The Grattan Institute has lodged a submission to the Senate Inquiry into the Treasury Laws Amendment (Enterprise Tax Plan) Bill 2016, which argues against cutting company taxes.

Below is the summary of the submission:

This submission evaluates the case for the Government’s plan to cut the company tax rate from 30 to 25 per cent over 10 years.

It is an article of faith in Australia’s business community that corporate tax cuts are the big lever for increasing economic growth. Australia’s corporate tax rate is high relative to most developed countries. OECD studies show that lower corporate tax rates tend to lead to higher investment and hence higher economic output. Many studies – including the 2012 Game Changers report for Grattan Institute – picked up this research and highlighted company tax cuts as one of the big opportunities for government to increase prosperity.

Yet ironically legislation to cut the company tax rate over 10 years has been introduced at the precise time that doubts are growing about the payback of corporate tax cuts, especially for countries such as Australia that have dividend imputation systems. Australia’s unusual dividend imputation system means that domestic investors are largely unaffected by the company tax rate since any profits paid to them are taxed at their personal income tax rate. Yet because foreign investors, by contrast, do not benefit from dividend imputation, a cut to the company tax rate provides bigger benefits to them. For those who have already made long-term investments in Australia, a reduction in the tax rate would be a windfall. Many of the international studies about the economic impacts of cutting corporate tax rates are therefore not readily applicable to Australia.

The Government maintains that the change will boost GDP by more than 1 per cent in the long-term, at a budgetary cost of $48.2 billion over the next 10 years. But the best analysis from the Commonwealth Treasury shows that the net benefits to Australians’ incomes will be much smaller once profits flowing out of Australia are taken into account. Raising other taxes to compensate for the foregone company tax revenue will create their own economic costs. Because additional corporate investment will phase in slowly, the benefits of company tax cuts for Australian incomes will be a long time coming. And the substantial costs of the measure in the short term could see company tax cuts drag on national incomes for the next ten years. Weighing the balance, it is not clear that corporate tax cuts should be Australia’s top priority.

Instead, wholesale company tax cuts should be deferred until we have eliminated the large and persistent budget deficits that increase the vulnerability of the Australian economy, and drag on future incomes. In the interim, corporate tax reform should focus on providing tax cuts in ways that minimise the windfall for existing foreign investors. Options include an investment allowance or faster depreciation rates that only apply to new investments.

The submission also explains in detail why Australia’s dividend imputation system is such a game changer and renders international studies supporting company tax cuts largely irrelevant for Australia:

Advertisement

Australia’s unusual dividend imputation system means that when profits are paid out, they are only taxed at the domestic investors’ personal income tax rates. A company tax cut does not help them much since their effective company tax rate is already close to zero. This system is known as a franking credits regime and other few developed countries have it.

Most countries tax corporate profits, and then investors also pay personal income tax on the dividends (albeit sometimes at a lower rate). As a result, although Australia has a relatively high headline corporate tax rate compared to our peers, in practice the comparable tax rate is lower – at least for local investors.

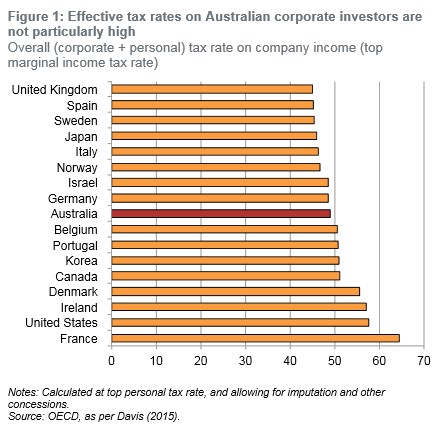

By contrast, corporate taxes have a much bigger economic impact in other OECD countries where they reduce the rate of return for local investors. International comparisons show that Australia has a median level of taxes on corporate profits for local investors when both company taxes and individual income taxes are considered (Figure 1).

Consequently, many of the international studies about the economic impacts of cutting corporate tax rates do not readily apply to Australia. Local shareholders do get one benefit from cutting corporate tax rates. If companies pay less tax, then they have more to reinvest, so long as the profits are not paid out to shareholders. Yet in practice, most profits are paid out.9 Therefore a company tax cut will generate little change in domestic investment.

Foreign investors, on the other hand, do not benefit from franking credits. They pay tax on corporate profits twice: first at the company tax rate, then as income tax on the dividends at home (potentially at a discounted rate). Therefore a cut to the company tax rate provides bigger benefits to them. For those who have already made long-term investments in Australia, a reduction in the tax rate would be a windfall.

