Market demand sentiment recently weakened, which caught investors by surprise; normally this time of year demand picks up alongside construction activity.

• Current demand for steel and iron ore is not as strong as expected in view of lofty expectations

• Most industry operators are unsure of the overall outlook

Iron ore prices will continuously be driven by the NDRC policy. The NDRC capacity cuts last year not only impacted the coal industry but also iron ore.

For this year, uncertainty remains ongoing pertaining to further coal capacity reforms.

For the second half of the year, our trader contact is not too pessimistic on iron ore and steel prices. Demand for iron ore and steel should remain stable.

• The government is very likely to continue stimulating the economy to support GDP growth

• On account of China’s political transition in September, the government aims to avoid any major economic surprises

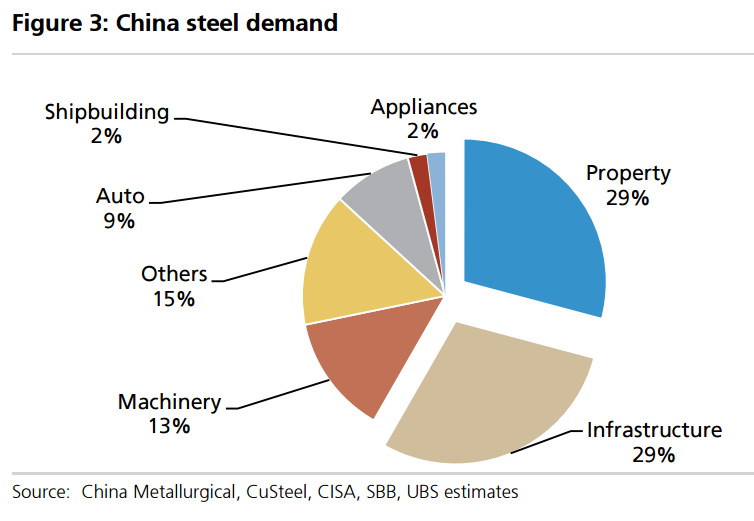

Is demand strength driven by infrastructure or property?

Infrastructure plays a bigger role now as even the government expects lower property spending.

• For every 1% drop in property investment, the industry needs 2% of infrastructure spending to offset it

• The problem with infrastructure investment this year is y/y growth is from an already high base

However, property investment may not drop as much as industry operators expect.

What is 2018 view post political transition?

It is not clear as it depends on the political outcome.

It seems there is a conflict between top two government official figures in China.

Stimulus will eventually fade and be replaced by government reforms.

So far, there have been limited reforms; only stimulus.

After the political transition, there will be one person in charge which should help get things done faster. However, it is unclear if the top official will have the determination to implement key reforms.

