DXY took a breather last night, a little odd given US inflation was strong. Interestingly, yuan has flattened out. Is there a deal with Trump in return for supporting the One China policy?

Commosity currencies roared again. More ot the point, iron ore currencies roared as the the BRL, AUD and ZAR took off:

Advertisement

Gold rose:

Brent held on:

Base metals fell:

Advertisement

Big miners too:

EM stocks have broken out:

EM high yield has not:

Advertisement

US bonds were flogged again:

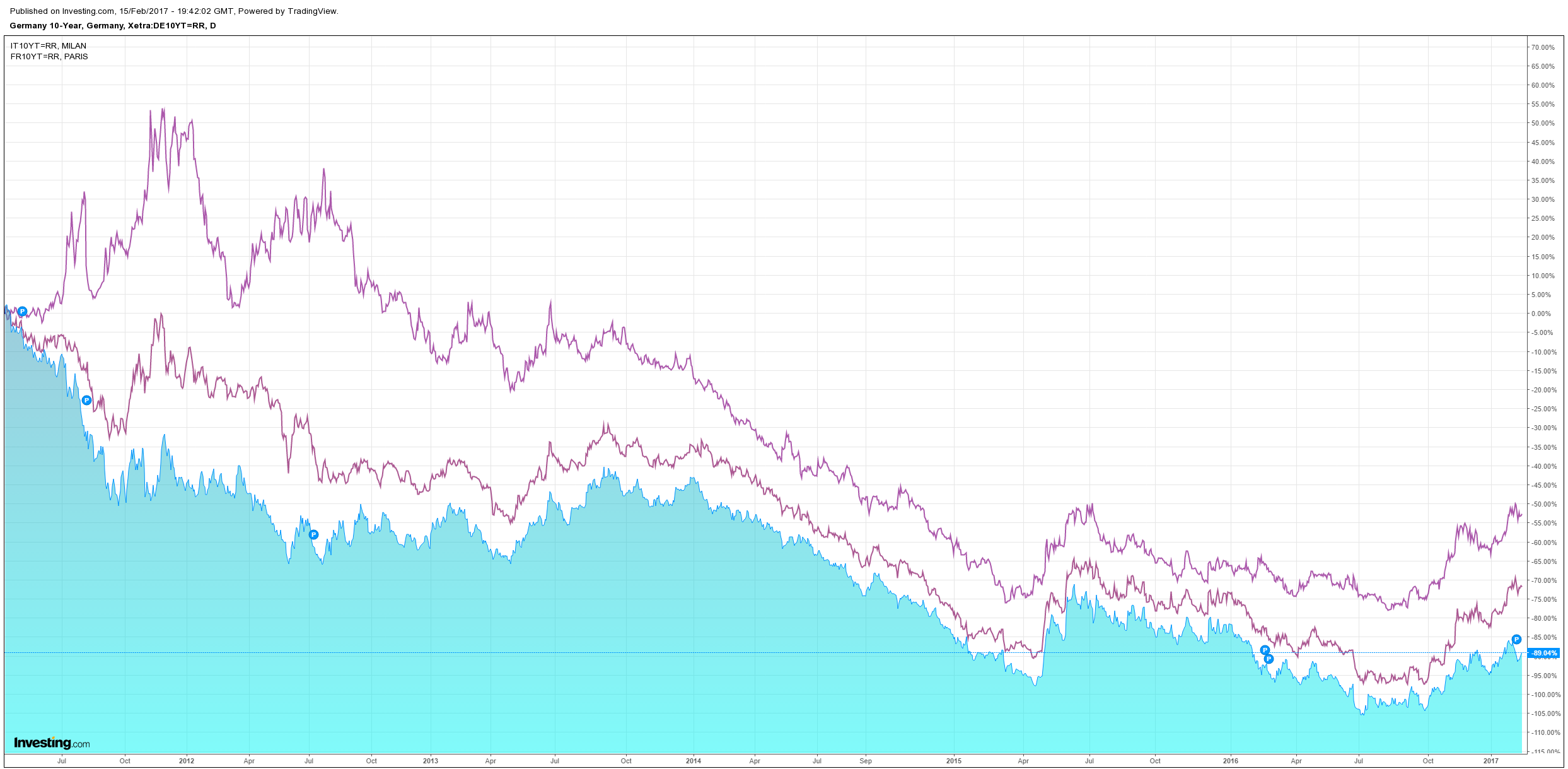

European spreads were stable:

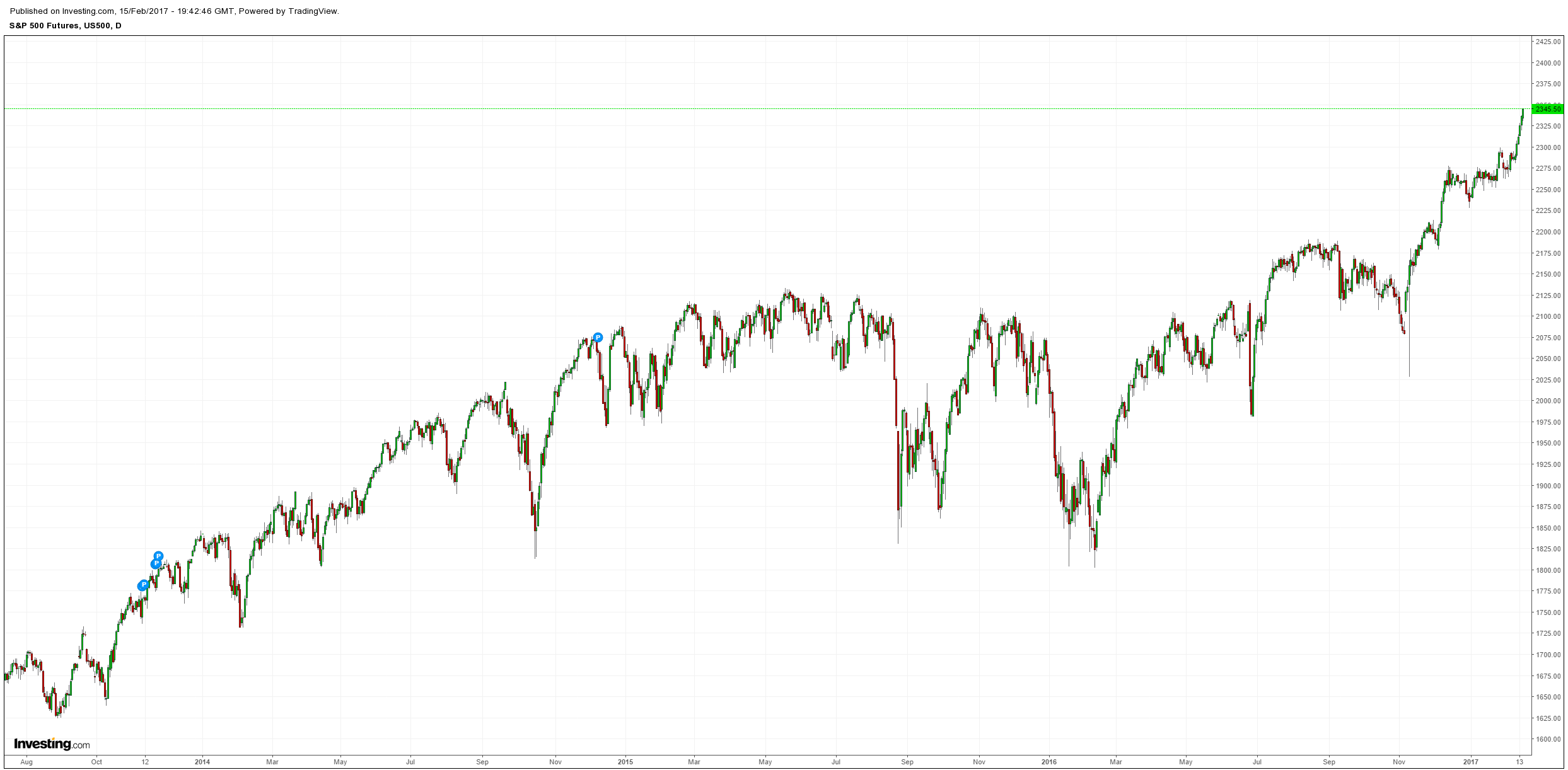

And the S&P bull market keeps on giving:

Advertisement

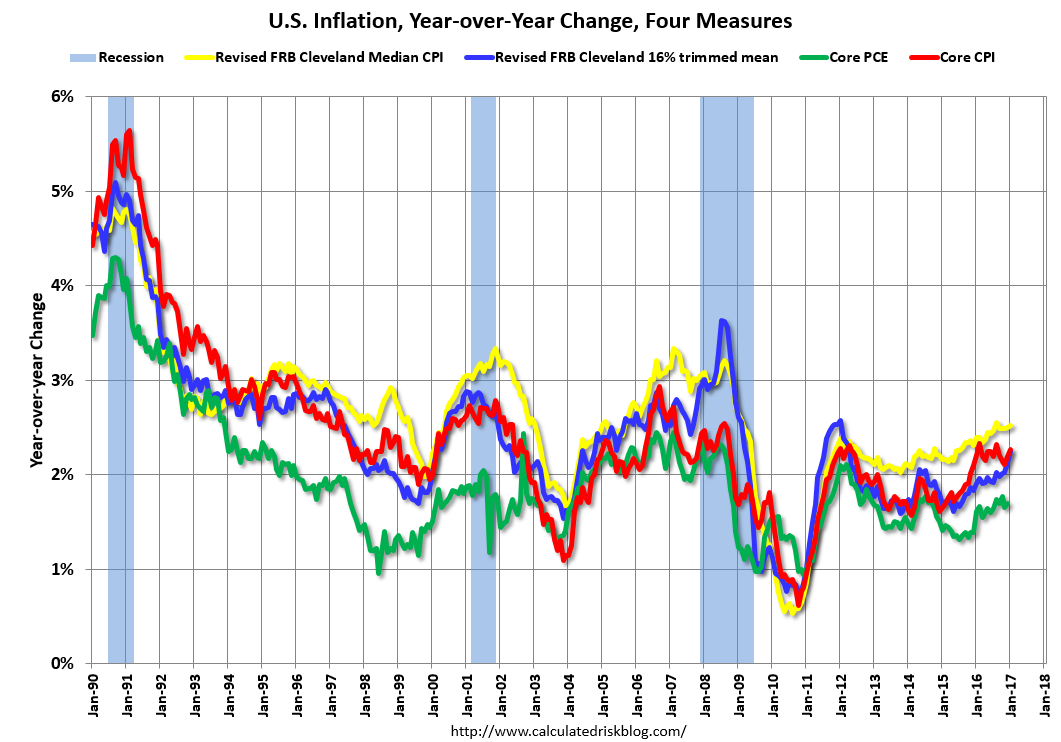

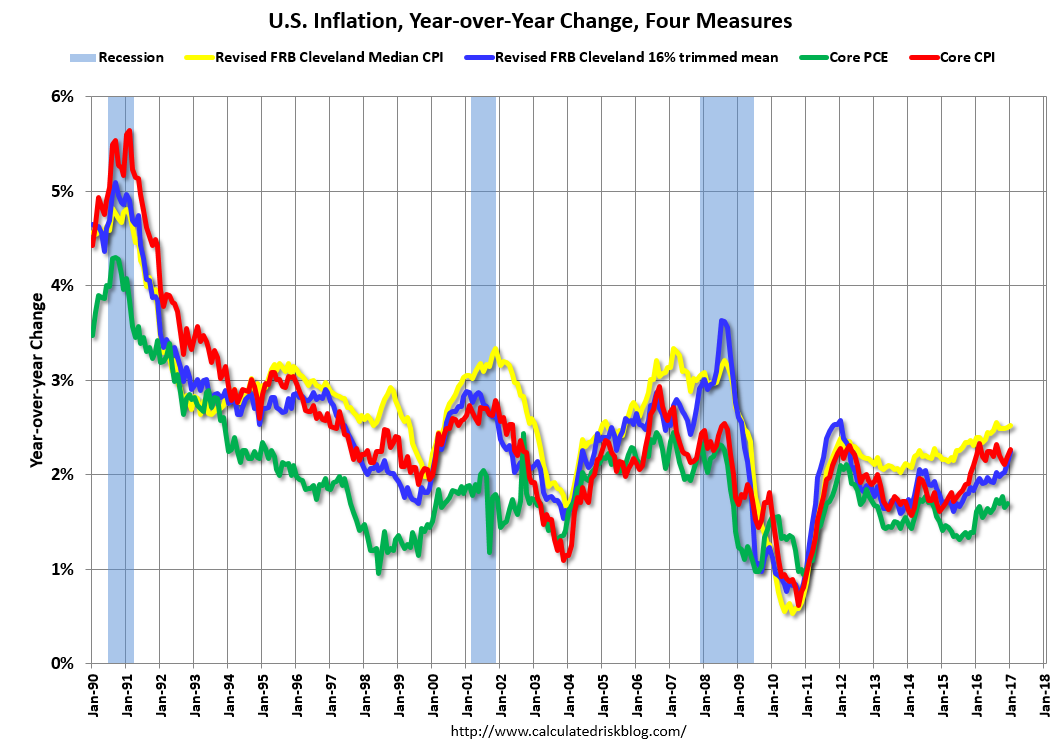

In data, US inflation is firming (charts from CR):

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.3% (3.3% annualized rate) in January. The 16% trimmed-mean Consumer Price Index also rose 0.3% (3.7% annualized rate) during the month. The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report.

Remember that it’s the green line that matters to the Fed so there is no panic here.

Retail sales were good:

Advertisement

Advance estimates of U.S. retail and food services sales for January 2017, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $472.1 billion, an increase of 0.4 percent from the previous month, and 5.6 percent above January 2016. … The November 2016 to December 2016 percent change was revised from up 0.6 percent to up 1.0 percent.

