DXY marched again last night:

Not even a fading yuan could save commodity currencies:

Or gold:

Or oil:

Or base metals:

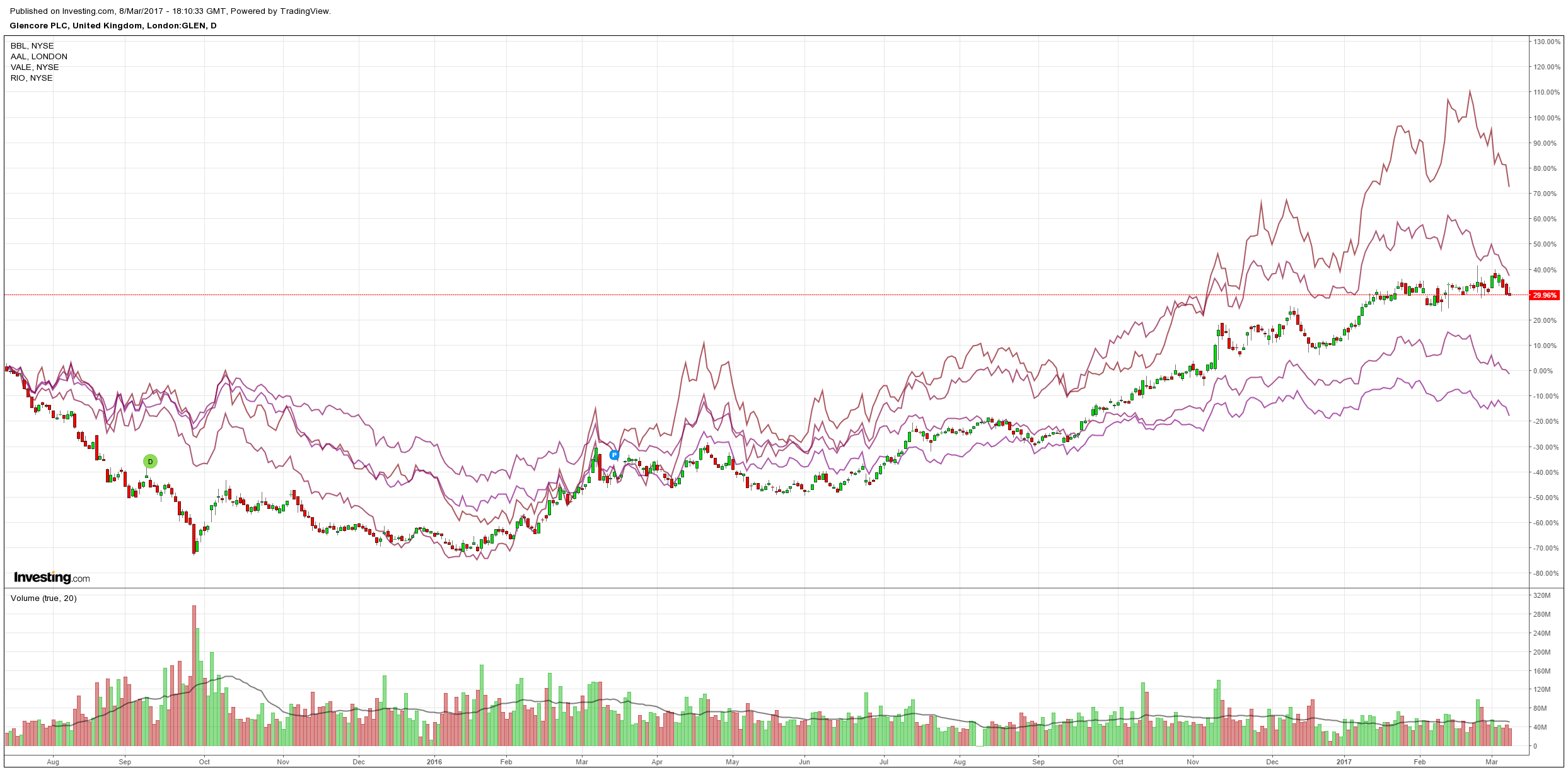

Or big miners:

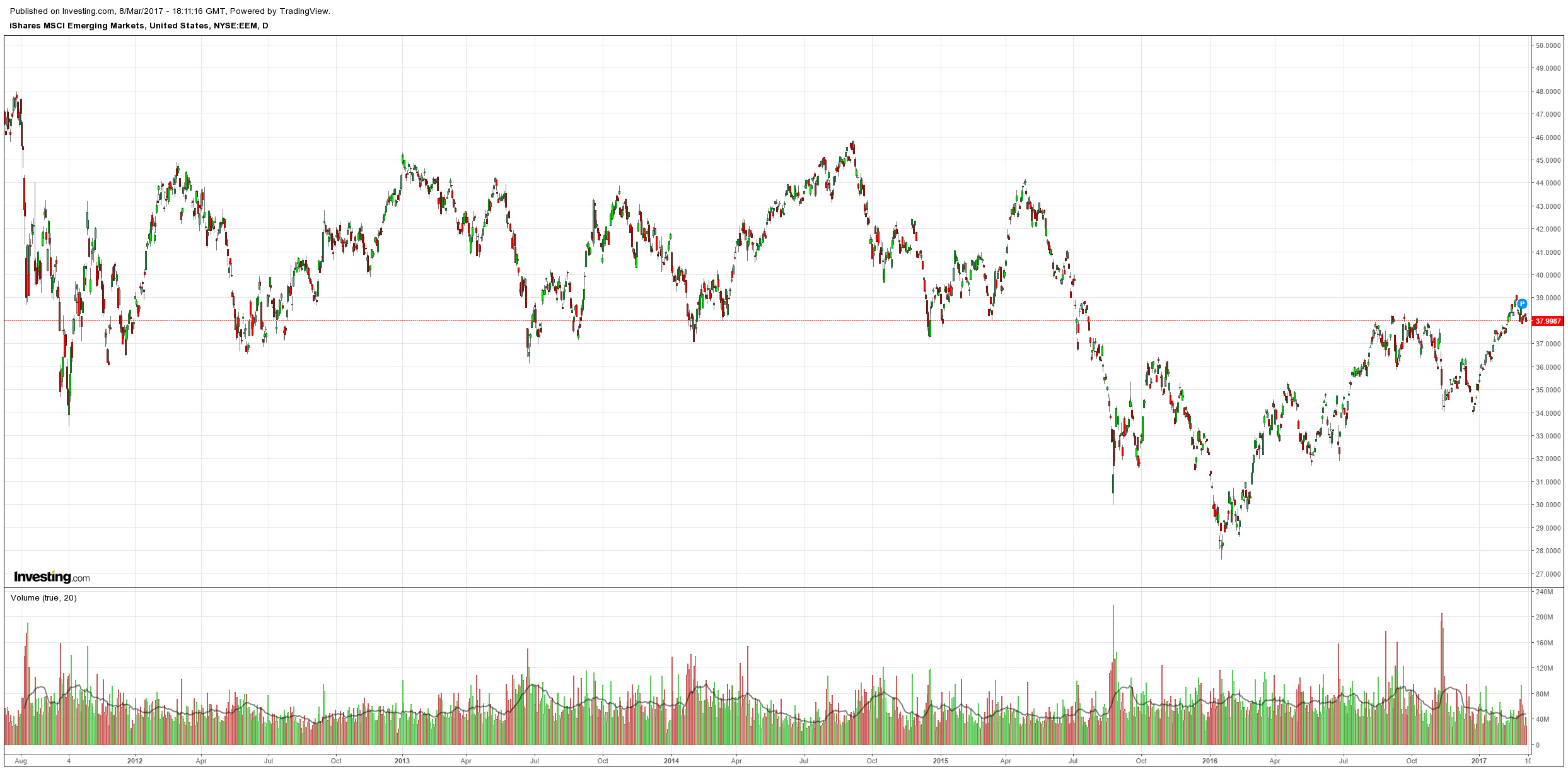

Or EM stocks:

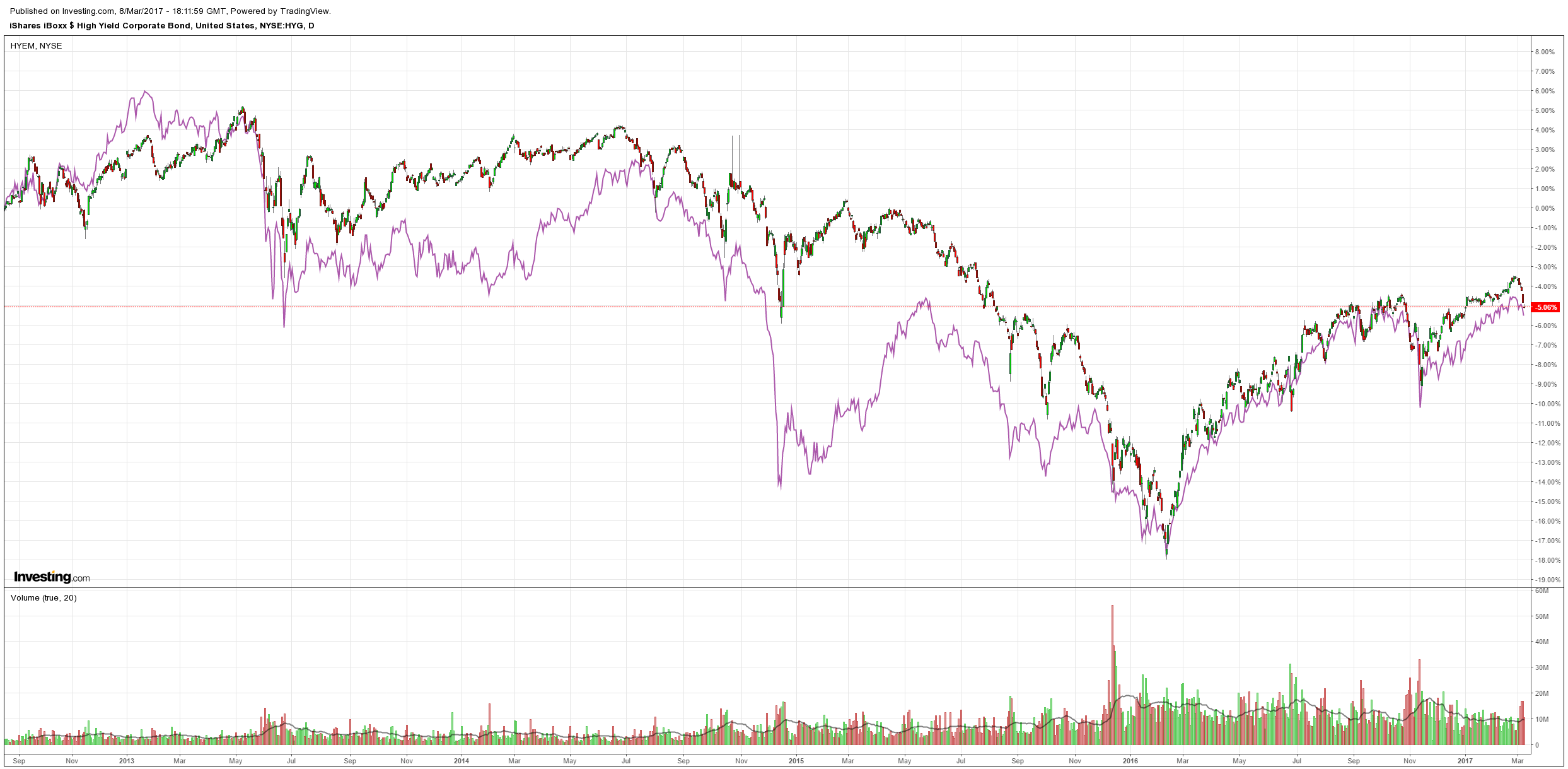

Or high yield:

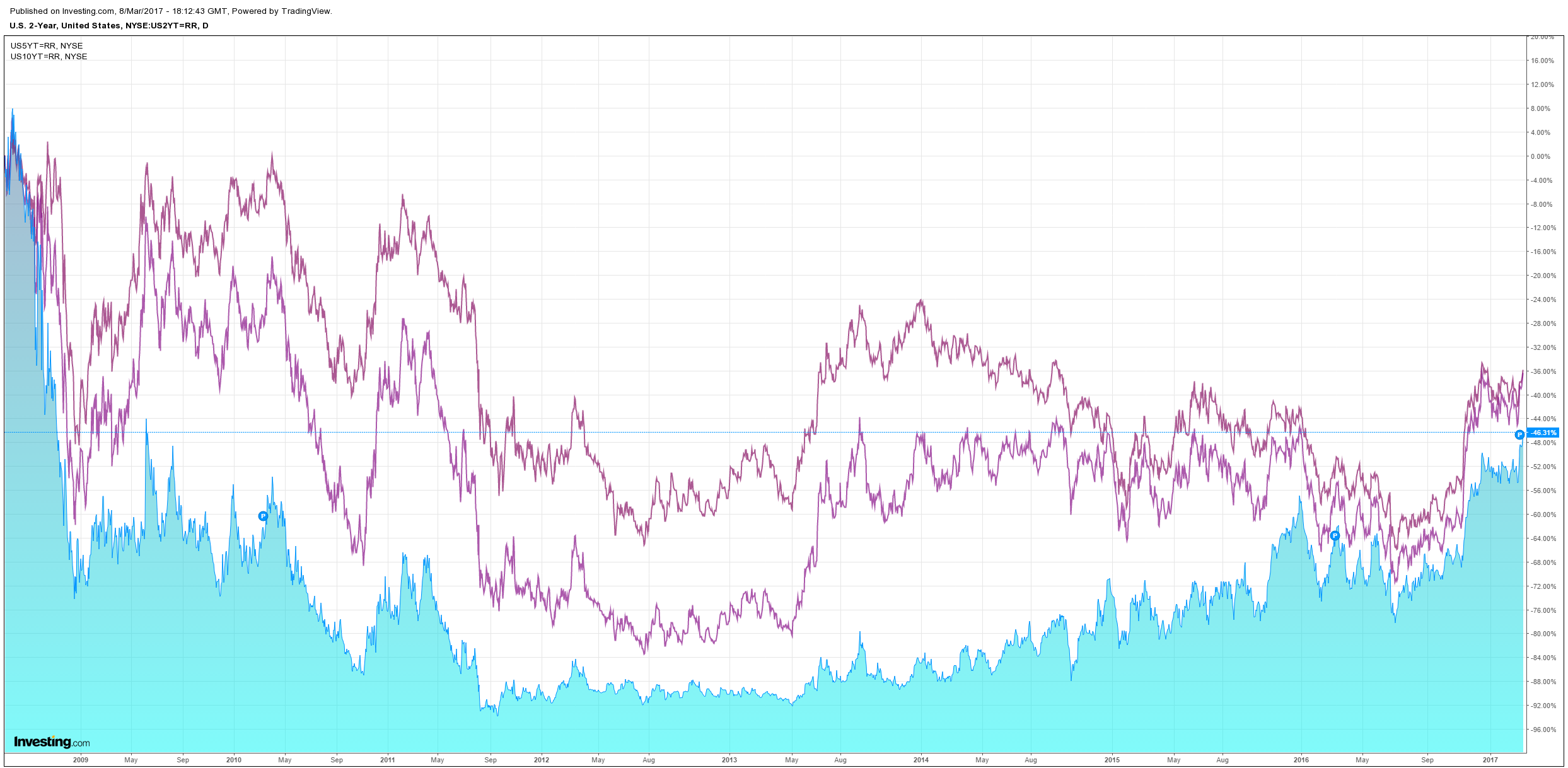

US bonds were flogged:

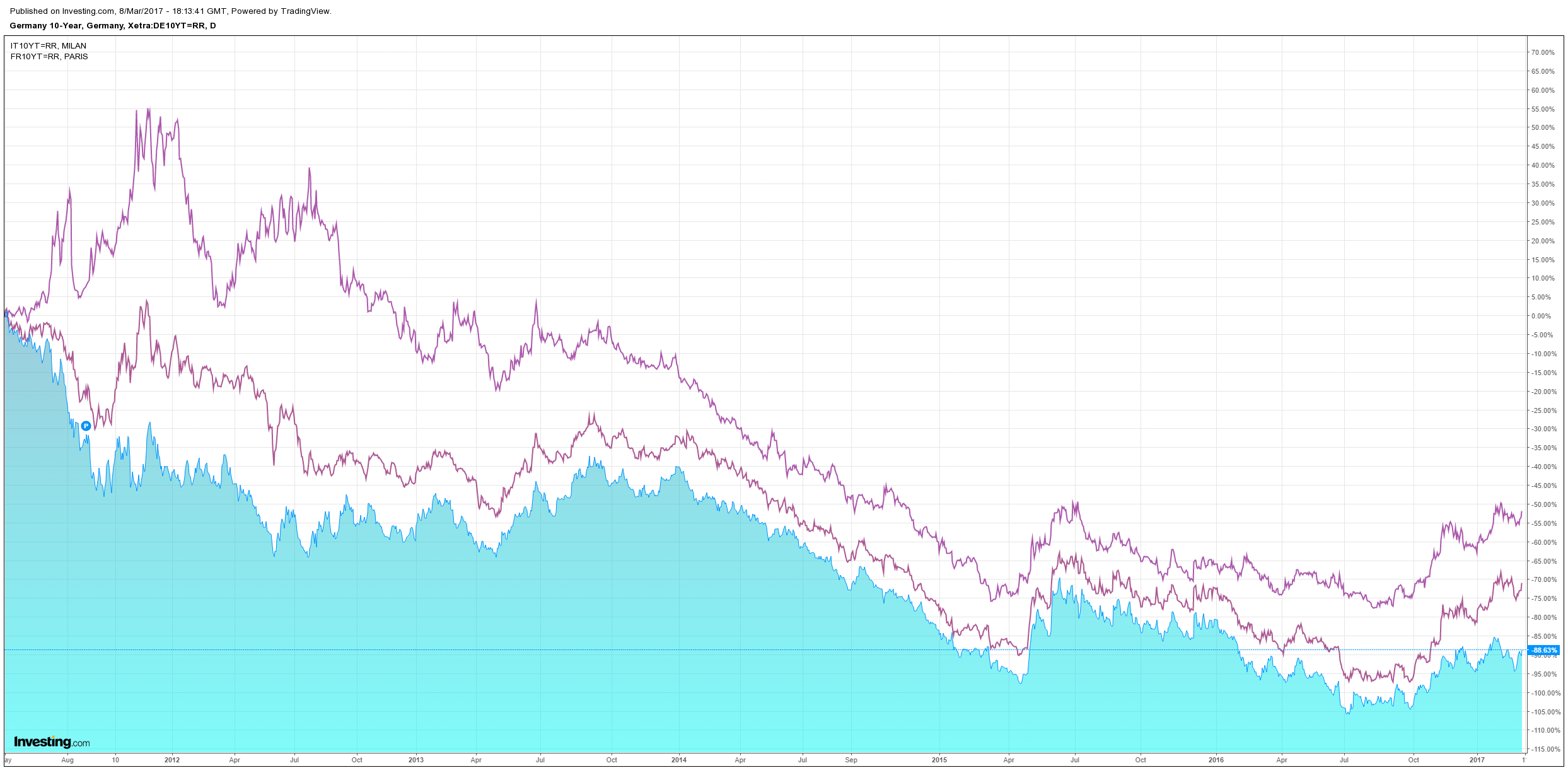

European spreads widened:

And stocks rebounded:

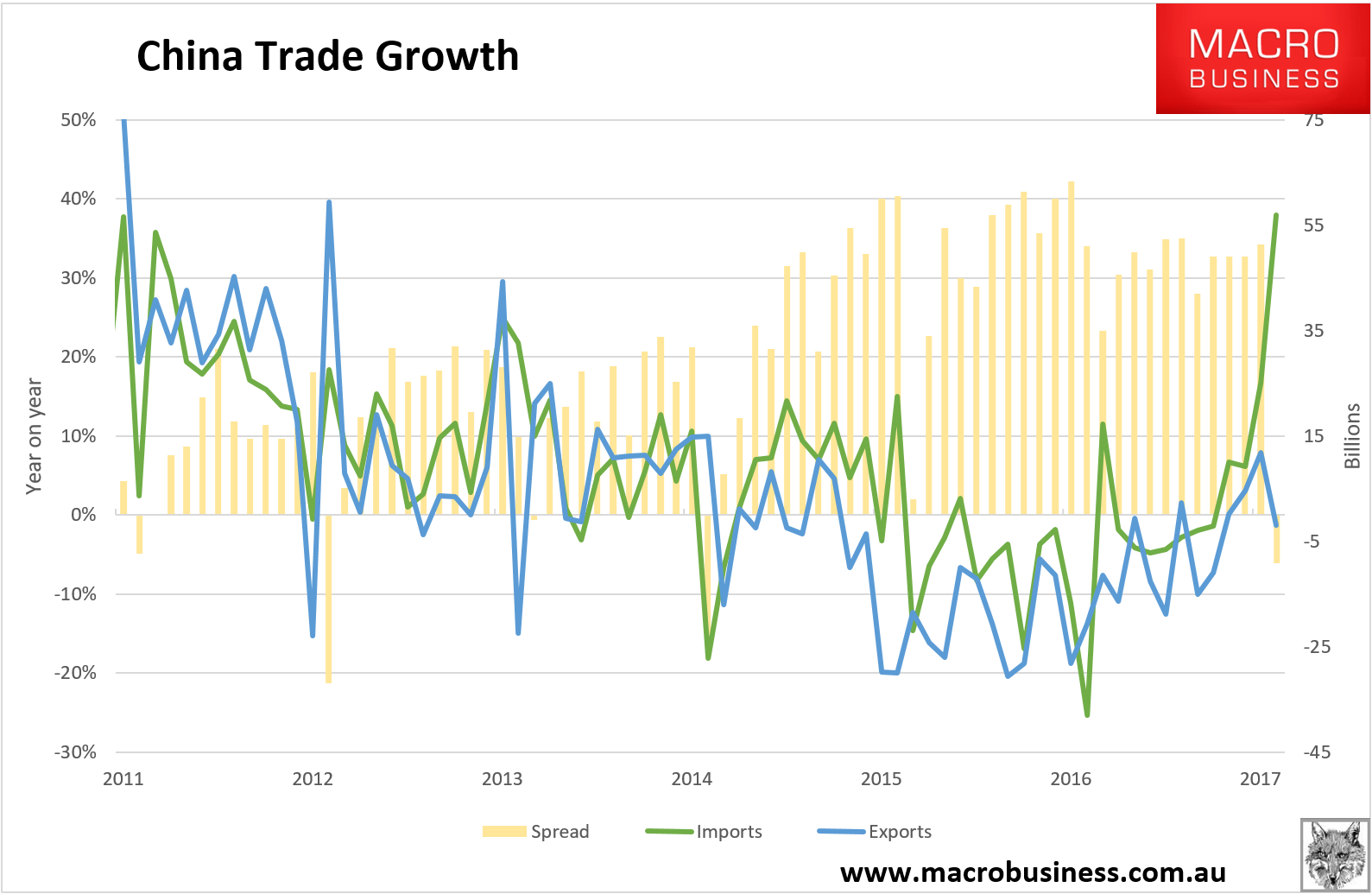

That cracking sound you can hear is the entire commodities complex as global reflation takes a back seat to US reflation. The trigger was twofold. Chinese trade data was pretty ordinary and its swing to deficit shows just how quickly the commodities bubble has wrecked its external position. Anyone thinking that China is not concerned about this is wrong. It will reverse it whichever way it can without derailing growth, hence futures markets investigations, no more coal output cuts etc:

The second, even larger trigger, is a looming US jobs report that is giving off good signals. The ADP was a ripper:

Private sector employment increased by 298,000 jobs from January to February according to the February ADP National Employment Report®. … The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.

“February proved to be an incredibly strong month for employment with increases we have not seen in years,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “Gains were driven by a surge in the goods sector, while we also saw the information industry experience a notable increase.”

Mark Zandi, chief economist of Moody’s Analytics said, “February was a very good month for workers. Powering job growth were the construction, mining and manufacturing industries. Unseasonably mild winter weather undoubtedly played a role. But near record high job openings and record low layoffs underpin the entire job market.”

Calculated Risk goes on:

The consensus, according to Bloomberg, is for an increase of 195,000 non-farm payroll jobs in February (with a range of estimates between 168,000 to 215,000), and for the unemployment rate to decline to 4.7%.

The BLS reported 227,000 jobs added in January.

Here is a summary of recent data:

• The ADP employment report showed an increase of 298,000 private sector payroll jobs in February. This was well above expectations of 183,000 private sector payroll jobs added. The ADP report hasn’t been very useful in predicting the BLS report for any one month, but in general,this suggests employment growth above expectations.

