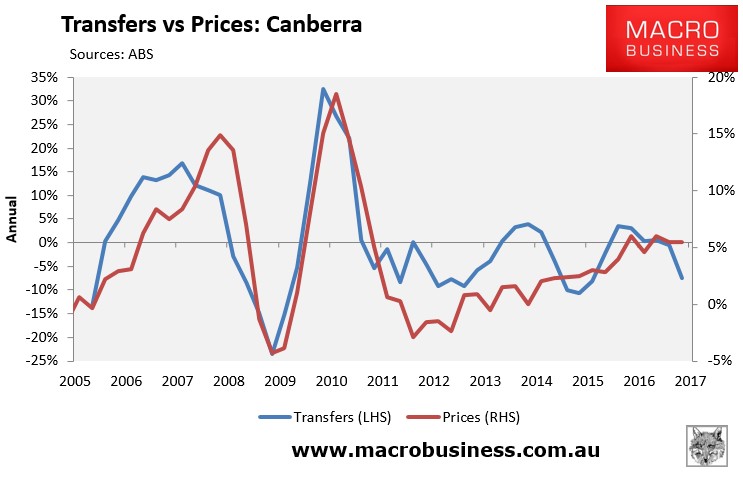

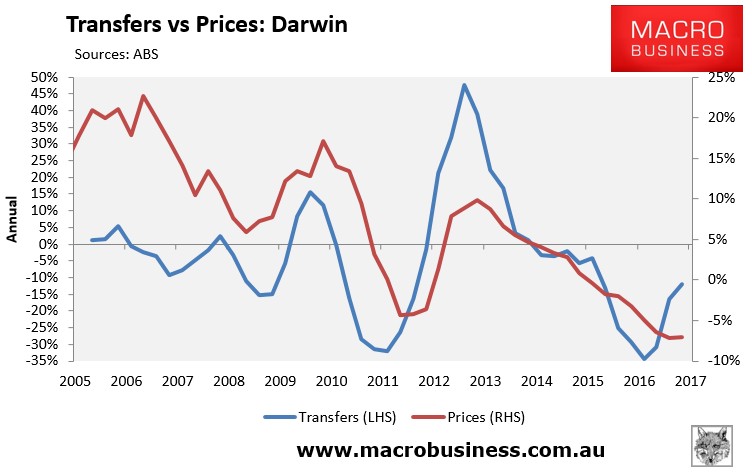

Nevertheless, changes in transfer volumes have historically been a good leading indicator of prices, at least for the major capitals:

But as you can see above, there has been a breakdown in this relationship over recent times, which is unusual.

Nevertheless, the RBA did note some important implications of the falling turnover rate its recent Bulletin article, namely:

- Reduced revenue for occupations involved in housing transactions, such as real estate agents, lawyers and finance professionals;

- Reduced stamp duty receipts;

- Reduced household retail spending, particularly on durable goods such as furniture, home appliances and electrical or electronic devices; and

- Reduced housing equity withdrawal (a good thing).

Housing shrinkflation is clearly bad news for the economy at large. Not only do sectors exposed to turnover take a hit (think real estate agents and mortgage lenders), but so does household consumption and state revenues. Moreover, with folks unable or unwilling to shift home, participation rates in the labour market fall as sclerosis eats away at market flexibility.

Basically, the Australian property bubble is now so absurdly large, so ludicrously dependent upon policy distortions and Coalition carpet-baggers, so hilariously dislocated from the sad little economy beneath it, that even traditional beneficiaries of such booms – like the banks and real estate agents – are now shivering in its titanic shadow.