Yesterday the People’s Bank of China said in its third-quarter monetary policy implementation report:

While creating neutral and appropriate monetary and financial environments for structural reforms and keeping liquidity reasonably ample, we should pay attention to curbing asset bubbles and preventing economic and financial risk.

The balance between stabilizing growth and preventing bubbles has become more challenging.

On the same day, the Dalian Commodities Exchange tightened restrictions of futures trading for coking coal. The reason is simple enough, there’s a bubble in Chinese commodity futures and at its core is a crazy coking coal market drunk on the Chinese policy error of limiting coal output.

Don’t get me wrong. The result has been a shortage of coking coal, with mine output down, inventories at record lows and steel output good. But, what is happening is that that kernel of truth has inflated coking coal futures volumes 500% in a month and pushed prices far above those needed to trigger the required supply response. Moreover, that bubble has spread into steel, iron ore, base metals and this week began to impact softs as well. All are setting records for the number of positive price days as hoarding returns as a favourite Chinese speculative pastime.

So, today, I will run through all of the implications of this as I see them.

Chinese policy

My working model for Chinese policy is this:

- good ideas come from the top;

- as they dribble down the bureaucratic value chain they are debased by the less competent and corrupt which figure out how to game them;

- thus when implementation comes the policies nearly always overshoot;

- when this becomes obvious, more good ideas come the top to counter the distortions arising from the first wave;

- these are again debauched in implementation and are usually ineffective;

- more Draconian measures to counter the distortions of the first two waves of good ideas come from the top, and

- reversal of the original good ideas nearly always overshoots.

We are currently in phase 5 of this process when it comes to the supply-side reform of coal and the attached bubble with the original good idea done poorly, then gamed like crazy, then partly reversed, gamed again, now partly reversed a second time. Whether we’ll see a more Draconian reversal is hard to say but, in the end, it will not matter. Supply will do it anyway.

