The USD was weak last night after possible delays to Trump stimulus:

Commodity currencies roared:

Gold launched:

Advertisement

Brent fell back:

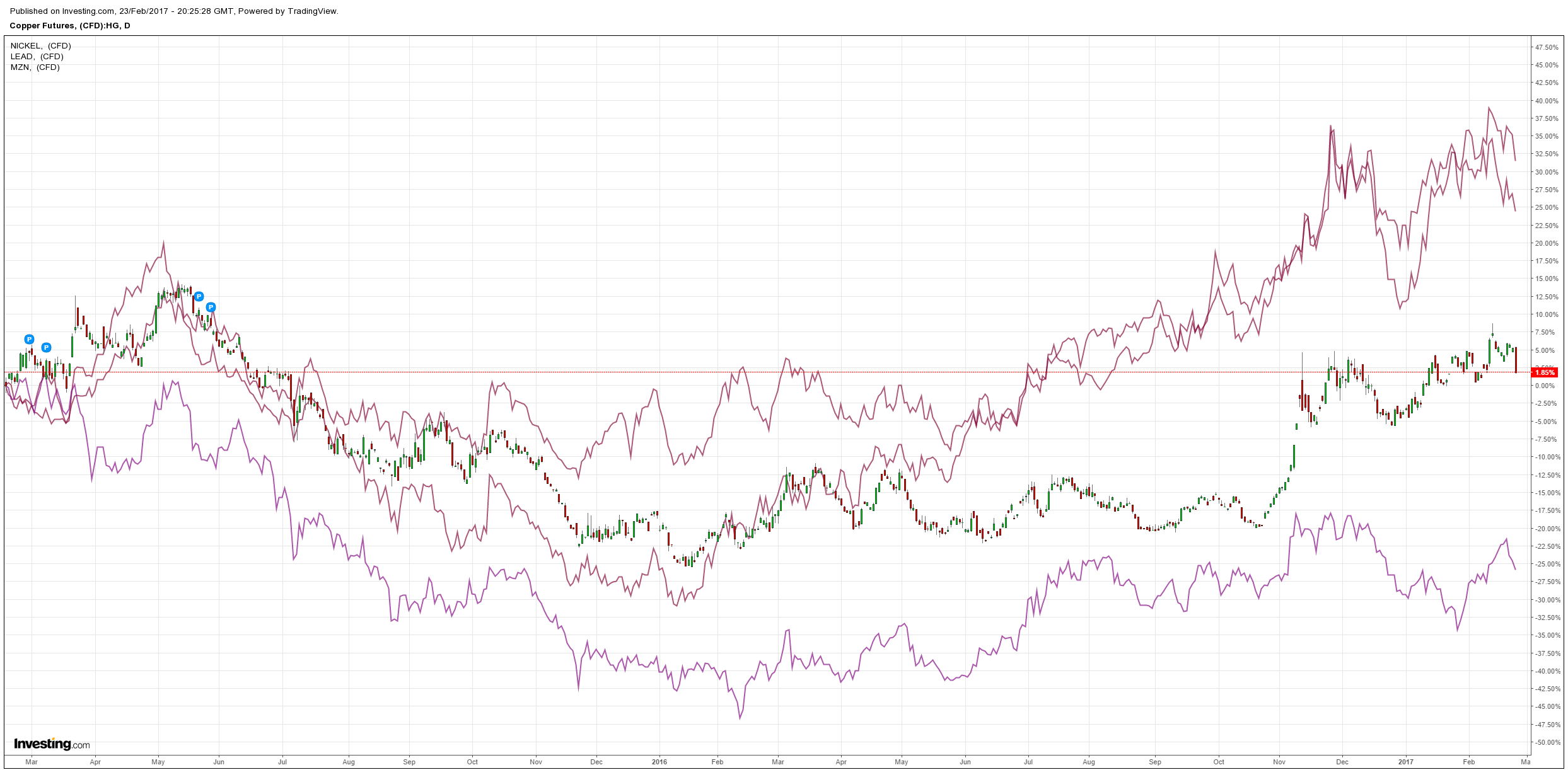

Base metals were hit:

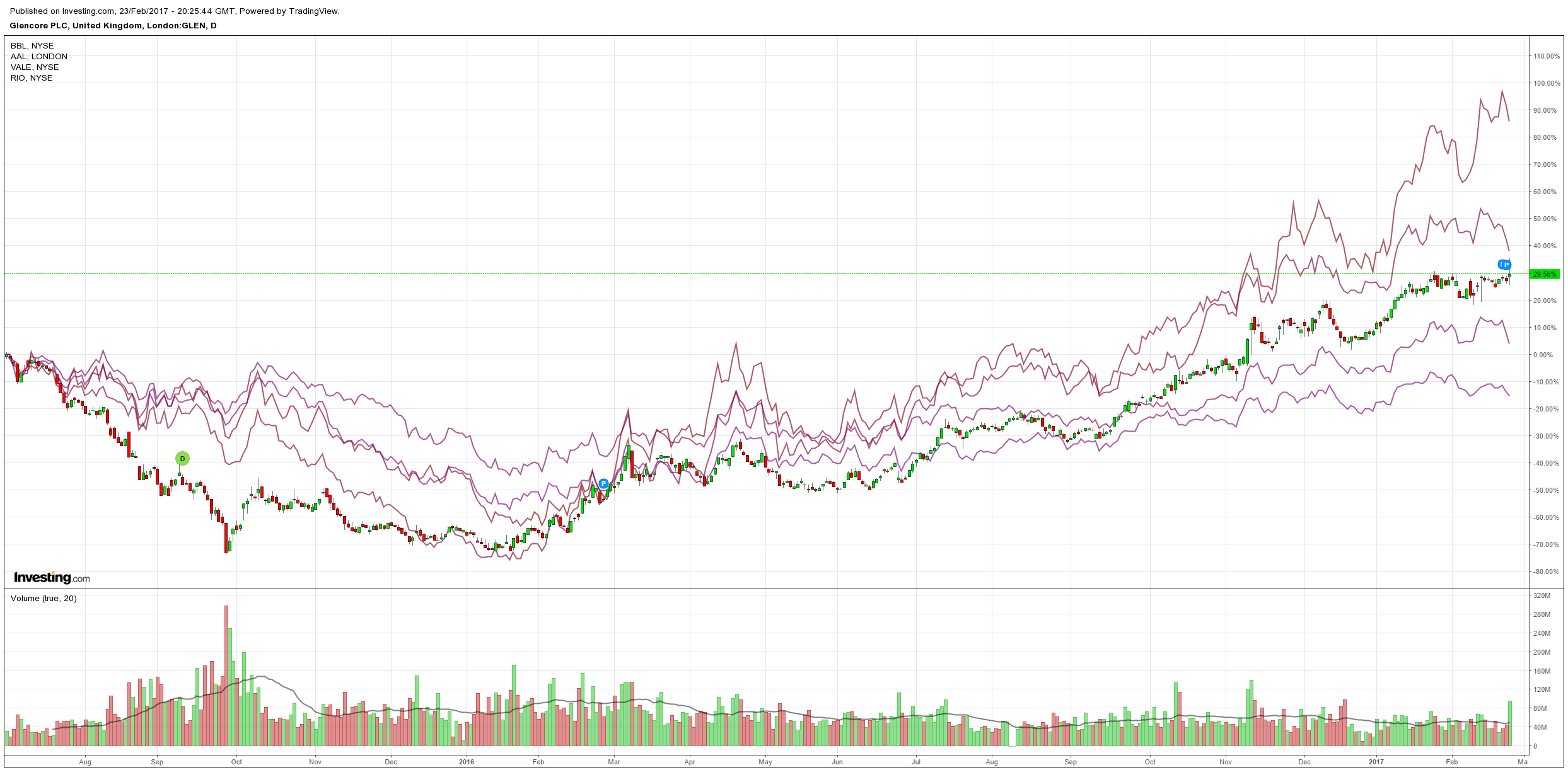

Big miners thumped:

Advertisement

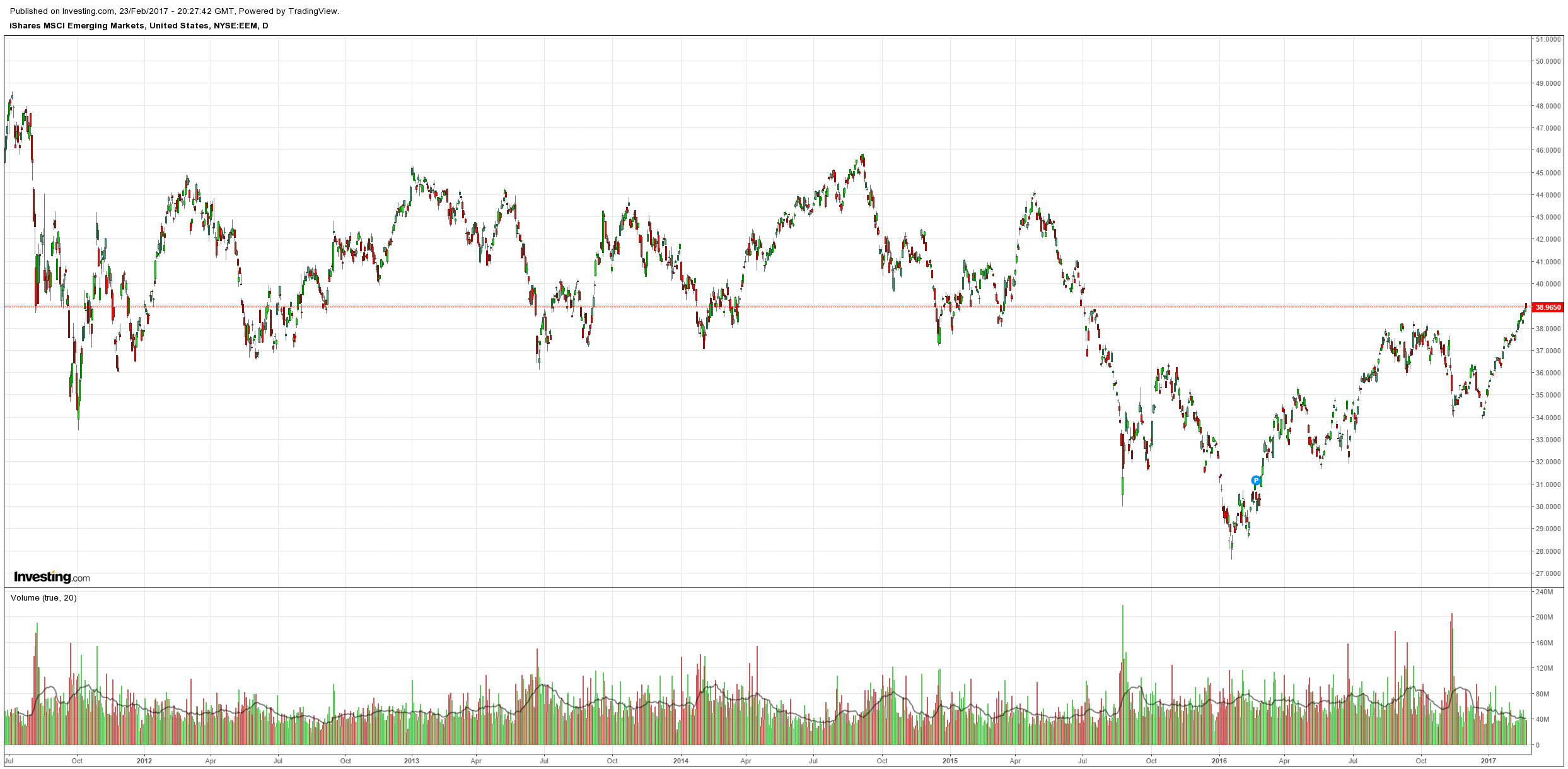

EM stocks reversed:

And high yield debt:

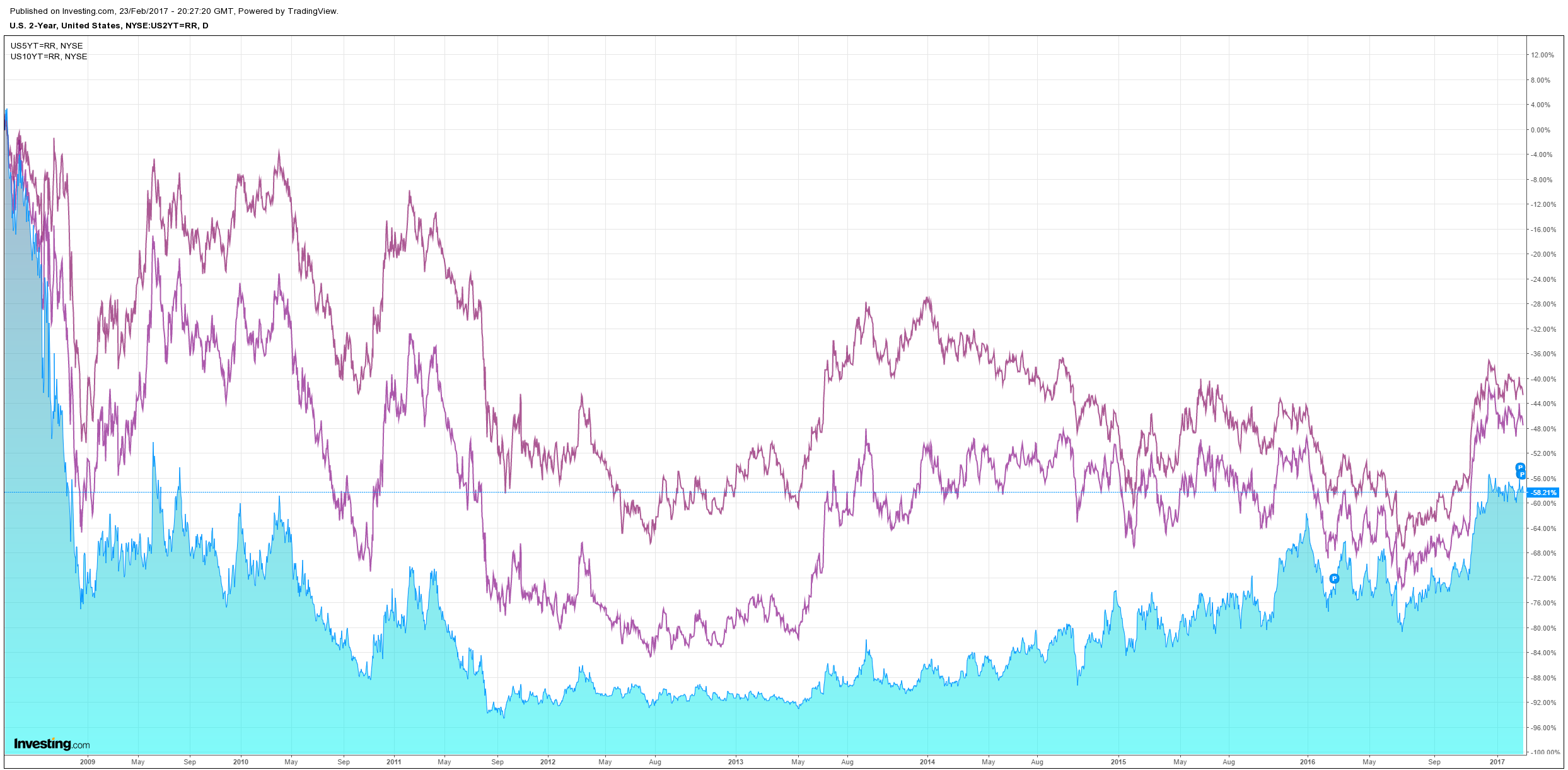

US bonds were bought:

Advertisement

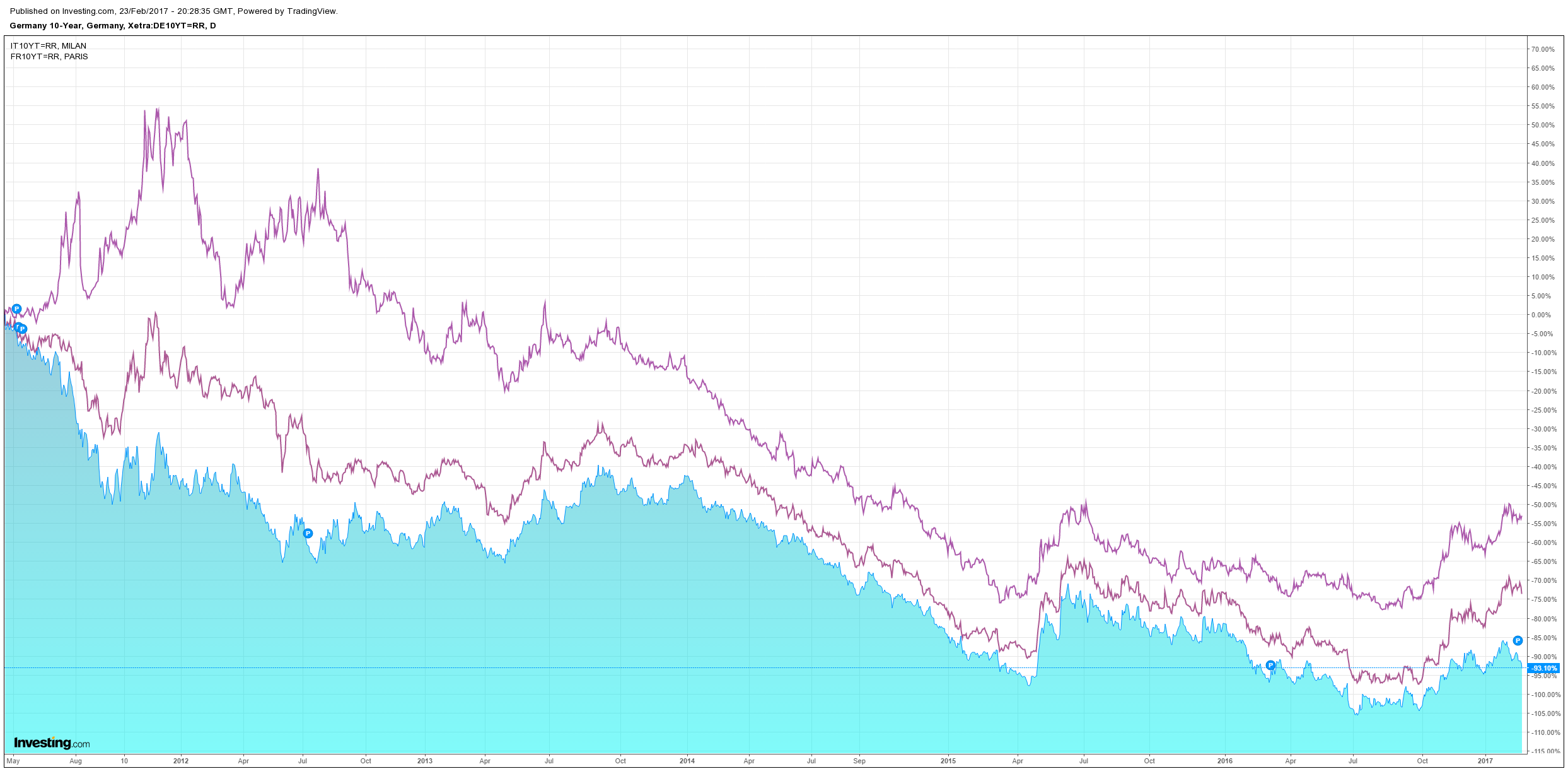

European spreads tightened:

And stocks still eked out new highs:

Clearly Trumpflation is hitting turbulence. The reasons are pretty obvious:

Advertisement

Chinese housing is a lead indicator for slowing;

valuations are very high in the US, and

we’re entering European election season.

