Australia has just concluded its 25th year of consecutive economic growth.

This has not occurred by accident – it is the product of more than 30 years of economic reform and hard work, ingenuity and sacrifice from millions of Australians.

Events have both assisted us and challenged us – but overall we have prevailed, where so many other countries have failed.

This remains true, and is demonstrated by the successful transition underway from the investment phase of our mining boom to a more diversified economy that can set us up for yet another generation of growth.

Today, we have one the highest rates of economic growth in the advanced world. At the G20 there is no other place than Australia’s where you would rather be seated.

We should acknowledge our relative success. But there is a terrible risk that our continued success has been steadily sowing the seeds of complacency.

A generation has grown up not ever having known a recession, of seeing unemployment rates at more than ten percent, with one million Australians out of work or mortgage rates at 18 per cent or where inflation is actually a problem, rather than an aspiration.

In addition, a generation has grown up in an environment where receiving payments from the Government is not seen as the reserve of those who unfortunately will be forever dependent on support or in need of a hand up, but a common and expected component of their income over their entire life cycle.

On current settings, more Australians today are likely to go through their entire lives without ever paying tax than for generations. More Australians are also likely today to be net beneficiaries of the Government than contributors – never paying more tax than they receive in government payments.

There is a new divide – the taxed and the taxed nots.

Deficits are dismissed as temporary, cyclical and self-correcting. If it means payments and services are maintained, then deficits are ok, just increase the taxes or increase the debt. The only problem is fewer people are paying the taxes, as our working age population contracts relative to the balance of our population and our population ages.

After so many years of growth, we must ask ourselves a few hard questions.

Are we still up to the challenge of doing what we need to do to ensure another 25 years of consecutive economic growth?

Are we more interested in preserving the benefits of what the past 30 years of economic reform has given us, than relinquishing and re-investing some of those dividends to create a stronger economy for both our own future and the generations that follow?

Do we any longer appreciate the consequences of what actually happens when it all goes south, as we did more than 25 years ago when we had the recession we had to have?

Do we really appreciate how quickly our economic success can turn, and are we as prepared as we can be to deal with it, as we were when the last crisis hit, thanks to the Howard Costello Government?

The next generation will know how well and how quickly we answered these questions by the Australia we leave them, by how much debt they will have to repay, by the taxes they will be forced to endure and the standards and access to services they are able to afford, and therefore have to accept.

My greatest concern is that we end up answering these questions too late and the hard way.

There are some who seem to wish for a burning platform to bring about the changes that are necessary – as occurred in other jurisdictions, such as Europe and the UK, but I am not one of them.

I do not want my kids to know what a recession is and everything that goes along with that.

I recognise that in the absence of a ‘recession we have to have’, or the threat of ‘becoming a banana republic’, achieving necessary change will be more frustrating and more difficult. But it is no less necessary, and achieving it this way is far better than the alternative.

In the next five to seven years we have a window of opportunity to prepare our country for what lays ahead and to set our nation up for a new generation of growth and prosperity.

As a re-elected Government and a newly elected Parliament there are three things we must do over the next three years. I will expand further on these points in the weeks and months ahead.

Firstly, we must take action to strengthen our economic resilience to deal with the shocks that will inevitably come – to get debt under control by returning the budget to balance through disciplined expenditure restraint and a tax system that supports growth and provides sustainable revenues. We must also build on the strength, integrity and resilience of our banking and financial system. These are my topics for today.

Secondly, we must support and implement policies that help us to increase what we can earn as a nation, as businesses and as individuals in a low growth, low interest rate, low inflation, low wages growth, volatile world.

While the GFC was many years ago, the effects continue and will be felt for years to come, the world over.

We need to earn more from what we do and what we produce. This is how we lift real incomes. This is not just an Australian problem, but a global one, and we are faring better than most.

In this global economy we have to fight for every inch of growth and for every dollar, yuan, yen and euro we can get.

To achieve this we must lift our levels of private investment, to replace what has been exhausted in the mining sector, to boost our productive capacity.

Global capital is sitting dormant. How else do you interpret the absurdity of negative bond yields – where it is apparently better to give the German or Japanese Government your own money for a decade only to just get it back and pay for the privilege rather than invest in a productive enterprise.

The response of Central banks and Governments around the world has been to exhaust monetary policy with rate cuts and QE and collapse their budgets with fiscal stimuli in the hope that it can replace the vacuum created by the evacuation of private capital.

The outcome has been private capital remaining on the sidelines while public debt soars to new records and cash rates go negative as central banks push against the string.

Private capital is looking for something to invest in. Something that creates value. Real income earning projects and enterprises. An economy where growth is organic, rather than fabricated and reforms are unlocking value and creating opportunity.

This is the type of the economy that can coax private capital out of its cave. That is our task.

That is why the Budget in May was not just another budget but an economic plan for jobs and growth.

