Basically, it was an evening with George Soros as stocks fell as well. Our George was out with his bearish bets on gold and short stocks yesterday and markets followed the script to a tee. A splendid array of lightweight counter-contrarians sprayed George from Murdoch to Dumbfax but, let’s face it, when you can move markets like this MSM blather has the impact of an imperceptible breeze.

Meanwhile, my musings yesterday that it won’t be long before the Fed returns to jawbone the market down were taken up by Goldman Sachs:

Advertisement

In our “Top 10 Market Themes for 2016”, we argued that the ‘Bernanke put’ might gradually be replaced by the ‘Yellen call’. Whereas the ‘Bernanke put’ was the idea that meaningful declines in market sentiment would be met with aggressive monetary action, thus providing a buffer to downside risk, our notion of the ‘Yellen call’ was the converse. With labour markets tightening and inflation rising, we cautioned that the FOMC would likely respond to easier financial conditions with a more robust withdrawal of policy accommodation. This ‘Yellen Call’, we said, would likely ‘cap’ the upside potential for risky assets.

Such concerns were rendered moot by the sharp sell-off in in Q1. When we last revisited the theme back on 31 March, Chair Yellen had just given a very dovish speech to the Economic Club of New York (foreshadowed in speeches by FOMC members Dudley and Brainard). Chair Yellen emphasized downside risks to the US economic outlook stemming from slower global growth, and cited the FOMC’s “asymmetric” capacity to respond to economic shocks as a key reason for the FOMC’s March decision.

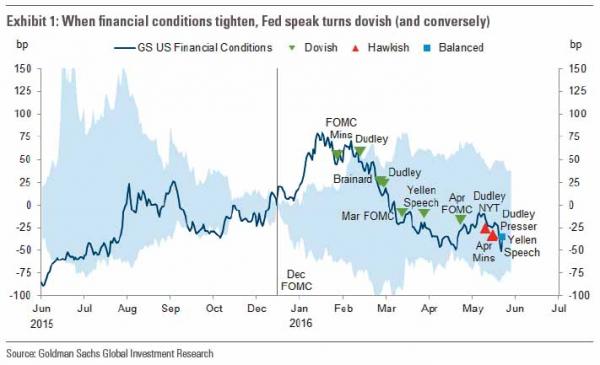

Exhibit 1 below shows how these speeches and other subsequent Fed speeches and events responded to the extreme elevation of financial conditions in early January and February. We have coded these news events as ‘dovish’, ‘hawkish’ or ‘balanced’ based on our assessment of the core message relative to market sentiment and expectations at the time. The solid line displays the GS Financial Conditions Index (GSFCI), which is our preferred measure of financial conditions (constructed as a weighted average of the 10-year rate, the trade-weighted Dollar, BBB credit spreads and equity prices). The shaded area represents the historical range of financial conditions before and after the first rate hike of the previous 4 hiking cycles (March 1988, January 1987, February 1994 and June 2004; the chart looks broadly similar if the 1988 hike is treated as part of the 1987 cycle).

We draw three conclusions from Exhibit 1. First, the magnitude of the pre-December rise in our GSFCI was somewhat unusual by the standards of historical hiking cycles. Our GSFCI increased by roughly 75bp in the six months prior to the December hike. Our rule of thumb is that a 100bp increase in the GSFCI corresponds to roughly 100- 150bp worth of hikes in the Fed funds rate, implying 4-5 hikes worth of tightening in the second half of 2015. While some of this tightening obviously anticipated the Fed’s actions, the magnitude of the tightening suggests markets were concerned about more than just rate hikes. In addition to the China and global growth concerns that were dominating headlines, we also suspect that rising balance sheet pressures, driven by a variety of factors, including regulation, may have amplified market moves by constraining the availability of ‘efficiency capital.’

Second, and further outside the range of recent historical experience, the GSFCI continued to tighten by another 75bp in the weeks following the December hike. By the time of the January FOMC meeting, it was clear that the cumulative tightening in financial conditions was far in excess of the gradual tightening that the FOMC was trying to engineer. As shown above in Exhibit 1, a series of dovish FOMC meetings and key speeches were activating the ‘Yellen put’. These dovish meetings along with a selection of key (dovish) communications from FOMC members are indicated on the chart as green triangles. As Chair Yellen put it in her speech on Monday, citing turbulent financial markets here and abroad, “… the FOMC decided at its January, March, and April meetings that it would be prudent to maintain the existing target range for the federal funds rate”. When financial conditions eventually eased to the low end of the historical range shown above, Fed speak began to turn more hawkish.