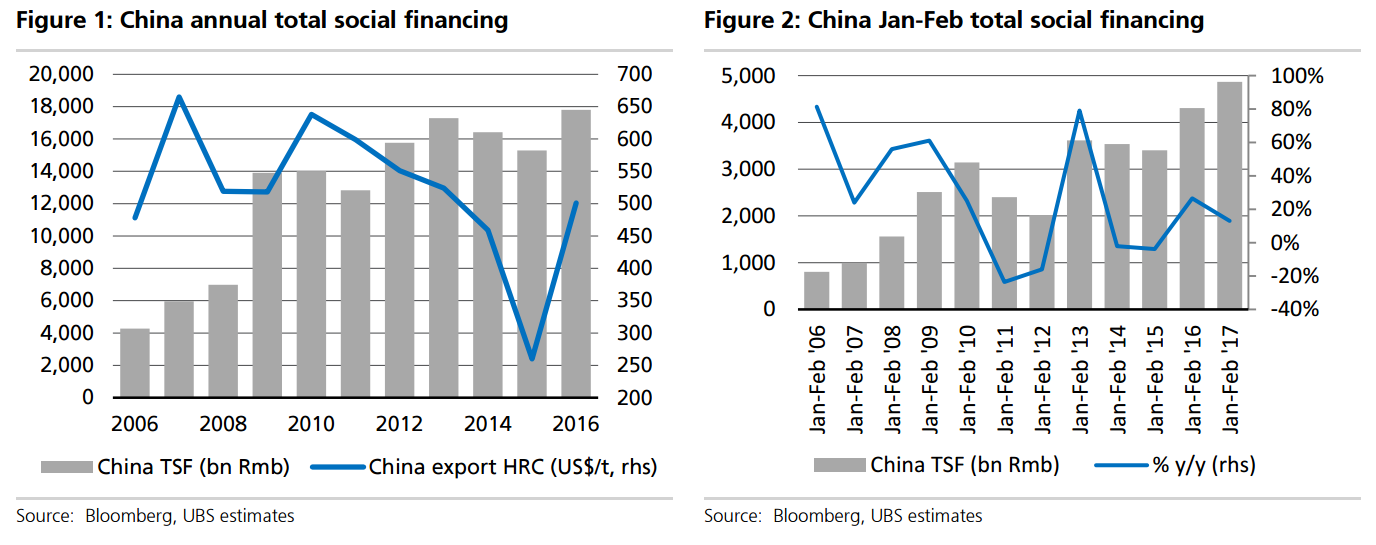

The government has been very unpredictable over the past few years. Our contact did not expect the government to stimulate so much, but over the last few months the stimulus program has been even bigger than 2009 (see charts on previous page).

Is speculation part of recent price support?

The NDRC is the primary driver of steel, iron ore and met coal prices. That is the one responsible for surge of commodity prices this past year.

Government capacity cuts likewise caused the price of coke to increase.

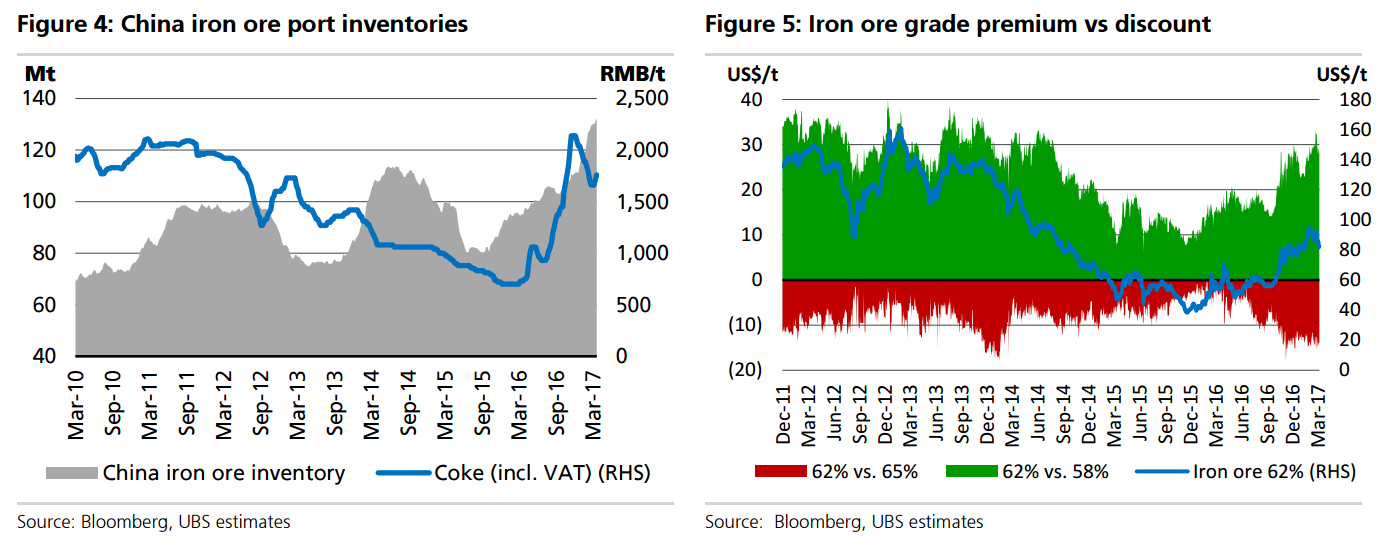

What is the update on rising iron ore inventories?

When the coke price is high, most steel mills will limit the use of low-grade iron ore as it is less economical in the sintering process (as mills need to consume a higher amount of coke at currently high prices).

Steel mills did not have sufficient supply of high-grade iron ore this year and subsequently bid up prices

• The coke price incentive price to use low grade iron ore is ~RMB 1,200/t from currently ~RMB 1,800/t.

• In order to accelerate port destocking, either 1) coke prices correcting another 30% to Rmb1,200/t; or 2) low-grade iron ore prices to decline further.