A plan to drive investment, to drive innovation, to transform our defence manufacturing industries right across the supply chain, to reduce the tax burden on investment and enterprise, to open up our enterprises to new markets through more new export trade deals, to develop infrastructure that underpins investment and to remove the impediments to investment in critical sectors such as construction by restoring the Australian Building and Construction Commission. This is the course we must stay.

This is where the jobs will come from. This is where wages growth will come from. This is where the profits will come from and this is where the revenues will come from – not from increasing the tax burden on the economy.

And thirdly, we must keep our doors open. We must keep the drawbridge down.

In today’s global political environment, trade, investment and positive immigration policies are increasingly seen as the problem and not the solution. At the same time, more of our citizens want to believe that they can be insulated from what is occurring globally by disconnecting from the very sources of our own economic prosperity for centuries. We must face up to their concerns and address them.

Many Australians feel the system no longer works for them and indeed works against them. It is politically popular to endorse this sentiment. There is great danger in taking such a cynical approach.

As a government we know that trade, foreign investment and positive, well controlled immigration focussed on bringing those to Australia who come to make a contribution rather than take one, creates jobs, drives growth and always has.

There is more than three trillion worth of foreign investment in Australia today, with an annual inflow of around $200 billion. In 2015, our global export volume trade, including our tourism and international educations sectors, delivered around $363 billion to our economy and accounted for around 19 per cent of our GDP and around 1.3 per cent of annual growth.

We cannot pull the doona over our head by taking false comfort in renewed protectionism. Rather than secure our economic future, it will cost it.

Today I want to discuss further our ongoing work to strengthen Australia’s economic resilience in the face of the real global economic threats and uncertainties we face.

When Australia last faced an historic global economic shock – the GFC, we were well prepared. Our nation’s finances were in order, our AAA credit rating was in place and our banking and financial system was strong – it was well regulated, well capitalised and well managed.

To ensure we are prepared for whatever events may occur in the future we have much more work to do, especially in the area of budget repair, to strengthen our nation’s finances.

This was the core component of the national economic plan for jobs and growth set out in this year’s budget, that we took to the election and was endorsed. We intend to now deliver that plan. And it will be necessary.

The muted impact of Brexit recently reminded us of the type of events that really don’t impact on our economic circumstances at home.

However, if similar shocks emanated from within our own region and key trading partners, especially China, or the United States, the impact would be far more dramatic. We learned this during the GFC in reverse where China’s stimulus proved to be more important than our own.

Looking forward, the growth outlook in the US is modest, but stable.

However, in China, events may prove far less predictable. Interesting times may lay ahead, and we must prepare.

The good news out of China is that the transition of their economy from production to consumption is synchronising well with our own transition to broader based growth, particularly in the services sector.

Our trade agreement further enhances these opportunities. Few countries could better hope to continue to benefit from the economic upside of China than Australia.

While China’s growth is slowing, it continues to grow at 6.7 per cent, off a much higher base. And there is a clear commitment from the Chinese leadership that growth remains the goal. It is essential to their stability as a nation, and always has been.

The issue that arises is how this growth continues to be sustained and what the risks are for Australia.

China has been no more immune to falling private sector investment than other economies. China’s response to falling private investment has been to dramatically increase their public investment through their SOEs in the most significant way since the GFC.

Compounded with the activity of local government administrations, China’s debt levels are now rising steadily at 13 per cent per annum and are more than 250 per cent of GDP.

More than half of this debt is essentially government debt, with SOE’s now accounting for more than half of all corporate debt. Bank loans account for around 70 per cent of the total debt at the end of 2015.

At a macro level, in isolation, this is not evidence of a problem. China has more than sufficient foreign reserves. The Bank of International Settlements estimates China’s foreign currency denominated liabilities at around 7.5 per cent by end 2015. By comparison, prior to the Asian Financial Crisis, borrowing from international banks from Korea, Indonesia and Thailand was between 24 per cent and 50 per cent.

The issues arise at the micro level. What is the composition of this debt? How is it being managed, what are the assets underpinning it and what is the profitability of the enterprises and the quality of the revenue streams servicing it?

The ability to repay loans is deteriorating as profits continue to deteriorate, especially for SOEs. The level of non-performing loans has increased by 126 per cent since 2013.

The IMF estimates NPLs at 7 per cent of GDP, not including exposure to the shadow banking sector, whose assets grew by 30 per cent in 2015 and now stand at 79 per cent of GDP or $US 8 trillion.

The growing size of the shadow banking sector means that during a liquidity tightening, difficulties could arise replacing shadow banking credit, leaving borrowers who rely on such financing at risk of a credit crunch.

Add to this that China has an unfunded social security liability of around 70 per cent of GDP in 2015 for the period 2015-50, and we can see an increasing number of balls in the air.

The IMF advises that taking further steps now to pursue structural reforms in the SOE sector and curbing local government borrowing would have immediate and short term impacts on China’s growth rate. This would also impact Australia. However they argue the benefit would be a more sustainable growth rate moving forward.