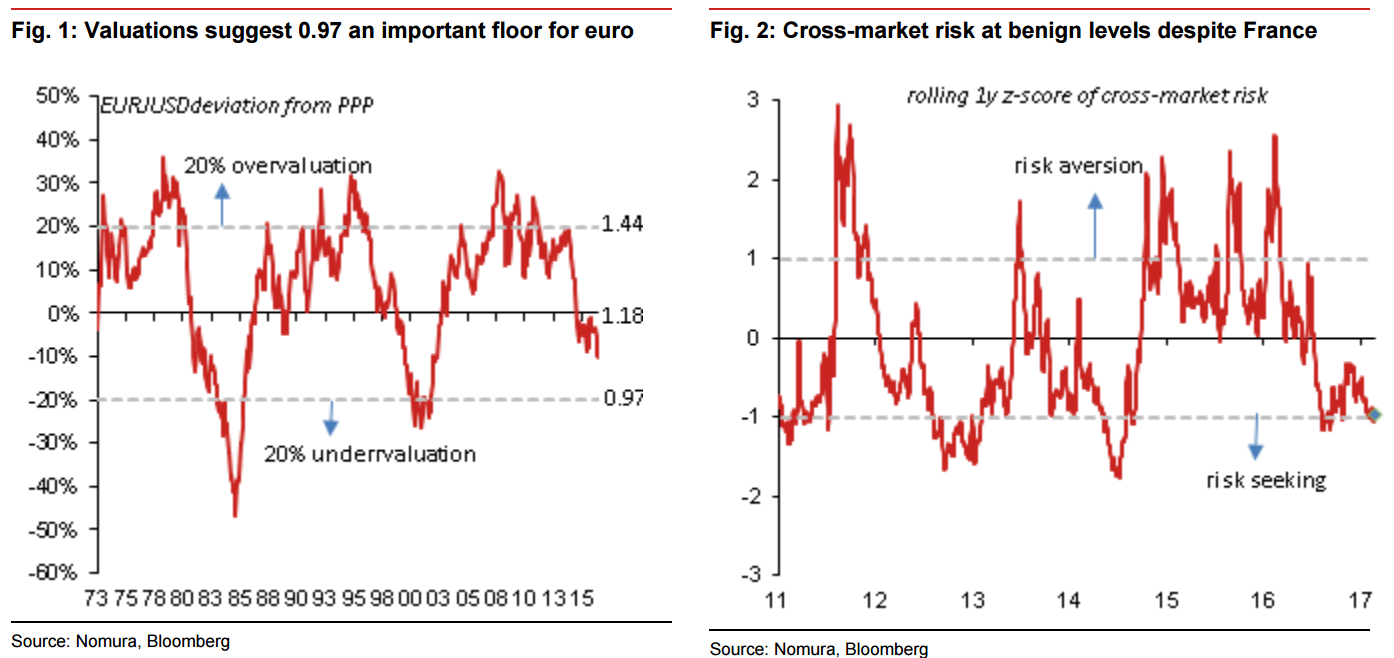

Nomura has more on the last:

We have been doggedly bearish on the dollar since the start of the year, but we have been avoiding buying the euro for concerns that the coming elections in the Netherlands and particularly France would weigh on it. Recent weakness in the euro due in part to polls suggesting more support for Marine Le Pen, the anti-EU candidate, has justified this caution. However, while she could win the election, our bias is still for her to lose, and so we would be hesitant to instigate short euro positions. We could be accused of ignoring the lesson of 2016 (Brexit and Trump) – one key difference is that the French system entails two rounds of voting. So imagine the outcome of last year’s votes if everyone had a second chance to vote some weeks after the shock results. Despite our view on the French election, there are still a few questions to be answered. Three stand out: how low could the euro fall if the fears escalate? Will euro crisis fears derail the global risk rally? What happens if the fears subside?

1. On the first, it is important to note that even if Ms Le Pen becomes president her party is unlikely to have a majority in parliament (the Front National currently only has two seats). Therefore, there would be a question of whether she or parliament has the authority to call a referendum on EU membership which would be up to the courts to decide. So there would be a protracted time period between her win and a referendum (should it come under her purview). This would lessen the “shock” of her victory. Given this, we would defer to currency valuations to determine how low the euro could go. Typically, the euro has fluctuated about 20% around its purchasing power parity value. Currently, the euro is about 10% undervalued – a move to 0.97 would take it to 20% undervalued (Figure 1). This would likely provide the obvious level the euro could settle to in the event of a Le Pen victory.