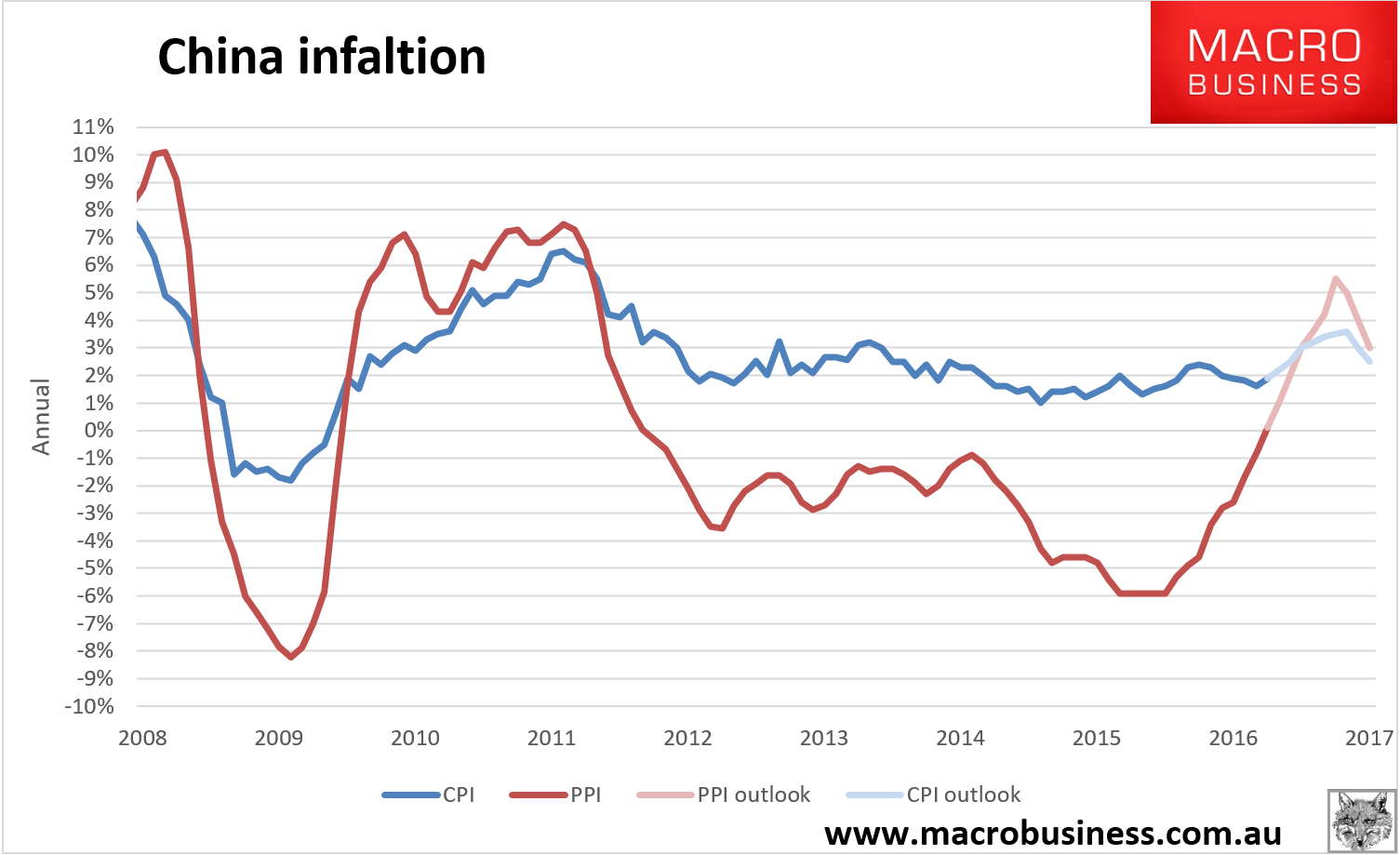

That gives us two scenarios to work with: a quick policy reversal that crashes the bubble or a supply response that lets the air out more slowly. There is one reason to think that a more concerted effort will arrive to stamp out the bubble. Producer inflation is going to rip and drag up the CPI as well if past relationships hold:

Whether the hard brake is pulled probably depends upon whether or not food prices take off as well.

My view is that China will not want to stomp on this too hard. It is clearly prioritising growth and it will not raise interest rates given it wants a lower yuan and to destock oversupplied housing markets. That leaves the PBOC using prudential tools to lean against local bubbles like eastern cities property. This will probably work over time.

Thus the slower deflation is the higher probability outcome.

Beneficiaries

The three main beneficiaries are:

- thermal coal is an abundant and flexible market and China has already rebuilt half of its inventories so the price is going to peak this quarter (maybe already). I see it at half current levels within a year;

- coking coal is less flexible but as Alan points out the supply response is underway. The spot price is probably somewhere near its peak today given the restock is also roughly halfway done but will remain higher for longer because mines need to be re-opened and that takes time. I still see it at half current prices within a year as well;

- iron ore is also a flexible and abundant market so its peak must be very close too. It’s restock only has 5mt to run before ports have the most dirt in history. Next year it’ll see another new 50mt of super-cheap ore. I see it down a third within a year.