The submission then explains why cutting company taxes would likely reduce national income, at least over the first decade:

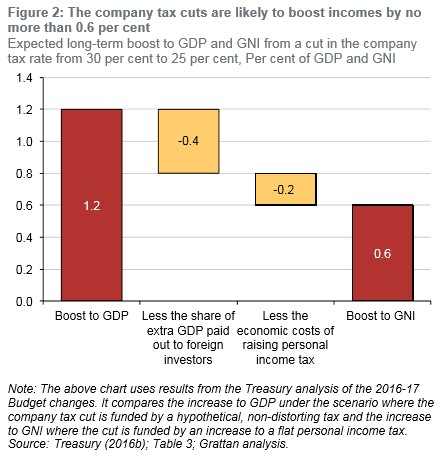

A recent Treasury research paper revised the estimates of the impact of a corporate tax cut. One headline was that in the long run – over 20 years – the cut in the company tax rate from 30 per cent to 25 per cent would increase GDP by 1.2 per cent as larger foreign companies are attracted to invest more in Australia.

Yet it is a mistake to assume that all the increase in economic activity will make Australians better off. We often use Gross Domestic Product – the sum of all economic activity – as a shorthand measure for prosperity. But when the benefits disproportionately flow to non-residents, GDP can be misleading. It’s much better to look at Gross National Income (GNI), which measures the increase in the resources available to resident Australians. A corporate tax cut increases economic activity (measured by GDP) by more than it increases national incomes (measured by GNI). When foreign-owned corporates pay less tax, more money flows out of the Australian economy. And most of the profits on their additional investments in Australia don’t benefit Australians.

Treasury estimated that cutting corporate tax rates to 25 per cent would only increase the incomes of Australians – GNI – by 0.8 per cent. Roughly a third of the benefits of greater economic growth would go to foreigners.

The story doesn’t end there. Tax cuts must be funded from elsewhere. If company taxes are lower, other taxes have to be higher, all other things being equal. And those other taxes will typically impose economic costs of their own.

In the modelling discussed so far, Treasury first assumes that the company tax cut is funded by a fantasy tax that imposes no costs on the economy.

But that’s not what happens in the real world. So the Treasury research paper also models a scenario in which the company tax cut is funded by a hypothetical flat rate personal income tax. On this more realistic assumption, Treasury estimates that GNI will increase by just 0.6 per cent in the long term, or roughly $10 billion a year in today’s dollars (Figure 2). Alternative economic modelling produced by Chris Murphy of Independent Economics reaches the same conclusion.14 The reform might still be worth doing, but it’s less of a game-changer.

Even this more modest Treasury figure may well over-estimate the long-term boost to GNI. In the real world, progressive income taxes impose higher costs than the hike to a hypothetical flat-rate personal income tax that Treasury modelled. Companies may not increase investment as much as Treasury expects, and those firms that are part of oligopolies in Australia may not increase wages by as much as Treasury assumes…

The overall economic benefit of a 0.6 per cent increase in GNI needs to be seen in context. If Australian per capita GDP and GNI increase at 1.5 per cent a year (as the budget papers routinely assume), then over 25 years, incomes will rise by 45.1 per cent. Corporate tax cuts mean that instead, incomes will rise by closer to 46 per cent. It may still be worth doing, but it’s not a plot twist that dramatically changes Australia’s story…

Inherently, a tax cut for foreign-owned companies – as the legislation effectively proposes – would reduce Australian incomes for about a decade. It would reduce government revenue – and national income – as soon as large foreign companies start to pay less tax on their existing investments. Foreigners own about 20 per cent of capital stock in the economy, so it’s a big windfall gain for them. We estimate that when a 5 percentage point tax cut for big business is first implemented, national incomes will be reduced by about 0.5 per cent, as a result of the immediate loss in company tax revenues formerly paid by foreign investors.

Advertisement

Finally, Grattan proposes an alternative to cutting company taxes that would better target investment:

There are alternatives to a full-blown company tax cut that could boost investment without delivering large windfall gains to foreign investors at such cost to the budget bottom line. Grattan Institute’s Orange Book 2016 suggests lowering effective company tax rates via investment allowances or accelerated depreciation on new investment.

An investment allowance, via a tax deduction to businesses for the purchase of new assets, would provide incentives to boost investment. Since the deduction would apply only to future investments, not past ones, it provides incentives to investment without sacrificing tax revenue on existing investment.

In the past, including at the height of the Global Financial Crisis, governments have adopted investment allowances to promote investment. In its 2015-16 Budget the Coalition included an accelerated depreciation allowance, albeit only for small businesses.31 Some argue that the unwillingness of major business groups to engage with these alternatives suggests they are less interested in the economic gains than in the windfall benefits of a tax cut.

Great report.

Advertisement

With the Federal Budget facing chronic structural pressures and a “revenue problem” – as acknowledged by Treasurer Scott Morrison in his recent speech – where is the sense in gifting tens-of-billions of dollars to foreign owners/shareholders, and in the process worsening the Budget position and lowering national income?

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.