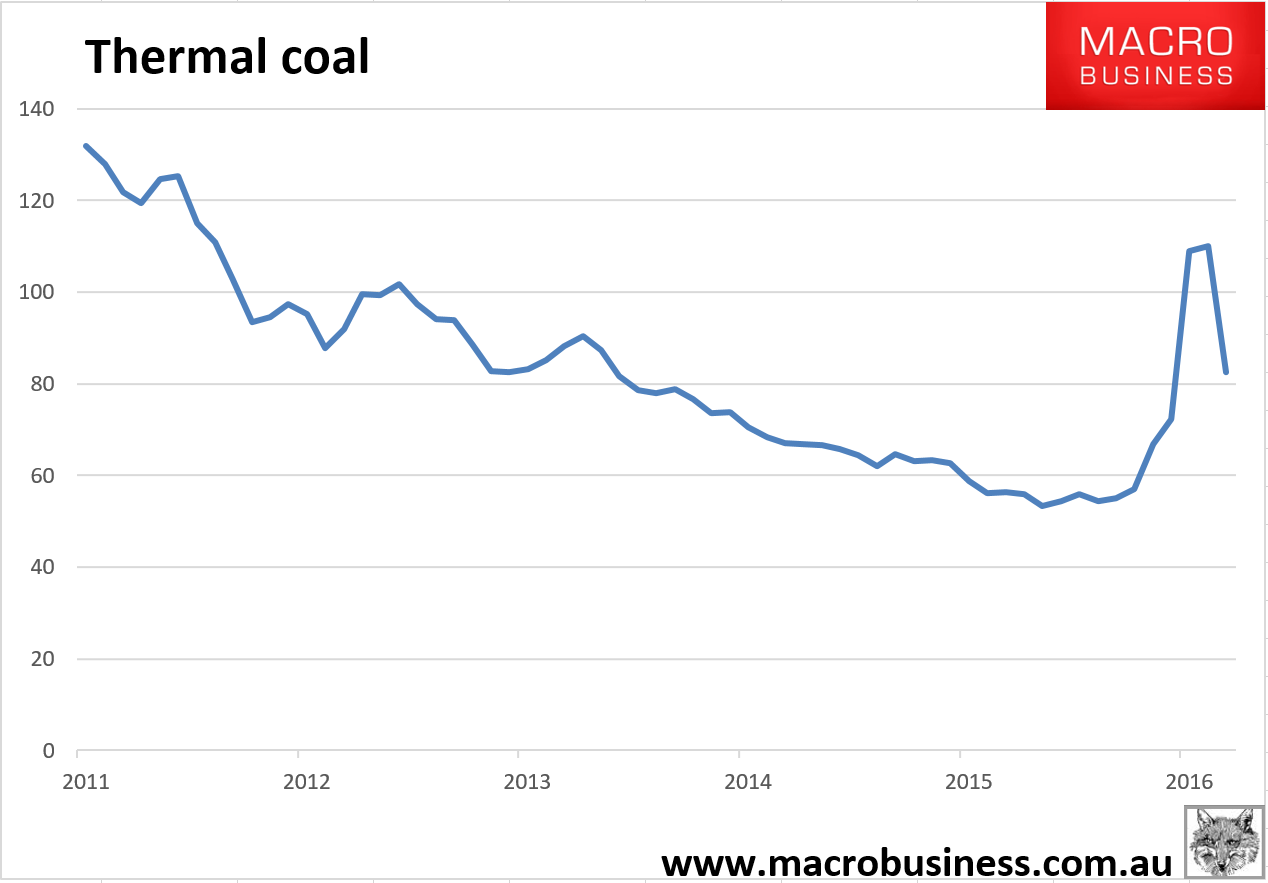

Thermal coal is well into its bust, today at $83 after peaking above $110:

Coking coal is now beginning to follow. After peaking at $314 it is down to $300 today:

Advertisement

From Morgan Stanley:

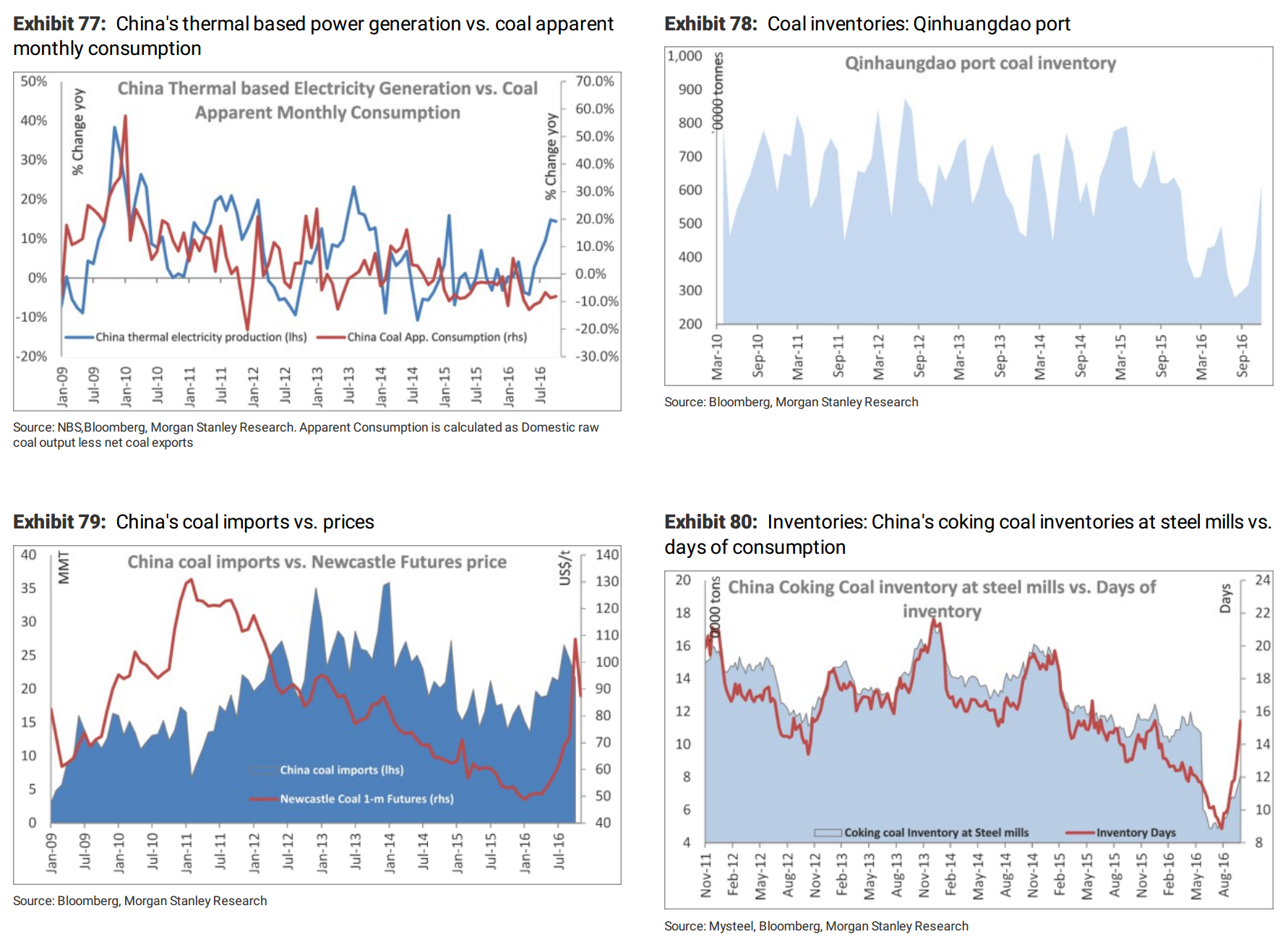

Turmoil persists: Seaborne metallurgical coal’s last round of quarterly price contractnegotiations were messy (commodity fruitCAKE: Met-coal’s peculiar Q4 deals, 11-Oct-16). That’s because the backdrop to 2016Q4’s talks was complicated by China’s surprise surge in spot imports,a major reversal of its general trade withdrawal over several years. The cause? China’s mid-year floods + aggressive industry reform created an unexpected coal shortfall. On 10-Oct-16, the mills of Japan hurriedly locked in unorthodox HCC 2016Q4 terms, correctly anticipating an extension of met-coal’s spot spike. Have conditions normalized,ahead of Q1’s talks? We don’t think so.

Current conditions,explained: Yes, met-coal’s key spot prices are just starting to slide now. Since stalling for a few weeks in November, HCC’s down 4% to US$300/t fob Aust.;LV-PCI’s -2% to $185/t; SSCC’s -2% to $141/t. Down a bit, but all are still 25-40% above spot levels reported at the 2016Q4 settlements; 8- 50% above the Q4 deals themselves. While the quieter northern winter trade has begun, seaborne spot prices are likely to remain elevated into 2017 – mainly because of the lack of clarity over the NDRC’s ongoing reform program (for metcoal, this includes a review of mining practices in its primary source, Shanxi Province), Queensland’s wet-season (Dec-Mar),and the lack of a meaningful supply response anywhere (Australia, US) – to current high prices.

Re-thinking forecasts: Our price forecasts (Global Metals Playbook: 4Q 2016 – Winter dawn,27-Sep-16) pre-date the full impact of the NDRC’s universal constraint on China’s domestic supply. A review of China’s altered import flows is now needed, to reset our price outlook. Industry reform is likely to continue over the next 12-24 months,given what is known of the scale/duration of this program. A reasonable estimate of the potential upside risk to the market’s 12-month price outlook for the key met-coal products (HCC,LV-PCI, SSCC) would be at least 30%.

Equity exposure: The return from bankruptcy of once-popular US-based metcoal plays of Alpha Natural (emerged, Jul-16) and Arch Coal (Oct-16) flags the extraordinarily tight conditions in global coal trades. Key beneficiary of seaborne’s high met-coal spot prices is BHP Billiton: controls 75Mtpa of trade’s total 300Mtpa; done mostly on spot terms. Other big met-coal exporters (MSe, top export rate) include Teck (24Mtpa), Anglo (24Mtpa), Peabody (20Mtpa), Rio Tinto and Glencore (15Mtpa each). Quarterly price contract talks typically begin 2-3 weeks before the new quarter starts.

It’s far too late to be getting long. This is the top and the higher percentage play is to get short (if you want to invest):

the coking coal spike was largely a restocking episode, it’s advanced a lot but will not be entirely done until end of Q1;

the second driver was the Chinese policy error in production curbs that have already been reversed;

coking coal is not as flexible a market as thermal but there’s still plenty of seaborne capacity that can come back over time and it will;

Chinese construction should still slow H1 2017.

Advertisement

There’ll no doubt be lot’s more contract tensions but, really, who cares? By mid next year it’ll all be reversing fast.

I do not expect coking coal to return to $80 for a few years now. China has shocked the market such that a risk premium ought to be built in now that keeps it above $100. It won’t be until China really hits the construction down slope that it falls below $100 again. $120 by this time next year seems reasonable.

The final point to make is that as coking coal falls, I can’t see how iron ore is going to hold up.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.