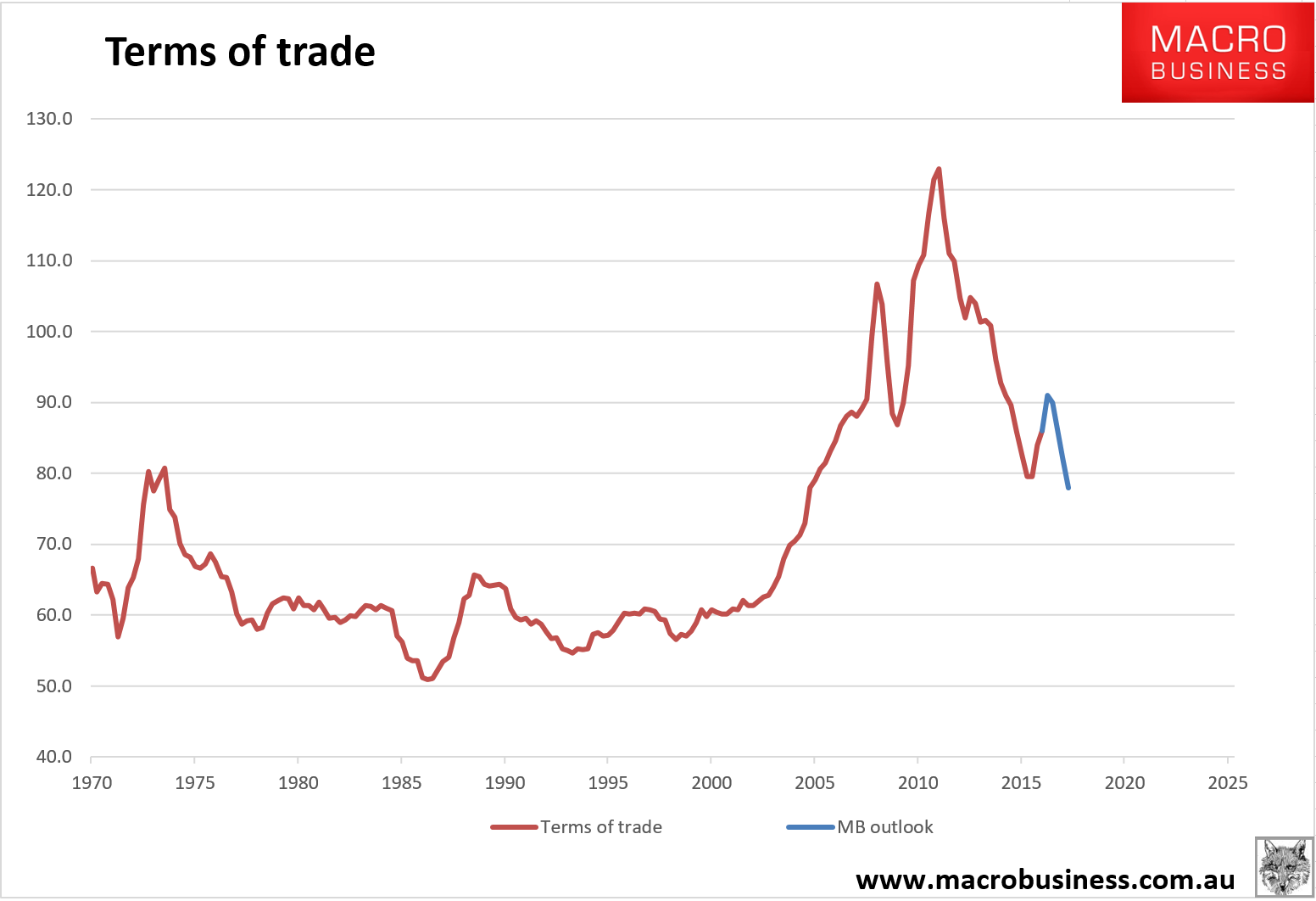

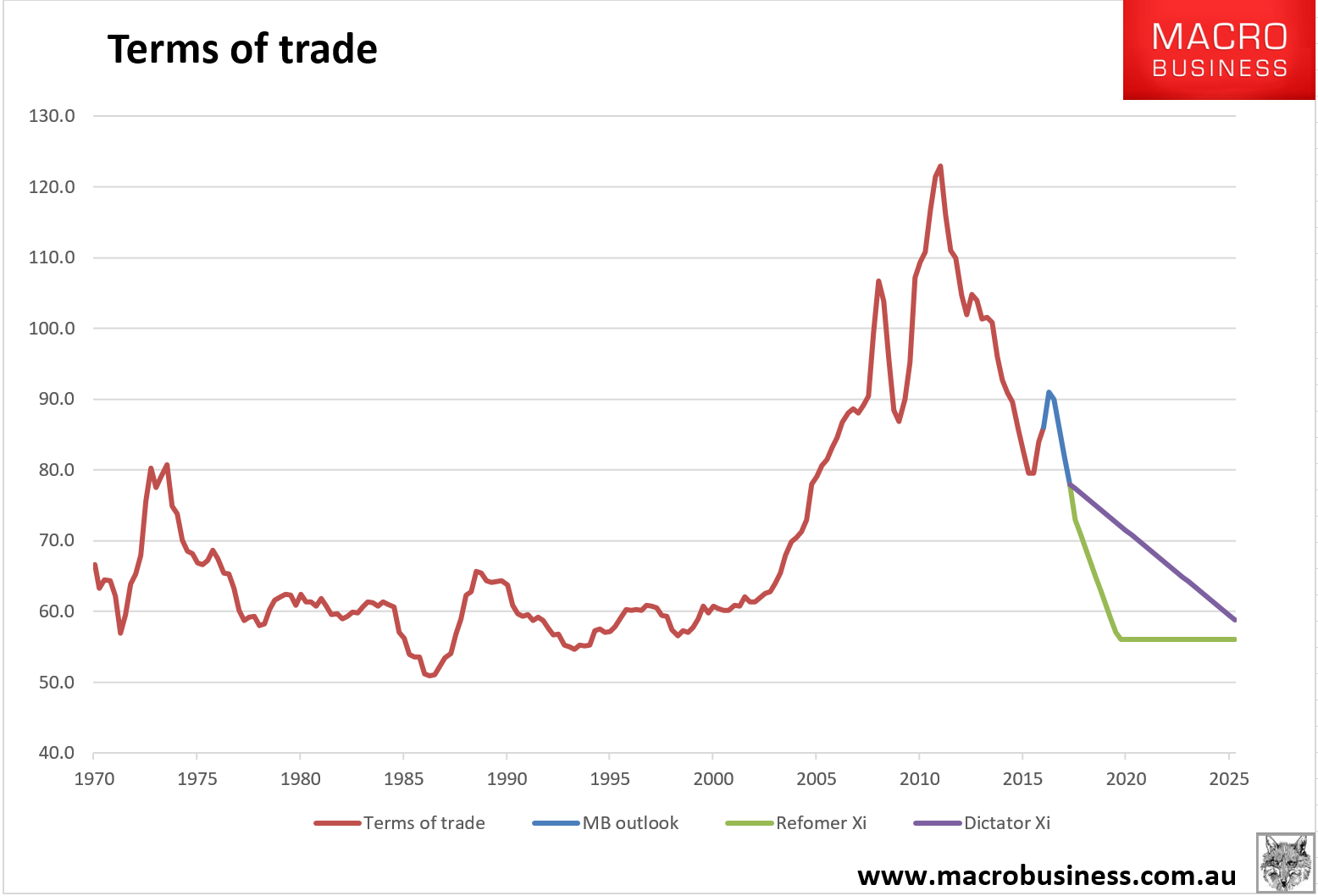

Thus Australia’s terms of trade will look like this over 2017:

That means higher nominal GDP, higher national income, better budget receipts and improved miner share prices. I do not expect much of an impact on wages because much of the tax revenue will be saved and there will be minimal investment flow through from the price jumps. The major beneficiaries will be the budget and mining shareholders.

