You think after being firmly debunked twice before (here and here) that Stephen Koukoulas (“the Kouk”) would have learned his lesson. But no, like some hideous singed moth drawn to the flame of its own incinerated credibility, yesterday he published another tirade spouting that millennials have nothing to complain about on housing affordability, and telling them to stop wasting their money at cafes and on entertainment if they want a home. From Yahoo Finance:

I thought kids stopped screaming and being blindingly selfish when they turned 3 or maybe 4. I was wrong. It could be that 30 is the new 3.

Having witnessed, first hand, some of the froth and bubble surrounding the issue of consumption patterns of millennials, that they prefer spending money on lattes and smashed avocado on toast rather than a dwelling, there is an irrational, self centered discussion that blames anyone and everyone for their inability to get into the housing market.

If Twitter and some of media articles are anything to go by, a bevvy of millennials have explicitly expressed their overwhelming desire to spend their money on avocado, ubers, the latest phones and travel rather than saving to buy a house…

Rather than leaving it there, the millennial group then unrelentingly complain about their perceived in ability to tap into the housing market… Of course, we would all like to own a lovely house AND eat out a lot, have the latest technology and go on holidays…

No one can be sure why this is the case, but maybe this is because they will simply never compromise on spending and lifestyle choices…

By belligerently shouting out a preference of spending a share of their limited income on lattes, smashed avocados and holidays, the millennials are undermining their veracity of their claims about being squeezed out of housing. In what should be a definitive fact check on the issue, the RBA note that housing affordability now is at about the average of the last 30 years. But point that out and you are shot down with “it’s like, not affordable, like, where I live”.

Millennials do admit they cant have both, yet somehow, like the two year old with Thomas the Tank Engine and Peppa Pig’s deluxe play house who can only play with one toy at a time, their otherwise well trained minds are angry about this.

It’s Thomas or Peppa. It’s avocado and all that stands for, or a deposit for a house…

Worse still, the millennials unleash a Trump-eque fact flow which ignores all research from the RBA and data from the ABS and substitutes a hotch potch of opinion, falsities and made up ‘facts’. The house price often referred to by Millennials as they grasp at straws, is from a private sector firm that the RBA no longer relies on because the data were inaccurate. But that spoils the story because these (inaccurate) data show house prices in Sydney (it’s always Sydney and never Hobart) are about $200,000 higher than the accurate and reliable ABS house price measure.

The ABS may have stuffed up the Census but its house price data are sound. What’s more, for ones so worldly, the Millennials seem unaware that they don’t need a 20 per cent deposit to tap into the housing market…

The end point of all this is that people, young or old, can spend their income which ever way they want. If the boomers ate baked beans, drank international roast coffee and holidayed in a cockroach infested caravan on the beach while they struggled to enter the housing market, good on them!

Just as if todays millennials want to spend their hard earned income on lattes, backpacking in South America, craft beer and technology – good on them too!..

Economics worked 40 years ago. It still does.