While some actions are being taken, such as the local government debt swap program, it is clear that driving growth is the top priority.

Based on the IMF’s assessment, a no reform option will see China’s growth hold up above baseline until the end of the decade, but after that, continue to head south rather than stabilise. Australia would not be isolated from the effects of that outcome either.

Of course all of these decisions are outside our control and are an entirely a matter for the Chinese Government to determine in accordance with their own national priorities.

What is more important is to ensure that whatever the outcome, we ensure that Australia is as resilient as it can be.

This requires two priority responses:

Firstly, we must arrest the growth in our public debt, before it is too late, by getting expenditure under control at sustainable levels and boosting revenues through growth friendly tax policies and protecting the integrity of our tax base.

Secondly, we must continue to reinforce and build on the strength of banking and financial system.

As a Government we inherited $240 billion in accumulated deficits and a debt of $317 billion, and projected to increase to $667 billion within next ten years. As a Government we have so far acted to reduce that projected debt by $55 billion. However we are still a long way from where we need to be, and time is running out to get there.

Our debt now stands at around $430 billion, with interest payments at $16 billion this year, now one of the largest line items in the budget and growing.

Our CGS on issue, our gross debt, is increasing by $6 billion a month or $1.4 billion per week in 2016/17 ($72 billion for the year).

While our debt is low by global standards, and our placements are well covered, this is no excuse to be complacent about debt.

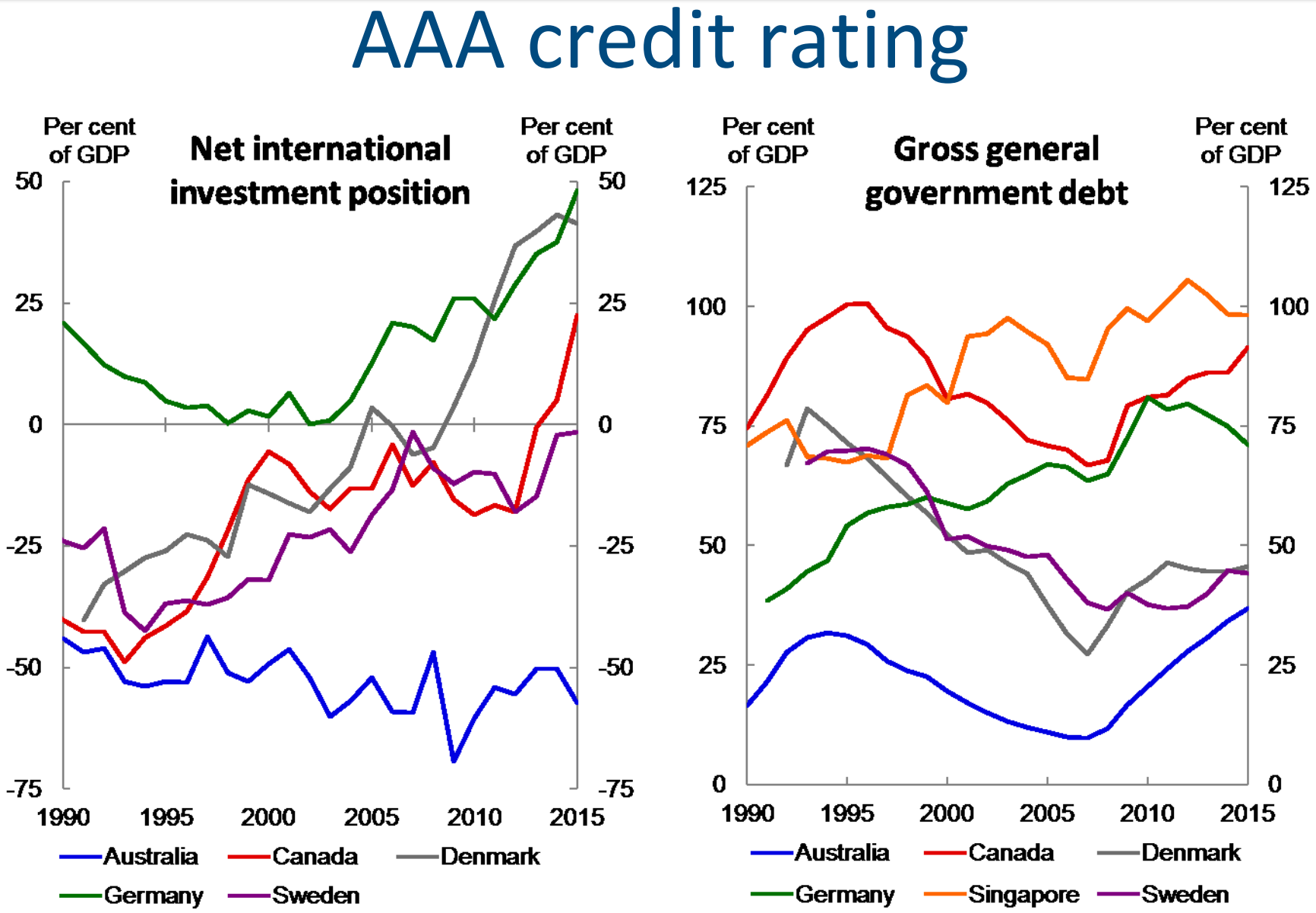

Our government debt to GDP is well below other AAA rated countries. However our net international investment position is the inverse.