• The ISM manufacturing employment index decreased in February to 54.2%. A historical correlation between the ISM manufacturing employment index and the BLS employment report for manufacturing, suggests that private sector BLS manufacturing payroll increased about 3,000 in February. The ADP report indicated 32,000 manufacturing jobs added in February.

The ISM non-manufacturing employment index decreased in February to 55.2%. A historical correlation between the ISM non-manufacturing employment index and the BLS employment report for non-manufacturing, suggests that private sector BLS non-manufacturing payroll jobs increased about 212,000 in February.

Combined, the ISM indexes suggests employment gains of about 215,000. This suggests employment growth above expectations.

• Initial weekly unemployment claims averaged 234,000 in February, down from 248,000 in January. For the BLS reference week (includes the 12th of the month), initial claims were at 244,000, up from 237,000 during the reference week in January.

The increase during the reference suggests slightly more layoffs during the reference week in February than in January. This suggests an employment report close to January – above the consensus.

• The final February University of Michigan consumer sentiment index decreased to 96.3 from the January reading of 98.5. Sentiment is frequently coincident with changes in the labor market, but there are other factors too like gasoline prices and politics.

• Conclusion: Unfortunately none of the indicators alone is very good at predicting the initial BLS employment report. However the ADP report and ISM surveys suggest stronger job growth. Weekly unemployment claims suggest job growth similar to January. So my guess is the February report will be above the consensus forecast.

Looks that way to me too. That’s why bond yields are flying, the USD roaring, and hard assets stinking it up.

My guess is that this is the pattern that will dominate global markets in H2, thus allocations remain:

- buy the dips in the USD and S&P500;

- sell rallies in the AUD and commodities;

- buy dips in short end Aussie bonds;

- buy dips in gold for portfolio protection;

- sell property!