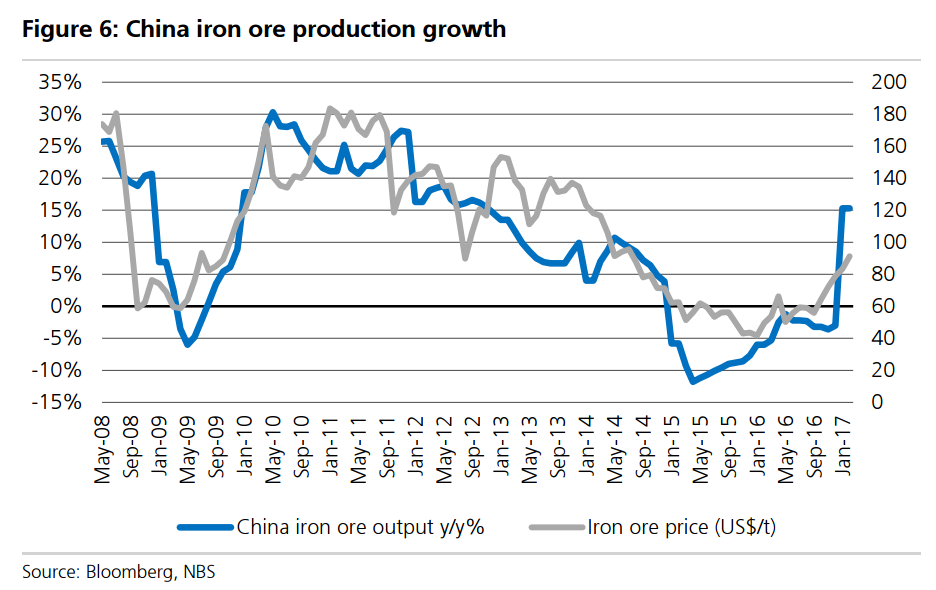

How is Chinese iron ore production tracking?

They were slow to ramp up over the past 12-months during the rally. But many have started up this year and many more are currently starting up.

Last month, customers in China were sintering domestic concentrates as high as 50% which is surprising.

At currently high iron ore prices right now, all mines are doing their best to restart production. Supply is coming online quickly. There is a risk 2017 domestic output doubles (on an annualised basis) compared to last year.

Hence, the steel price outlook remains better than the iron ore outlook.

What is the latest update on steel capacity closures?

Our contact believes steel capacity closures have remained limited in recent years.

Local governments are doing their best to protect the steel mills and restart idled furnaces

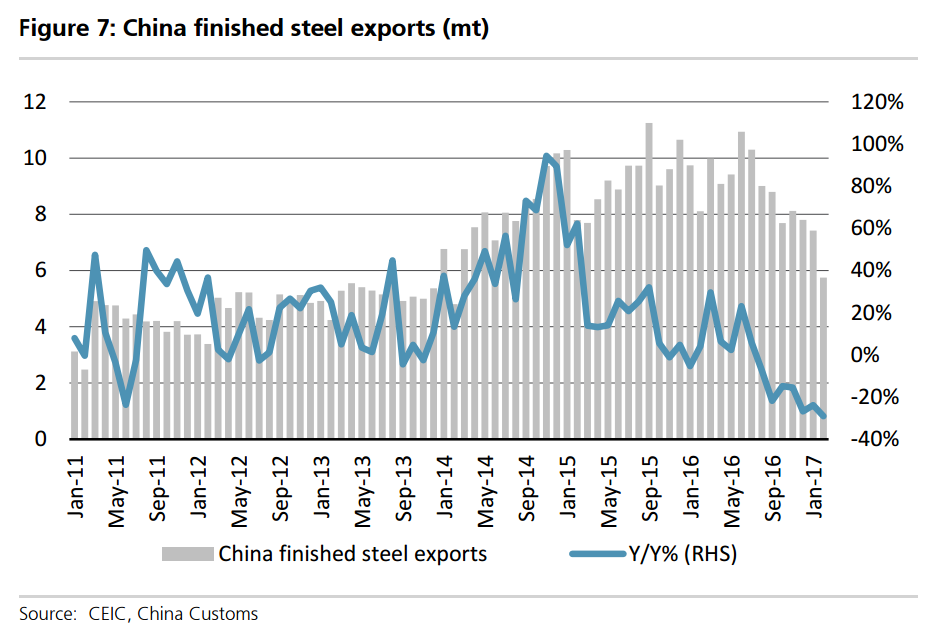

Will Chinese steel exports regain momentum?

No, they will continue to drop until they are incentivized to export via higher prices versus domestically.

Currently, it makes perfect sense for the mills to sell to sell domestically as domestic prices are higher and as it takes longer to collect payment from exports customers.

A few comments:

the stimulus may big in yuan terms versus 2009 but it’s nowhere near it percentage terms;

not much point in asking Banana Man if speculation is playing a role in prices is there?

if Chinese output jumps then prices will fall so prices are going to fall before year end;

Chinese steel exports will rebound as the price falls but the peak is well and truly in;

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.