This is because Australia has always been a net importer of capital, especially in the private sector. This has been a key source of our prosperity and development. Of itself, this is not a problem, as the investment is supported by real assets and is in productive enterprises.

However, it does mean we have less head room for Government debt than other advanced economies that fund their own debt, and why ratings agencies tend to be very focussed on Australia’s deficit and debt position. All Australian Governments must therefore be more conscious of our collective debt position. Just because rates are low, doesn’t mean the money is free – you still have to pay it back.

To arrest our debt we must restore the budget to balance.

Deficits have proven difficult to shift in recent years, despite applying significant expenditure controls. The situation has been made even worse by the budget sabotage engaged in by the Opposition during the last parliament and the unwillingness of the previous Senate to enable the Government to implement our agenda for budget repair.

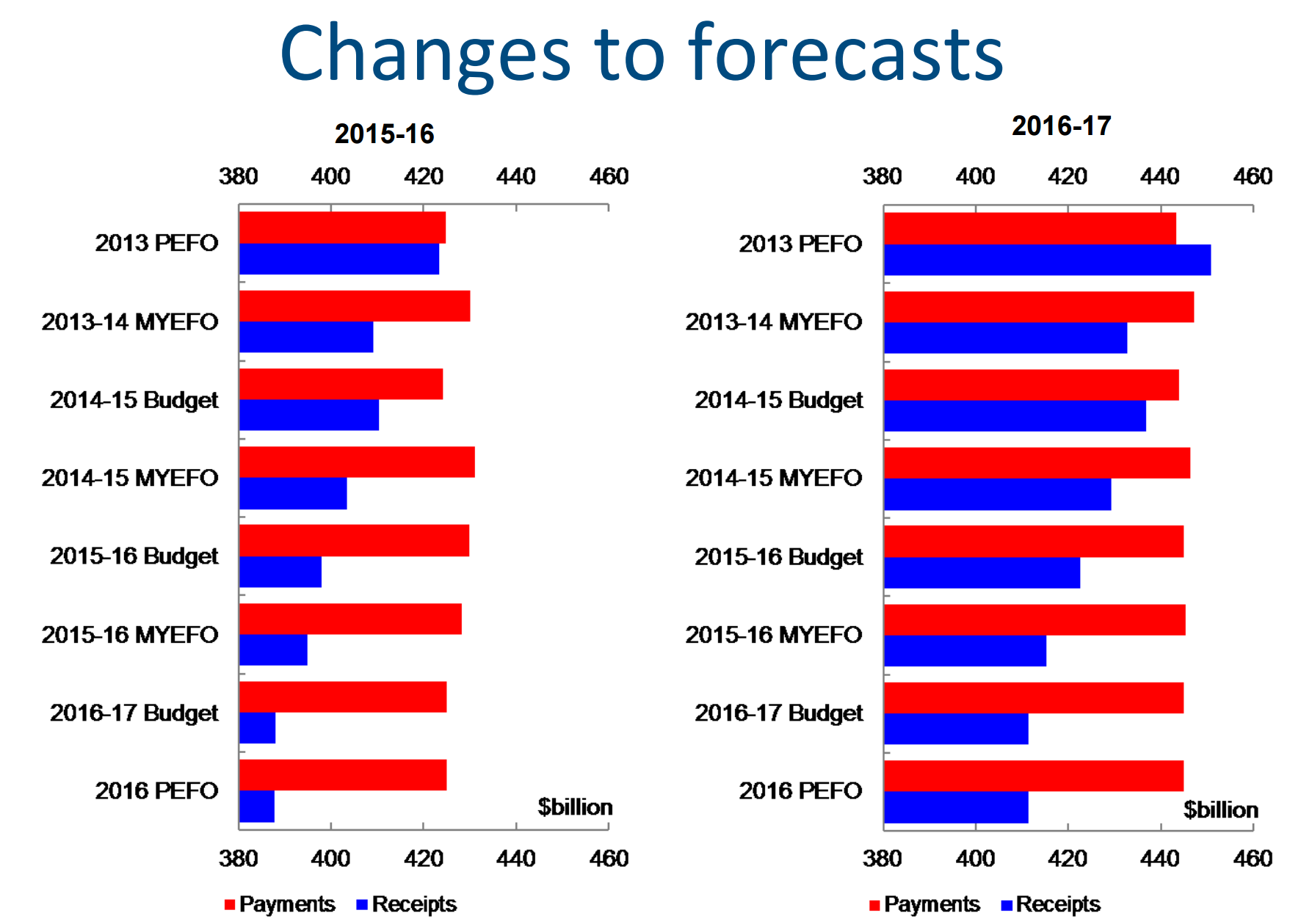

Despite these challenges, since the 2013 PEFO, even in nominal terms, we have kept expenditure under control. In 2013, the PEFO statement estimated Government payments in 2015/16 would be $425 billion. In the 2016 PEFO, which mirrored this year’s Budget, the estimated expenditure was the same at $425 billion. This outcome was replicated in the comparison for 2016/17.

