The CEOs of Australia’s big four accounting firms have joined forces to lobby for cutting the company tax rate to 25% from 30% for all businesses, claiming that it would unleash a wave of prosperity on Australians. From The AFR:

We are adding our voices to the many, including the Federal Treasury, the Organisation for Economic Co-operation and Development and the International Monetary Fund, all of whom believe lower company taxes can deliver sustained benefits for Australian workers, businesses and the community more broadly…

Treasury’s modelling estimates that the company tax cut will eventually generate an additional $16 billion in GDP per year in today’s terms, and a 1.2 per cent increase in the purchasing power of our wages – that’s almost $1000 extra a year for the average full-time worker.

In a time where wage growth is anaemic we need to pursue this opportunity.…a five percentage point reduction in the company tax rate is a low-cost, low-effort and efficient way of permanently boosting Australians’ living standards.

It’s a lower company tax rate that will make Australia attractive to new businesses wanting to set up their operations here, and help existing businesses to grow and employ more people. It’s clear that the world will not stand still just because Australia fails to act…

This Parliament has a real, live opportunity to make an economic difference. Take the politics out of it and do something that will boost Australia’s competitiveness, create more local jobs and contribute to our shared prosperity for years to come.

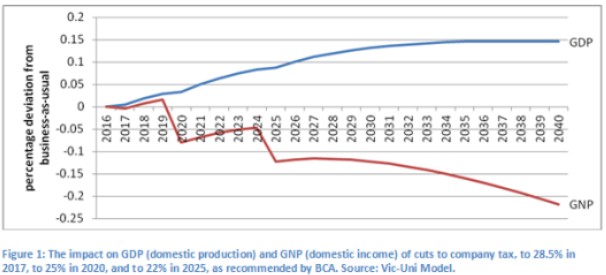

Surely delivering “sustained benefits for Australian workers, businesses and the community more broadly” would involve raising national income, right? Then why does modelling from Victoria University senior research fellow, Janine Dixon, show that cutting the company tax rate would actually lower national income (GNP) and living standards because the benefits would largely flow offshore:

What the Big Four’s CEOs have conveniently failed to mention is that Australia’s unique dividend imputation system means that domestic investors are largely unaffected by the company tax rate, since any profits paid to them are taxed at their personal income tax rate.

Hence, lowering the company tax rate from 30% to 25% would provide local owners and shareholders with minimal benefits, since any reduction in company taxes would be offset by a commensurate reduction in imputation credits.

By contrast, foreign owners/shareholders are major beneficiaries of a company tax cut because they cannot avail themselves of imputation credits. So a cut to the company tax rate provides them with the lion’s share of the benefits, and therefore represents a transfer from Australian taxpayers to foreign owners/shareholders.

Moreover, because of Australia’s dividend imputation system, many of the international studies about the economic impacts of cutting company tax rates are not readily applicable to Australia. So it is disingenuous for the Big Four CEOs to quote these as evidence for cutting Australia’s company tax rate.

The huge cost to the budget from cutting company taxes would also need to be made up by either raising taxes elsewhere or cutting government expenditure on public services and/or infrastructure – neither of which is desirable and could easily raise economic costs elsewhere.

We should also not forget that the modelling used to support the company tax cut showed minimal benefit to either GDP or employment, as explained by The Australia Institute’s Richard Denniss:

According to Treasury’s in-house modelling, and the modelling it commissioned from Chris Murphy, if the company tax rate is lowered from 30 per cent to 25 per cent then gross domestic product will double by September 2038, while without the tax cut it won’t double until December 2038. Wow, a whole three months earlier. Both modelling exercises conclude that in 20 years’ time the unemployment rate will be 5 per cent regardless of whether we spend $50 billion on company tax cuts or not…

The “benefits” are more accurately described as rounding error than significant reform.

The Grattan Institute has come up with similar conclusions, while also noting that national income would likely be lowered by cutting company taxes, at least over the first decade.

With the Federal Budget facing immense structural pressures and a “revenue problem” – as acknowledged by Treasurer Scott Morrison in his recent speech – where is the sense in gifting tens-of-billions of dollars to foreign owners/shareholders, and in the process worsening the Budget position and lowering national income?

The are far greater national priorities than cutting company taxes.