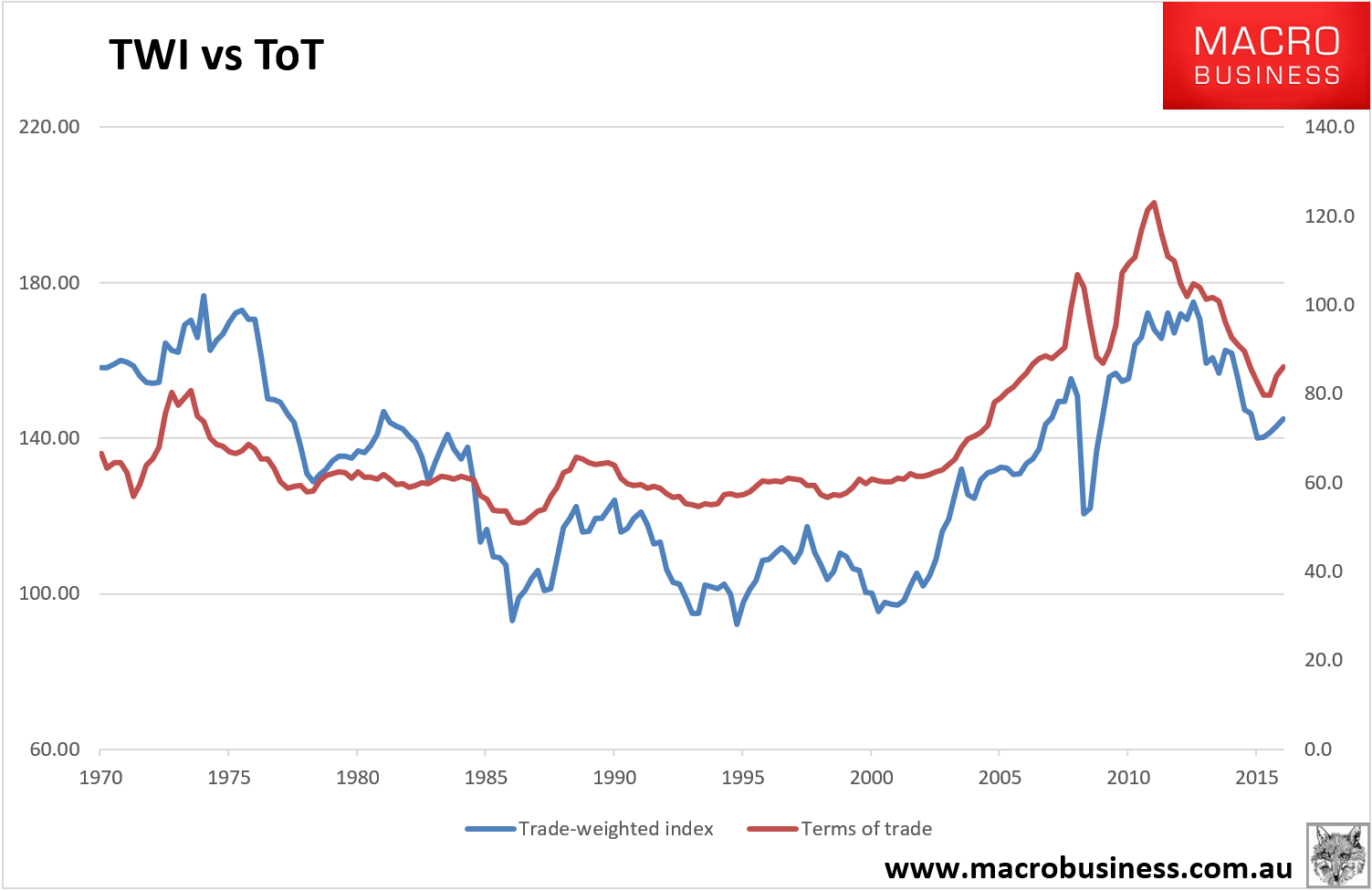

In fact, the net impacts for the wider Australian economy are probably negative. With the slow deflation route of the ferrous bubble most likely, the Australian dollar may break higher for a brief period, towards or above 80 cents. It is already bid strongly today in the mid-77 cent range:

Which makes sense given the relationship between the terms of trade and trade-weighted index:

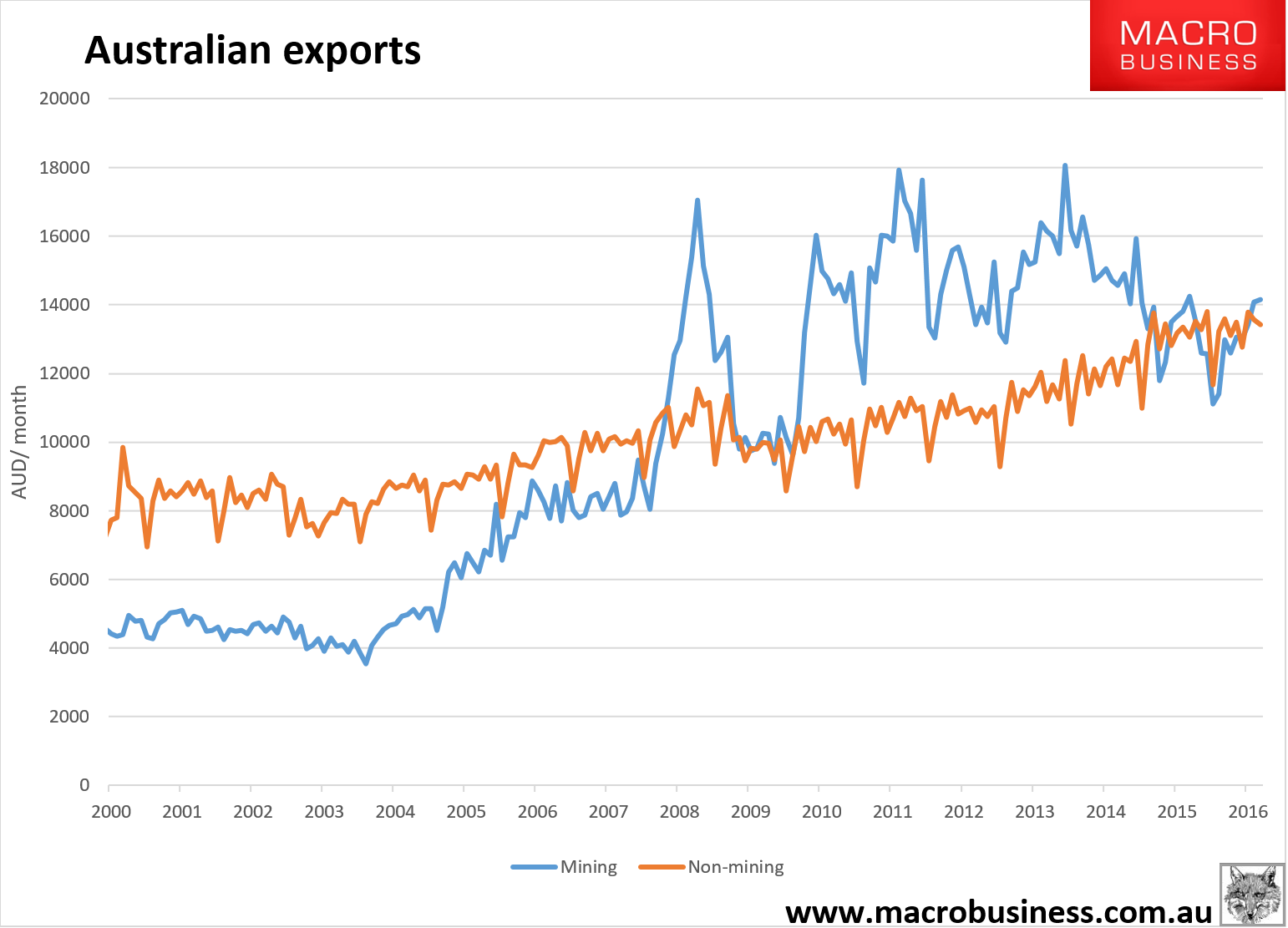

But, it also means Australian “rebalancing” to non-mining exports is taking a serious hit. It stopped growing two years ago and will soon start to shrink:

:

: These are the sectors where we are seeing pick-up in investment and employment to offset the ongoing mining capex cliff, hence the implications of the ferrous bubble being net negative for the real economy.

The budget could in theory provide some benefit if it recycled the windfall as tax cuts or more infrastructure spending but I can’t see it. The AAA rating is in severe jeopardy as we speak and may still be cut despite the ferrous bubble:

Therefore I see little to disrupt the outlook for the RBA here, either. Any inflationary pulse from the ferrous bubble will be muted. And, as I say, households are not likely to see much of the income anyway given wages will not be impacted much. Perhaps bouncing mining share prices will boost confidence and spending at the margin but we’ve not seen it so far.

Backbone Phil has shown he’d not like to cut rates again and this will give him his excuse but as the bubble deflates he’ll be forced to return to cuts sometime next year.

Asset classes

The obvious beneficiaries of the bubble are miners, which have suddenly found themselves operating lean operations with massive margins. It’s too late to get long. The risks are now all skewed to the downside. Short looks good for the bold.

There is one longer term outcome here. As both WHC and FMG are showing, the ferrous bubble has afforded them the opportunity to deleverage their arses off. This is the case worldwide in mining. Dead and buried majors like Anglo and Vale are now reconsidering all asset sales as rocketing cash flow pays down debt. This is a great outcome for shareholders in the short term but longer term it means just one thing: more supply for longer.

China may be prioritising growth now, and it may keep doing so under its emerging dictator as well. But that is the path of Japanese stagnation for China and it will kill its growth over time. Over time, commodity demand will fall whether he is reformer or dictator, and it would be better for the world if it didn’t also prevent China from advancing its development beyond the “middle income trap”:

So, longer term the ferrous bubble deleveraging will only ensure that commodity prices remain under more pressure for longer by preventing what the market really needs, a decent supply-side shakeout.

The second market worth discussing is bonds. The ferrous bubble is large enough to push a little short-term inflation out of China and into Western economies. At the margin at least this will encourage the long bond sell-off underway globally. It’s not big enough to be a game changer but along with oil and the base effect, it may be enough to accelerate tightening pressures in the US and ending QE in Europe. That would be a mistake but the long end of the curve worldwide is at risk of higher rates in the short-term.

For Aussie bonds the same outcome is probable. Though I expect the short end to remain anchored given I do not expect much economic benefit nor change in RBA outlook.

Finally, we should consider house prices. Will the ferrous bubble have any impact? Perhaps at the margin. If the Aussie dollar does rise further as the yuan falls then Australian house prices will look attractive to Chinese buyers even as they get more expensive. So we can probably expect no diminution of those pressures. The local bid may be benefited a little via confidence but I don’t expect much. Perhaps Perth can hope for better in the short term before the dark closes over again.

If there is an impact on prices, look to APRA not the RBA to tighten. The latter will be freaking out about the currency.

All up, it is perhaps surprising how little the ferrous bubble is likely to change the fortunes of Australia. A swing here and roundabout there, yes, but no change in basic trajectory. The fact is, this remains a brief reprieve in the great march lower to the marginal cost of production for commodities not a serious change of direction. The world has already built out the supply for a hundred years of dirt. It’s relatively easy to switch it back on again when needed.