However, the projected revenues set out in the 2013 PEFO were not realised. The revenue estimate for 2015/16 fell by $35.5 billion and for 2016/17 fell by $39.5 billion by the 2016 PEFO statement. These declines match closely the projected deficits in each of these years.

During the same period forecasts for nominal GDP growth in both years were reduced from 5¼ per cent to 2½ per cent. As noted before, we earned less – the reduction in the terms of trade, commodity prices, in wages and in profits – than had previously been anticipated.

In other words, we have an earnings problem.

Our nominal growth today is lower than our real growth, by a full percentage point. This is an uncommon predicament and a core challenge in working to bring the budget back to balance. We are not being assisted by the tail winds that supported previous periods of successful fiscal consolidation, including in the lead up to the GFC.

However, we cannot take this as an invitation to increase the tax burden on the economy, especially on investment. This is not the way to remedy this problem. You don’t encourage growth by taxing it more. This is why we have consistently rejected Labor’s tax and spend approach.

It is, however, necessary to act to protect the revenue base from structural weaknesses, to ensure the base is contemporary and ensure that taxes are paid – as the Prime Minister said, taxes should be as low as they can be, but they must also be paid.

That is why we have introduced our tough new laws to crack down on multinational tax avoidance, including our new diverted profits tax introduced in the budget. It is also why we have moved to tax digital products and services and remove the GST on bitcoin and deal with the tax challenges of the shared economy. And it is why structurally – not because of any malfeasance – we have recalibrated the way generous tax concessions are provided in the superannuation system and to ensure that these incentives are aligned with their purpose as proposed in the Murray review.

These measures will support protecting our revenue base, but budget repair must always start with getting your expenditure under control and keeping it at sustainable levels.

Current projections show that expenditure as a share of the economy remains stubbornly high. While expenditure is projected to fall from 25.8 per cent to 25.2 per cent, revenue as a share of GDP rises more quickly, with bracket creep being the principal contributor.

