The Reserve Bank of Australia (RBA) yesterday released its quarterly Bulletin, which included some interesting analysis of housing ‘shrinkflation’: the unusual phenomenon whereby housing turnover falls as dwelling prices rise.

Below are the key extracts.

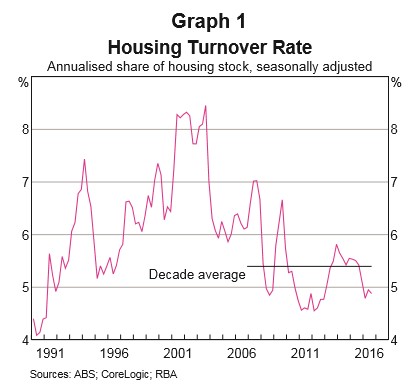

After rising for a number of years, the rate of housing turnover (that is, the number of transactions relative to the stock of housing) has trended lower since the early 2000s (Graph 1). The most recent decline in the turnover rate has been unusual, particularly given the strength in other indicators of national housing market activity, such as housing prices…

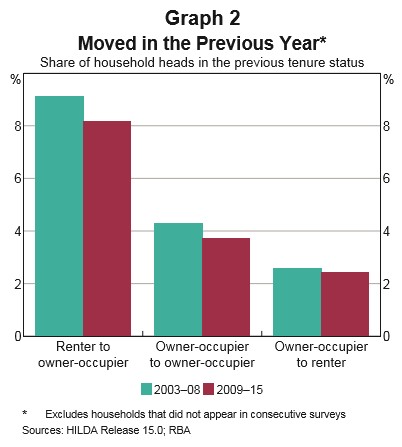

While the reasons for moving have not changed much over time, the HILDA Survey shows that households are moving less often than they were in the early 2000s (Graph 2).

The largest declines in moving frequencies that involve the transfer of ownership have been for renters transitioning to owner-occupiers and then owner-occupiers moving between dwellings…

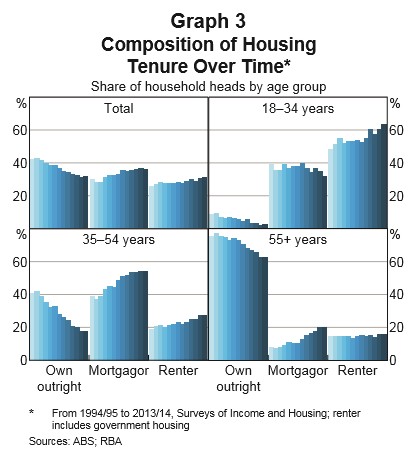

Data from the ABS Survey of Income and Housing show a small increase in the aggregate share of renter households, driven largely by households with a household head aged under 55 years (Graph 3). All else being equal, a larger proportion of renter households would be expected to reduce housing turnover…

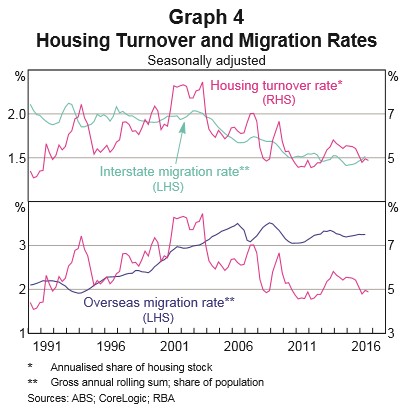

The decline in the turnover rate since the early 2000s appears to have been associated with a significant decline in the rate of gross interstate migration (Graph 4)…

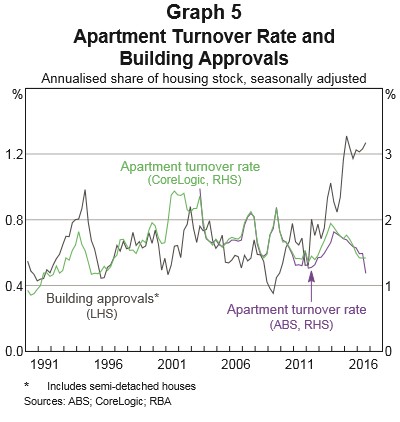

The decline in the national housing turnover rate in recent years has occurred despite strength in a number of housing market indicators such as national housing price growth, which has historically been positively correlated with the turnover rate… part of the recent weakness could be due to measurement issues arising from the increased share of apartments in new housing construction. Private residential building approvals for higher density housing have increased sharply since 2009 and now account for around half of all approvals (Graph 5). Meanwhile the apartment turnover rate, which has historically moved in line with building approvals, has declined…

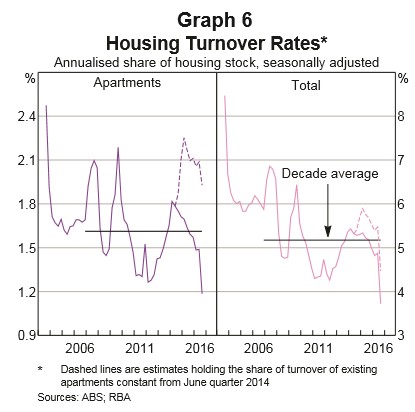

This seems unlikely, suggesting that total apartment turnover is understated. We can estimate the effect of the understatement by adjusting existing apartments’ share of turnover to more reasonable levels. For example, keeping the share constant from the June quarter 2014 (at around 18 per cent) and scaling up the volume of total turnover implies that the actual turnover rate may be around ½–¾ percentage point higher than reported over this period (Graph 6)…

