The USD bull market is the only game in town ripping to new highs last night. Zombieuro is close to all-time lows. JPY is crashing. CNY held up:

Commodity currencies were mixed, Aussie got flogged:

Gold broke down:

Brent fell:

Base metals too:

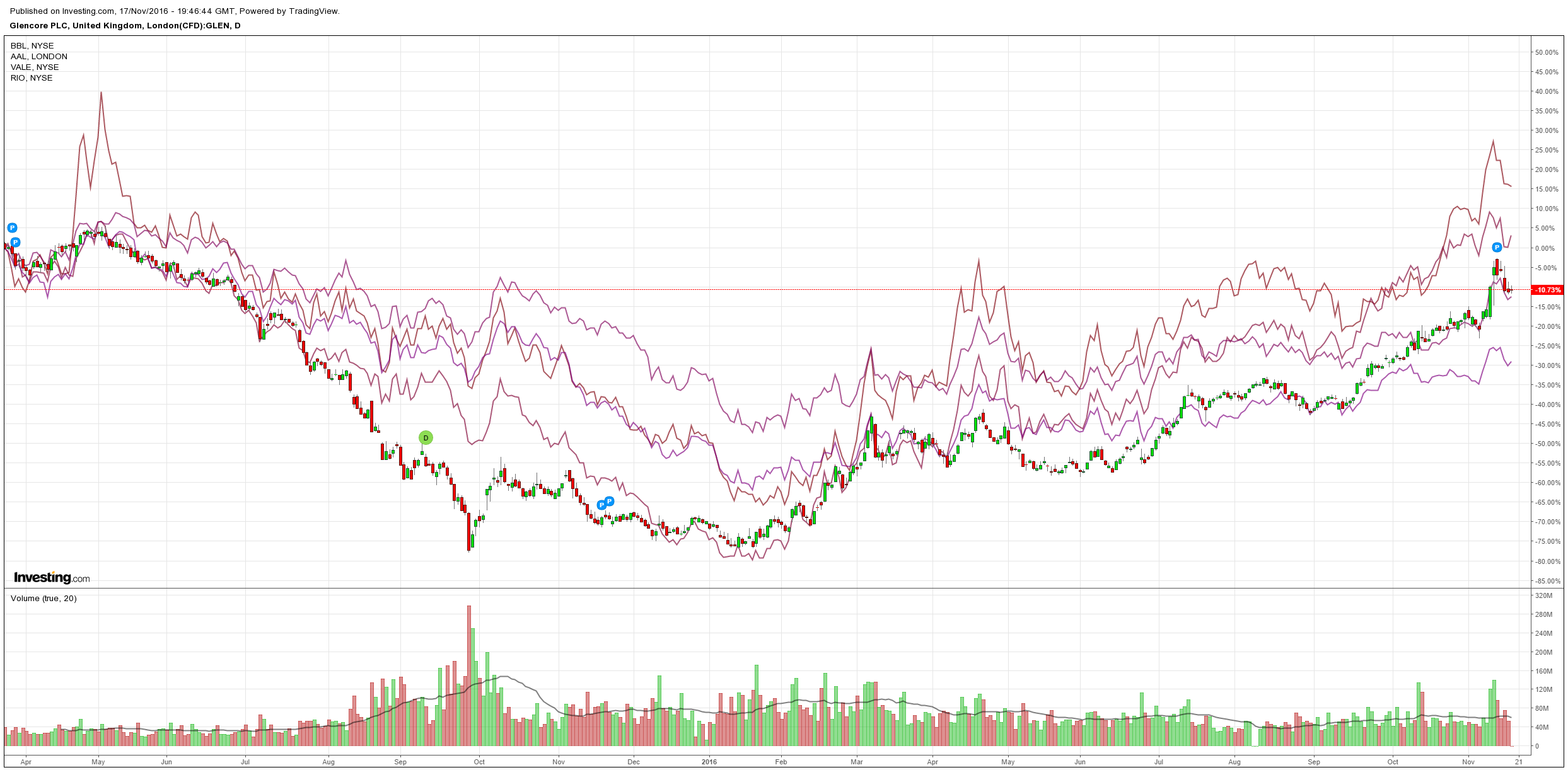

Big miners were mixed:

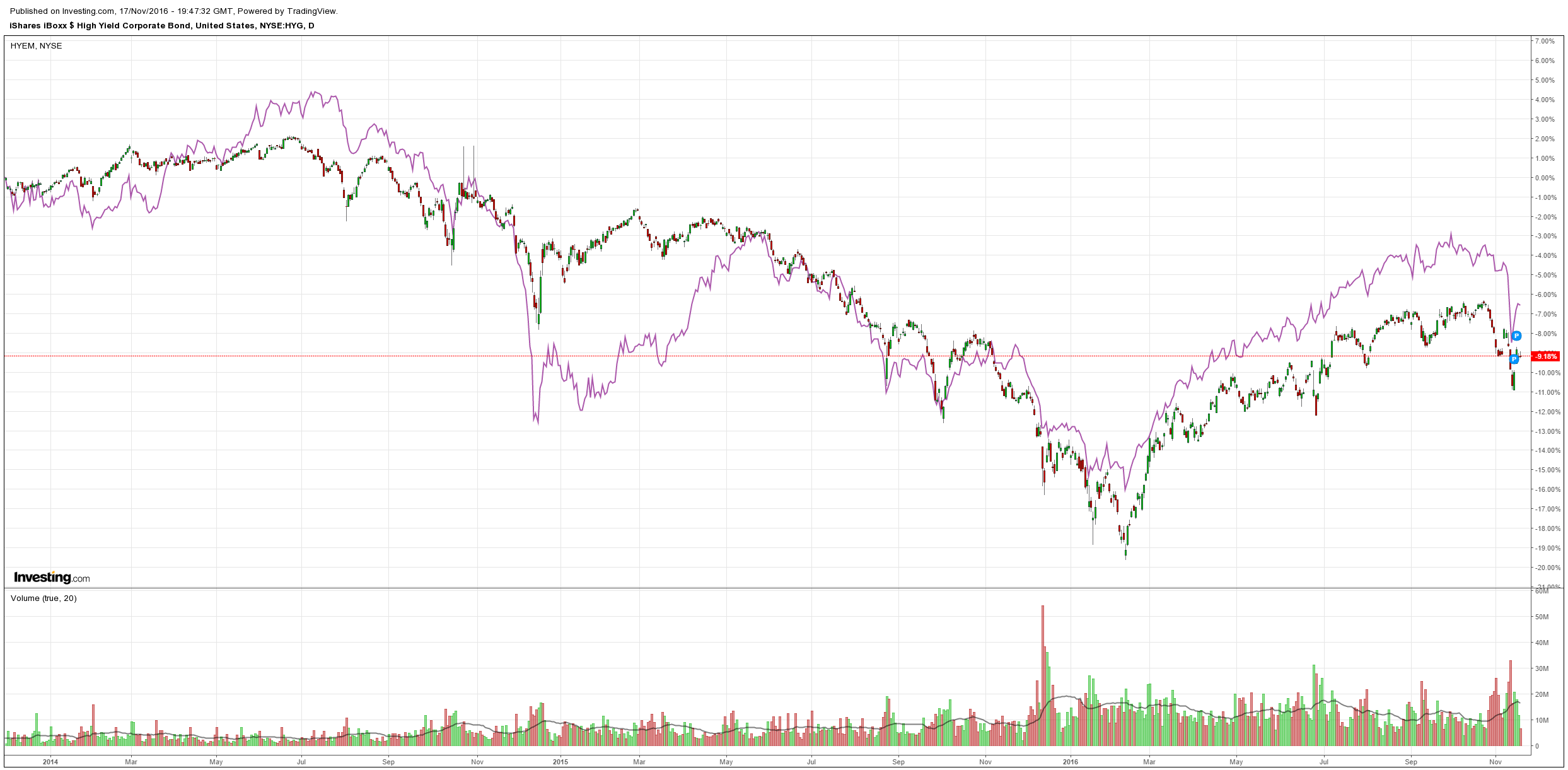

US and EM high yield eased:

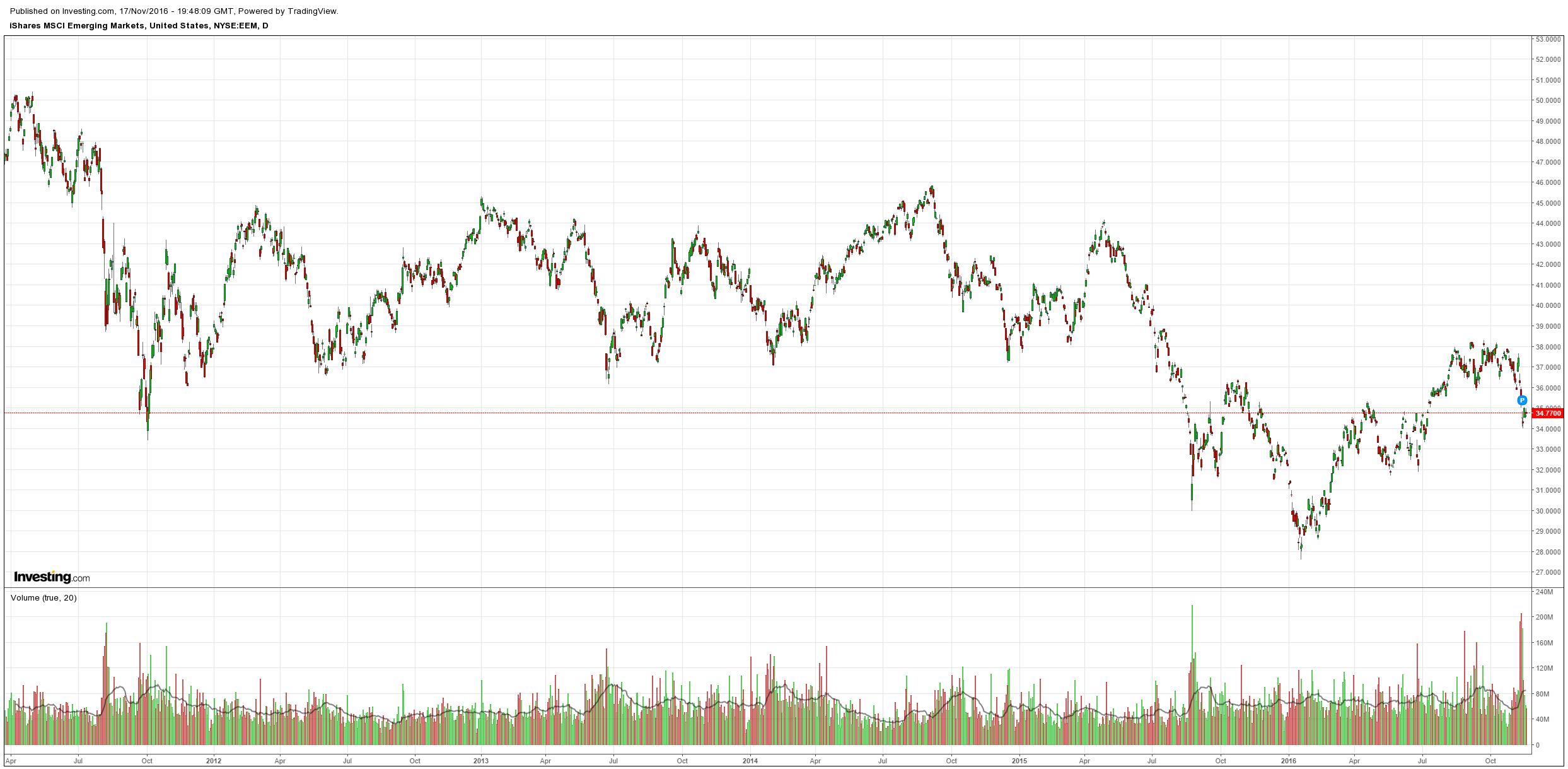

As did EM stocks:

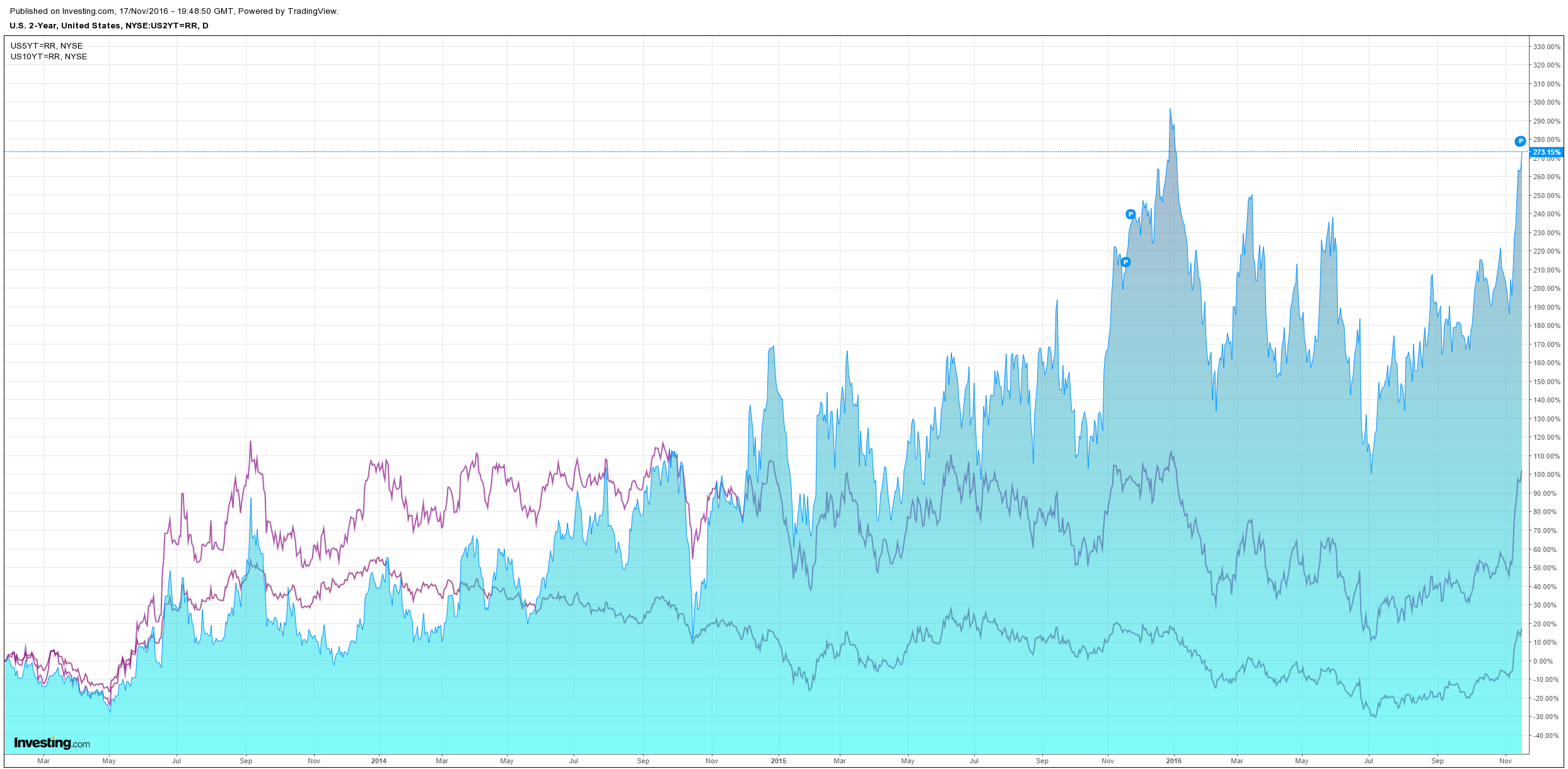

US bonds were flogged:

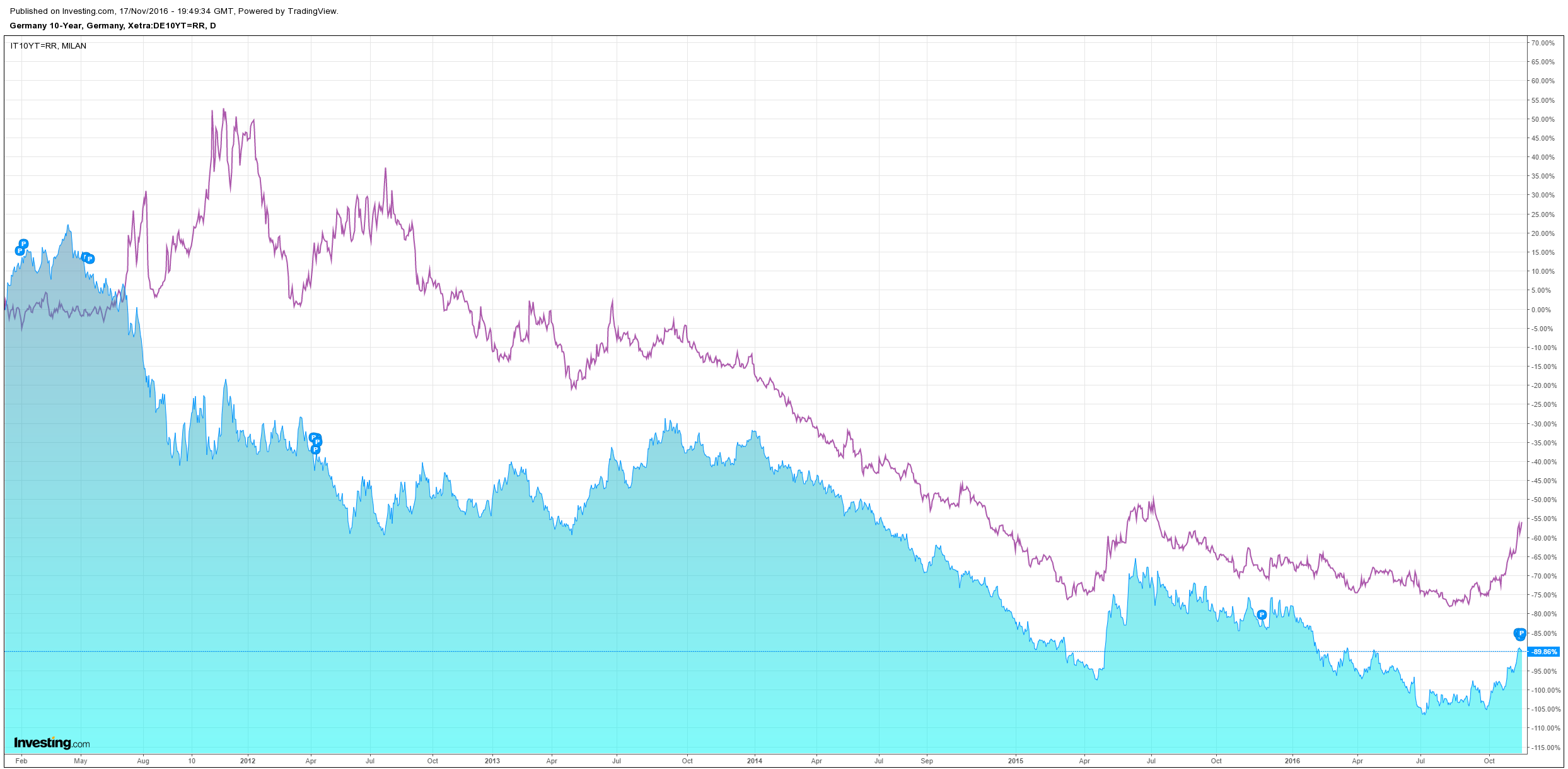

Italian spreads widened:

But US stocks lifted:

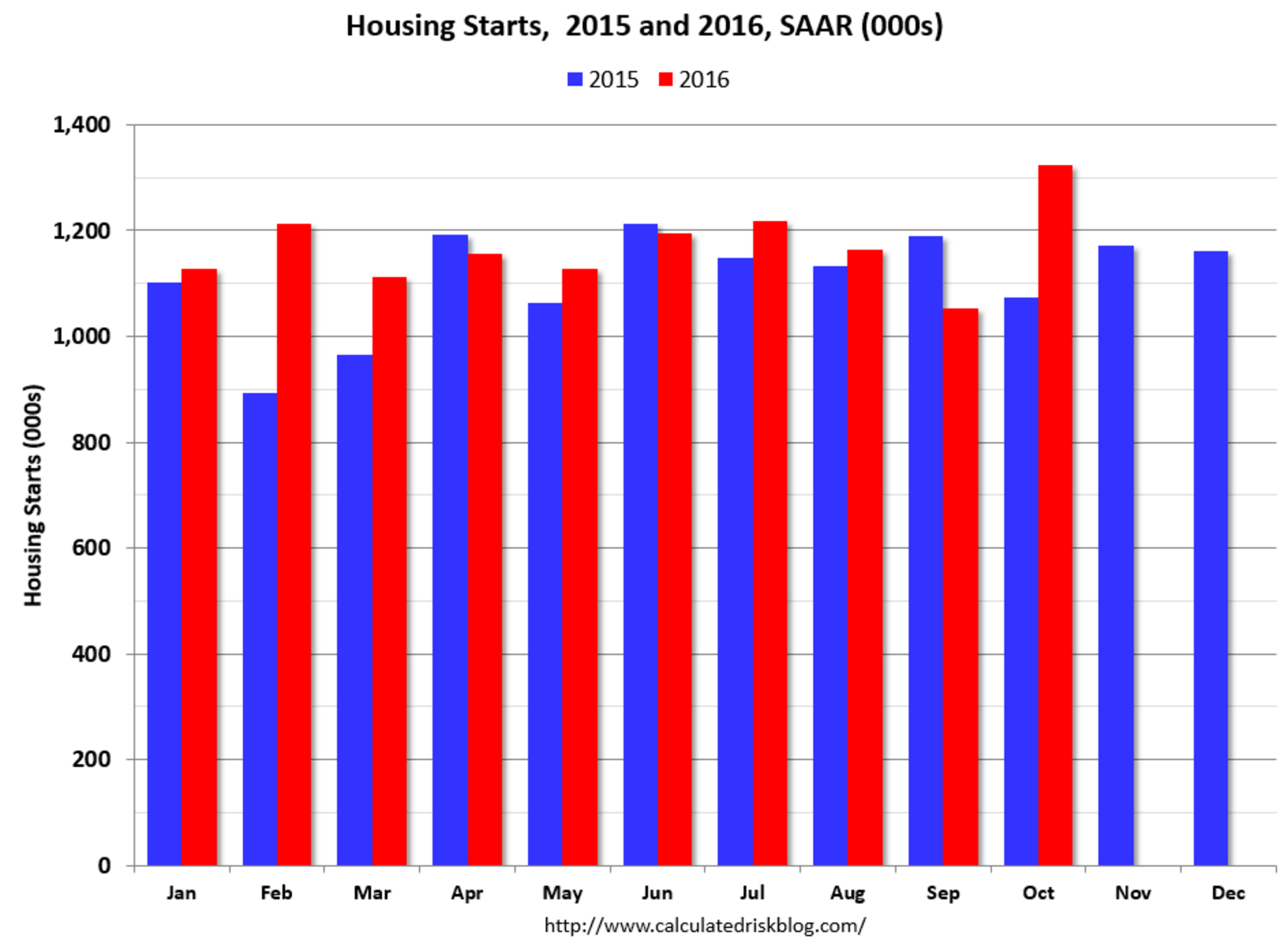

News on the night was a everything going right for the US dollar with rampaging housing starts (charts from CR):