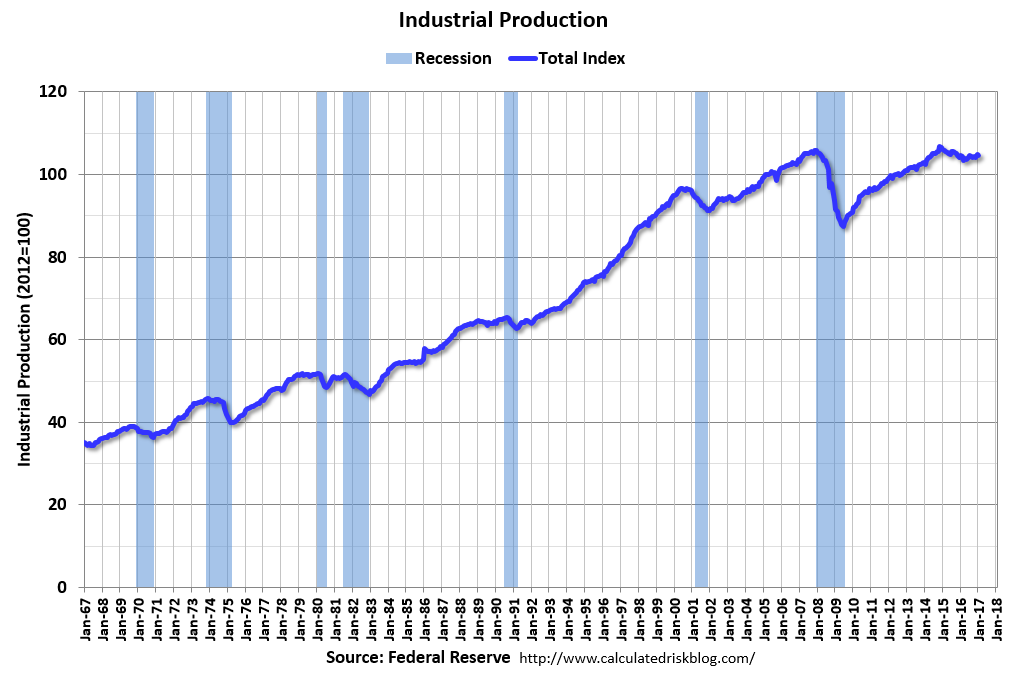

Industrial production was not:

Industrial production decreased 0.3 percent in January following a 0.6 percent increase in December. In January, manufacturing output moved up 0.2 percent, and mining output jumped 2.8 percent. The index for utilities fell 5.7 percent, largely because unseasonably warm weather reduced the demand for heating. At 104.6 percent of its 2012 average, total industrial production in January was at about the same level as it was a year earlier. Capacity utilization for the industrial sector fell 0.3 percentage point in January to 75.3 percent, a rate that is 4.6 percentage points below its long-run (1972–2016) average.

I expect IP to rebound with US shale ahead, as we are already seeing in PMIs, so the evening’s data was all reasonably favourable to the US reflation story.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.