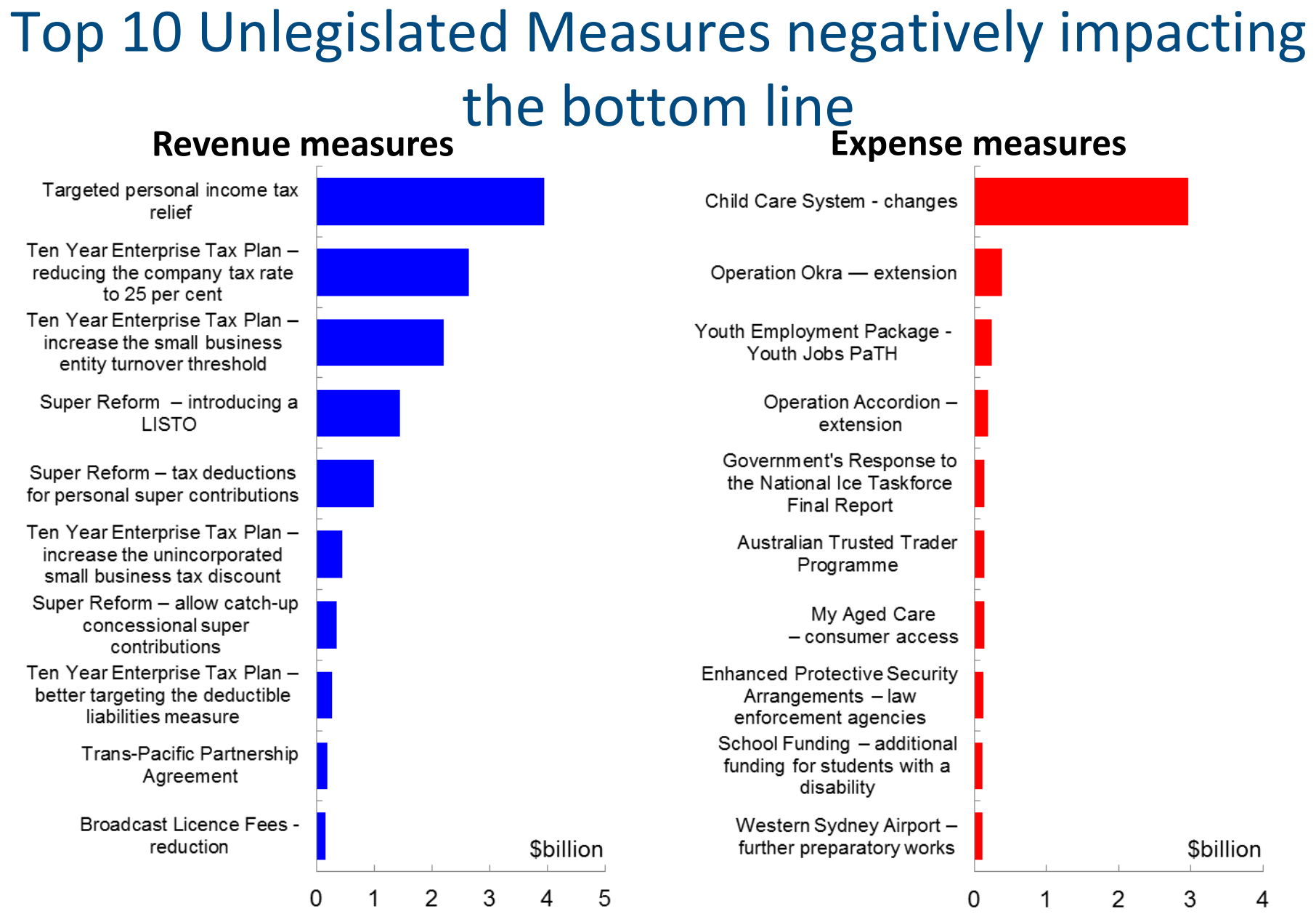

That said, of the $40 billion in budget improvement measures that are as yet un-legislated, $25 billion, more than 60 per cent, constrain spending, while just over a third, or $15 billion, increase revenues. In other words the policy emphasis of our measures to improve the budget is on controlling spending, rather than increasing revenue.

The bulk of our savings measures on outlays are not surprisingly weighted to the largest spending portfolios, in particular social services. Reigning in the growth in welfare spending is one of the most difficult challenges confronting the budget.

In most cases these initiatives on spending are designed to flatten the growth curve in future costs – no different to what any business in the country seeks to do in response to the demands of their customers. Where the growth in your costs is greater than the growth in your revenues, then you have a problem.

Customers demand better standards of services at lower costs. Citizens are no different. We have to work together to find better and more innovative ways of delivering our services, particularly in areas such as health, education and human services that delivers for citizens and is affordable and sustainable. Professor Harper’s report, which has been taken up by the Government is guiding our approach in addressing these challenges.

In addition to these measures there are also important revenue and expenditure measures that are key to our national economic plan. Improving the flexibility of superannuation, reducing taxes for small and medium sized businesses and average full time wage earners, supporting start-ups and making child care more affordable to support work force participation.

The net impact on budget improvement measures after talking these other measures into account over the forward estimates is more than $18 billion. This is a clear plan, with real measures that we are determined to see supported through the Parliament.

Whether the measures that are necessary to return to budget balance are supported is yet to be seen. The first test will be seen when the Opposition will have to decide whether to honour their commitments in the election to support the more than $6 billion in savings measures on expenditure that they included in their own budget costings during the election.

As the Prime Minister said yesterday, we are asking Labor to vote for measures they have already said and indicated they support. But this cannot be the end of the process. We expect their support for other revenue measures such as tobacco excise, which will follow. But we also expect them to engage on expenditure savings they have habitually blocked. At the same time we will be putting these questions to the cross bench in the Senate and the Greens.

Ratings agencies have all warned that they want to see budget measures passed or this will increase the risk of a rating downgrade. They have expressed serious doubt about whether this parliament will be up to the task.

The consequences of the alternative are too stark.

