An interesting article out yesterday revealed the largesse local developers are now showering on brokers and real estate “advisers” to help move unsold stock from upcoming off the plan apartment developments:

Commission payments of up to15 per cent, free tickets to Adele concerts and luxury holidays to Greece are on offer to mortgage brokers and financial advisers to recommend, sell and advertise property or consider mortgage products.

That means up to $90,000 for selling a $600,000 apartment, can be pocketed by the adviser, rebated to the buyer, or split between the adviser and client.

Taylor Dow, director of Taylor Dow Property Group, which last year sold $2 billion of Australian property to buyers in seven countries, including China and the US, said commissions range from 5 per cent and 15 per cent.

15%! – when a commission number like that gets bandied around you know there is going to be trouble.

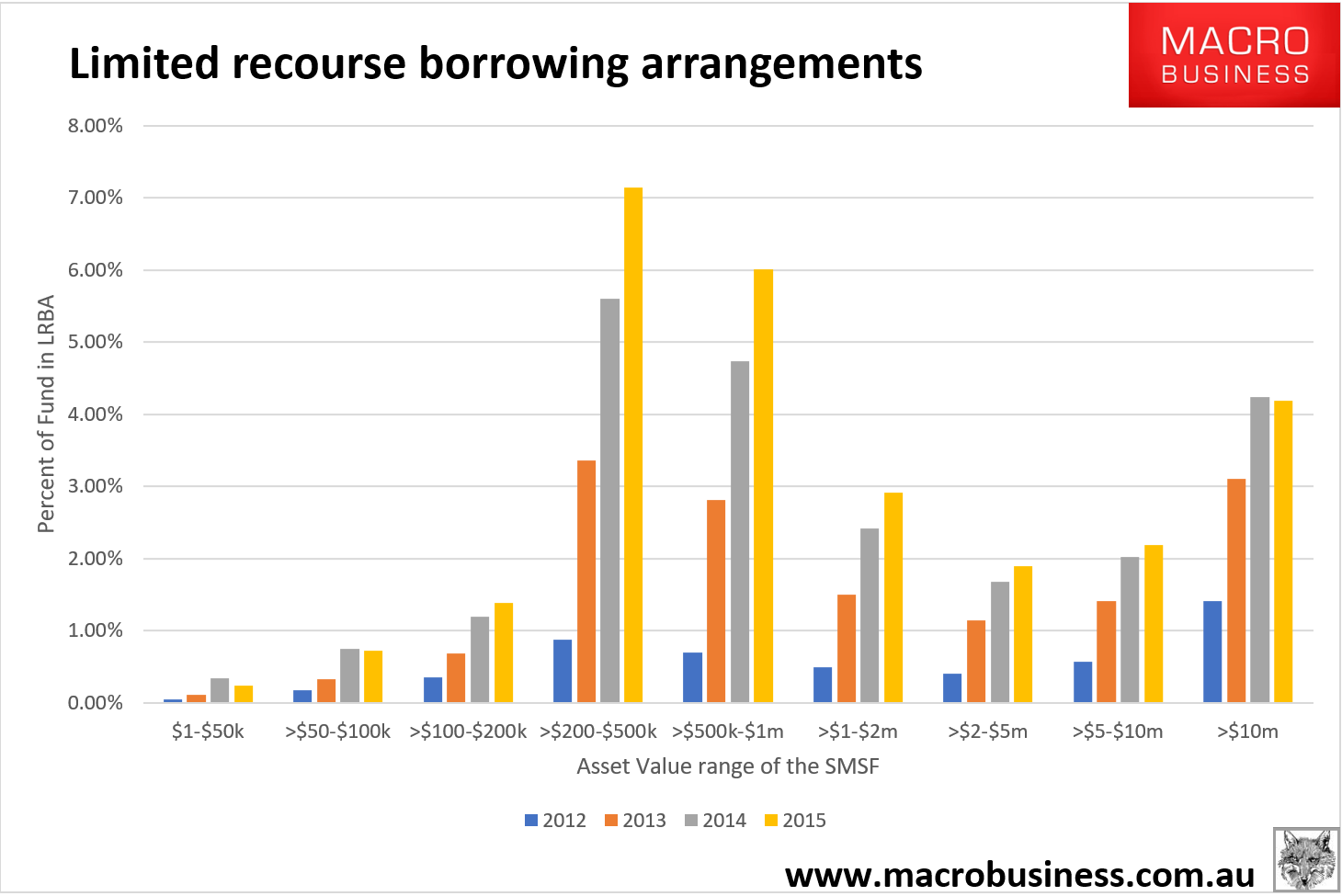

Armed with these new developments, I’ll draw attention to one of the favored tools used when closing the deal and scoring a big commission, the Limited Recourse Borrowing Arrangement within a Self Managed Super Fund.

Here’s a graph highlighting the increase in the use of borrowed funds from last year’s ATO SMSF report:

Blind freddy can see a trend developing.

Thankfully there has been some changes in legislation that may have some impact on the ability for the less scrupulous to guide unsuspecting property punters into their own slice of sky – namely the recently repealed ‘accountants exemption’ to provide advice around setting up an SMSF.

Let’s be clear here, I’m not pointing the finger at accountants. More to the point, by forcing anyone who provides advice on the creation of an SMSF for a client to either be licensed to give that advice, or find someone that can, it is slowly removing avenues for property spruikers to access the super system in return for these exorbitant commissions.

I should point out here that LRBA’s can be an effective tool in SMSF’s, particularly in small business where the family shop / warehouse is brought into the fund and back rented to the company. For suitable situations, it’s a terrific strategy.

However, for everyone else, it’s obvious that the marked growth in LRBAs (particularly for the $200k – $500k segment) would be a concern to a regulator already concerned with the height of real property prices currently.

Once again, it’s easy to see that a 20% pullback in apartment prices (possible with 15% commissions built in? – you be the judge) in even a moderately geared investment would wipe out a couples collective retirement savings over 10 years or more.

I am sure I’m not the only one waiting to see whether the mid July report from the ATO yields a drop in LRBA’s, or you can be sure more regulation is on the way.

Tim Fuller is Head of Operations at the MB Fund launching in May 2017. Register your interest now (if you haven’t already):