Implications for economic activity:

Developments in the rate of housing market turnover can affect broader economic activity through several channels. A number of occupations are involved in housing transactions; these include real estate agents, lawyers and finance professionals…

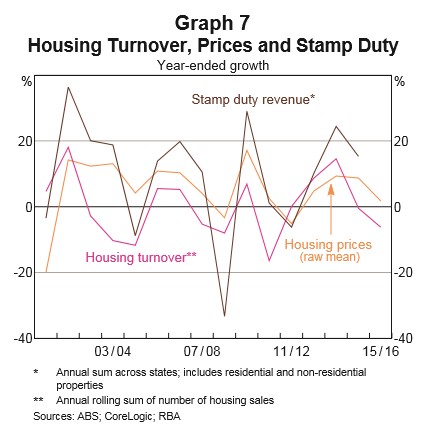

Housing turnover also affects property tax revenue, which accounted for about 40 per cent of total state tax revenue in 2014/15… All else being equal, a decline in the number of housing transactions would be expected to reduce stamp duty revenue. However, given that stamp duty is calculated as a proportion of the sale price of the property, strong growth in national housing prices can more than offset a decline in turnover, as occurred in 2014/15 (Graph 7)…

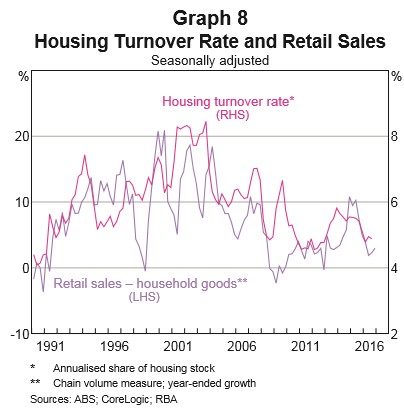

Housing turnover can have a number of indirect effects on household spending. For example, housing turnover is positively correlated with household retail spending, particularly on durable goods such as furniture, home appliances and electrical or electronic devices (Graph 8). Renovation activity is another channel through which housing turnover can indirectly affect household spending, as new owners might choose to modify homes to suit their needs or existing owners might renovate to add value to their home before listing. Renovation activity would also be expected to have flow-on effects for activity in the construction industry.

Another indirect channel through which housing market turnover can affect economic activity is housing prices. A common feature of housing markets in advanced economies is a positive correlation between housing price growth and turnover. One strand of literature posits that changes in housing turnover can lead changes in housing prices… Changes in housing prices can subsequently affect household consumption via the household wealth channel…

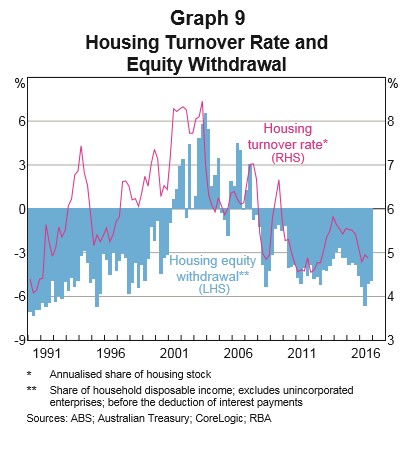

Higher rates of housing turnover have been associated with periods of housing equity withdrawal, which indicates an excess of mortgage borrowing over new investment in housing, and was seen in Australia for much of the early to mid 2000s (Graph 9)… Relatedly, lower rates of housing turnover will tend to increase the average age of housing loans and the level of mortgage buffers. Households with newer or larger mortgages have had less time to build up buffers…

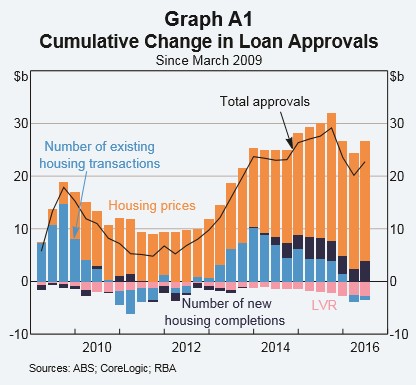

There is a close relationship between housing market turnover and the total amount borrowed to purchase residential property… turnover of existing housing has been an important driver of trends in loan approvals since 2009 (Graph A1)…

Over the past two years, its contribution to new housing finance has been declining. Over the same period, housing prices have been making a large contribution to growth in housing finance. The decline in turnover of existing housing goes some way to explaining why housing credit growth has been relatively muted, despite rapidly rising housing prices.

Housing shrinkflation is clearly bad news for the economy. Not only do sectors exposed to turnover take a hit (think real estate agents and mortgage lenders), but so does household consumption and state revenues. Moreover, with folks unable or unwilling to shift home, participation rates in the labour market fall as sclerosis eats away at market flexibility.

Basically, the Australian property bubble is now so absurdly large, so ludicrously dependent upon policy distortions and Coalition carpet-baggers, so hilariously dislocated from the sad little economy beneath it, that even traditional beneficiaries of such booms – like the banks and real estate agents – are now shivering in its titanic shadow. Just as McGrath Real Estate.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.