Third, the easing in the GSFCI over the past few months has more than reversed the year-to-date tightening.Financial conditions have eased back to levels that are comfortably back within the range of past hiking cycles. Indeed, Exhibit 1 shows that the GSFCI is roughly back to where it was last October, prior to the tightening that occurred in the final weeks leading up to the December meeting.

With financial conditions having significantly recovered, it is reasonable to expect that the Yellen call will soon be back in the money following the June FOMC meeting. We believe June is largely off the table given the weakness of Friday’s employment report and the UK referendum on its EU membership in June. But we think the July meeting is live, without our US Economics team seeing a 40% probability of a second hike. With equity markets posting new highs this week, we think the ‘Yellen call’ is on track to move back into the money in 2016H2.

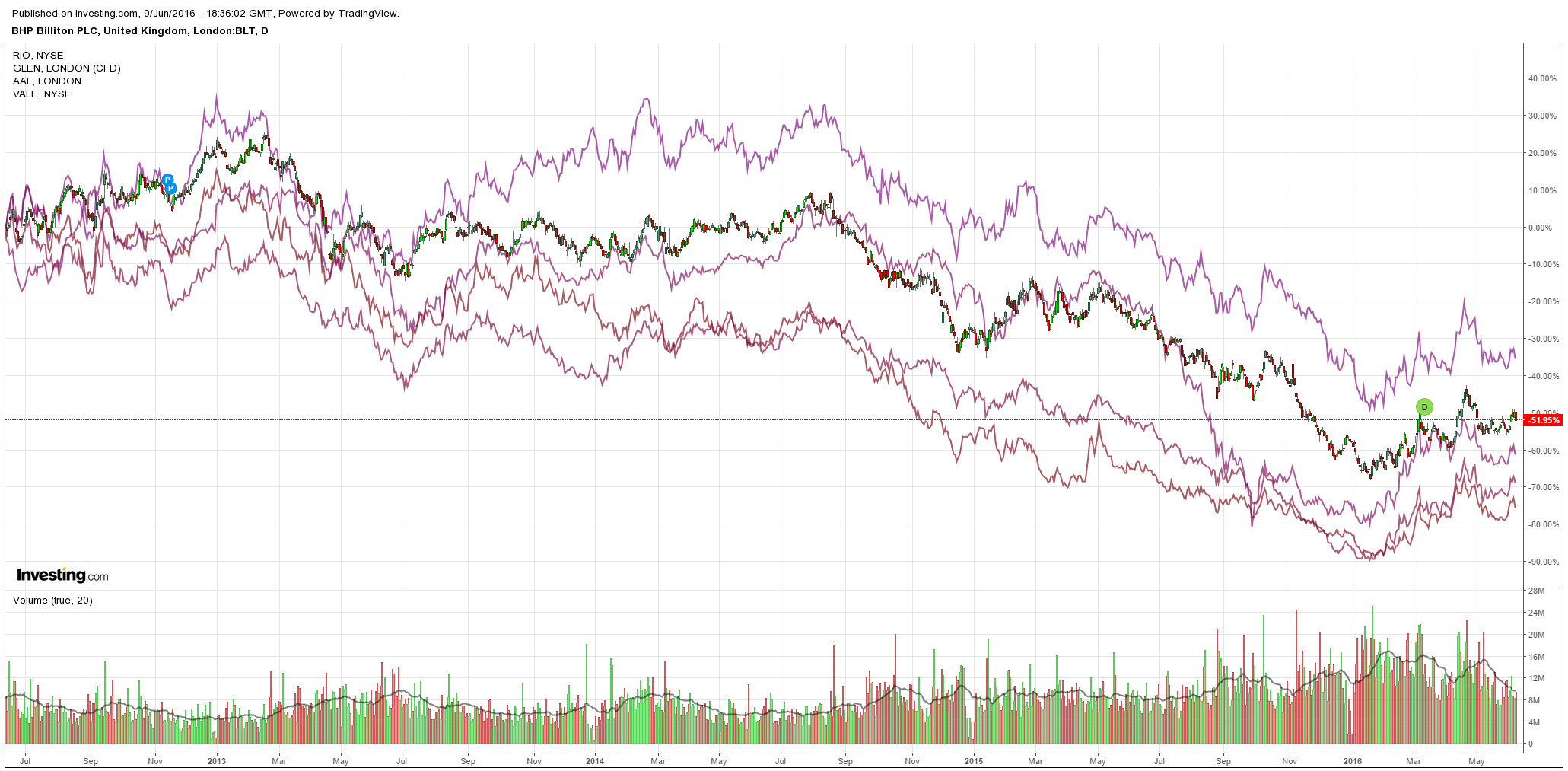

That’s right, I think. But it will very likely coincide with a slowing in Chinese growth so if the Fed does pull the trigger then it’ll have Mining GFC 2.0 upon it in a jiffy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.