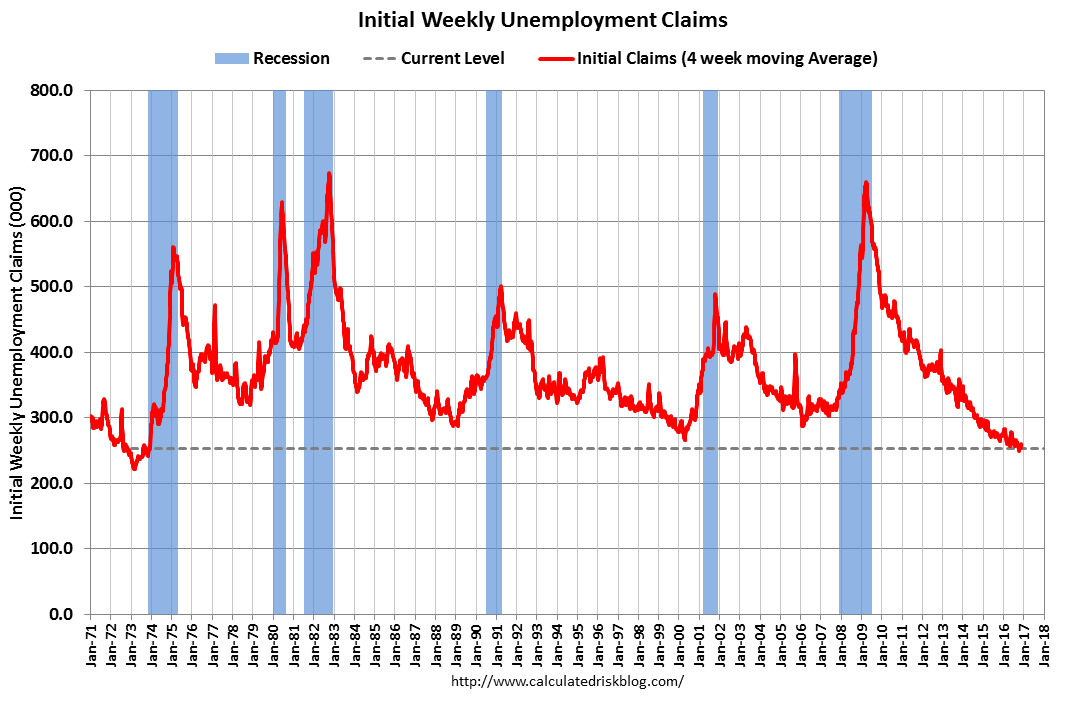

Tumbling unemployment claims:

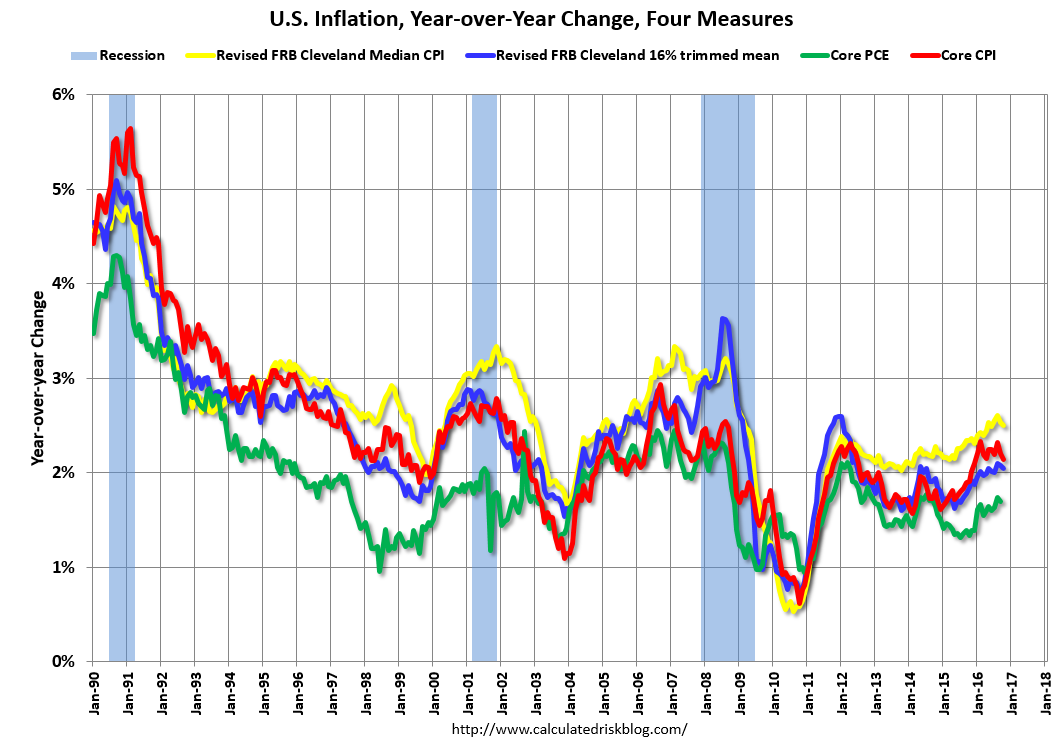

A slight easing inflation with intact up trend:

And a hawkish Yellen speech:

I will turn now to the implications of recent economic developments and the economic outlook for monetary policy. The stance of monetary policy has supported improvement in the labor market this year, along with a return of inflation toward the FOMC’s 2 percent objective. In September, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent and stated that, while the case for an increase in the target range had strengthened, it would, for the time being, wait for further evidence of continued progress toward its objectives.

At our meeting earlier this month, the Committee judged that the case for an increase in the target range had continued to strengthen and that such an increase could well become appropriate relatively soon if incoming data provide some further evidence of continued progress toward the Committee’s objectives. This judgment recognized that progress in the labor market has continued and that economic activity has picked up from the modest pace seen in the first half of this year. And inflation, while still below the Committee’s 2 percent objective, has increased somewhat since earlier this year. Furthermore, the Committee judged that near-term risks to the outlook were roughly balanced.

Waiting for further evidence does not reflect a lack of confidence in the economy. Rather, with the unemployment rate remaining steady this year despite above-trend job gains, and with inflation continuing to run below its target, the Committee judged that there was somewhat more room for the labor market to improve on a sustainable basis than the Committee had anticipated at the beginning of the year. Nonetheless, the Committee must remain forward looking in setting monetary policy. Were the FOMC to delay increases in the federal funds rate for too long, it could end up having to tighten policy relatively abruptly to keep the economy from significantly overshooting both of the Committee’s longer-run policy goals. Moreover, holding the federal funds rate at its current level for too long could also encourage excessive risk-taking and ultimately undermine financial stability.

The FOMC continues to expect that the evolution of the economy will warrant only gradual increases in the federal funds rate over time to achieve and maintain maximum employment and price stability. This assessment is based on the view that the neutral federal funds rate–meaning the rate that is neither expansionary nor contractionary and keeps the economy operating on an even keel–appears to be currently quite low by historical standards. Consistent with this view, growth in aggregate spending has been moderate in recent years despite support from the low level of the federal funds rate and the Federal Reserve’s large holdings of longer-term securities. With the federal funds rate currently only somewhat below estimates of the neutral rate, the stance of monetary policy is likely moderately accommodative, which is appropriate to foster further progress toward the FOMC’s objectives. But because monetary policy is only moderately accommodative, the risk of falling behind the curve in the near future appears limited, and gradual increases in the federal funds rate will likely be sufficient to get to a neutral policy stance over the next few years.

December hike locked in. The USD is hugely overbought and will pull back at some point but it is an unstoppable juggernaut.