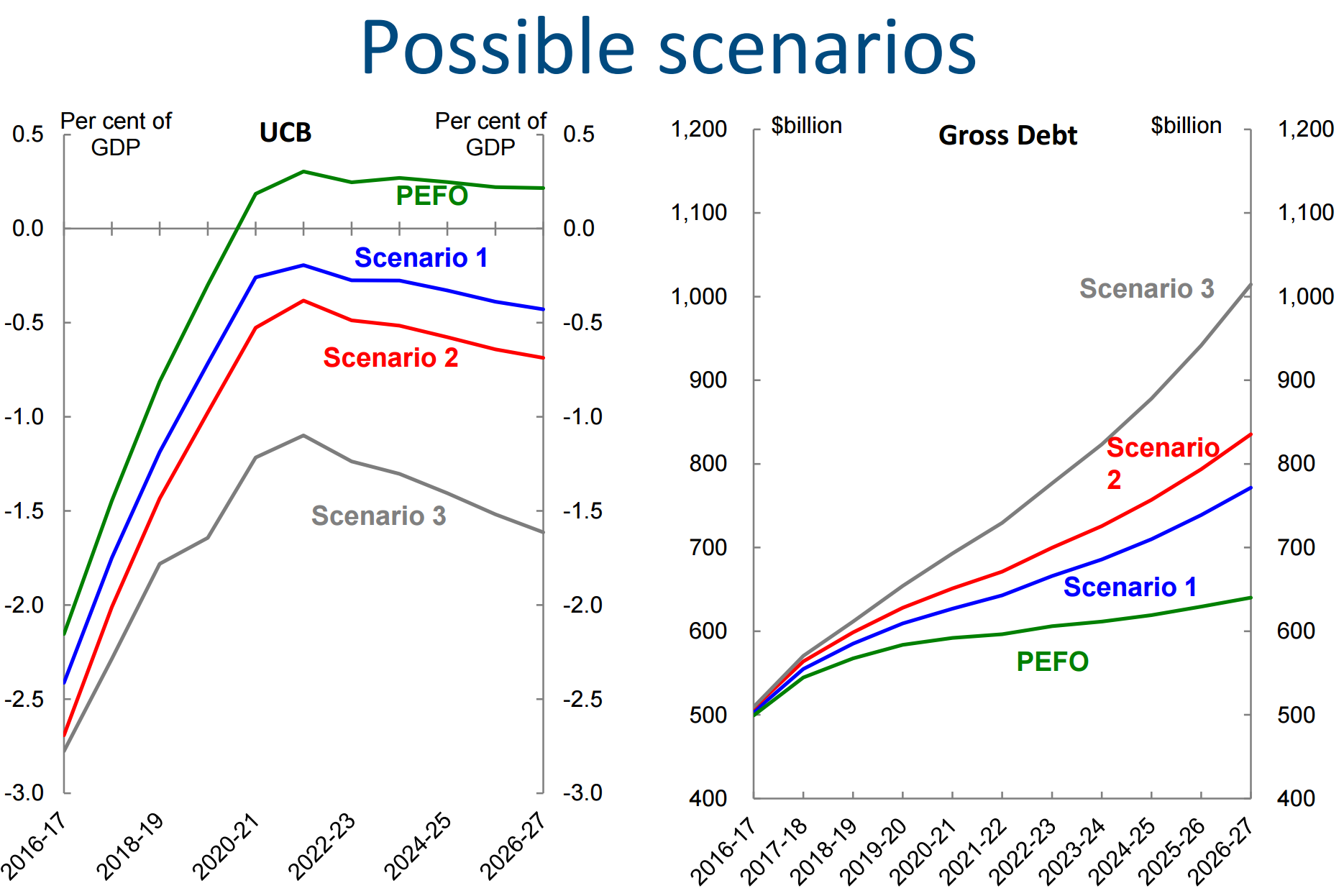

Deficit and debt projections prepared by Treasury estimate the impact of three scenarios. The first involves only the $25.3 billion in budget improvement measures including the omnibus savings bill and other non-contentious measures being passed and additional spending pressures, such as the PBS, state partnership agreements and the like coming onto the budget. $14.6 billion in other budget improvement measures would be reversed.

Scenario 2 includes everything in scenario 1, with further downgrades due to economic parameters in the order of $18 billion over four years. Scenario three assumes all currently un-legislated measures are unsuccessful.

The worst case scenario will see our gross debt exceed $1 trillion in a decade. The other scenarios place debt just above and below $800 billion. In all three scenarios the budget does not return to balance, and over the medium term, we are moving away from that goal and not toward it, as major expenditure items like the NDIS start to fully kick in.

These scenarios set our stark choices. Our plan makes the choice to combine measures to drive growth to support revenues, while getting expenditures under control so they can be sustained at levels where the Government is living within its means.

The period of this term could well prove to be the tipping point on the trajectory of debt our children and grandchildren will be saddled with. Once that debt fully takes hold, it will build its own momentum and will only grow more difficult to tame.

I choose to maintain an optimistic disposition. I remain optimistic about Australia’s future growth and will work with the Parliament to secure the right result.

Finally we must also not take for granted the strength of our banking and financial system.

This is arguably one of our most important assets we have when it comes to driving and facilitating growth in our economy, to support jobs and to boost incomes. That is why, as a Government, we have acted to further strengthen the system.

Earlier this year when the Opposition proposed a royal commission into our banking system, terms of reference still outstanding, the then Assistant Treasurer Kelly O’Dwyer was in Washington for IMF meetings, where she was approached and asked what is wrong with Australia’s banking system.

Labor’s careless approach and cynical politics on this issue is a genuine risk to broader confidence in our banking and financial system which can only weaken the system.

Rather than engage in cynical politics, the Government understands the importance of our banking and financial system and has been working to strengthen the system for borrowers, depositors and shareholders alike.

Our objectives are to improve consumer outcomes, further strengthen the regulatory architecture, drive innovation in areas such as Fintech and crowd source funding and further build system resilience.

