Evaluation of LNG import facility. AGL is evaluating the potential to import LNG into the south eastern seaboard (SA, Vic, NSW) due to the tightness in the east coast gas markets. AGL’s view is that there is a risk around gas deliverability availability from 2020 and that it needs to explore options to meet its customer needs from this date. Total capex to be spent ahead of FID is $17m, with total construction cost estimated to be in the $200-300m range, with FID expected in 2018-19. How real is this option? When we analyse AGL’s gas supply portfolio, contracted gas supply declines from FY17-19 as existing supply agreements expire. In particular, AGL’s contract with the Gippsland Basin JV (GBJV) expires in 2020. Ultimately the only other indigenous gas supply of any quantity is in Queensland, which effectively would require AGL to negotiate with an LNG producer to not liquefy gas and instead transport the gas volume to Southern markets. Not only would this LNG price be at (oil-linked) LNG netback prices, but would also require the addition of around $2/GJ for gas transportation to NSW (more if to Victoria). The serious analysis of LNG imports (likely via Floating Storage and Regasification Unit or FSRU) into either Victoria or NSW makes sense to apply some degree of competitive tension in price negotiations with GBJV. The merit of LNG imports would depend on a number of variables, but the cost of this option wouldn’t be cheap. Assuming a Henry Hub price of US$3/mmbtu, liquefaction fee of US$3/mmbtu, shipping cost of US$1.50/mmbtu and regas charge of US$0.50/mmbtu we estimate a landed cost in NSW or Victoria of US$8.3/mmbtu (A$10.50/GJ). Arguably AGL could secure LNG cargoes at lower cost until LNG markets tighten up from 2023 (UBS view), but this would expose it to the spot LNG market and less security of supply.

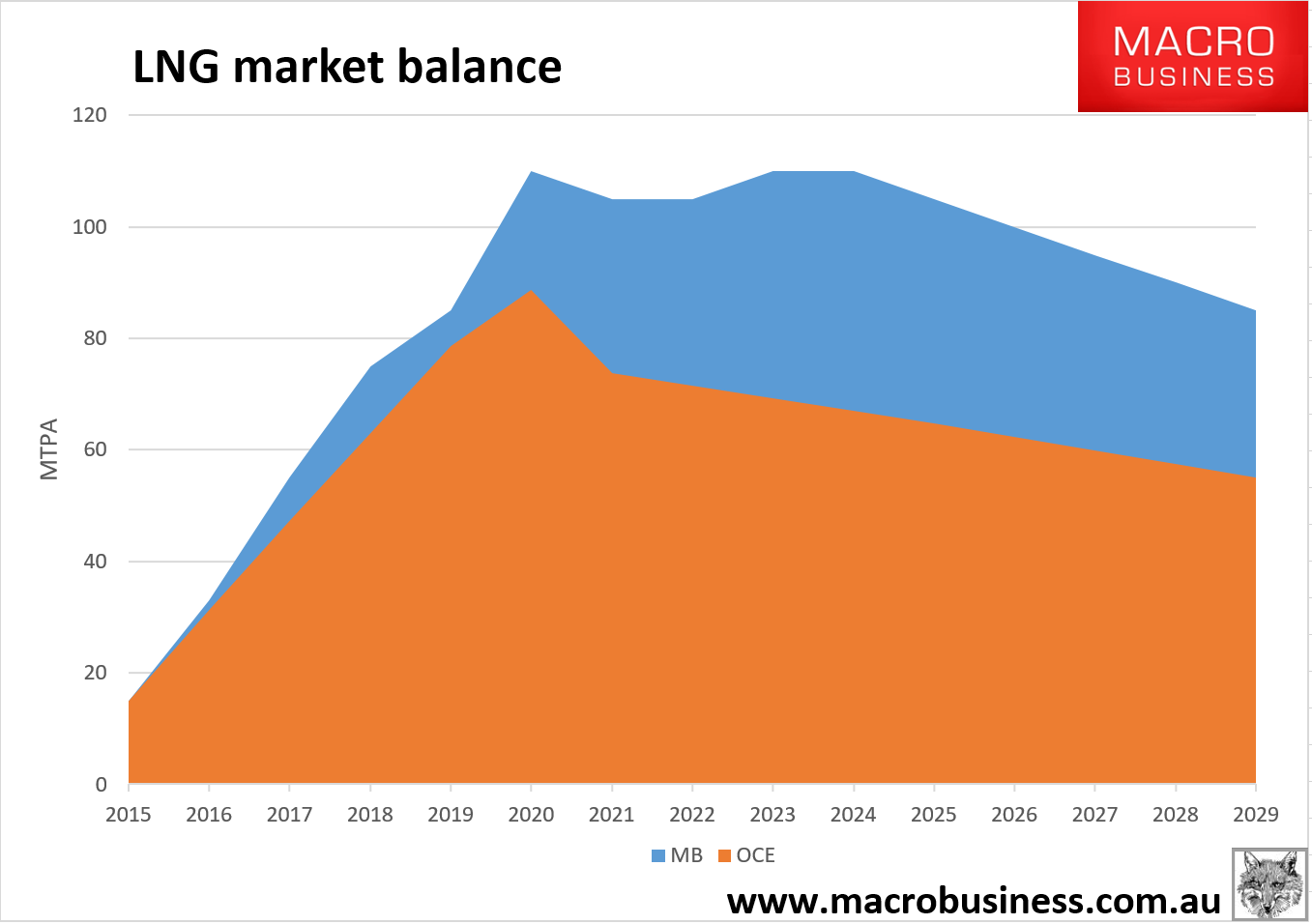

The LNG glut will be so big by 2020 that I’d be quite surprised if AGL couldn’t secure supplies at better prices than that:

Spot markets are burgeoning and will be much larger by 2020 including resales of contract gas once Asian nations break the destination clauses in their contracts (as early as pre-Xmas when Japan rules them illegal). It’s quite possible that AGL could be buying Japanese purchased gas, sold at a loss by QLD producers at $4mmBtu, and shipped south to NSW or VIC for $5.50mmBtu (or A$7 GJ). Mind you, by then the Aussie dollar at 50 cents might change things.

Advertisement

Yes, that’s how stupid it is (not AGL, Straya) not having domestic reservation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.