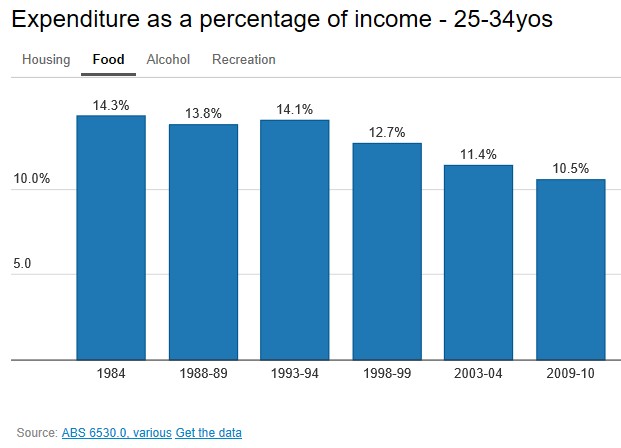

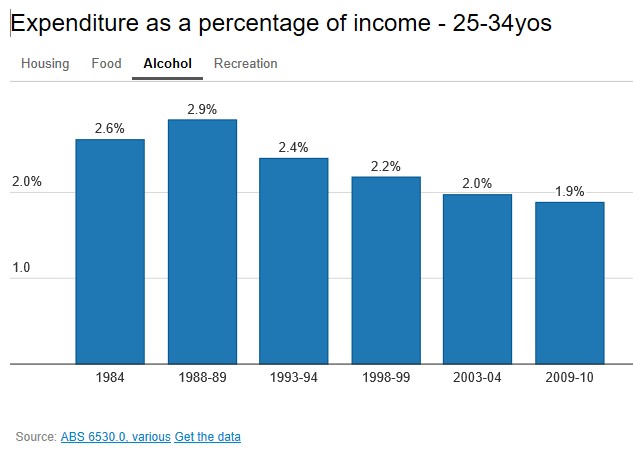

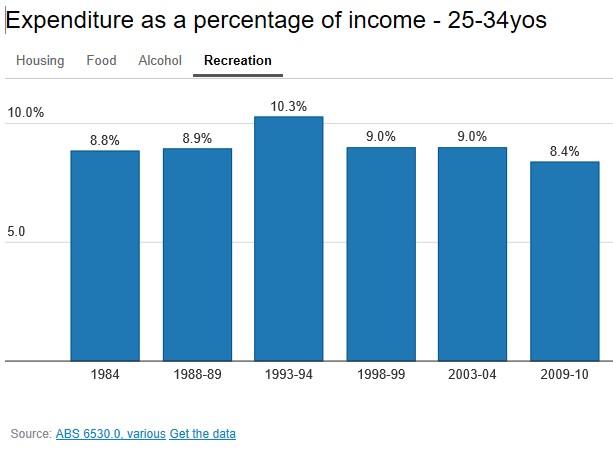

First, this notion that baby boomers were frugal whereas today’s millennials are wasteful does not pass scrutiny. The ABS publishes survey data on household expenditure and its shows clearly that in 2010, 25-34 year olds spent less on food, alcohol, and recreation (let alone tobacco) than they did in 1984:

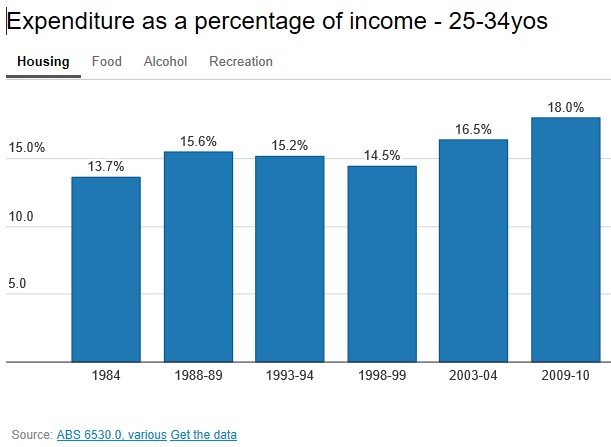

By contrast, they spent way more on housing than their baby boomer counterparts:

So it would appear that young Aussies are compromising on “spending and lifestyle choices” – more so than their baby boomer counterparts ever did.

Second, the notion that “housing affordability now is at about the average of the last 30 years” is easily debunked.

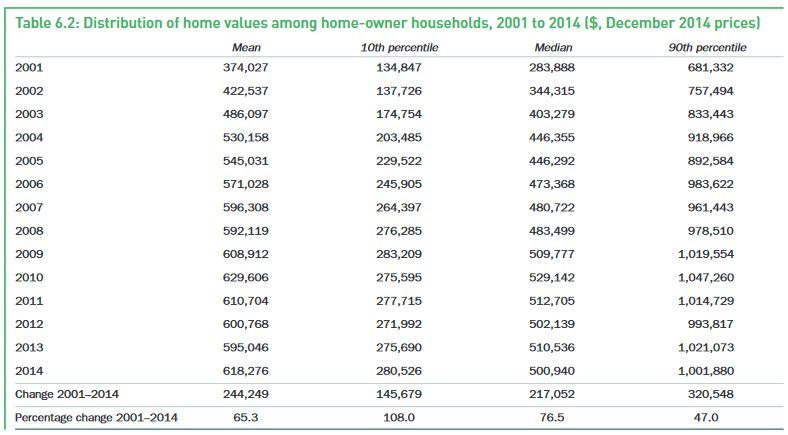

The 2016 Household, Income and Labour Dynamics in Australia (HILDA) survey, released in July, revealed that entry level homes – i.e. those priced at the 10th percentile and more likely to be purchased by first time buyers – skyrocketed in value between 2001 and 2014, rising by 108% over that period, compared to 47% growth for 90th percentile properties at the top end of the market:

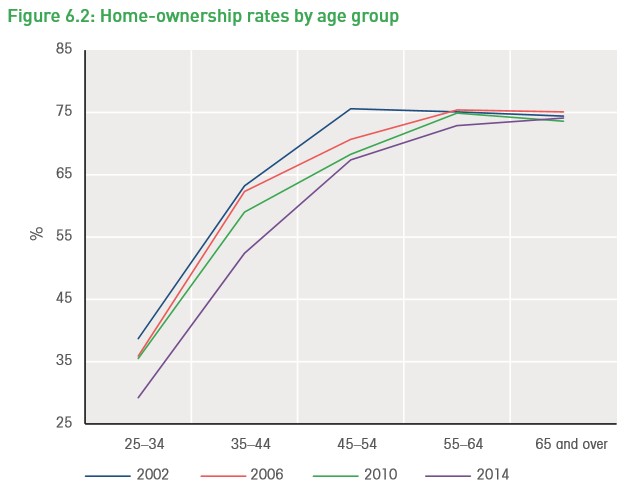

Not surprisingly, then, home ownership rates among younger Australians collapsed in the 12-years to 2014, according to HILDA:

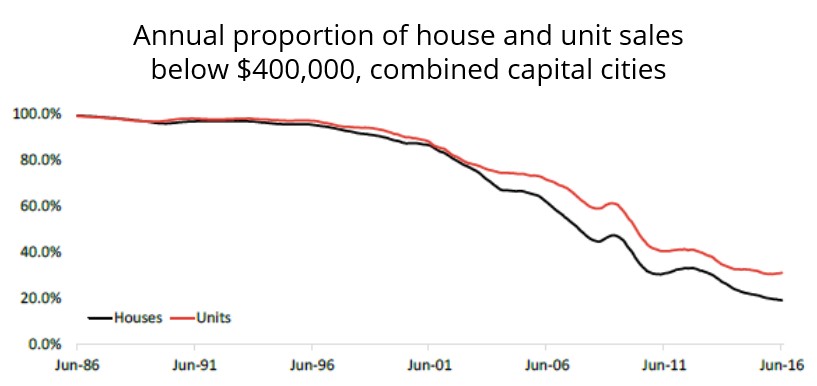

Consistent with the above, recent data from CoreLogic showed that less than one-in-five (19.1%) houses and less than one-in-three (31.0%) units sold across Australia’s capital cities were priced below $400,000, and that the number has collapsed. Thus there are fewer housing options available for first home buyers and those on lower incomes:

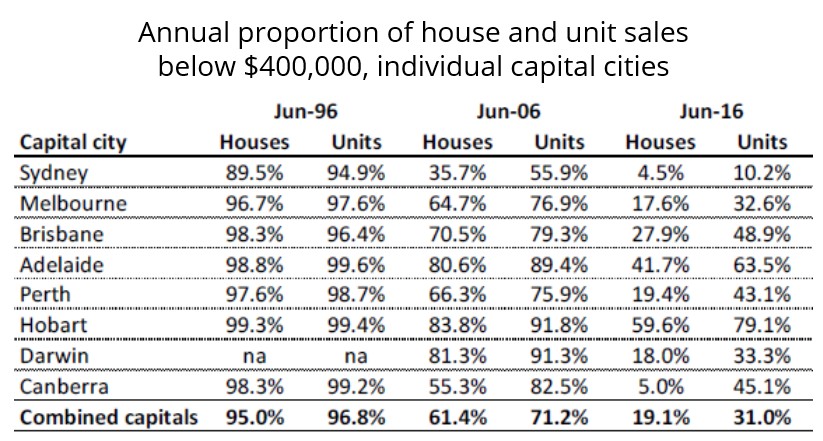

As expected, the situation is worst in Australia’s two biggest and most expensive markets – Sydney and Melbourne – with would-be buyers hard pressed to find much housing available below $400,000:

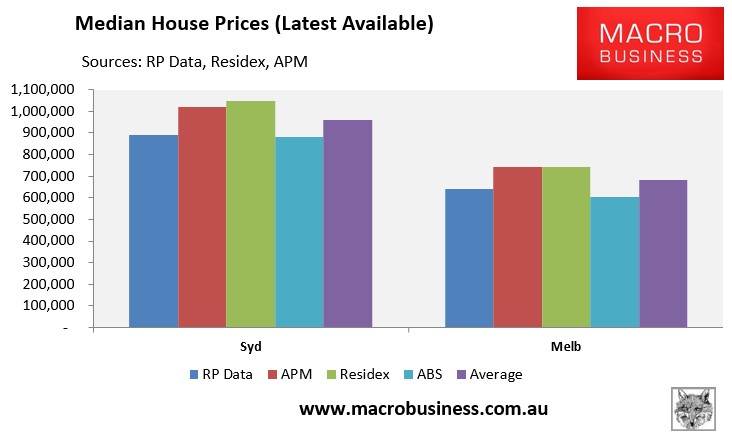

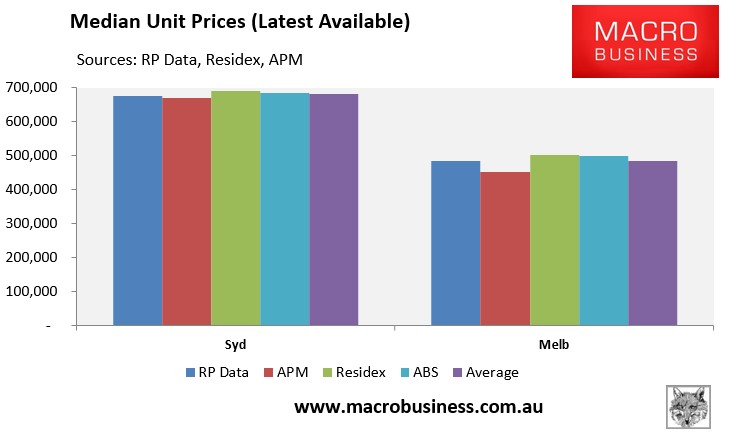

I know, the Kouk says that CoreLogic’s figures cannot be trusted. So I have compared them against the other three major data providers across Sydney and Melbourne:

Clearly, the affordability picture does not change if the other data providers are used instead. In Sydney’s case it is worse.

Finally, the Kouk’s claim that the RBA believes housing is just as affordable as 30-years ago does not stack up against recent statements from its governors.

Just last month, new Governor Phillip Lowe expressed his concern noting that “as a father of three children I worry … because people are paying so much for housing”…

Former Governor Glenn Stevens also expressed similar concerns about housing affordability on multiple occasions.

In 2010, Stevens lamented the fact that the high cost of housing in Sydney is making it increasingly difficult for his children to afford their own home:

“I’ve got kids that within not too many more years are going to want somewhere of their own to live, and you wonder how’s that going to be afforded because these prices are getting quite high”.

In 2011, Stevens again expressed concern that young Australians are being adversely affected by high housing prices:

“There’s a very big inequality between generations building up and I think that’s a social problem as much as any economic point”…

And in August this year, Stevens noted that high prices meant parents would have to help their kids get into the housing market:

“A lot of people of my generation are actually going to find themselves, if they haven’t already, helping their children into the housing market…

“Of course, if we come from a rental household ourselves, then we’re not going to have that equity to pass to the next generation, and certain types of disadvantage, therefore, are going to be perpetuated into that next generation.”

Hardly sounds like the RBA genuinely believes that “housing affordability now is at about the average of the last 30 years”, does it?

unconventionaleconomist@hotmail.com