Most significantly, has been the conduct and response to the Financial Systems Inquiry by David Murray Inquiry.

This has already produced results.

APRA advise that according to their update in July the banks now broadly achieve the relative positioning on capital strength suggested by the Financial Systems Inquiry.

The Crisis management tool kit legislation will make its way back into this parliament to strengthen APRA’s crisis management powers over the banks.

This year’s budget reforms to superannuation were driven by Murray’s call to make concessions fit for purpose, and the Government is working to deliver improved governance of superannuation funds and greater choice for consumers in selecting their funds.

Interchange fee and customer surcharging restriction are being activated. Corporate administration and bankruptcy reforms have been taken up in the National Innovation and Science Agenda. Unfair Contract terms legislation was passed in the last parliament

And we acted to strengthen the powers and resources of ASIC to deal with direct failures and malfeasance within the banking system as also recommended by the FSI. APRA has also been active in this space, focusing on aspects of bank governance, culture and remuneration that promote sound risk taking.

We are working to put in place improved dispute resolution mechanisms across the sector, not just in banking, that gives customers better access to having their matter heard and determined on a more level playing field. The Ramsay review announced by Minister O’Dwyer a few weeks ago, will advise the Government on how to put such a new tribunal in place, and will obviously draw on the work done by the PJC on Corporations and Financial Services.

The House of Representatives Standing Committee will now take on a permanent watching brief on the banking and financial sector, in the same way it conducts hearings with the Reserve Bank. This measure will provide a new forum for accountability and transparency, including a standing report on the Banks own efforts to transform bank culture.

In my own engagement with the banks leadership, there is both a recognition and commitment to deal with this issue. I agree with those in the banking sector who have said they believe the key to making this cultural shift is to restore banking as a profession. A professional banker should serve their clients like a doctor cares for their patients.

Now the medical profession is not perfect either. But I agree that such an approach is a good place to start.

These are all real examples of how as a Government we are both acknowledging and acting on the concerns and issues that Australians have about the banking and financial system. Such concerns have to be addressed. Our approach is to deal practically with these issues and address them.

We are in even better shape today when it comes to the resilience of our banking and financial system than we have ever been, but as always we cannot be complacent. This should not be an invitation to take cheap shots and undermine the system, but to continue work constructively to further improve it.

As we face the challenges of the future we can we take the easer route of higher taxes and leave spending untouched. We can appropriate the budget to fill the vacuum left by private investment rather than pursue policies that will re-engage private capital. And we can shut the door and jump under the doona and hope it all goes way, or we can recognise that continuing to be a successful open economy has always been and will always be our ticket to prosperity.

This is what our national economic plan for jobs and growth has always been about. Making the choices that will set Australia up for another generation of economic success. The Turnbull Government is up for it and we will seek to lead the nation along this path. I believe Australian’s are up for it. In the weeks and months ahead we will learn the extent to which the Parliament will be supporting the Government to implement what we promised and give the Australian people the economic leadership they voted for in returning the Government.

A few points:

not a bad fist of it but because it’s not situated within any broad economic narrative of structural post-mining change who cares?

that is, where does this take the country, Scott (and Malcolm)? Not to some magical services-driven China engagement that stalled a year ago;

Budget repair is welcome but it will fail without productivity, innovation, competitiveness and changing growth drivers, not just lower service provision and taxes. The government’s agenda on this front, the most important of all, is laughable: “A plan to drive investment, to drive innovation, to transform our defence manufacturing industries right across the supply chain, to reduce the tax burden on investment and enterprise, to open up our enterprises to new markets through more new export trade deals, to develop infrastructure that underpins investment and to remove the impediments to investment in critical sectors such as construction by restoring the Australian Building and Construction Commission. This is the course we must stay.” In reality that is an innovation advertising campaign, pork for Chris Pyne, defending negative gearing plus giving foreign shareholders free money, useless and distorting FTAs, a few less strikes on building sites and some light rail in Sydney and Melbourne as a gesture at back-filling population growth choked eastern cities. Some of it is certainly welcome but this is place-holding not revolution or even reform; status quo protection of rentiers and ponziers while the outsiders wear a lot of pain that produces nothing new;

the opportunity for Budget repair is not the next 5-7 years, it’s now by design or soon enough by crisis. Notice how fast Australian debt is growing versus all other AAAs. Moreover, the external imbalance that Morrison points to as undermining the rating is driven by the very economic model that Morrison’s plan will make worse. Cutting public spending will lower growth and interest rates and push up the very useless foreign borrowing for house price growth that is the core of the imbalance. What Morrison needs is structural reform that cuts the Budget for repair and changes the patterns of Australian growth.

Labor has no incentive to support Budget repair when the Government will be blamed for losing the AAA rating and on that basis I would say that Morrison’s ‘scenario two’ is the real base case and ‘scenario three’ is more than just possible except for the fact that we’d be forced into severe austerity long before it came true.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.