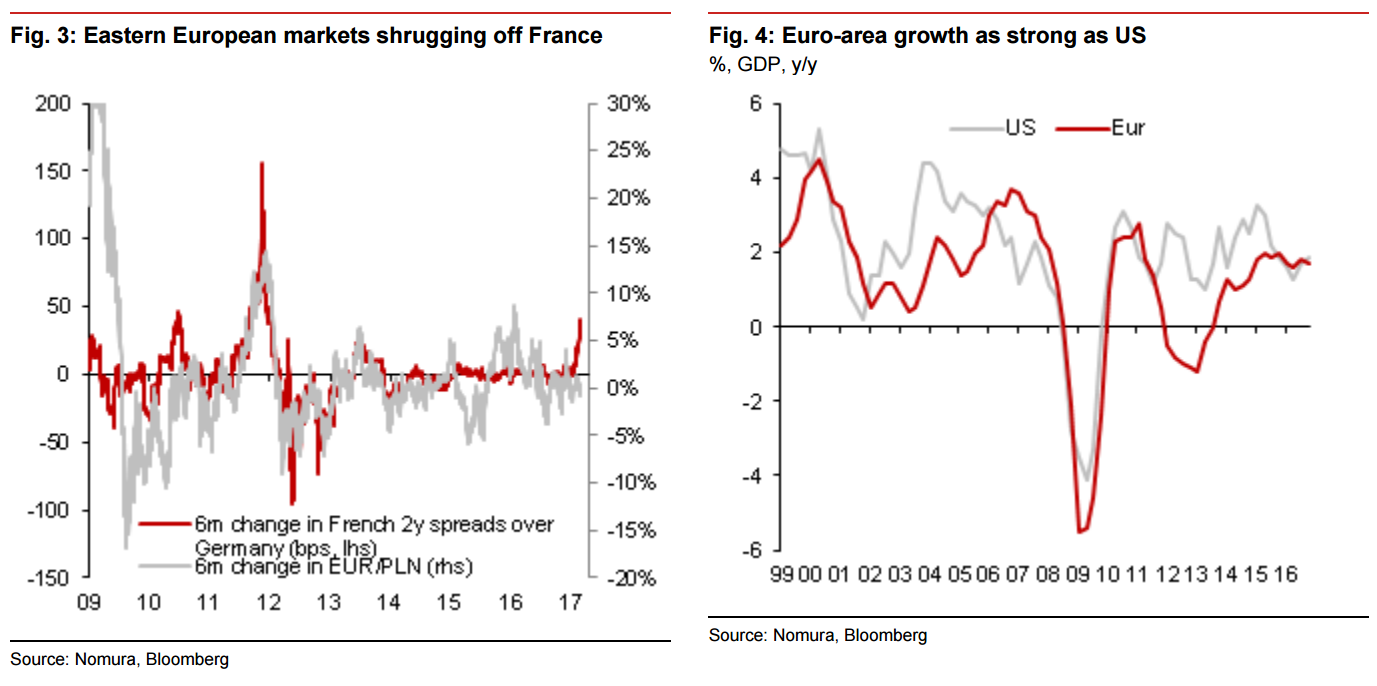

2. As for the second question, it is noteworthy that equity markets, emerging markets and credit are generally performing well despite increasing concerns about France (Figure 2). In the past, an escalating crisis has not always globalised to all markets, but at the very least it affects broader European markets. Typically, a currency like the Polish zloty would suffer if a euro crisis escalates. However, such markets are currently showing no signs of fear (Figure 3). Therefore, this inconsistency will have to be resolved if French fears were to increase.

3. Finally, if our base case of a benign outcome does pass, then this should provide a very constructive picture for the euro. Growth has picked up over the past year such that it is similar to US levels (Figure 4). Headline inflation is almost at the ECB’s 2% target and core inflation is primed to head higher over the course of the year. The ECB, then, will likely signal some form of exit from its QE policy this year. It would mark the first time in years that the ECB and Fed are both heading in the same direction. This should help the euro participate in dollar weakness and head notably higher. That said, French fears could continue to weigh on the euro and could spill over to broader risk aversion. Our short USD/JPY view could be one way of capturing this risk as well as capturing our broader bearish dollar view. Another would be to sell EUR/JPY.

All fair enough. We remain bullish on the USD but any delays in Trump’s fiscal roll out will halt the rally. Moreover, so will a rising euro. The French election is an asymmetric bet so it’s too early to get long Europe but we are preparing for a favourable outcome which would lift everything euro a lot.

Advertisement

So, today, we’re taking some profits in the wildly successful S&P500 long. We remain bullish and in the trade but locking in some big gains as risk rises makes sense. The gains have been so big, so fast that we’ve gone from long to super long so we’ll sell to pull that back to just long.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.